EXERCISE 9-5 (Continued)

*

Jan. 31

Feb. 28

Mar. 31

Apr. 30

Inventory at cost

$15,000

$15,100

$17,000

$13,000

Inventory at the lower-of-cost-

or-market

14,500

12,600

15,600

12,300

(b)

Jan. 31

Loss Due to Market Decline of Inventory ………………….

500

Allowance to Reduce Inventory

to Market ……………………………………………………..

500

Feb. 28

Loss Due to Market Decline of Inventory ………………….

Allowance to Reduce Inventory

Apr. 30

Allowance to Reduce Inventory to Market …………………….

700

Recovery of Loss Due to Market

EXERCISE 9-6

Net realizable value (ceiling)

$45 – $14 = $31

Net realizable value less normal profit (floor)

$31 – $ 9 = $22

Replacement cost

$35

Designated market

$31

Ceiling

Cost

$40

$31

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 9-23

EXERCISE 9-7 (15–20 minutes)

Cost Per Lot

(Cost Allocated/

No. of Lots)

$2,100

* 9 – 5 = 4

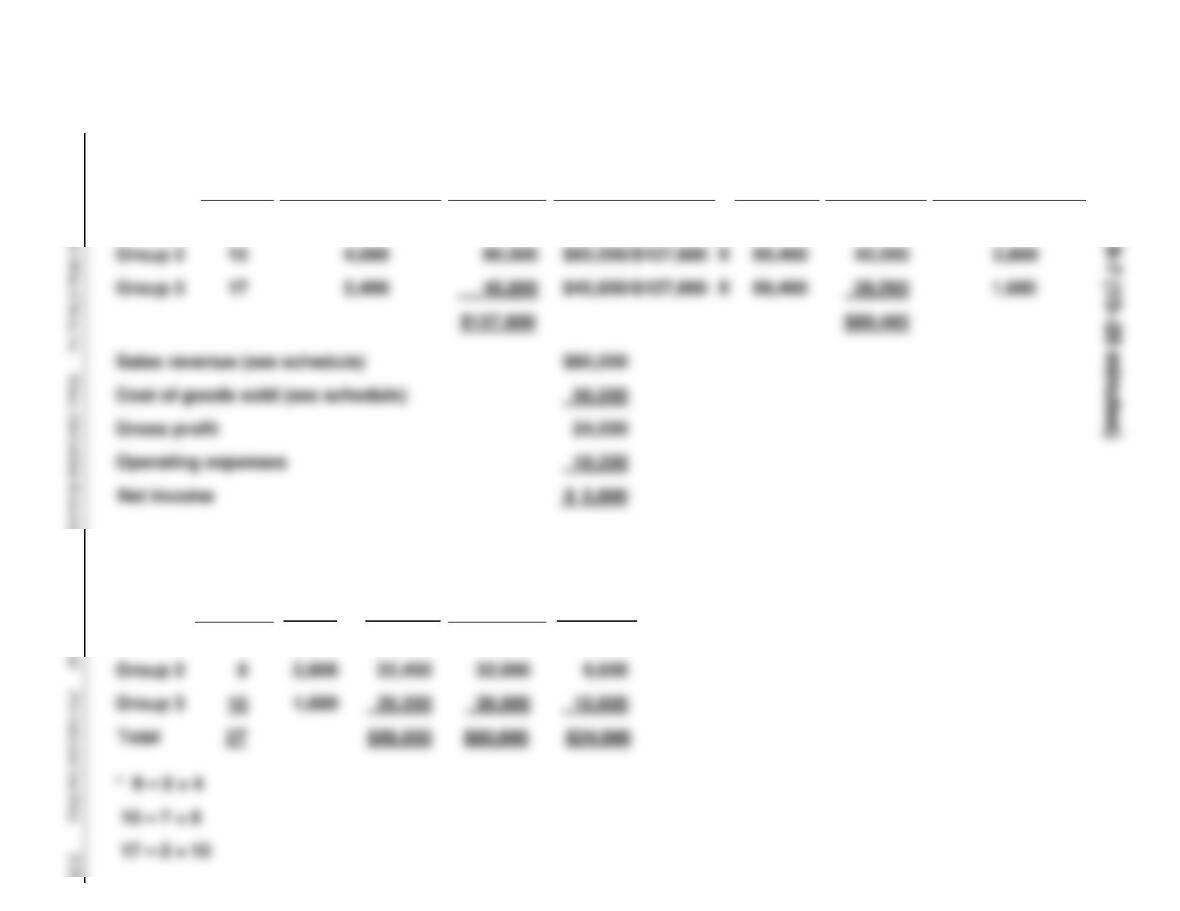

Group 3

Cost

Allocated

to Lots

$18,900

Total

Cost

$89,460

X

Relative Sales

Price

$27,000/$127,800

Gross

Profit

$ 3,600

Total

Sales

Price

$ 27,000

Sales

$12,000

Sales

Price Per Lot

$3,000

Cost Cost of

Per Lots

Lot Sold

$2,100 $ 8,400

No. of

Lots

9

Number

of Lots

Sold*

4

Group 1

Group 1

Cost of goods sold (see schedule)

