COMPARATIVE ANALYSIS CASE

THE COCA-COLA COMPANY and PEPSICO, INC.

(a)

Coca-Cola

PepsiCo

(1)

Cash used in investing activities

$(2,524)

$(5,618)

(2)

Cash used for acquisitions and

investments

$ (977)

$(3,193)

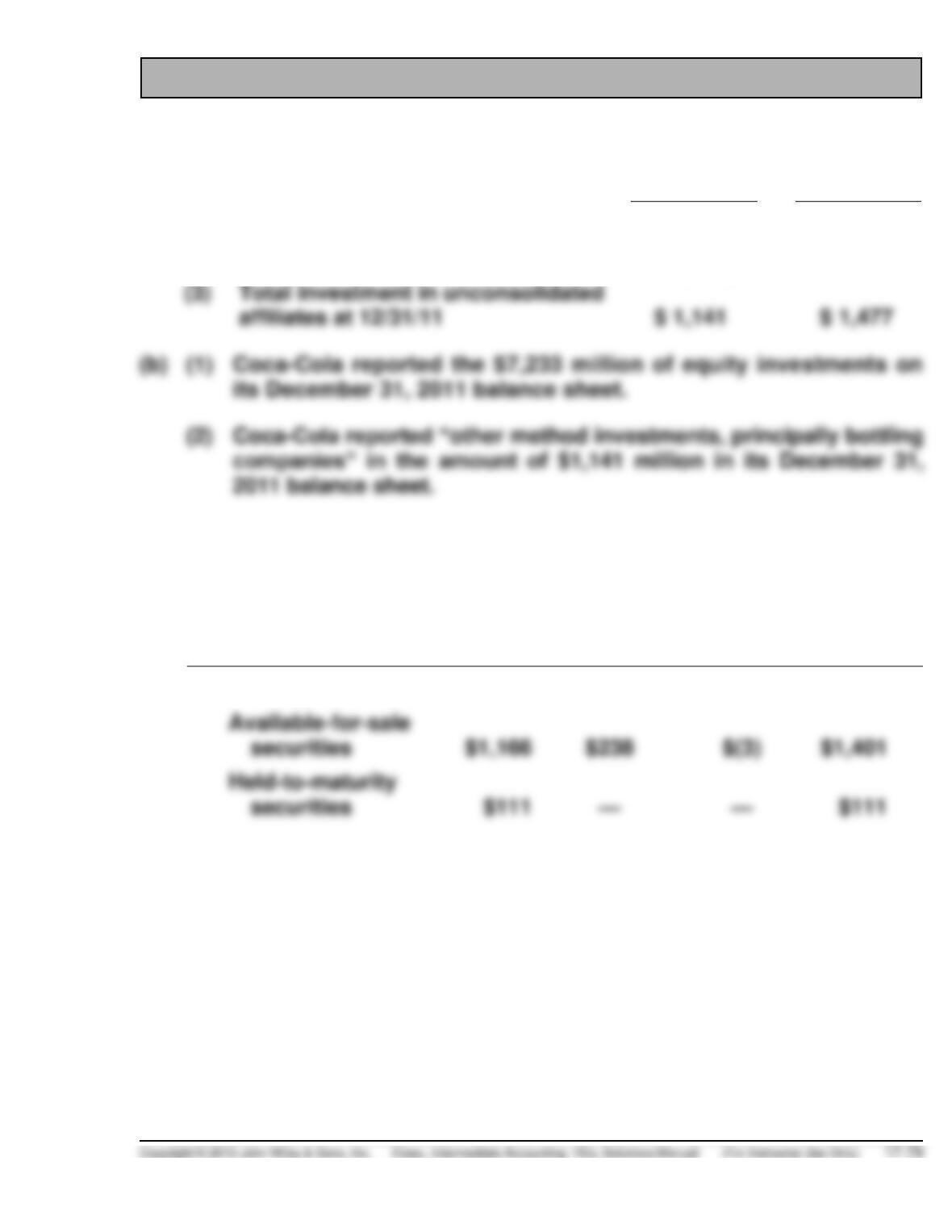

(c) At December 31, 2011, Coca-Cola reported in its Note 3 on Investments

the following:

