Time and Purpose of Problems (Continued)

Problem 20-12 (Time 35–45 minutes)

Purpose—to provide a problem that requires preparation of a worksheet, journal entries, and indicates

financial statement presentation.

SOLUTIONS TO PROBLEMS

20–42 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

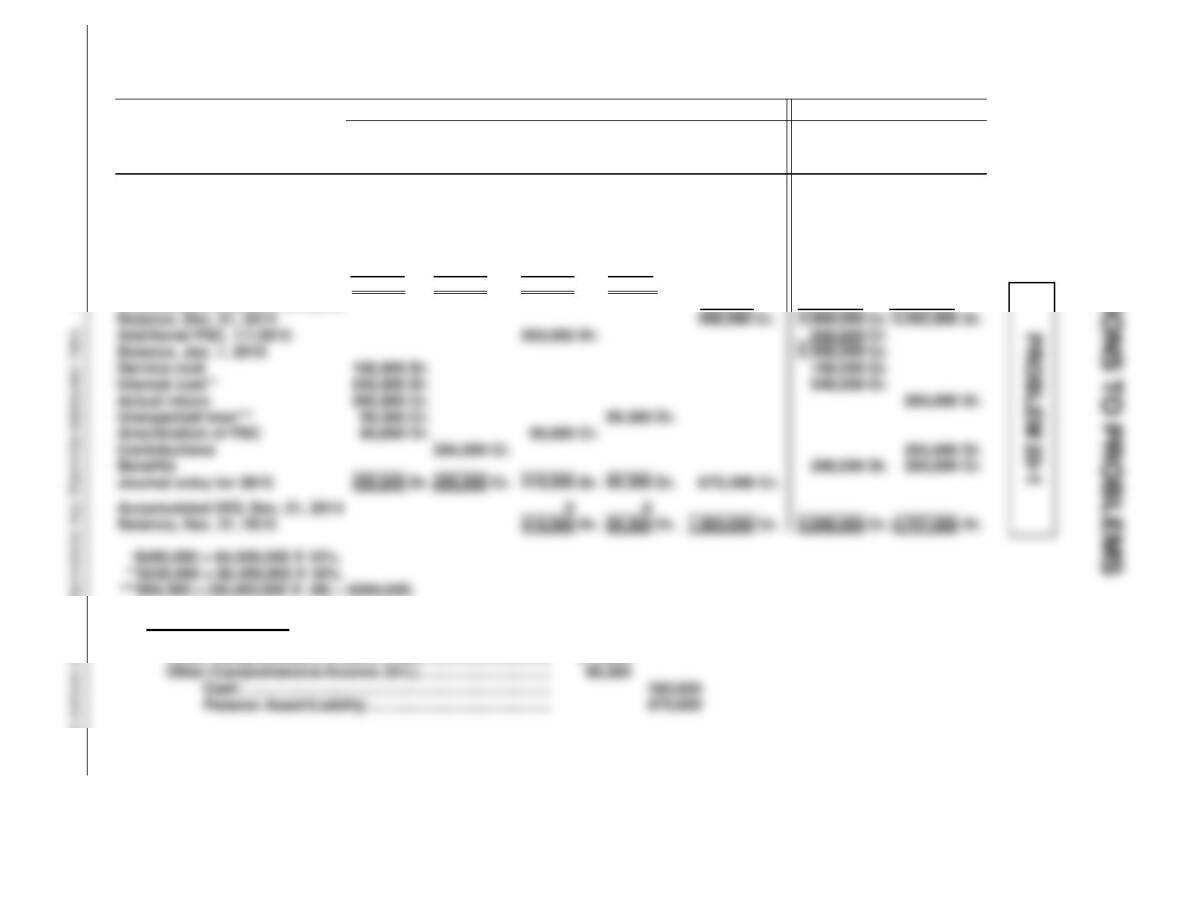

(a) HARRINGTON COMPANY

Pension Worksheet—2014 and 2015

General Journal Entries

Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—Gain/

Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

300,000 Cr.

4,500,000 Cr.

4,200,000 Dr.

Service cost

150,000 Dr.

150,000 Cr.

Interest cost*

450,000 Dr.

450,000 Cr.

Actual return

252,000 Cr.

252,000 Dr.

Contributions

240,000 Cr.

240,000 Dr.

Benefits

200,000 Dr.

200,000 Cr.

Journal entry for 2014

348,000 Dr.

240,000 Cr.

0

0

108,000 Cr.

Accumulated OCI, Dec. 31, 2013

(b) Journal Entry (2015)

Pension Expense ……………………………………………………… 450,640

Other Comprehensive Income (PSC) ………………………… 410,000

408,000 Cr.

4,900,000 Cr.

4,492,000 Dr.

Additional PSC, 1/1/2015

500,000 Cr.

Balance, Jan. 1, 2015

5,400,000 Cr.

180,000 Dr.

180,000 Cr.

Interest cost**

540,000 Dr.