9-24 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

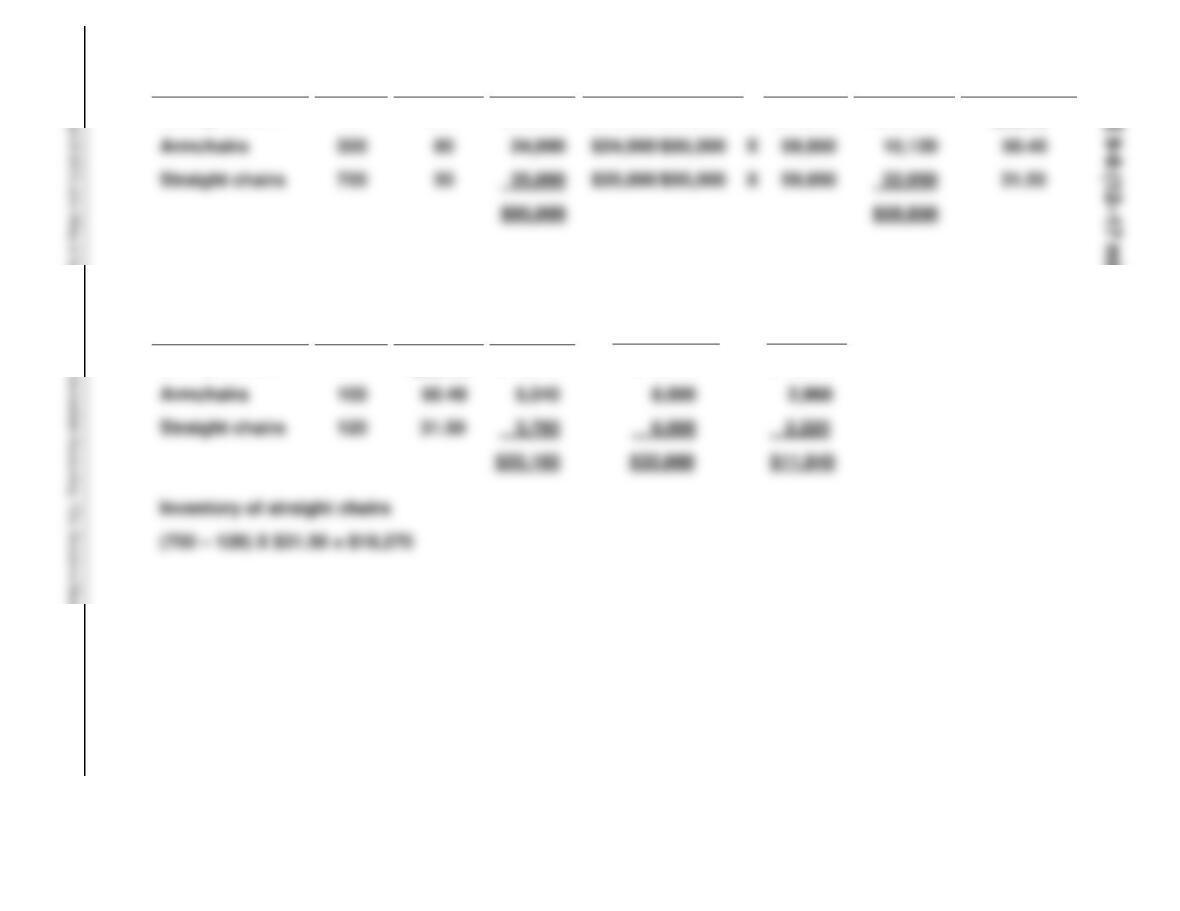

EXERCISE 9-8 (12–17 minutes)

Cost per

Chair

$56.70

Inventory of straight chairs

Straight chairs

Cost

Allocated

to Chairs

$22,680

Total

Cost

$59,850

Gross

Profit

$ 6,660

X

Relative Sales

Price

$36,000/$95,000

Sales

$18,000

Total

Sales

Price

$36,000

Cost of

Chairs

Sold

$11,340

Sales

Price

per Lot

$90

Cost

per

Chair

$56.70

No. of

Chairs

400

Number

of Chairs

Sold

200

Chairs

Lounge chairs

Chairs

Lounge chairs

EXERCISE 9-9 (5–10 minutes)

Unrealized Holding Gain or Loss—Income

EXERCISE 9-10 (15–20 minutes)

(a) If the commitment is material in amount, there should be a footnote in

the balance sheet stating the nature and extent of the commitment.

(b) The drop in the market price of the commitment should be charged to

operations in the current year if it is material in amount. The following

entry would be made:

(c) Assuming the $10,800 market decline entry was made on December

31, 2014, as indicated in (b), the entry when the materials are received

in January 2015 would be:

EXERCISE 9-10 (Continued)

This entry records the raw materials at the actual cost, eliminates the

EXERCISE 9-11 (8–13 minutes)

