PROBLEM 14-8B

(a)

December 31, 2014

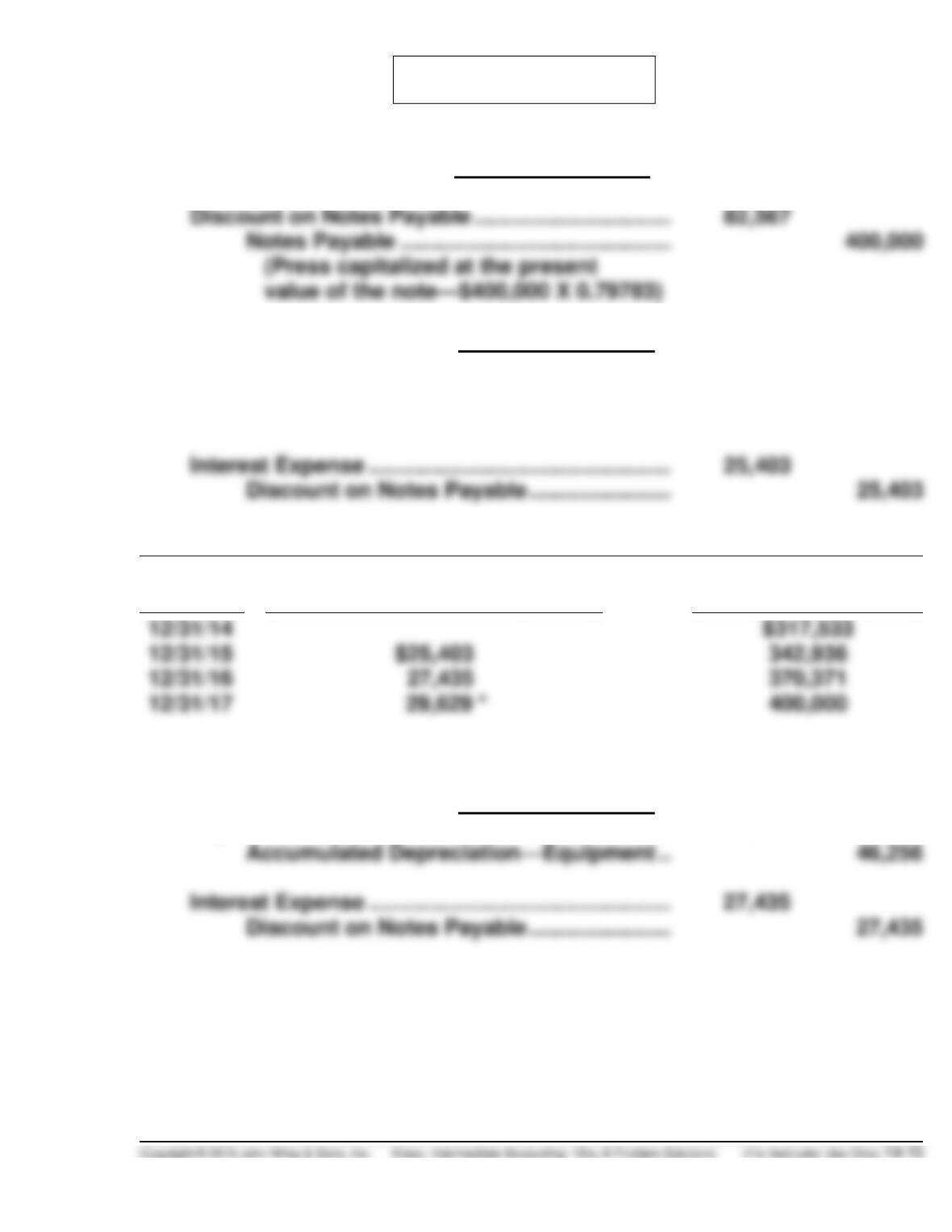

Equipment ……………………………………………………….

317,533

Discount on Notes Payable …………………………..

82,567

Notes Payable ………………………………………………..

