FINANCIAL STATEMENT ANALYSIS CASE 3 (Continued)

Note to Instructor: Although the analysis below is for 2005 – 2007,

this analysis is particularly useful as Circuit City subsequently filed

for bankruptcy.

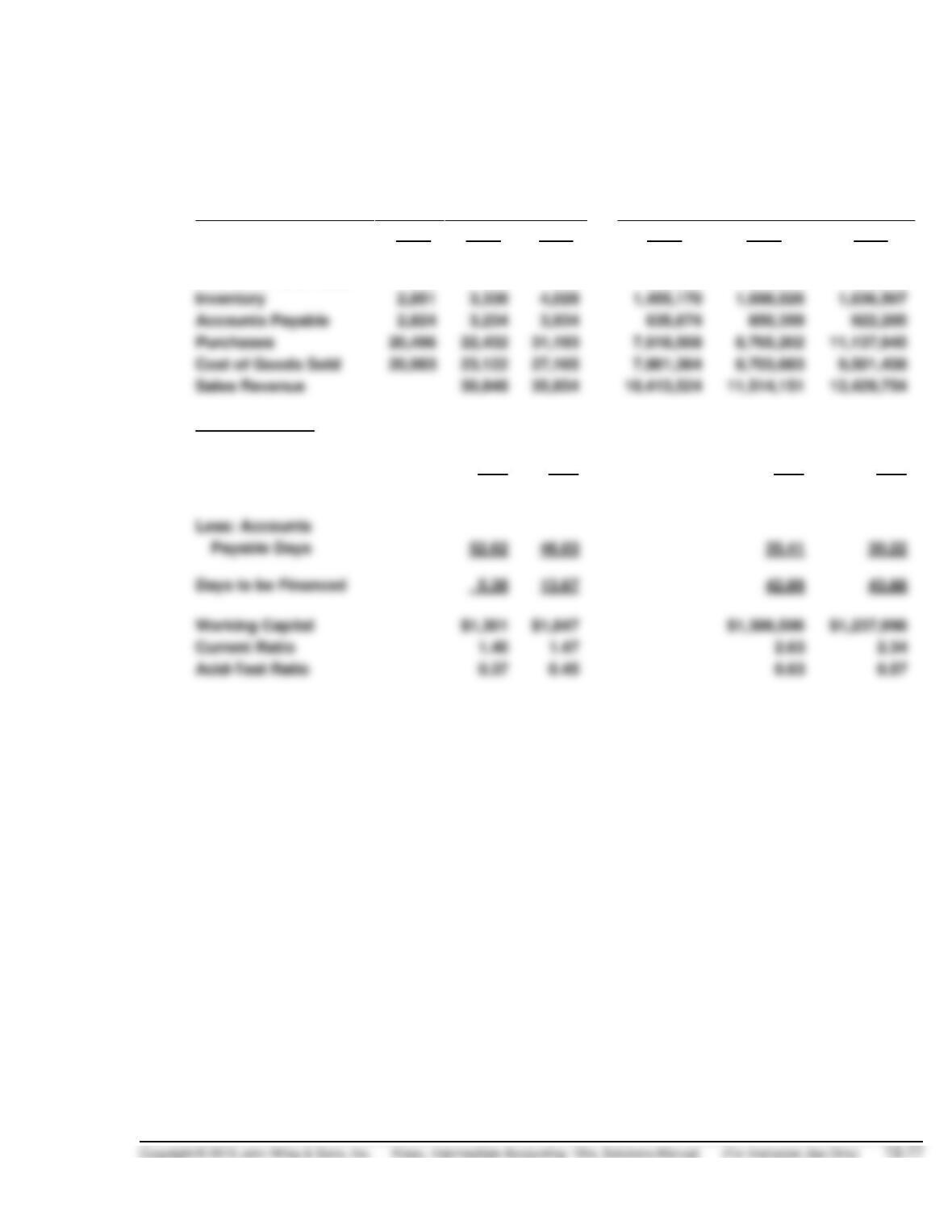

Best Buy (in millions)

Circuit City (in thousands)