540,000 Cr.

Actual return

260,000 Cr.

260,000 Dr.

99,360 Cr.

Amortization of PSC

90,000 Dr.

90,000 Cr.

Contributions

285,000 Cr.

285,000 Dr.

280,000 Dr.

280,000 Cr.

0

1,083,000 Cr.

4,757,000 Dr.

Actual return

18,000 Cr.

18,000 Dr.

Unexpected loss(b)

Contributions

16,000 Cr.

16,000 Dr.

Benefits

14,000 Dr.

14,000 Cr.

Journal entry for 2013

21,000 Dr.

16,000 Cr.

Accumulated OCI, Dec. 31, 2012

Balance, Dec. 31, 2013

2,000 Dr.

57,000 Cr.

277,000 Cr.

220,000 Dr.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 20–43

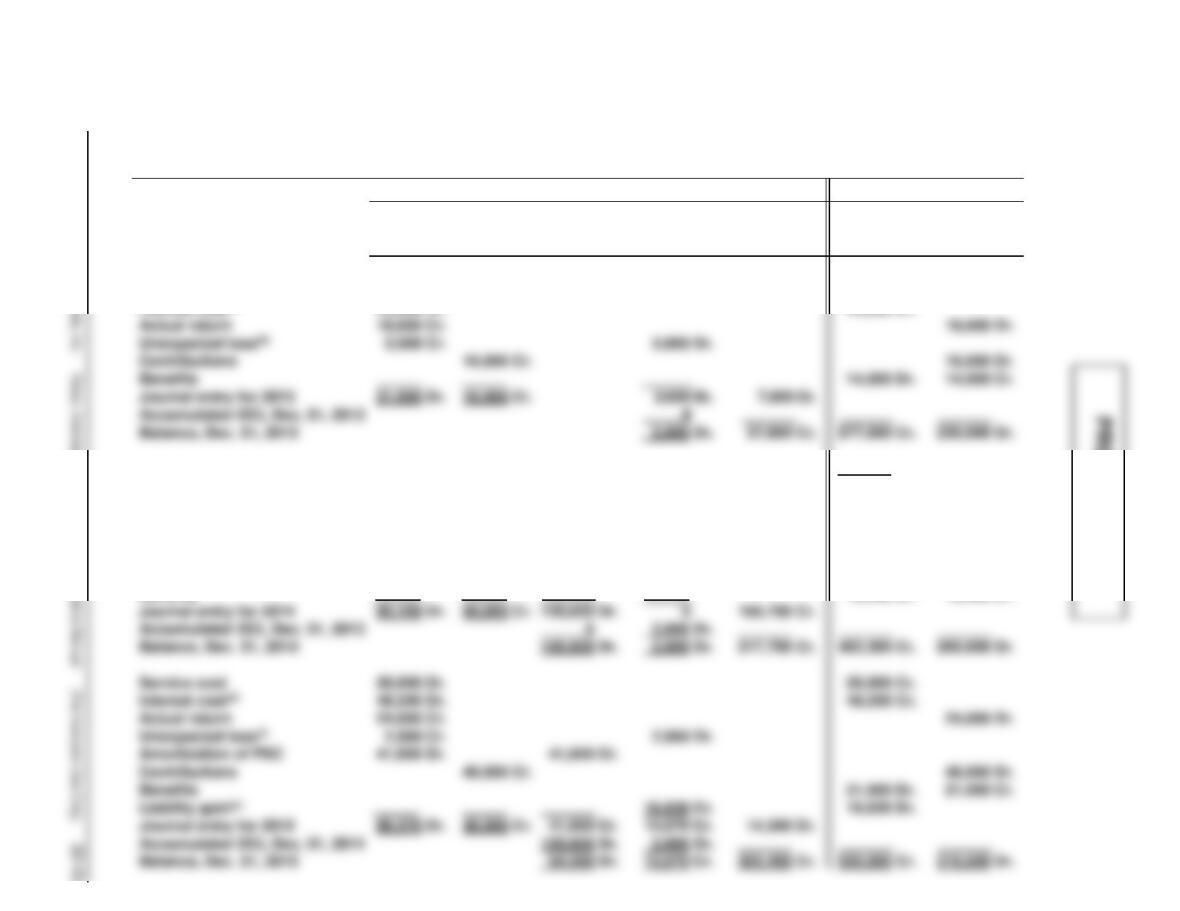

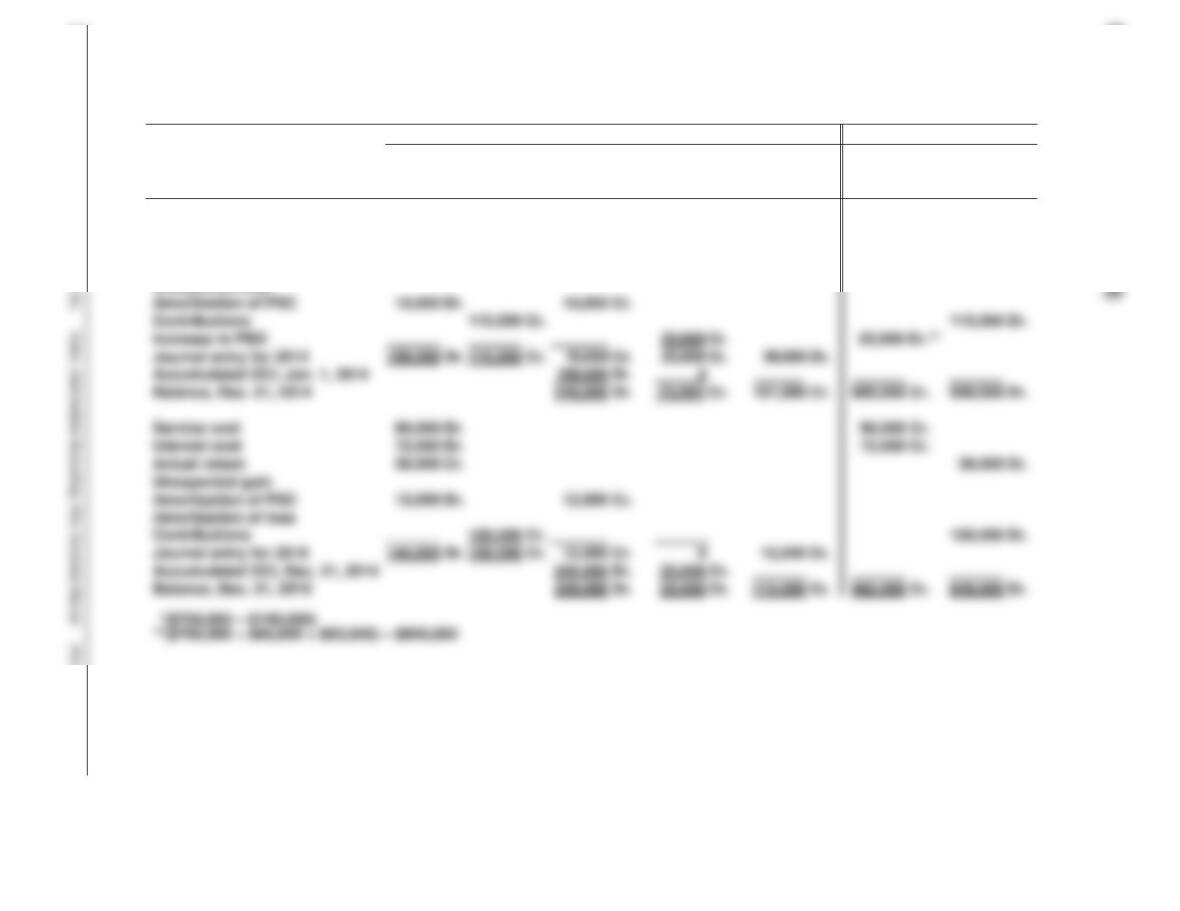

(a) JACKSON COMPANY

Pension Worksheet—2013, 2014, 2015

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2013

50,000 Cr.

250,000 Cr.

200,000 Dr.

Service cost

16,000 Dr.

16,000 Cr.

Interest cost(a)

25,000 Dr.