December 31, 2011

(in millions)

Cost

Gross

Unrealized

Gains

Gross

Unrealized

Losses

Estimated

Fair Value

Trading securities

$211

FINANCIAL STATEMENT ANALYSIS CASE

UNION PLANTERS

(a) While banks are primarily in the business of lending money, they also

need to balance their asset portfolio by investing in other assets. For

(b) Trading securities are shown on the balance sheet at current fair value,

and any unrealized gains and losses resulting from reporting them at

fair value are reported as part of income. Available-for-sale securities

(c) Securities are reported in three different categories because these three

different categories reflect the likelihood that any unrealized gains and

losses will eventually be realized by the company. That is, trading

FINANCIAL STATEMENT ANALYSIS CASE (Continued)

(d) The answer to this involves selling your “winner” stocks in your available–

for-sale portfolio at year-end. Union Planters could have increased

reported net income by $108 million (clearly, a material amount when

total reported income was $224 million). Management chose not to sell

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

(a) Instar’s investment in Dorsel Corp. bonds should be classified as

held-to-maturity because they have a specific maturity date and Instar

has the intent and ability to hold them until the maturity date.

Instar’s investment of idle cash in equity securities should be

classified as trading.

Instar’s investment in its supplier should be classified as an available–

for-sale security. Instar does not intend to sell it in the short term and

(b)

Fair Value Adjustment (trading) …………………………..

120,000

Unrealized Holding Gain or Loss—Income …..

120,000

(To record the increase in value of the

trading securities, $920,000 – $800,000)

Fair Value Adjustment (available-for-sale) ……………

350,000

Unrealized Holding Gain or Loss—Equity …….

350,000

Loss on Impairment ……………………………………………

150,000

Equity Investments (available-for-sale) ………..

150,000

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Equity Investments (Slobbaer) …………………………….

75,000

Investment Income ……………………………………..

75,000

Equity Investments (Slobbaer) …………………….

25,000

Analysis

The total effect on net income is $120,000 – $150,000 + $75,000 = $45,000.

Note that the gain on the available-for-sale securities is a component of

Principles

The rationale for reporting held-to-maturity securities at amortized cost is

that if management intends to hold the securities to maturity, fair values

PROFESSIONAL RESEARCH

(a) According to FASB ASC 320–10:

15-5 The guidance in the Investments—Debt and Equity Securities

Topic establishes standards of financial accounting and report-

ing for both of the following:

An equity security has a readily determinable fair value if it meets any

of the following conditions:

a. The fair value of an equity security is readily determinable if sales

prices or bid-and-asked quotations are currently available on a

securities exchange registered with the U.S. Securities and

b. The fair value of an equity security traded only in a foreign market

is readily determinable if that foreign market is of a breadth and

PROFESSIONAL RESEARCH (Continued)

(b) See FASB ASC 320-10–35

35–18 For individual securities classified as either available for sale or

held to maturity, an entity shall determine whether a decline in

35–30 If the fair value of an investment is less than its amortized cost

basis at the balance sheet date of the reporting period for

which impairment is assessed, the impairment is either

(c) See FASB ASC 320-10–25

25–14 Sales of debt securities that meet either of the following

conditions may be considered as maturities for purposes of the

classification of securities and the disclosure requirements

under this Subtopic:

1. The sale of a security occurs near enough to its maturity

date (or call date if exercise of the call is probable) that

2. The sale of a security occurs after the entity has already

collected a substantial portion (at least 85 percent) of the

PROFESSIONAL RESEARCH (Continued)

(d) See FASB ASC 320-10–50

50–10 For any sales of or transfers from securities classified as held–

to-maturity, an entity shall disclose all of the following in the

notes to the financial statements for each period for which the

results of operations are presented:

1. The net carrying amount of the sold or transferred security

2. The net gain or loss in accumulated other comprehensive

PROFESSIONAL SIMULATION

Note: This assignment is available on the Kieso website.

