CA 16-6 (Continued)

36,000 [(30,000 X $30) ÷ $25] shares of treasury stock at $25 with the proceeds. Therefore, if you add

the 30,000 exercised warrants to the common stock outstanding and then subtract the 36,000 shares

presumably purchased, the number of shares outstanding would be reduced to 94,000 (100,000 +

FINANCIAL REPORTING PROBLEM

(a) (1) Under P&G’s stock-based compensation plan (Note 7), 29,141,000

options were granted during 2011.

(2) At June 30, 2011, 271,096,000 options were exercisable by eligible

managers.

(b)

(In millions—except per share)

2011

2010

2009

Weighted-average common shares

3,001.9

3,099.3

3,154.1

Diluted earnings per share

$3.93

$4.11

$4.26

COMPARATIVE ANALYSIS CASE

(a) Coca–Cola sponsors restricted stock award plans, and stock option

plans.

(b)

Coca-Cola

PepsiCo

Options outstanding at year-end 2011

(c)

Coca-Cola

PepsiCo

Options granted during 2011

26,000,000

7,150,000

(d)

Coca-Cola

PepsiCo

Options exercised during 2011

32,000,000

19,980,000

(e)

Coca-Cola

PepsiCo

Average exercise price during 2011

$47.96

$47.74

(f)

Weighted-Average Number of Shares

(in millions)

Coca-Cola

PepsiCo

2011

2,323

1,597

2010

2009

(g)

Diluted Earnings Per Share

(in millions)

Coca-Cola

PepsiCo

2011

$3.69

$4.03

2010

$5.06

2009

FINANCIAL STATEMENT ANALYSIS CASE

(a) Account 2014 (,000)

Current Liabilities 554,114

Convertible Debt 648,020

(b) Ragatz is doing very well. Its ROA and ROE are above the industry

average. However, its debt level is quite high, compared to the

(c) Under GAAP, the debt and equity components of a convertible bond

are not separately recorded as liabilities and stockholders’ equity. If

Merck had non-convertible bonds with detachable warrants, Merck

would allocate the bond amount between debt and equity. Therefore,

(1) Rate of return on Assets 4.15% = Net Income/Total Assets

(2) Rate of return on Common Stock 17.9% = Net Income/Stockholders’

Equity Equity

(3) Debt to Total Assets 76.8% = Total Debt/Total Assets

FINANCIAL STATEMENT ANALYSIS CASE (Continued)

The adjustment results in Ragatz reporting a higher level of

stockholders’ equity and less debt. Although Ragatz reports the same

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

(a) Under U.S. GAAP, proceeds from the issuance of convertible debt are

recorded entirely as debt.