2005

2006

2007

2005

2006

2007

Cash

$ 470

$748

1,205

879,660

315,970

141,141

Accounts Receivable

375

449

548

230,605

222,869

382,555

Inventory

2,851

4,028

Accounts Payable

2,824

3,934

635,674

850,359

922,205

Purchases

Cost of Goods Sold

Sales Revenue

Operating Cycle

Receivable Days

5.3

5.6

7.1

11.2

Inventory Days

52.7

54.1

71.2

62.9

Operating Cycle

58.0

59.7

78.3

74.1

Days to be Financed

13.67

Working Capital

Current Ratio

1.40

1.47

2.63

2.34

Acid-Test Ratio

0.37

0.45

0.63

0.57

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

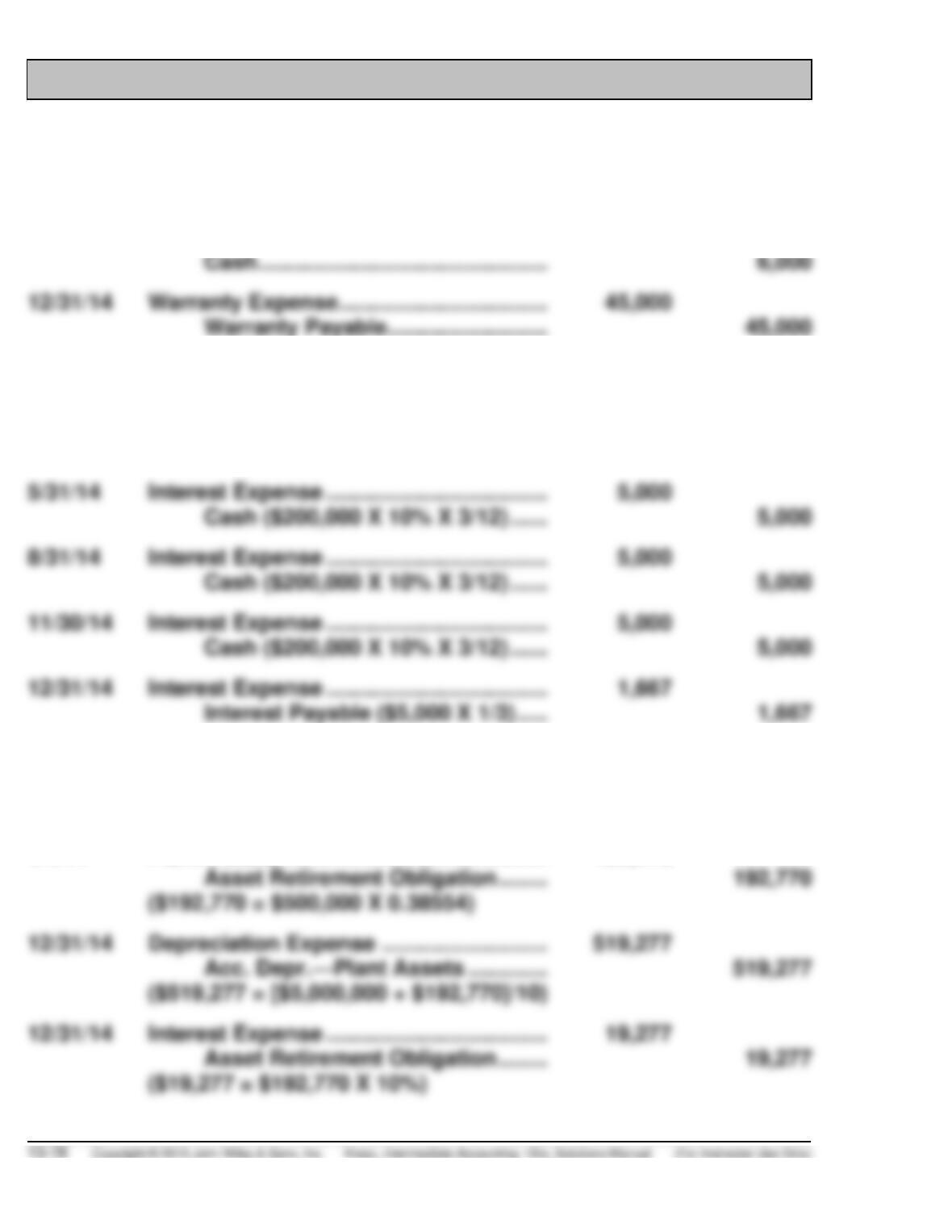

(1)

During 2014

Warranty Expense ……………………………………..