Journal Entries

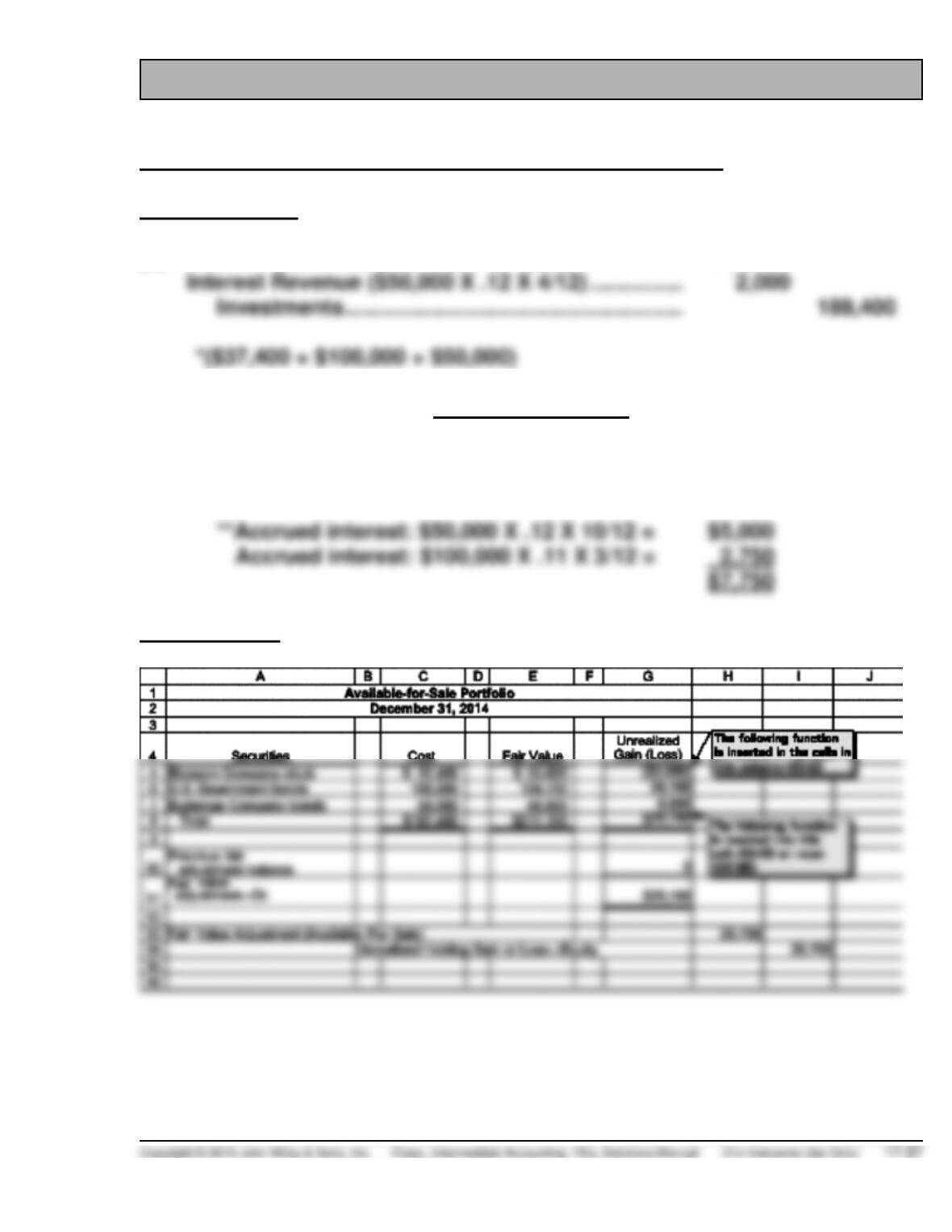

(a) Debt Investments (available-for-sale) ……………… 187,400*

(b) December 31, 2014

Interest Receivable ………………………………………… 7,750

Interest Revenue ……………………………………….. 7,750**

Measurement

PROFESSIONAL SIMULATION (Continued)

Explanation

If Powerpuff owns 30%, it will use the equity method to account for the

investment. As a result, this investment would not be reported at fair value

IFRS CONCEPTS AND APPLICATION

IFRS17-1

The accounting for investment securities is discussed in IAS 27 (“Consoli–

dated and Separate Financial Statements”), IAS 28 (“Accounting for

Investments in Associates”), IAS 39 (“Financial Instruments: Recognition

and Measurement”), and IFRS 9 (“Financial Instruments”).