(Press capitalized at the present

value of the note—$400,000 X 0.79783)

(b)

December 31, 2015

Depreciation Expense ……………………………………………..

46,256

Accumulated Depreciation—Equipment

[($317,533 – $40,000) ÷ 6] …………………………..

46,256

Interest Expense …………………………………………………….

Discount on Notes Payable …………………………..

25,403

Schedule of Note Discount Amortization

Date

Debit, Interest Expense Credit,

Discount on Notes Payable

Carrying Amount

of Note

12/31/15

12/31/16

12/31/17

*$1 adjustment due to rounding.

(c)

December 31, 2016

Depreciation Expense ……………………………………………..

46,256

Accumulated Depreciation—Equipment …………..

46,256

Discount on Notes Payable …………………………..

27,435

PROBLEM 14-9B

(a)

12/31/13

Machinery ……………………………………………………….

533,139

Discount on Notes Payable …………………………..

66,861

Cash ……………………………………………………….

100,000.00

Notes Payable …………………………..

[To record machinery at the

present value of the note plus

the immediate cash payment:

PV of $125,000 annuity @ 6%

for 4 years ($125,000 X

3.46511)] ………………………………………………………

$433,139

Down payment…………………………..

100,000

Capitalized value of

Machinery …………………………..

$533,139

(b)

12/31/14

Notes Payable ……………………………………………………….

125,000.00

Cash ……………………………………………………….

125,000.00

Interest Expense …………………………..

25,988

Discount on Notes Payable …………………………..

Schedule of Note Discount Amortization

Date

Cash Paid

Interest

Expense

Amortization

Carrying

Amount of Note

12/31/13

$433,139

12/31/14

$125,000

$25,988

$99,012

334,127

12/31/15

12/31/16

12/31/17

*$1 adjustment due to rounding.

PROBLEM 14-9B (Continued)

(c)

12/31/15

Notes Payable ……………………………………………………….

125,000

Cash ……………………………………………………….

125,000

Interest Expense …………………………..

20,048

Discount on Notes Payable …………………………..

20,048

(d)

Notes Payable ……………………………………………………….

125,000

Cash ……………………………………………………….

125,000

Interest Expense …………………………..

13,750

Discount on Notes Payable …………………………..

13,750

(e)

12/31/17

Notes Payable ……………………………………………………….

125,000

Cash ……………………………………………………….

125,000

Interest Expense …………………………..

Discount on Notes Payable …………………………..

PROBLEM 14-10B

(a)

Lauderdale Co.

Selling price of the bonds ($2,000,000 X 105%) ……

$2,100,000

Accrued interest from January 1 to April 30,

2015 ($2,000,000 X 8% X 4/12) ………………………….

Total cash received from issuance of the bonds ….

Less: Bond issuance costs ………………………………..

Net amount of cash received ………………………………

(b)

Fort Co.

Carrying amount of the bonds on 1/1/14 ……………..

$692,639

Effective-interest rate (8%) …………………………………

X 0.08

Interest expense to be reported for 2014 …………….

$ 55,411

(c)

Lauderhill Co.

Maturities and sinking fund requirements on long-term debt for

(d)

Pompano Inc.

Only the $4,000,000 in unsecured serial bonds are reported as

PROBLEM 14-11B

Dear Alicia,

When a bond is issued at face value, the annual interest expense and the

interest payout equals the face value of the bond times the interest rate

stated on its face. However, if the bond is issued to yield a higher or lower

amortization.

One method of amortization is the straight–line method whereby the amount of

the premium or discount is divided by the number of interest periods in the

bond’s life. The result is an even amount of amortization for every period.

However, a better way of recording interest expense in the period during

which it is incurred is the effective–interest method. Assume a discount: the

To amortize the discount applying this method to the data provided, you

must know the bond’s face amount, its stated rate of interest, its effective

rate of interest, and its premium.

1. Multiply the stated rate times the face amount. This is the interest

payout.

PROBLEM 14-11B (Continued)

3. Subtract the amount calculated in #1 from that found in #2. This is the

amount to be amortized for the period.