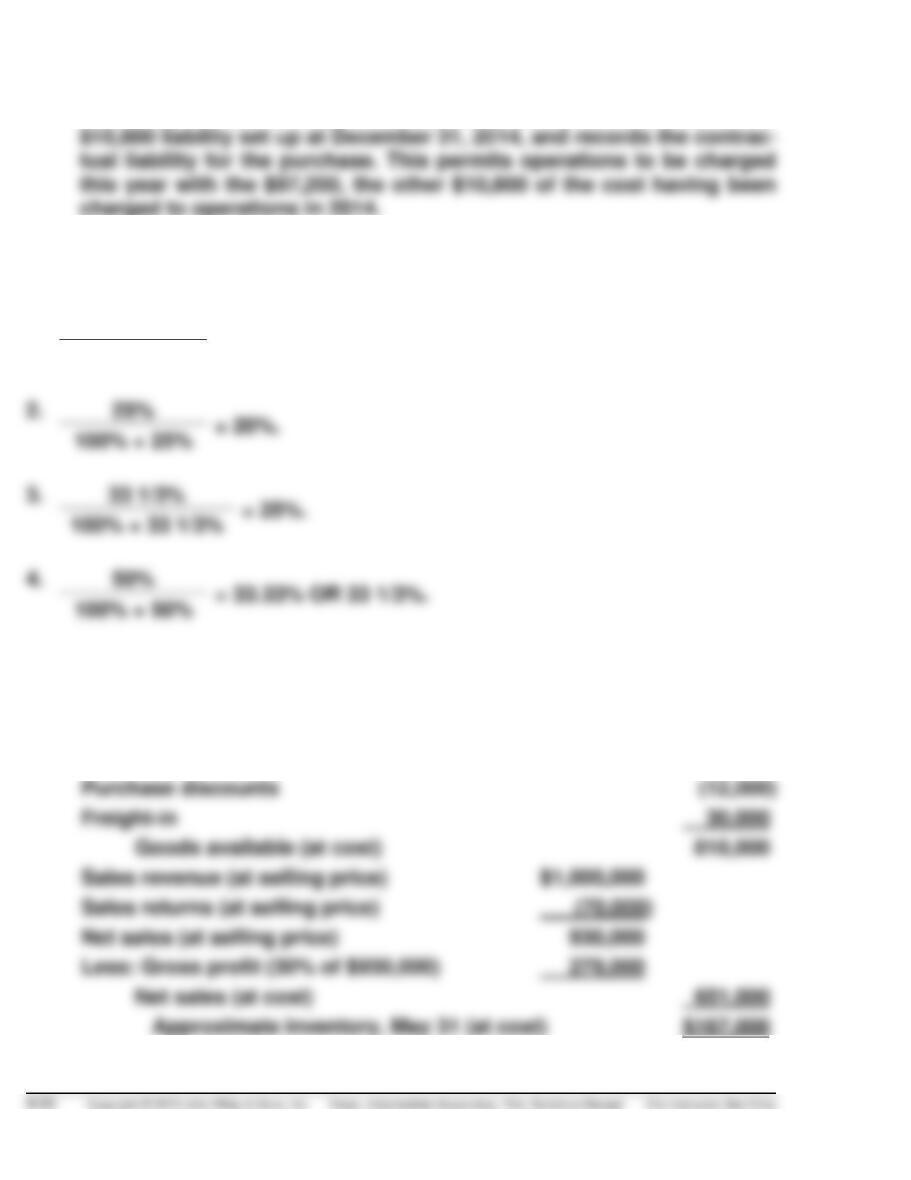

1.

20%

= 16.67% OR 16 2/3%.

100% + 20%

2.

25%

100% + 25%

3.

= 25%.

4.

50%

= 33.33% OR 33 1/3%.

100% + 50%

EXERCISE 9-12 (10–15 minutes)

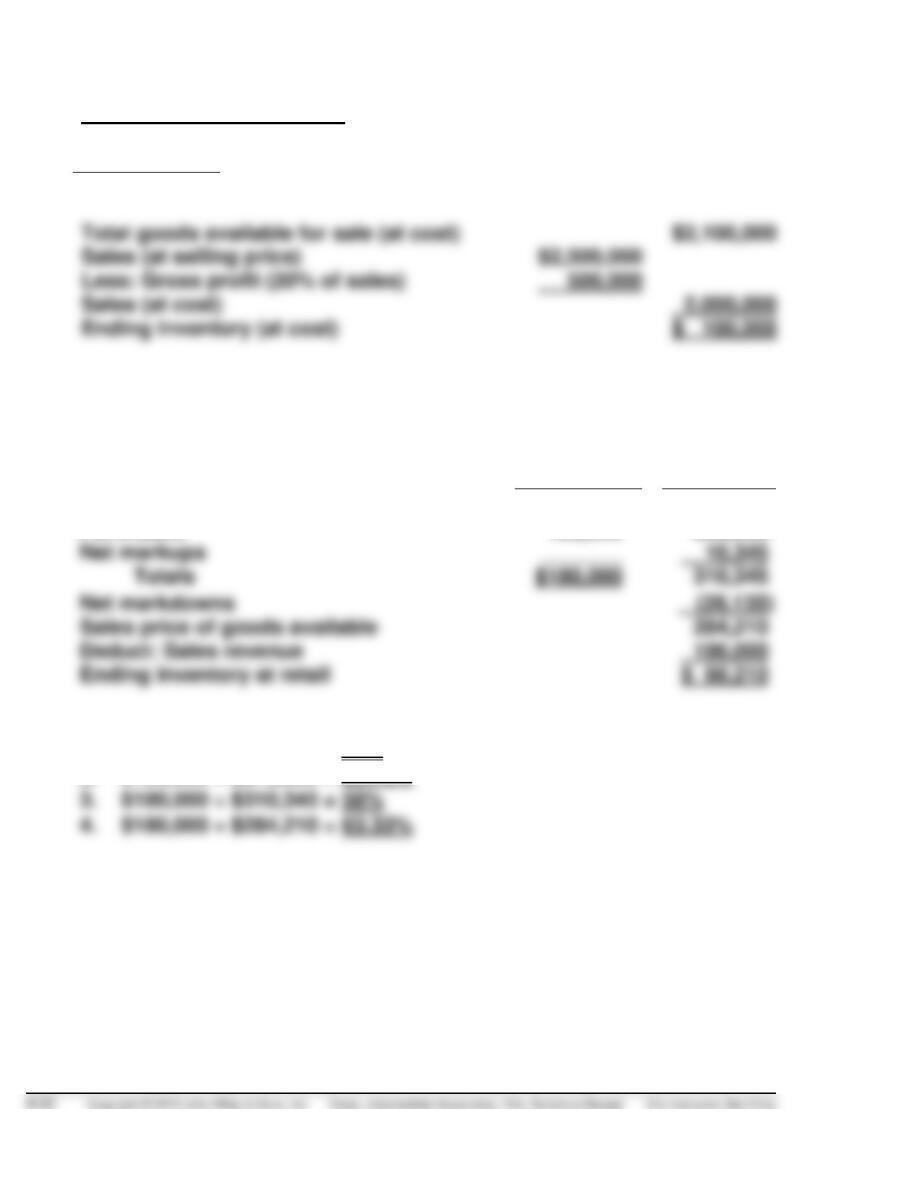

(a)

Inventory, May 1 (at cost)

$160,000

Purchases (at cost)

640,000

Purchase discounts

30,000

Goods available (at cost)

Sales revenue (at selling price)

Sales returns (at selling price)

Net sales (at selling price)

Less: Gross profit (30% of $930,000)

Net sales (at cost)

651,000

EXERCISE 9-12 (Continued)

(b) Gross profit as a percent of sales must be computed:

30%

= 23.08% of sales.