IFRS17-2

GAAP classifies investments as trading, available-for-sale (both debt and

Both GAAP and IFRS use the same test to determine whether the equity

method of accounting should be used—that is, significant influence with a

general guide of over 20 percent ownership.

The basis for consolidation under IFRS is control. Under GAAP, a bipolar

approach is used, which is a risk-and-reward model (often referred to as a

While measurement of impairments is similar, GAAP does not permit the

reversal of an impairment charge related to available-for-sale debt and equity

investments. IFRS allows reversals of impairments for held-for-collection

investments.

IFRS17-3

The two criteria for determining the valuation of financial assets are the

IFRS17-4

Only debt investments such as loans and bond investments are valued at

IFRS17-5

Lady Gaga should classify this investment as a trading investment because

IFRS17-6

If Lady Gaga plans to hold the investment to collect interest and receive the

principal at maturity, it should account for this investment at amortized cost.

IFRS17-7

Unrealized holding gains and losses for trading investments should be

IFRS17-8

(a) Under U.S. GAAP, Ramirez makes no entry, because impaired invest–

ments may not be written up if they recover in value.

IFRS17-9

(a) Debt Investments ……………………………………………. 65,118

Cash ……………………………………………………….. 65,118

IFRS17–10

(a) Equity Investments …………………………………………. 13,200

Cash ……………………………………………………….. 13,200

IFRS17–11

(a) Equity Investments …………………………………………. 13,200

Cash ……………………………………………………….. 13,200

IFRS17–12

(a) January 1, 2014

Debt Investments ………………………………………. 537,907.40

(b) Schedule of Interest Revenue and Bond Premium Amortization

12% Bonds Sold to Yield 10%

Date

Cash

Received

Interest

Revenue

Premium

Amortized

Carrying Amount

of Bonds

1/1/14

—

—

—

$537,907.40

12/31/14

$60,000

$53,790.74

$6,209.26

531,698.14

12/31/15

53,169.81

524,867.95

12/31/16

52,486.80

517,354.75

12/31/17

51,735.48

509,090.23

(c) December 31, 2014

Cash ……………………………………………………….… 60,000.00

(d) December 31, 2015

Cash ……………………………………………………….… 60,000.00

IFRS17–13

(a) January 1, 2014

IFRS17-13 (Continued)