25,000 Cr.

Additional PSC, 1/1/2014

160,000 Dr.

160,000 Cr.

Balance, Jan. 1, 2014

437,000 Cr.

Service cost

19,000 Dr.

19,000 Cr.

Interest cost(c)

43,700 Dr.

43,700 Cr.

Actual return(d)

22,000 Cr.

22,000 Dr.

Amortization of PSC

54,400 Dr.

54,400 Cr.

Contributions

40,000 Cr.

40,000 Dr.

Benefits

16,400 Dr.

16,400 Cr.

Journal entry for 2014

95,100 Dr.

40,000 Cr.

105,600 Dr.

Accumulated OCI, Dec. 31, 2013

0

Balance, Dec. 31, 2014

105,600 Dr.

483,300 Cr.

265,600 Dr.

Service cost

26,000 Dr.

26,000 Cr.

Interest cost(e)

48,330 Dr.

48,330 Cr.

Actual return

24,000 Cr.

24,000 Dr.

Unexpected loss(f)

Contributions

48,000 Cr.

48,000 Dr.

Benefits

21,000 Dr.

21,000 Cr.

Liability gain(g)

16,630 Dr.

Journal entry for 2015

89,370 Dr.

48,000 Cr.

41,600 Cr.

14,300 Dr.

Accumulated OCI, Dec. 31, 2014

105,600 Dr.