100% + 30%

Inventory, May 1 (at cost)

$160,000

Purchases (at cost)

640,000

Purchase discounts

30,000

Goods available (at cost)

Sales revenue (at selling price)

Sales returns (at selling price)

Net sales (at selling price)

Less: Gross profit (23.08% of $930,000)

Net sales (at cost)

715,356

Approximate inventory, May 31 (at cost)

$102,644

EXERCISE 9-13 (15–20 minutes)

(a)

Merchandise on hand, January 1

$ 38,000

Purchases

72,000

Less: Purchase returns and allowances

(2,400)

3,400

Total merchandise available (at cost)

Cost of goods sold*

75,000

Ending inventory

36,000

Less: Undamaged goods

10,900

*Gross profit =

= 25% of sales.

EXERCISE 9-13 (Continued)

(b)

Cost of goods sold = 66 2/3% of sales of $100,000 = $66,667

[$111,000 (as computed above) – $66,667]

Less: Undamaged goods

EXERCISE 9-14

Beginning inventory

$170,000

Purchases

390,000

560,000

Purchase returns

Goods available (at cost)

530,000

Sales revenue

Sales returns

Net sales

Less: Gross profit (40% X $626,000)

375,600

damage)

154,400

$21,000 X (1 – 40%)

realizable value)

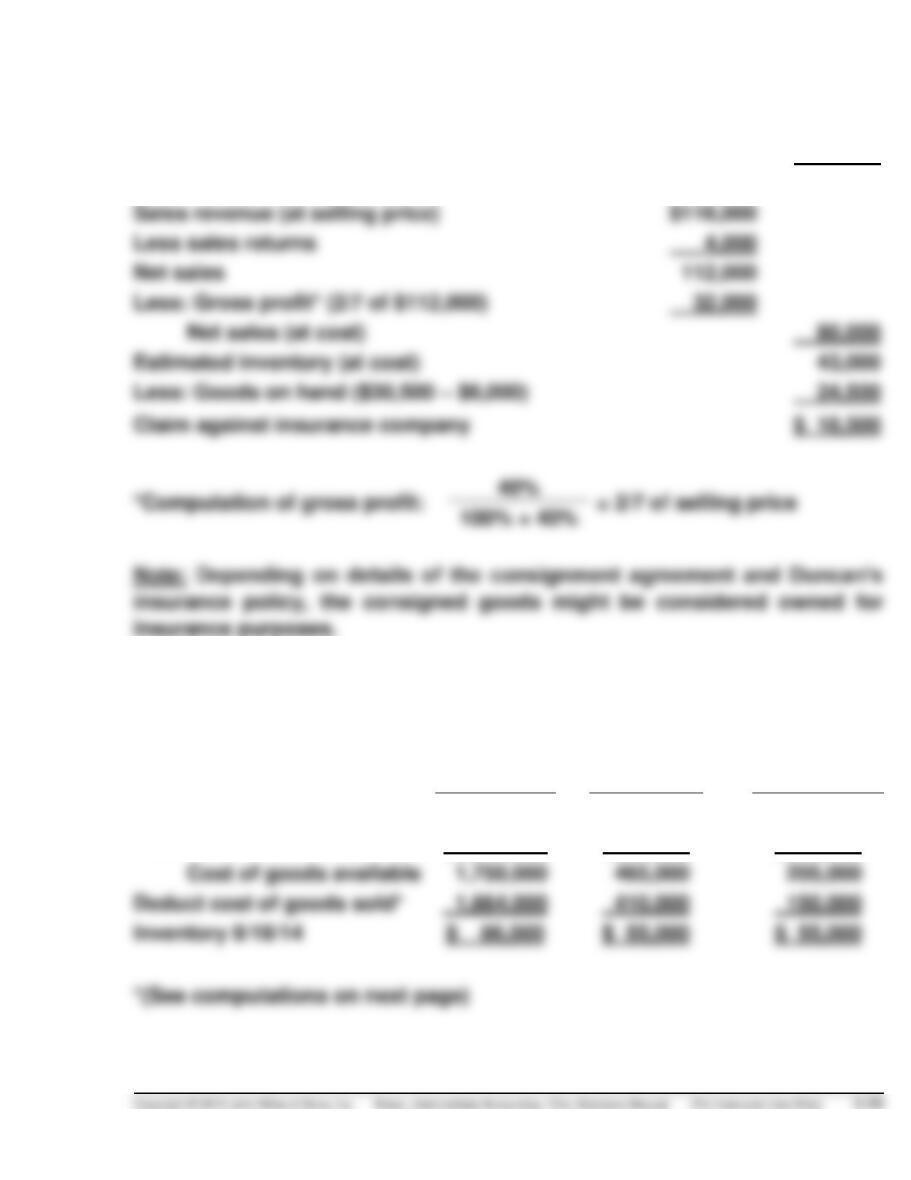

EXERCISE 9-15 (10–15 minutes)

Beginning inventory (at cost)

$ 38,000

Purchases (at cost)

85,000

Goods available (at cost)

123,000

Sales revenue (at selling price)

$116,000

Less sales returns

4,000

Net sales

112,000

Less: Gross profit* (2/7 of $112,000)

32,000

Net sales (at cost)

80,000

Less: Goods on hand ($30,500 – $6,000)

Claim against insurance company

EXERCISE 9-16 (15–20 minutes)