4. Add the difference computed in #3 to the carrying amount. The

process begins all over when you apply the effective rate to this new

carrying amount for the following period.

The schedule below illustrates this calculation. The face value ($5,000,000)

is multiplied by the stated rate of 8 percent, while the carrying amount

($4,613,913) is multiplied by the effective rate of 10 percent. Because this

Attachment to letter

SCRIBNER COMPANY

Interest and Discount Amortization Schedule

8% Bond Issued to Yield 10%

Date

Cash

Paid

(8%)

Interest

Expense

(10%)

Premium

Amortized

Carrying

Amount of

Bond

6/30/14

$4,613,913

12/31/14

$200,000

$230,696

$30,696

4,644,609

*PROBLEM 14-12B

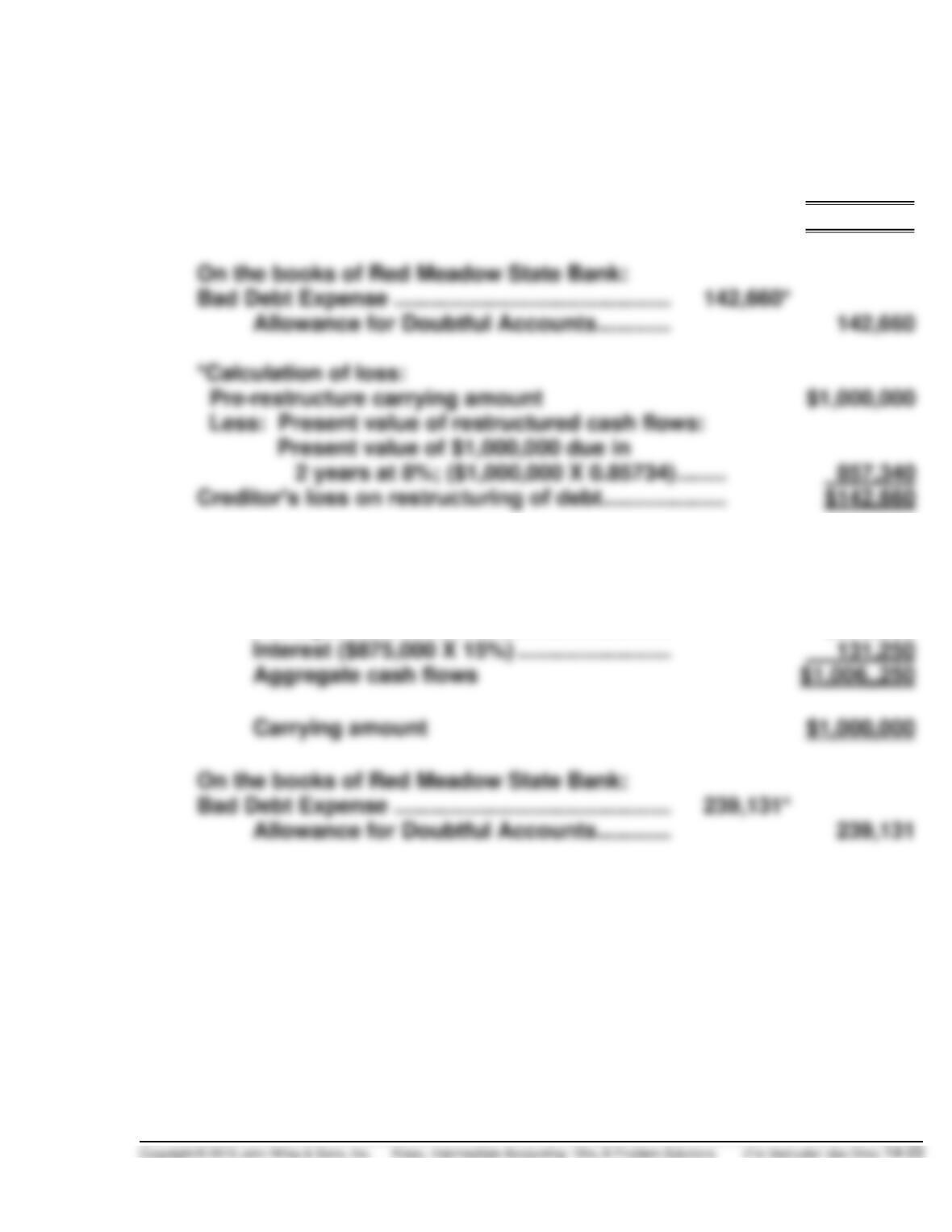

(a) It is a troubled debt restructuring.