PROBLEM 20-2 (Continued)

Worksheet computations:

(a)$25,000 = $250,000 X 10%

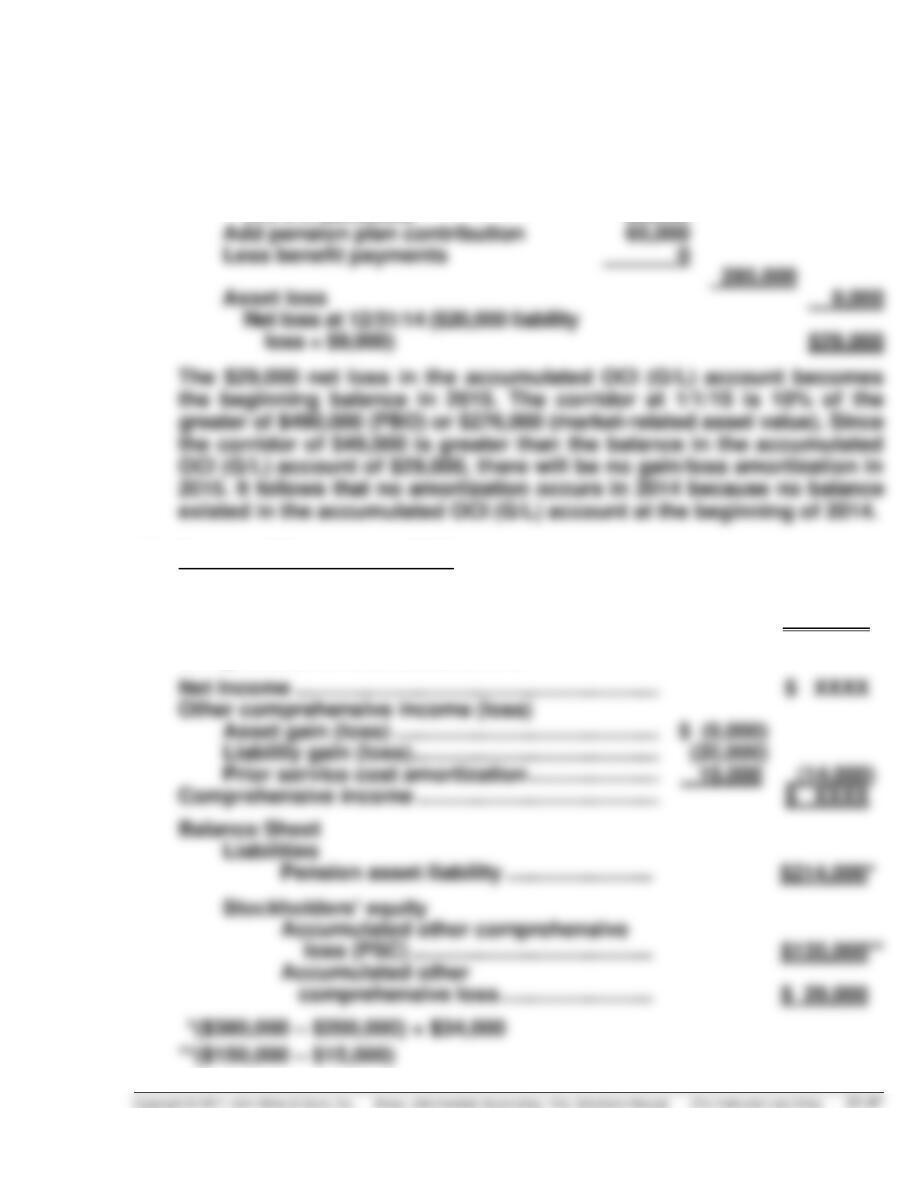

(b) Journal entries:

2013

Other Comprehensive Income (G/L) ………………….. 2,000

Pension Expense …………………………………………….. 21,000

Cash ………………………………………………………… 16,000

Pension Asset /Liability ……………………………… 7,000

PROBLEM 20-2 (Continued)