Lumber

Millwork

Hardware

Inventory 1/1/14 (cost)

$ 250,000

$ 90,000

$ 45,000

Purchases to 8/18/14 (cost)

1,500,000

375,000

160,000

Cost of goods available

1,750,000

465,000

205,000

Deduct cost of goods sold*

1,664,000

410,000

150,000

Inventory 8/18/14

$ 55,000

EXERCISE 9-16 (Continued)

Computation for cost of goods sold:*

Lumber:

$2,080,000

= $1,664,000

1.25

Millwork:

= $410,000

1.30

*Alternative computation for cost of goods sold:

Markup on selling price: Cost of goods sold:

Lumber:

= 20% or 1/5

$2,080,000 X 80% = $1,664,000

Millwork:

= 3/13

$533,000 X 10/13 = $410,000

Hardware:

= 2/7

$210,000 X 5/7 = $150,000

EXERCISE 9-17 (20–25 minutes)

Ending inventory:

(a)

Gross profit is 45% of sales

Total goods available for sale (at cost)

$2,100,000

Sales (at selling price)

Less: Gross profit (45% of sales)

Sales (at cost)

(b)

Gross profit is 60% of cost

60%

= 37.5% markup on selling price

100% + 60%

Total goods available for sale (at cost)

$2,100,000

Sales (at selling price)

Less: Gross profit (37.5% of sales)

Sales (at cost)

(c)

Gross profit is 35% of sales

Total goods available for sale (at cost)

$2,100,000

Sales (at selling price)

Less: Gross profit (35% of sales)

Sales (at cost)

EXERCISE 9-17 (Continued)

(d)

Gross profit is 25% of cost

25%

= 20% markup on selling price

100% + 25%

Total goods available for sale (at cost)

$2,100,000

Sales (at selling price)

Less: Gross profit (20% of sales)

Sales (at cost)

Ending inventory (at cost)

EXERCISE 9-18 (20–25 minutes)

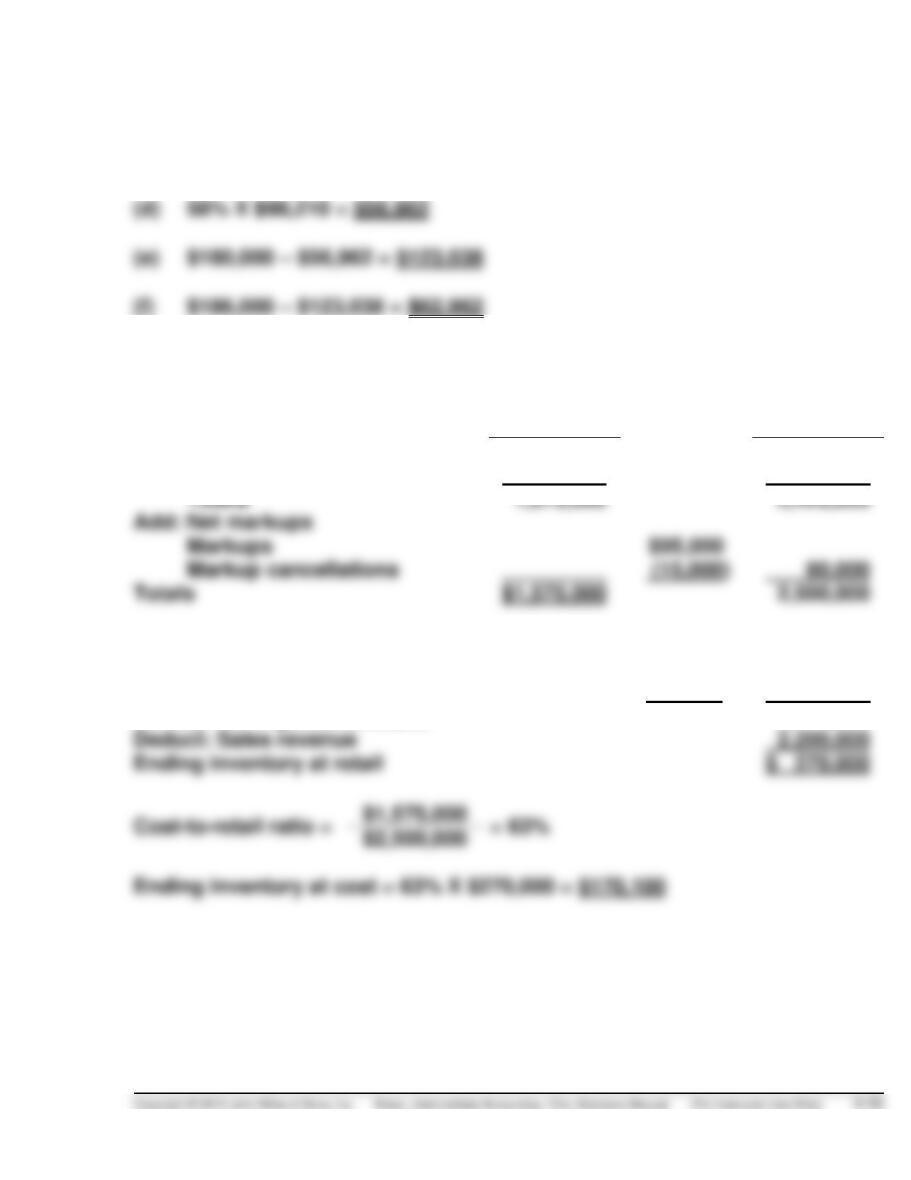

(a)

Cost

Retail

Beginning inventory

$ 58,000

$100,000

Purchases

122,000

200,000

Net markups

Totals

Net markdowns

Sales price of goods available

284,210

Deduct: Sales revenue

Ending inventory at retail

(b)

1.

$180,000 ÷ $300,000 = 60%

2.