6,000

Cash …………………………………………………

12/31/14

Warranty Expense ……………………………………..

Warranty Payable …………………………..

(2)

2/28/14

Interest Expense ($5,000 X 2/3) …………………..

3,333

Interest Payable ($5,000 X 1/3) ……………………

1,667

Cash ($200,000 X 10% X 3/12) …………….

5,000

5/31/14

Interest Expense ……………………………………….

5,000

Cash ($200,000 X 10% X 3/12) …………….

5,000

8/31/14

Interest Expense ……………………………………….

5,000

Cash ($200,000 X 10% X 3/12) …………….

5,000

11/30/14

Interest Expense ……………………………………….

5,000

Cash ($200,000 X 10% X 3/12) …………….

5,000

12/31/14

Interest Expense ……………………………………….

1,667

Interest Payable ($5,000 X 1/3) ……………

1,667

(3)

1/1/14

Plant Assets ……………………………………………..

5,000,000

Cash …………………………………………………

5,000,000

1/1/14

Plant Assets ……………………………………………..

192,770

Asset Retirement Obligation ………………

12/31/14

Depreciation Expense …………………………..

519,277

Acc. Depr.—Plant Assets …………………..

($519,277 = [$5,000,000 + $192,770]/10)

12/31/14

Interest Expense ……………………………………….

Asset Retirement Obligation ………………

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Analysis

The warranty payable and the interest payable are current liabilities, so all

else equal, these will decrease both the current and acid-test ratios.

Because of the commitment letter from First Trust Corp., the $200,000 loan

Principles

According to FASB Concepts Statement No. 6, liabilities are probable

future sacrifices of economic benefits arising from present obligations of a

particular entity to transfer assets or provide services to other entities in

the future as a result of past transactions or events. With respect to the

new warranty plan, YellowCard would be currently obligated to provide

PROFESSIONAL RESEARCH

(a) FASB ASC 605-20-25 addresses how revenue and costs from a

separately priced extended warranty or product maintenance contract

should be recognized.

(b) An Extended Warranty is an agreement to provide warranty protection

Product Maintenance Contracts are agreements to perform certain

agreed-upon services to maintain a product for a specified period of

time. The terms of the contract may take different forms, such as an

agreement to periodically perform a particular service a specified

number of times over a specified period of time, or an agreement to

(c) Costs that are directly related to the acquisition of a contract and that

would have not been incurred but for the acquisition of that contract

(incremental direct acquisition costs) shall be deferred and charged to

PROFESSIONAL SIMULATION

Note: This assignment is available on the Kieso website.