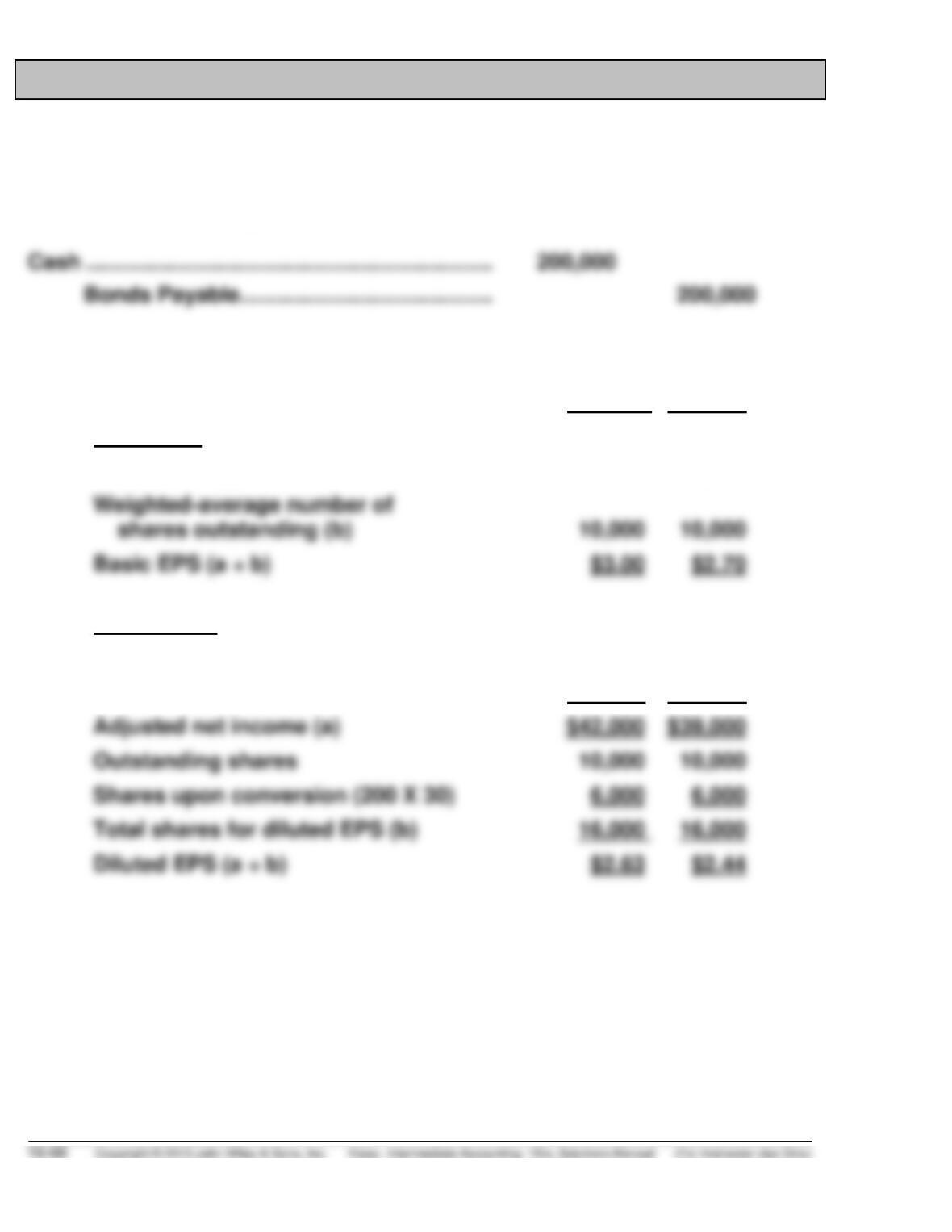

(b)

2014

2013

Basic EPS

Net income (a)

$30,000

$27,000

Basic EPS (a ÷ b)

Diluted EPS

Net income

$30,000

$27,000

Add: Interest savings ($200,000 X 6%)

12,000

12,000

Adjusted net income (a)

$42,000

$39,000

Outstanding shares

Shares upon conversion (200 X 30)

Total shares for diluted EPS (b)

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

(c)

Bond Conversion Expense** ……………………….

7,500

Bonds Payable …………………………………………..

150,000

Common Stock* ………………………………..

9,000

Cash …………………………………………………

7,500

Analysis

EPS Presentation:

2014 2013

Net income $30,000 $27,000

EPS standards are important to analysts who rely on reported earnings per

share numbers in their analyses. A price-earnings (P-E) ratio is the price

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Principles

IFRS for convertible debt primarily differs from U.S. GAAP on convertible

debt in that IFRS requires that companies split the proceeds from issuance

into a debt component and an equity component. For example, in part (a)

Cash …………………………………………………………

200,000

Discount on Bonds Payable ……………………….

70,000

Bonds Payable …………………………………..

200,000

Share Premium-Conversion Equity……..

70,000

Supporters of the IFRS treatment would argue that separating the bond

issue into liability and equity components provides more representational

faithful information into the financial statements. That is, the resulting

PROFESSIONAL RESEARCH

(a) The accounting for stock compensation is addressed in the FASB

Codification at FASB ASC 718-10 (Compensation-Stock

Compensation).

(b) See FASB ASC 718-10-10 (Compensation—Stock Compensation,

Overall, Objectives).

10-1 The objective of accounting for transactions under share-based

payment arrangements with employees is to recognize in the

Currently Viewing:

718 Compensation—Stock Compensation

10–2 This Topic requires that the cost resulting from all share-based

payment transactions be recognized in the financial statements.

This Topic establishes fair value as the measurement objective in

PROFESSIONAL RESEARCH (Continued)

(c) See FASB ASC 718-50–25.

25-1 An employee share-purchase plan that satisfies all of the

1. The plan satisfies either of the following conditions:

(a) The terms of the plan are no more favorable than those

available to all holders of the same class of shares. Note

(b) Any purchase discount from the market price does not

exceed the per-share amount of share issuance costs that

would have been incurred to raise a significant amount of

capital by a public offering. A purchase discount of 5

2. Substantially all employees that meet limited employment

qualifications may participate on an equitable basis.