$180,000 ÷ $273,865 = 65.73%

3.

$180,000 ÷ $310,345 = 58%

4.

$180,000 ÷ $284,210 = 63.33%

EXERCISE 9-18 (Continued)

(c)

1.

Method 3.

2.

Method 3.

3.

Method 3.

$186,000 – $123,038 = $62,962

EXERCISE 9-19 (12–17 minutes)

Cost

Retail

Beginning inventory

$ 200,000

$ 280,000

Purchases

1,375,000

2,140,000

Totals

1,575,000

2,420,000

Add: Net markups

Markups

$95,000

Markup cancellations

80,000

Deduct: Net markdowns

Markdowns

35,000

Markdowns cancellations

(5,000)

30,000

Sales price of goods available

2,470,000

Deduct: Sales revenue

2,200,000

EXERCISE 9-20 (20–25 minutes)

Cost

Retail

Beginning inventory

$30,000

$ 46,500

Purchases

48,000

88,000

Purchase returns

(2,000)

(3,000)

Freight on purchases

2,400

Totals

78,400

131,500

Add: Net markups

Markups

$10,000

Markup cancellations

(1,500)

Net markups

8,500

Deduct: Net markdowns

Markdowns

9,300

Markdowns cancellations

(2,800)

Net markdowns

6,500

Sales price of goods available

Deduct: Net sales ($99,000 – $2,000)

97,000

EXERCISE 9-21 (10–15 minutes)

(a) Inventory turnover:

2012

2011

2011

*EXERCISE 9-22 (25–35 minutes)

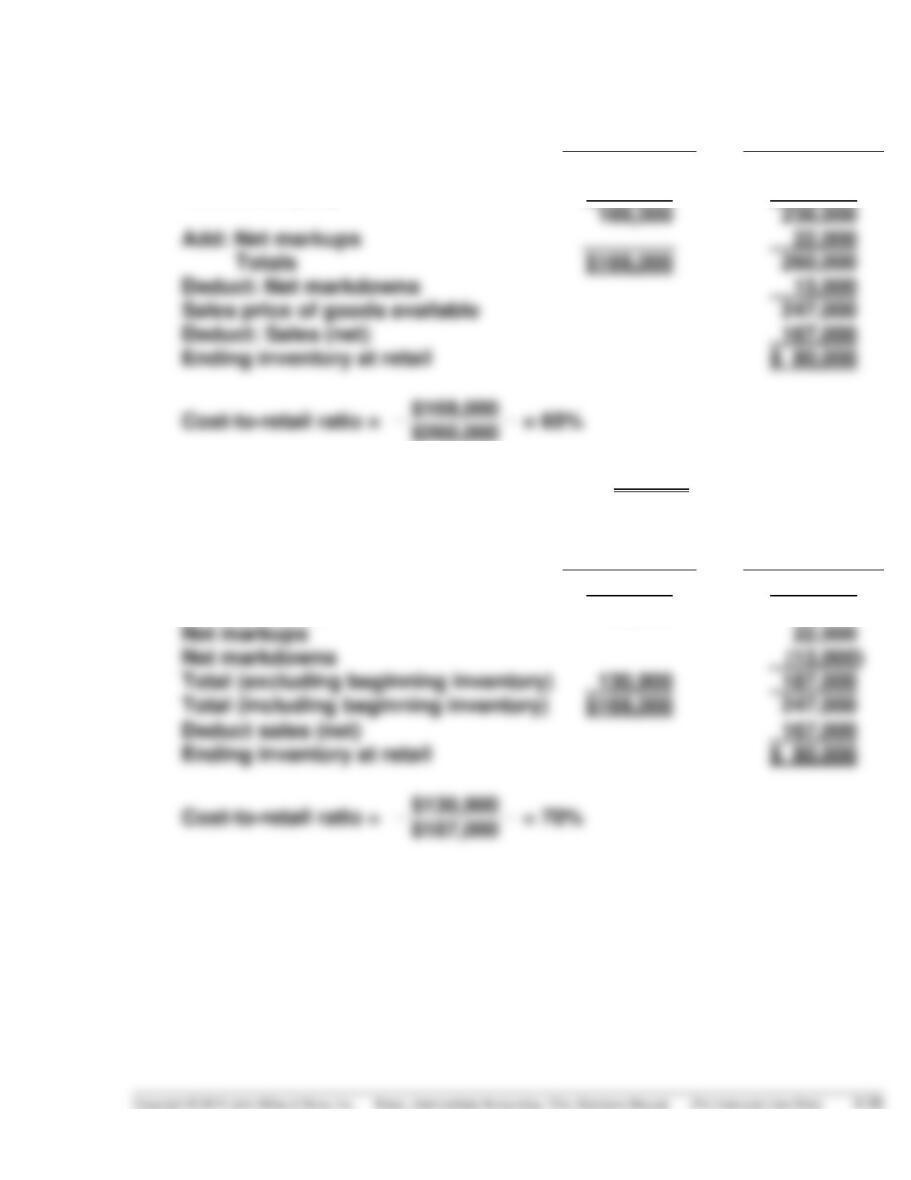

(a)

Conventional Retail Method

Cost

Retail

Inventory, January 1, 2013

$ 38,100

$ 60,000

Purchases (net)

130,900

178,000

169,000

238,000

Add: Net markups

Totals

$169,000

260,000

Deduct: Net markdowns

Sales price of goods available

247,000

Deduct: Sales (net)

167,000

Ending inventory at retail

Ending inventory at cost = 65% X $80,000 = $52,000

(b)

LIFO Retail Method

Cost

Retail

Inventory, January 1, 2013

$ 38,100

$ 60,000

Net purchases

130,900

178,000

Net markups

22,000

Net markdowns

Total (excluding beginning inventory)