Journal Entries

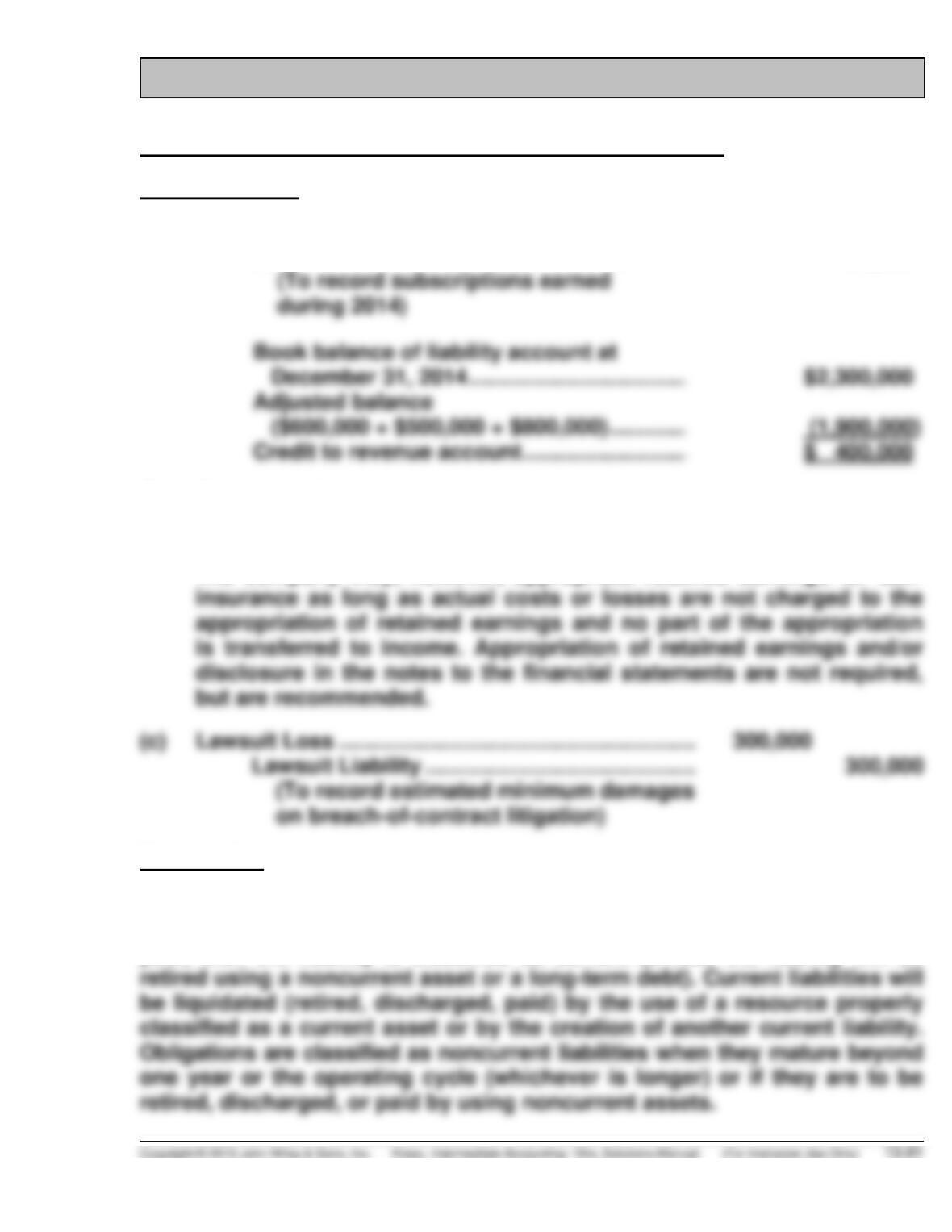

(a)

Unearned Sales Revenue ………………………………………..

400,000

Sales Revenue ……………………………………………….

400,000

(To record subscriptions earned

during 2014)

Adjusted balance

($600,000 + $500,000 + $800,000) …………………..

(b) No entry should be made to accrue for an expense, because the

absence of insurance coverage does not mean that an asset has been

impaired or a liability has been incurred as of the balance sheet date.

The company may, however, appropriate retained earnings for self–

Explanation

If a liability is scheduled to mature within one year after the date of an enter–

prise’s balance sheet or within an operating cycle that is longer than one

year, then the liability is classified as current (unless the liability will be

PROFESSIONAL SIMULATION (Continued)

Generally all three of these liabilities (accounts payable, notes payable,

bonds payable) would be classified as current liabilities on the company’s

balance sheet prepared as of December 31, 2014.

However, the bonds payable, and possibly the notes payable, could be clas-

sified as noncurrent liabilities if the company intends to refinance the obli–

gations on a long–term basis and the company’s intent to refinance the

IFRS CONCEPTS AND APPLICATION

IFRS13-1

A company should exclude a short-term obligation from current liabilities

IFRS13-2

The ability to defer settlement of short-term debt may be demonstrated by

IFRS13-3

A provision is defined as a liability of uncertain timing or amount and is

IFRS13-4

A provision should be recorded and a charge accrued to expense only if:

(a) the company has a present obligation (constructive or legal) as

a result of a past event,

IFRS13-5

A current liability such as accounts payable is susceptible to precise

measurement because the date of payment, the payee, and the amount of

IFRS13-6

Onerous contracts are ones in which the unavoidable costs of meeting the

obligations exceed the economic benefits expected to be received.

IFRS13-7

ALEXANDER COMPANY

Partial Statement of Financial Position

December 31, 2014

Current liabilities:

Notes payable (Note 1)……….……………….……………………………. $300,000

NOTE 1:

Short-term debt refinanced. As of December 31, 2014, the company had

IFRS13-8

(1) Mckee should classify $100,000 of the obligation as a current maturity

of long-term debt (current liability) and the $300,000 balance as a

noncurrent liability.