(b) December 31, 2014

Cash ……………………………………………………………. 60,000.00

Debt Investments ………………………………….. 6,209.26

Interest Revenue ($537,907.40 X .10) ………. 53,790.74

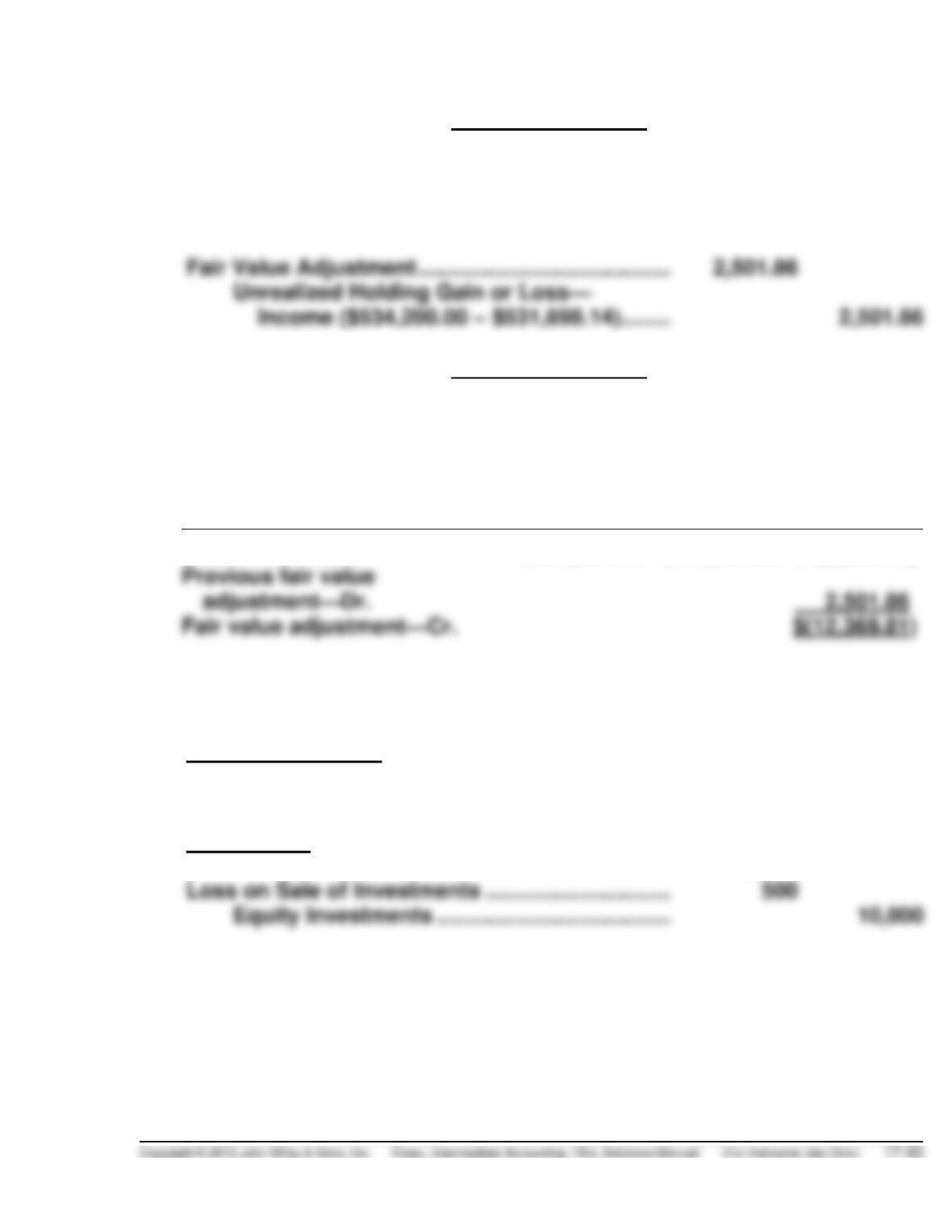

(c) December 31, 2015

Unrealized Holding Gain or Loss—Income …….. 12,369.81

Fair Value Adjustment …………………………... 12,369.81

Amortized

Cost

Fair Value

Unrealized

Gain (Loss)

Debt investments

$524,867.95

$515,000.00

$ (9,867.95)