(c) Financial Statements—2015

Income Statement

Pension expense ………………………………………. $ 89,370

PROBLEM 20-3

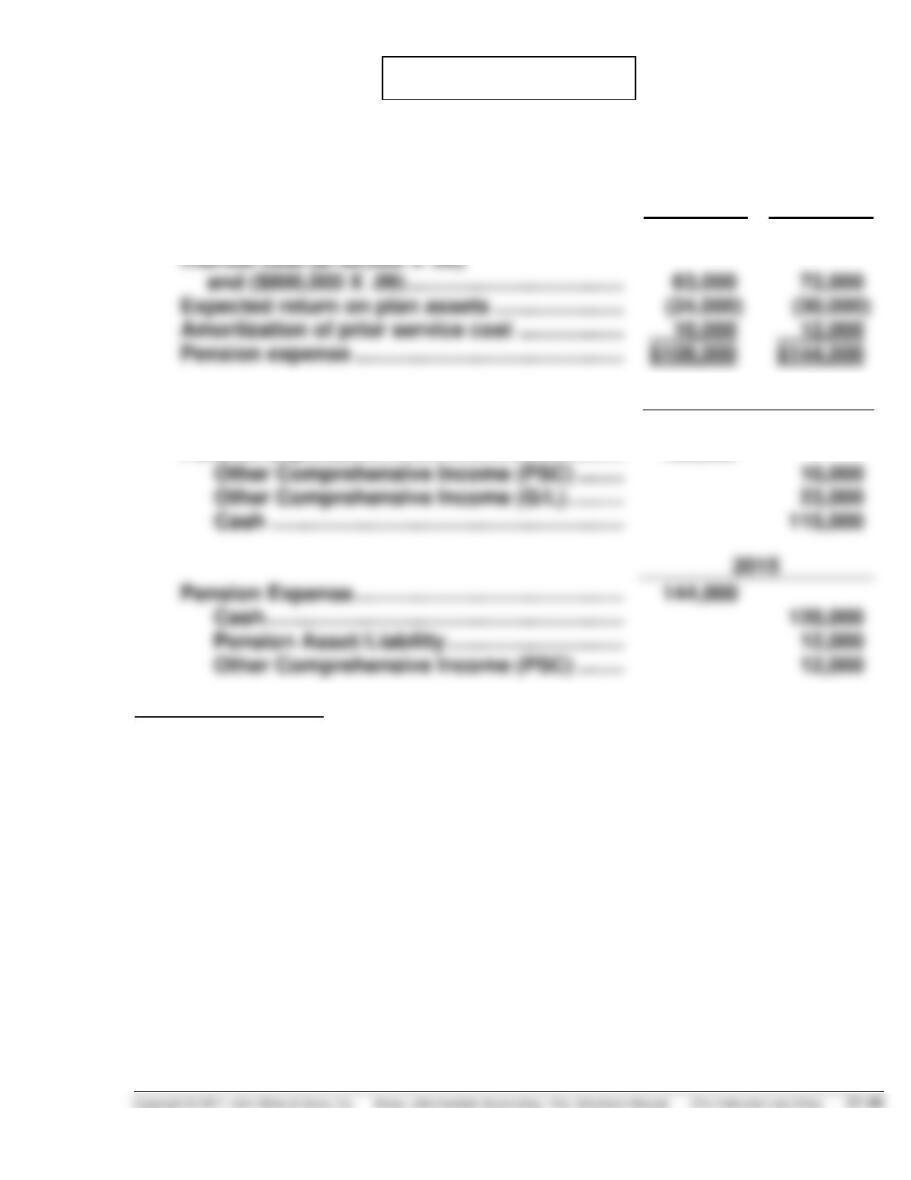

(a) Pension expense for 2014 comprises the following:

Service cost …………………………………………………… $52,000

Interest on projected benefit obligation

(b) Journal Entries—2014

Other Comprehensive Income (G/L) ………………… 29,000

(c) 2014 Increase/Decrease in Gains/Losses

(1) 12/31/14 new actuarially computed

PBO $490,000

Less: Projected benefit obligation

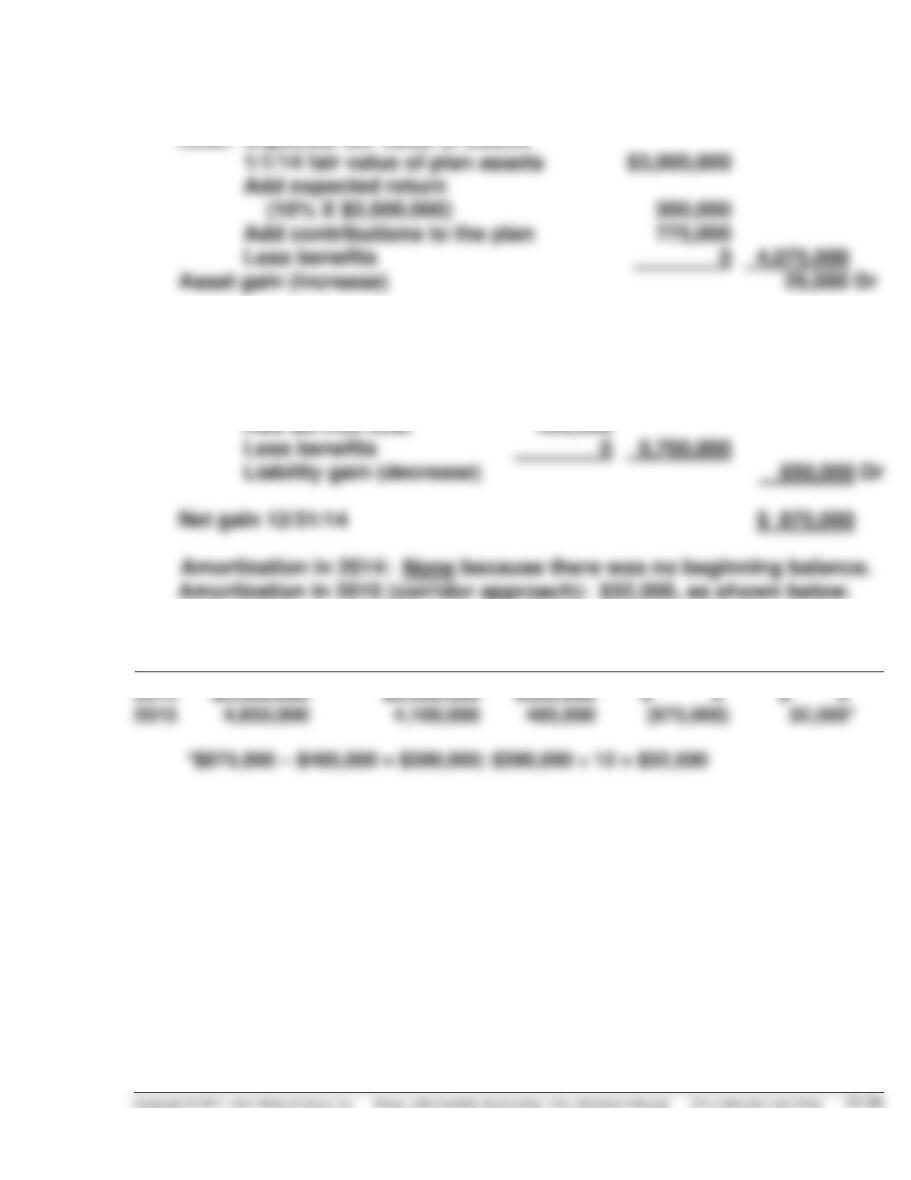

PROBLEM 20-3 (Continued)

(2) 12/31/14 fair value of plan assets $276,000

Less: Expected fair value

1/1/14 fair value of plan

assets $200,000

Add expected return

(10% X $200,000) 20,000

(d) Financial Statements—2014

Income Statement

Pension expense ……………………………………… $ 85,000

Comprehensive Income Statement

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

180,000 Cr.

380,000 Cr.

200,000 Dr.

Service cost

52,000 Dr.

52,000 Cr.

Interest cost

38,000 Dr.

38,000 Cr.

20–48 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 20-3 (Continued)

Actual return

11,000 Cr.

Unexpected loss

Liability loss

20,000 Cr.

Contributions

PSC amortization

15,000

Journal entry for 2014

85,000

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

490,000 Cr.

276,000 Dr.

PROBLEM 20-4

(a) Computation of pension expense:

2014

2015

Service cost ………………………………………………

($ 60,000

$ 90,000

Expected return on plan assets ………………….

Amortization of prior service cost ………………

12,000

Pension expense ……………………………………….

(b)

2014

Pension Asset/Liability ………………………………

(39,000

Pension Expense ……………………………………….

109,000

Other Comprehensive Income (PSC) ……..

Other Comprehensive Income (G/L)……….

Cash ……………………………………………………

Note to instructors: Although not required, students could be encouraged

to prepare a 2-year pension worksheet, as shown on the following page.

20–50 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

140,000 Cr.

700,000 Cr.

560,000 Dr.*

Service cost

60,000 Dr.

60,000 Cr.

Interest cost

63,000 Dr.

63,000 Cr.

Actual return

24,000 Cr.

24,000 Dr.

Unexpected loss

Amortization of PSC

10,000 Dr.

10,000 Cr.

Contributions

115,000 Cr.

Increase in PBO

23,000 Dr.**

Journal entry for 2014

115,000 Cr.

Accumulated OCI, Jan. 1, 2014

Balance, Dec. 31, 2014

800,000 Cr.

Service cost

90,000 Dr.

90,000 Cr.

Interest cost

72,000 Dr.

72,000 Cr.

Actual return

30,000 Cr.

30,000 Dr.

Unexpected gain

Amortization of PSC

12,000 Dr.

12,000 Cr.

Amortization of loss

Contributions

120,000 Cr.

Journal entry for 2015

120,000 Cr.

12,000 Cr.

12,000 Cr.

Accumulated OCI, Dec. 31, 2014

23,000 Cr.

Balance, Dec. 31, 2015

23,000 Cr.

962,000 Cr.

PROBLEM 20-5

(a) Pension expense for 2014 consisted only of the service cost component

amounting to $60,000. There were no prior service cost, net gain or loss,

plan assets, or projected benefit obligation as of January 1, 2014.

Pension expense for 2015 comprised the following:

PROBLEM 20-5 (Continued)

(1)

Year

Projected

Benefit

Obligation (a)

Plan Assets

(a)

Corridor

(b)

Accumulated

OCI (G/L) (a)

Minimum

Amortization

of (Gain) Loss

2014

$ 0

$ 0

$ 0

$( 0

$( 0

(b) Journal Entries—2014

Pension Expense …………………………………………….. 60,000

Cash ………………………………………………………… 50,000

Pension Asset /Liability …………………………..…. 10,000

Journal Entries—2015

Pension Asset /Liability …………………………..…. 105,000

Journal Entries—2016

Pension Expense ……………………………………………… 131,367

PROBLEM 20-5 (Continued)

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 20–53

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

Service cost

60,000 Dr.