(b)

1. No entry.

2. Bad Debt Expense …………………………..……………..

226,011*

Allowance for Doubtful Accounts ……………..

226,011

*Calculation of loss.

Pre-restructure carrying amount

$500,000

Present value of restructured cash flows:

Creditor’s loss on restructuring of debt ……………………

$226,011

(c) Losses are calculated based upon the discounted present value of

future cash flows. However, the debtor’s gain is calculated using the

*PROBLEM 14-13B

(a)

On the books of Pinker Corporation:

Notes payable …………………………..…………………………..

1,000,000

Common Stock …………………………..…………………..

50,000

Gain on Restructuring of Debt …………………………

200,000

Fair value of equity …………………………..

Gain on restructuring

On the books of Red Meadow State Bank:

Equity Investments …………………………………………………

Allowance for Doubtful Accounts …………………………..

Notes Receivable ……………………………………………

(b)

On the books of Pinker:

Notes Payable ……………………………………………………….

1,000,000

Land ……………………………………………………….

500,000

Gain on Disposal of Plant Assets …………………….

400,000

Gain on Restructuring of Debt …………………………

100,000

Fair value of land …………………………..

Book value of land …………………………..

Gain on disposal of

Note payable (carrying

amount) …………………………..

Gain on restructuring

On the books of Red Meadow State Bank:

Land ………………………………………………………………………

Allowance for Doubtful Accounts …………………………..

*PROBLEM 14-13B (Continued)

(c)

On the books of Pinker:

No entry is needed because aggregate cash flows equal

the carrying amount.

Aggregate cash flows—principal ……………………..

$1,000,000

Carrying amount …………………………………………….

$1,000,000

Bad Debt Expense ………………………………………………….

*Calculation of loss:

Present value of $1,000,000 due in

(d)

On the books of Pinker:

No entry is needed because aggregate cash flows

exceed the carrying amount.

Principal ……………………………………………………….

$875,000

Aggregate cash flows

Carrying amount

$1,000,000

Allowance for Doubtful Accounts …………………….

*PROBLEM 14-13B (Continued)

*Calculation of loss:

Pre-restructure carrying amount …………………………..

$1,000,000

Present value of restructured cash flows:

Present value of $875,000 due in

2 years at 15%, interest payable

(Table 6-2);

Annually; ($875,000 X 0.75614) ……………………..

Present value of $131,250 interest

payment at end of year 2 at 15%;

($131,250 X 0.75614) …………………………..