130,900

187,000

Deduct sales (net)

167,000

Ending inventory at retail

*EXERCISE 9-22 (Continued)

Computation of ending inventory at LIFO cost, 2014:

Ending Inventory

at Retail Prices

Layers at

Retail Prices

Cost to Retail

(Percentage)

Ending Inventory

at LIFO Cost

$80,000

2013 $60,000

X

63.5%*

$38,100

*EXERCISE 9-23 (15–20 minutes)

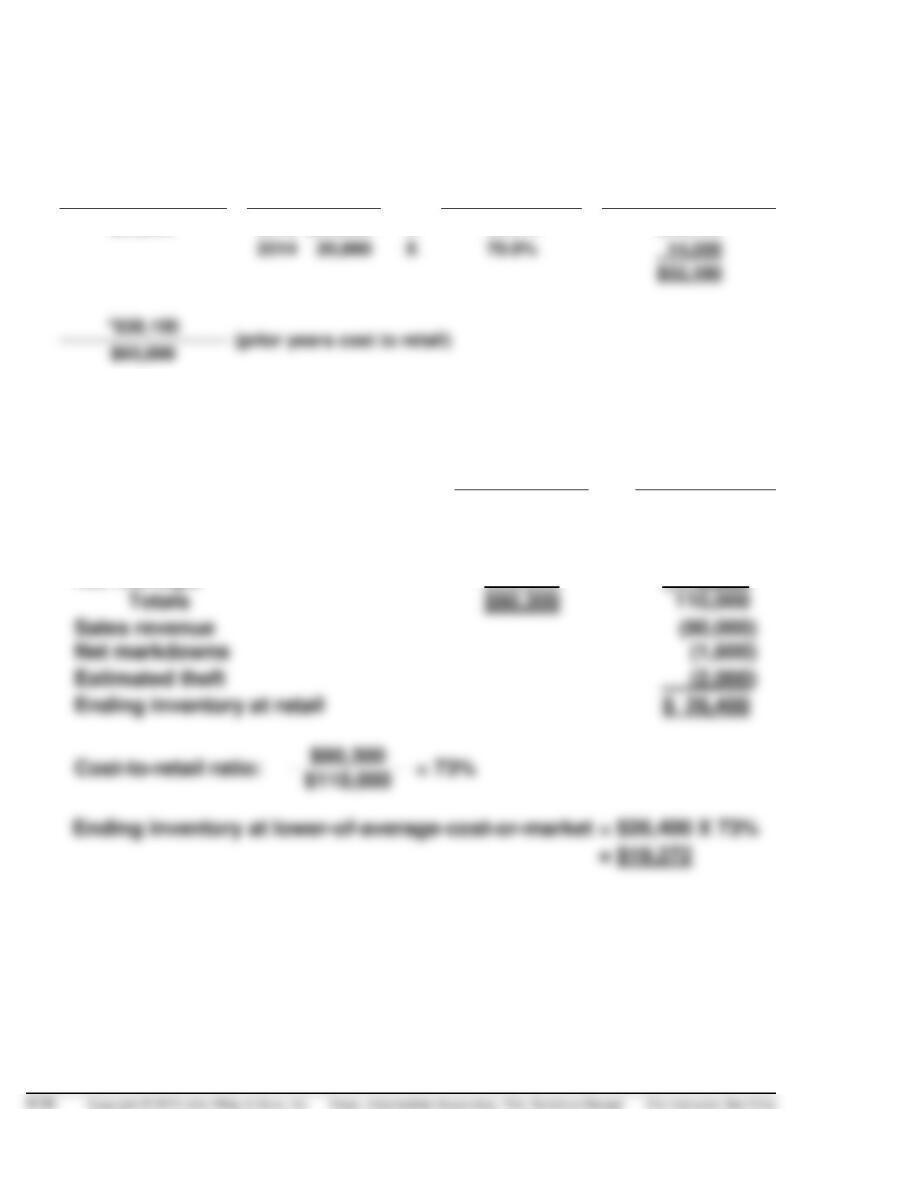

(a)

Cost

Retail

Inventory, January 1, 2014

$14,000

$ 20,000

Net purchases

58,800

81,000

Freight-in

7,500

Net markups

9,000

Totals

Sales revenue

Net markdowns

Estimated theft

Ending inventory at retail

*EXERCISE 9-23 (Continued)

(b)

Cost

Retail

Purchases

$58,800

$81,000

Freight-in

7,500

Net markups

9,000

Net markdowns

(1,600)

Totals

$66,300

$88,400

Cost-to-retail ratio:

= 75%

Beginning inventory, 2014

$14,000

$20,000

Increment

4,800

Ending inventory, 2014

$26,400

*EXERCISE 9-24 (10–15 minutes)

(a)

Cost-to-retail ratio—beginning inventory:

$216,000

= 72%

$300,000

*($294,300 ÷ 1.09) X 72% = $194,400

*EXERCISE 9-24 (Continued)

(b)

Ending inventory at retail prices deflated $365,150 ÷ 1.09

$335,000

Beginning inventory at beginning-of-year prices

300,000

Beginning inventory (at cost)

*($364,800 ÷ $480,000)

*EXERCISE 9-25 (5–10 minutes)