60,000 Cr.

Interest cost

Expected return

Contributions

50,000 Dr.

Journal entry for 2014

60,000 Dr.

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

60,000 Cr.

50,000 Dr.

Service cost

85,000 Dr.

85,000 Cr.

Interest cost

6,600 Dr.

6,600 Cr.

Actual return

5,000 Cr.

5,000 Dr.

Contributions

60,000 Cr.

60,000 Dr.

Increase in liability

78,400 Dr.

78,400 Cr.

Benefits

30,000 Dr.

30,000 Cr.

Journal entry for 2015

86,600 Dr.

60,000 Cr.

78,400 Dr.

105,000 Cr.

Accumulated OCI, Dec. 31, 2014

0

Balance, Dec. 31, 2015

78,400 Dr.

200,000 Cr.

85,000 Dr.

Service cost

119,000 Dr.

119,000 Cr.

Interest cost

16,000 Dr.

16,000 Cr.

Amortization of loss

4,867 Dr.

Contributions

105,000 Cr.

105,000 Dr.

Benefits

18,500 Dr.

18,500 Cr.

Liability loss*

7,500 Cr.

Journal entry for 2016

131,367 Dr.

105,000 Cr.

Accumulated OCI, Dec. 31, 2015

78,400 Dr.

Balance, Dec. 31, 2016

81,033 Dr.

324,000 Cr.

180,000 Dr.

PROBLEM 20-6

(a) Prior Service Cost Amortization

2014

$166,667

($2,000,000 ÷ 12 years)

2015

166,667

($2,000,000 ÷ 12 years)

2016

166,667

($2,000,000 ÷ 12 years)

(b) Pension expense for 2014 comprised the following:

Service cost ……………………………………………………………… $200,000

Interest on projected benefit obligation* …………………….. 500,000

(c) Pension liability, beginning of year …………………………... $2,000,000

Journal Entries—2014

Pension Expense ………………………………………….. 566,667

Pension Asset /Liability …………………………………. 1,250,000

PROBLEM 20-6 (Continued)

(d) 12/31/14 Fair value of plan assets $4,100,000

Less: Expected fair value of assets

12/31/14 Actuarially computed PBO 4,850,000

Less: 1/1/14 PBO $5,000,000

Add interest

(10% X $5,000,000) 500,000

Year

Projected Benefit

Obligation

Fair Value

of Plan Assets

Corridor

Accumulated

OCI (G/L)

Amortization

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

2,000,000 Cr.

5,000,000 Cr.

3,000,000 Dr.

Service cost

200,000 Dr.

200,000 Cr.

20–56 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 20-6 (Continued)

Interest cost*

500,000 Dr.

500,000 Cr.

Actual return

Unexpected gain

25,000 Cr.

Amortization of PSC

166,667 Dr.

Contributions

Decrease in PBO

850,000 Cr.

850,000 Dr.

Journal entry for 2014

566,667 Dr.

875,000 Cr.

1,250,000 Dr.

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

875,000 Cr.

4,850,000 Cr.

4,100,000 Dr.

Actual return

48,000 Cr.

48,000 Dr.

Unexpected loss**

4,000 Dr.

Amortization of PSC

25,000 Dr.

25,000 Cr.

Amortization of loss***

2,100 Cr.