(2) While the maturity of the obligation was extended to February 15,

IFRS13-9

1.

Warranty Expense ……………………………………..

5,000,000*

Warranty Payable ………………………………

5,000,000

* Expected warranty costs:

%

Units

Costs per Unit

Total Costs

No defects

Minor defects

2.

Income Tax Expense ………………………………….

400,000

Income Taxes Payable ……………………….

400,000

IFRS13–10

(a) No. IFRS indicate that refinancing a short-term obligation on a long-

IFRS13-10 (Continued)

(b) No. The events described will not have an impact on the financial

statements. Since Kobayashi Corporation’s refinancing of the long–

term debt maturing in March 2015 does not meet the conditions set

(c) Yes. The debt should be included in current liabilities. The issuance

IFRS13–11

(a) IAS 37, Provisions, Contingent Liabilities and Contingent Assets.

(b) Recognizing a liability from restructuring (IAS 37, 72 – 79).

A constructive obligation to restructure arises only when an entity:

(a) has a detailed formal plan for the restructuring identifying at

least: (i) the business or part of a business concerned; (ii) the

IFRS13-11 (Continued)

Evidence that an entity has started to implement a restructuring plan

would be provided, for example, by dismantling plant or selling assets

or by the public announcement of the main features of the plan. A

For a plan to be sufficient to give rise to a constructive obligation

when communicated to those affected by it, its implementation needs

to be planned to begin as soon as possible and to be completed in a

A management or board decision to restructure taken before the end

of the reporting period does not give rise to a constructive obligation

at the end of the reporting period unless the entity has, before the end

of the reporting period: (a) started to implement the restructuring

plan; or (b) announced the main features of the restructuring plan to

IFRS13-11 (Continued)

Although a constructive obligation is not created solely by a manage-

ment decision, an obligation may result from other earlier events

together with such a decision. For example, negotiations with employee

In some countries, the ultimate authority is vested in a board whose

membership includes representatives of interests other than those of

management (e.g. employees) or notification to such representatives

Even when an entity has taken a decision to sell an operation and

announced that decision publicly, it cannot be committed to the sale

until a purchaser has been identified and there is a binding sale

agreement. Until there is a binding sale agreement, the entity will be

Costs to include (IAS 37, 80)

A restructuring provision shall include only the direct expenditures

IFRS13-11 (Continued)

Costs to exclude (IAS 37, 81 – 82)

A restructuring provision does not include such costs as: (a) retraining

or relocating continuing staff; (b) marketing; or (c) investment in new

systems and distribution networks. These expenditures relate to the

As required by paragraph 51, gains on the expected disposal of assets

are not taken into account in measuring a restructuring provision,

even if the sale of assets is envisaged as part of the restructuring.

(c) The current warranty contract is considered an onerous contract. The

required accounting related to an onerous contract is in IAS 37, 81 – 82.

If an entity has a contract that is onerous, the present obligation

This Standard defines an onerous contract as a contract in which the

unavoidable costs of meeting the obligations under the contract

exceed the economic benefits expected to be received under it. The

IFRS13-11 (Continued)

Before a separate provision for an onerous contract is established, an

IFRS13–12

(a) M&S’s short-term borrowings were £327.7 million at 31 March, 2012.

SHORT-TERM DEBT

(In millions)

2012

Bank loans and overdrafts

£ 38.4

Medium term notes

Total short-term debt

(b) 1. Working capital = Current assets less current liabilities.

IFRS13-12 (Continued)

3.

Current ratio =

Current assets

Current liabilities

M&S’s acid-test ratio is at 0.54, and working capital and the current

ratio appear acceptable. The lower acid-test ratio may not be a

problem. Many large companies carry relatively high levels of

(c) M&S provided the following discussion related to commitments and

contingencies:

25 Contingencies and commitments

B. Other material contracts

In the event of a material change in the trading arrangements with

certain warehouse operators, the Group has a commitment to

IFRS13-12 (Continued)

C. Commitments under operating leases

The Group leases various stores, offices, warehouses and equipment

under non-cancellable operating lease agreements. The leases have

varying terms, escalation clauses and renewal rights

2012 2011

£m £m

Total future minimum rentals payable under

non-cancellable operating leases are as follows:

Within one year 257.8 242.6

The total future sublease payments to be received are £63.3m (last

year £65.8m)