3. The plan incorporates no option features, other than the

following:

(a) Employees are permitted a short period of time—not

PROFESSIONAL SIMULATION

Note: This assignment is available on the Kieso website.

Explanation

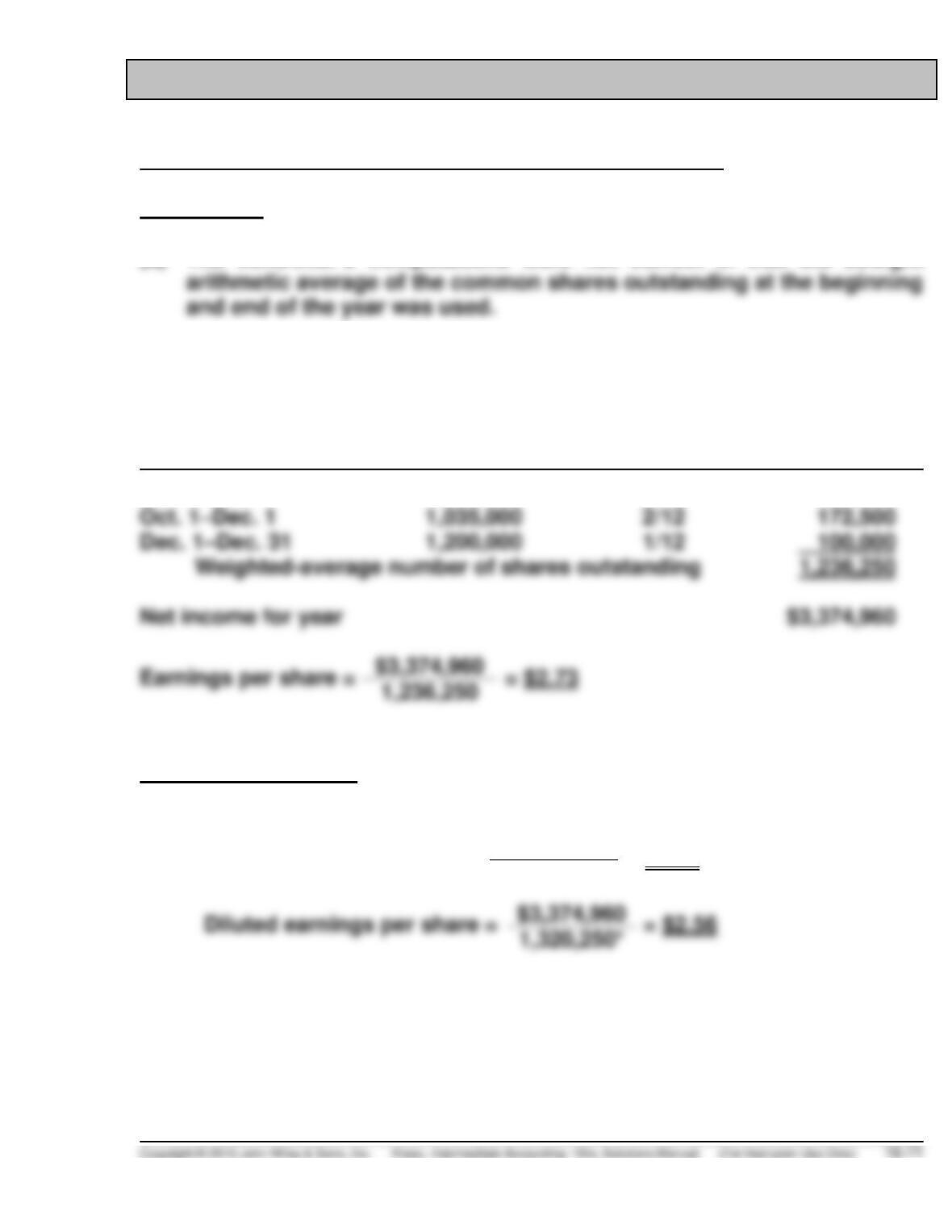

(a) The controller’s computations were not correct in that the straight

The weighted-average number of shares outstanding may be

computed as follows:

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

Jan. 1–Oct. 1

1,285,000

9/12

963,750

Oct. 1–Dec. 1

1,035,000

2/12

172,500

Financial Statements

(b)

Basic earnings per share =

$3,374,960

= $2.73

1,236,250

Diluted earnings per share =