Contributions

133,000 Dr.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 20–57

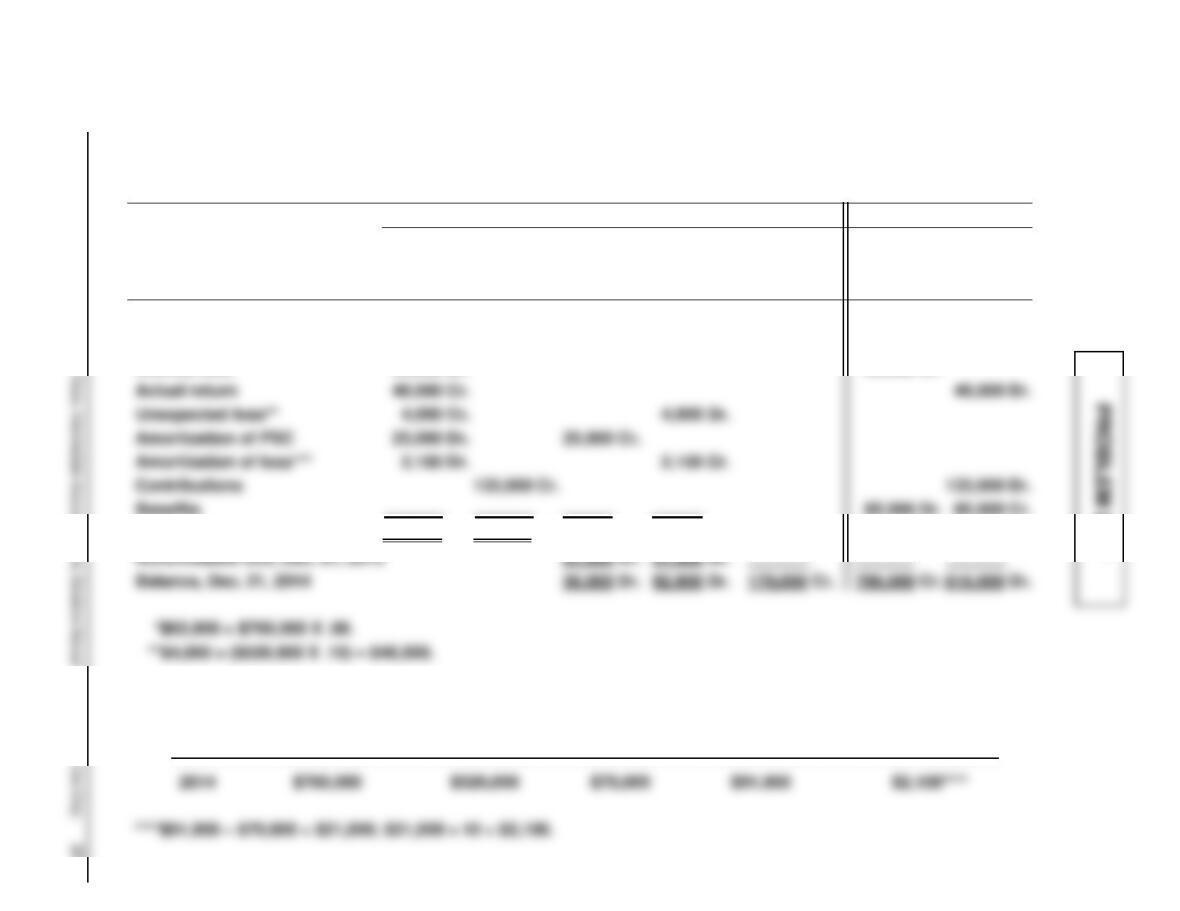

HANSON CORP.

Pension Worksheet—2014

General Journal Entries Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

180,000 Cr.

700,000 Cr.

520,000 Dr.

Service cost

108,000 Dr.

108,000 Cr.

Interest cost*

63,000 Dr.

63,000 Cr.

Benefits

85,000 Dr.

85,000 Cr.

Journal entry for 2014

146,100 Dr.

133,000 Cr.

25,000 Cr.

1,900 Dr.

10,000 Dr.

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

56,000 Dr.

92,900 Dr.

170,000 Cr.

786,000 Cr.

616,000 Dr.

***

Year

1/1 Projected

Benefit

Obligation

Value of 1/1

Plan Assets

10%

Corridor

Accumulated

OCI (G/L), 1/1

Minimum

Amortization of

Loss for 2012

PROBLEM 20-8

(a) LEMKE COMPANY

Pension Worksheet—2014 and 2015

General Journal Entries Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/

Liability

Projected

Benefit

Obligation

Plan Assets

Balance, Jan. 1, 2014

190,000 Cr.

600,000 Cr.

410,000 Dr.

Service cost

40,000 Dr.

40,000 Cr.

Interest cost(a)

60,000 Dr.

60,000 Cr.

Actual return

36,000 Cr.

36,000 Dr.

Unexpected loss(b)

5,000 Cr.

5,000 Dr.

20–58 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

Amortization of PSC

70,000 Dr.

70,000 Cr.

Contributions

97,000 Dr.

Benefits

31,500 Dr.

31,500 Cr.

Increase in PBO

87,000 Cr.

Journal entry for 2014

70,000 Cr.

Accumulated OCI, Dec. 31, 2013

0

Balance, Dec. 31, 2014

244,000 Cr.

755,500 Cr.

511,500 Dr.

Service cost

59,000 Dr.

59,000 Cr.

Interest cost(c)

75,550 Dr.

75,550 Cr.

Actual return

61,000 Cr.

61,000 Dr.

Unexpected gain(d)

9,850 Dr.

9,850 Cr.

Amortization of PSC

50,000 Dr.

50,000 Cr.

Amortization of loss(e)

Contributions

81,000 Dr.

Benefits

54,000 Dr.

54,000 Cr.

Accumulated OCI, Dec. 31, 2014

Balance, Dec. 31, 2015

236,550 Cr.

836,050 Cr.

599,500 Dr.

PROBLEM 20-8 (Continued)

Worksheet computations:

(a)$60,000 = $600,000 X 10%.

(b) 2014

Pension Expense ………………………………………………. 129,000

Other Comprehensive Income (G/L) ……………………. 92,000

Cash ………………………………………………………….. 97,000

Pension Asset /Liability ……………………………….. 54,000

Other Comprehensive Income (PSC) ……………. 70,000

PROBLEM 20-8 (Continued)

(c) Financial Statements—2015

Income Statement

Pension expense …………………………..………… $134,223

Comprehensive Income Statement