Previous fair value

IFRS17–14

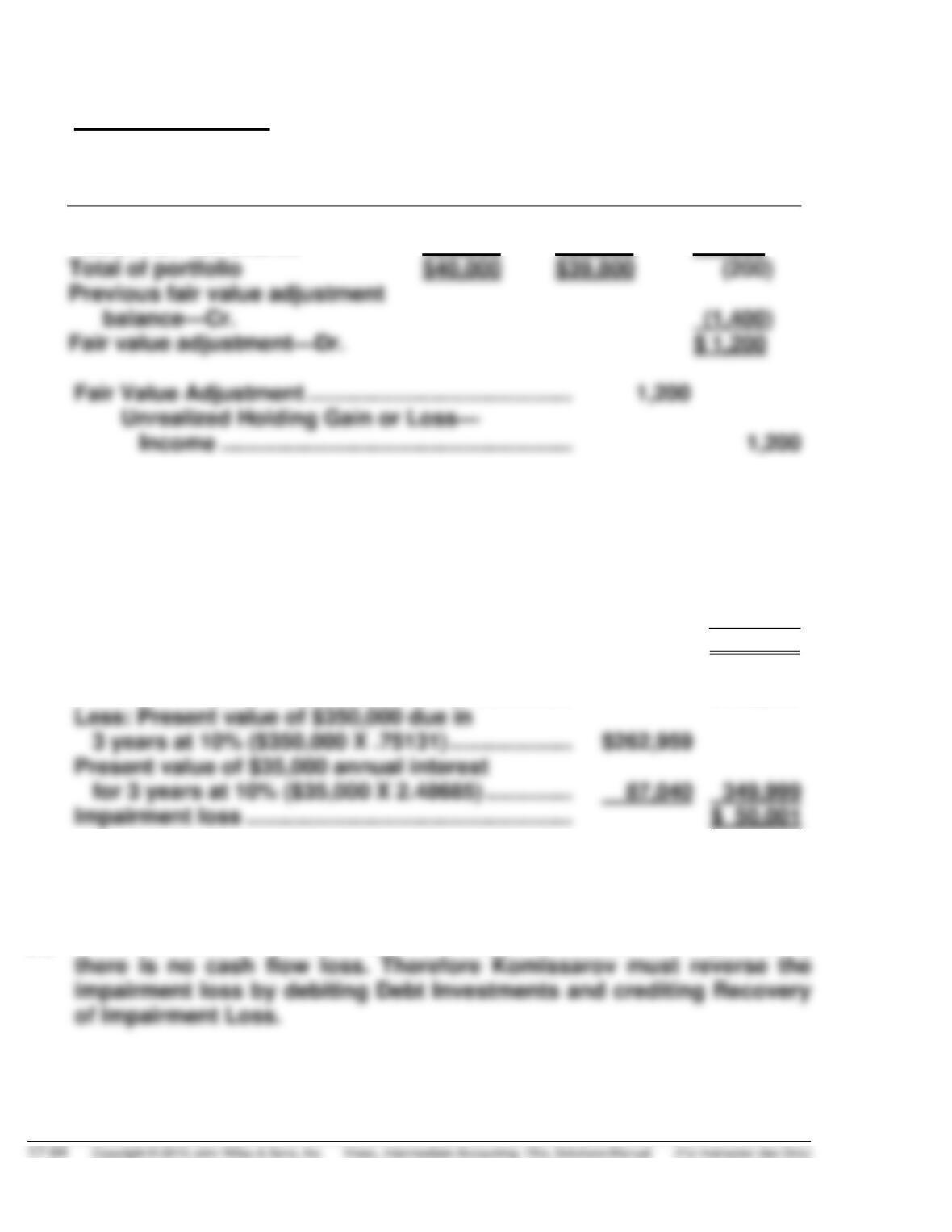

(a) December 31, 2014

Unrealized Holding Gain or Loss—Income …….. 1,400

Fair Value Adjustment …………………………... 1,400

(b) During 2015

Cash ……………………………………………………………. 9,500

IFRS17-14 (Continued)

(c) December 31, 2015

Investments

Cost

Fair Value

Unrealized

Gain (Loss)

Stargate Corp. shares

$20,000

$19,300

$ (700)

Vectorman Co. shares

20,000

20,500

500)

IFRS17–15

(a) Contractual cash flow

[($400,000 X .10 X 3) + $400,000] …………………… $520,000

Expected cash flow ………………………………………… (455,000)

Cash flow loss ……………………………………………….. $ 65,000

Recorded investment …………………………………….. $400,000

(b) Loss on Impairment ……………………………………….. 50,001

Debt Investments ……………………………………. 50,001

(c) Since Komissarov will now receive the contractual cash flow ($520,000)

IFRS17-16

(a) According to IAS 39, paragraph AG71, “A financial instrument is

regarded as quoted in an active market if quoted prices are readily

(b) According to IAS 39, paragraph IN22, “The Standard requires that

impairment losses on available-for-sale equity instruments cannot be

reversed through profit or loss, i.e. any subsequent increase in fair

(c) According to IFRS 9, paragraph B4.3,

Although the objective of an entity’s business model may be to hold

financial assets in order to collect contractual cash flows, the entity

1. the financial asset no longer meets the entity’s investment policy

(e.g., the credit rating of the asset declines below that required by

the entity’s investment policy);

IFRS17-17

(a) M&S reports both current and non-current “other financial assets,” along

with both current and non-current derivative financial instruments.

(c) M&S uses derivatives to manage its exposure to fluctuations in interest

rates and exchange rates.