Ending inventory at retail (deflated) $100,100 ÷ 1.10

$91,000

Beginning inventory at retail

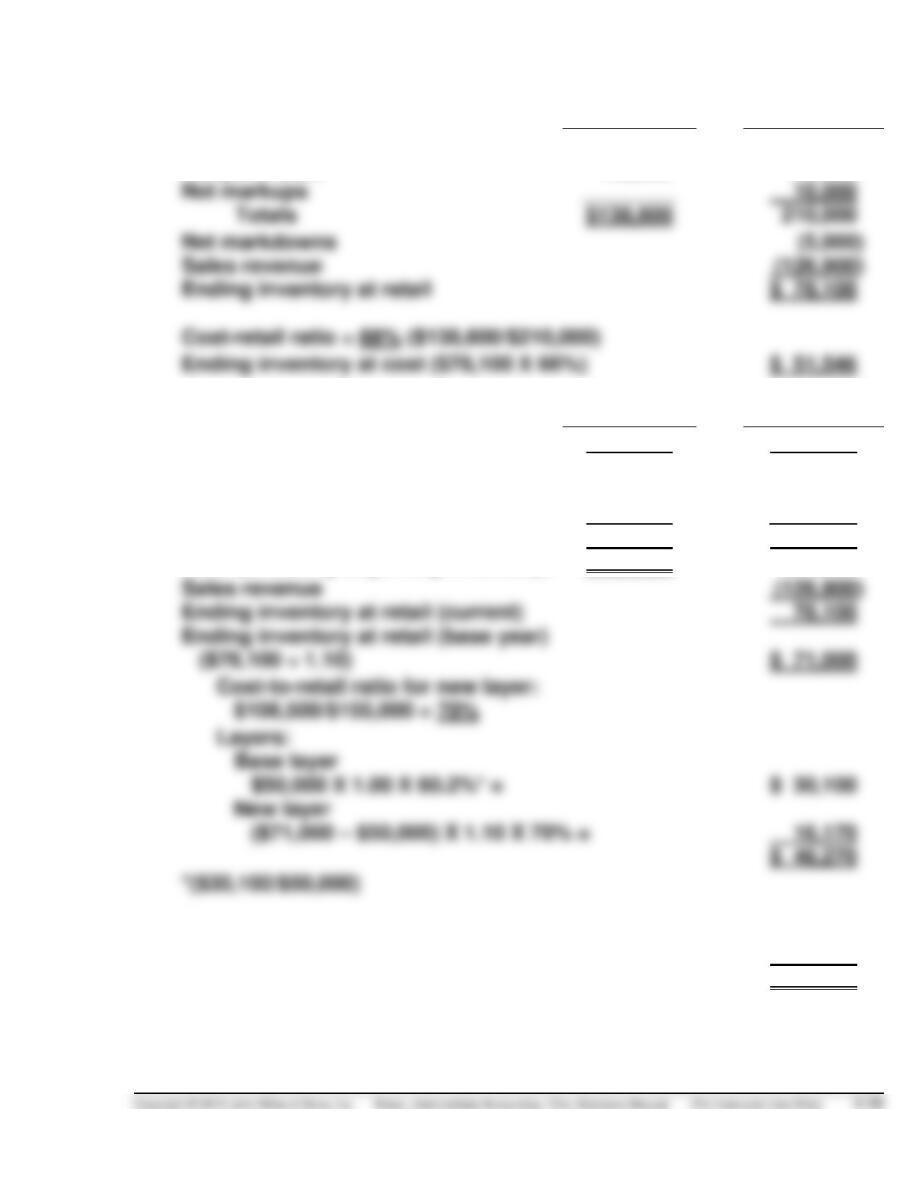

*EXERCISE 9-26 (20–25 minutes)

(a)

Cost

Retail

Beginning inventory

$ 30,100

$ 50,000

Net purchases

108,500

150,000

Net markups

10,000

Totals

$138,600

210,000

Net markdowns

Sales revenue

Ending inventory at retail

$ 78,100

Cost-retail ratio = 66% ($138,600/$210,000)

(b)

Cost

Retail

Beginning inventory

$ 30,100

$ 50,000

Net purchases

108,500

150,000

Net markups

10,000

Net markdowns

(5,000)

Total (excluding beginning inventory)

108,500

155,000

Total (including beginning inventory)

$138,600

205,000

Sales revenue

Ending inventory at retail (base year)

($78,100 ÷ 1.10)

$ 71,000

Cost-to-retail ratio for new layer:

$108,500/$155,000 = 70%

Layers:

Base layer

$50,000 X 1.00 X 60.2%* =

$ 30,100

New layer

($71,000 – $50,000) X 1.10 X 70% =

16,170

$ 46,270

*($30,100/$50,000)

(c)

Cost of goods available for sale

$138,600

Ending inventory at cost, from (b)

46,270

Cost of goods sold

$ 92,330

*EXERCISE 9-27 (20–25 minutes)

2013

Restate to base-year retail ($118,720 ÷ 1.06)

$112,000

Layers: 1. $100,000 X 1.00 X 54%* =

$ 54,000

2. $ 12,000 X 1.06 X 57% =

7,250

Ending inventory

$ 61,250

*$54,000 ÷ $100,000

2014

Restate to base-year retail ($138,750 ÷ 1.11)

$125,000

Layers: 1. $100,000 X 1.00 X 54% =

$ 54,000

2. $ 12,000 X 1.06 X 57% =

3. $ 13,000 X 1.11 X 60% =

8,658

Ending inventory

$ 69,908

2015

Restate to base-year retail ($125,350 ÷ 1.15)

$109,000

Layers: 1. $100,000 X 1.00 X 54% =

$ 54,000

2. $ 9,000 X 1.06 X 57% =

5,438

Ending inventory

$ 59,438

2016

Restate to base-year retail ($162,500 ÷ 1.25)

$130,000

Layers: 1. $100,000 X 1.00 X 54% =

$ 54,000

2. $ 9,000 X 1.06 X 57% =

3. $ 21,000 X 1.25 X 58% =

15,225

Ending inventory

$ 74,663

*EXERCISE 9-28 (5–10 minutes)

Inventory (beginning) ………………………………………………

Adjustment to Record Inventory at Cost* ………….

($212,600 – $205,000)

*Note: This account is an income statement account showing the effect of

changing from a lower-of-cost-or-market approach to a straight cost basis.