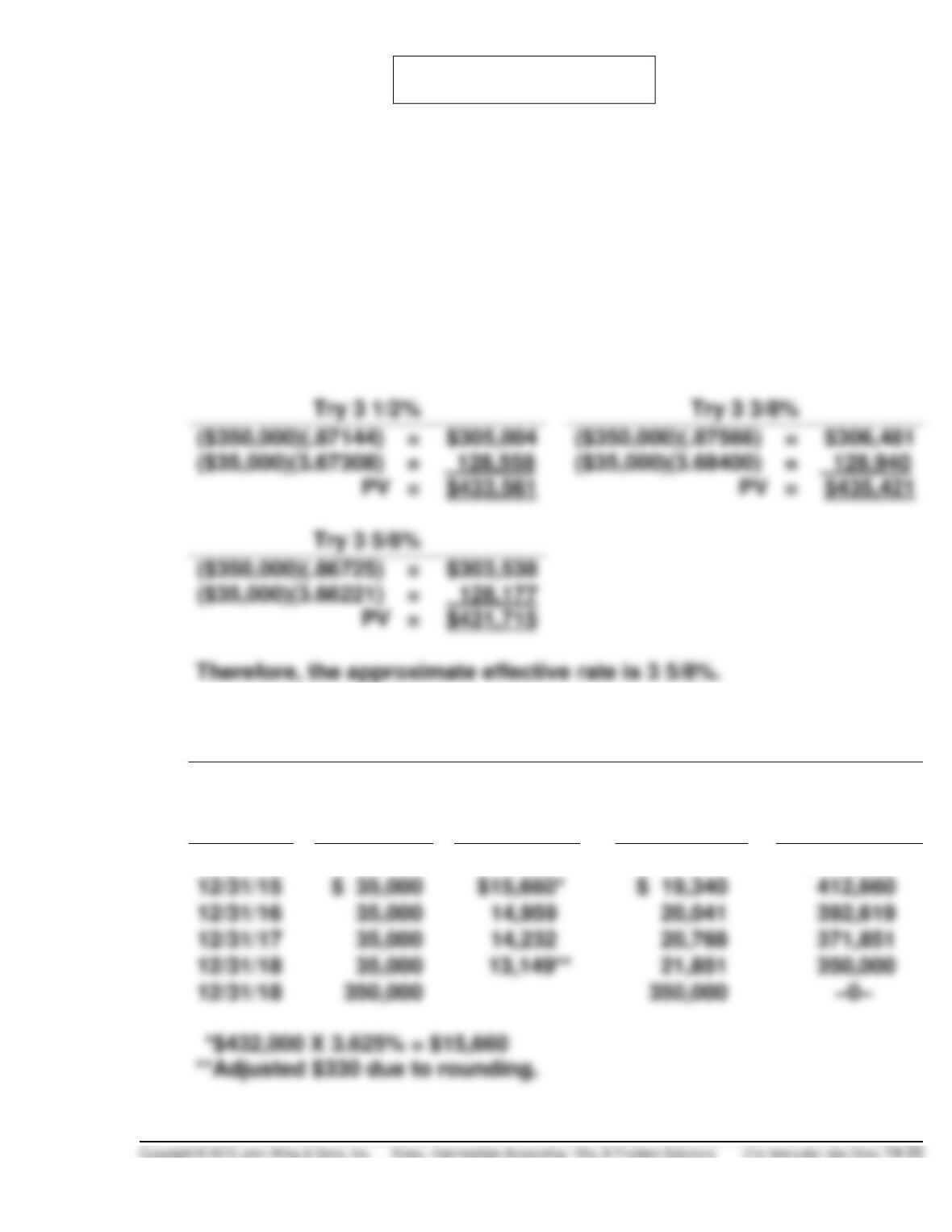

*PROBLEM 14-14B

Carrying amount of the debt at date of restructure, $400,000 + $32,000 =

$432,000. Total future cash flow, $350,000 + ($350,000 X 0.10 X 4) =

$490,000. Because the future cash flow exceeds the carrying amount of the

debt, no gain is recognized at the date of restructure.

(a) The effective-interest rate subsequent to restructure is computed by

trial and error using present value tables based on the present value

of $350,000 (new principal) plus $35,000 (interest per year) for four

years to equal $432,000.

(b) SCHEDULE OF DEBT REDUCTION

AND INTEREST EXPENSE AMORTIZATION

Date

Cash

Paid

Interest

Expense

Premium

Amortized

Carrying

Amount of

Note

12/31/14

$432,000

12/31/17

*PROBLEM 14-14B (Continued)

(c)

Calculation of loss:

Pre-restructure carrying amount …………………………..

$432,000

Present value of restructured cash flows:

Present value of $350,000 due in 4 years

at 10% , interest payable annually;

($350,000 X 0.68301) …………………………………….

Present value of $35,000 interest payable

annually for 4 years at 10% ;

($35,000 X 3.16987) ………………………………………

*Although the sum of the present value amounts is $340,999, the true

present value of a 10% note discounted at 10% is face value, or

$350,000. The $1 difference is due to rounding.

Date

Cash

Received

Interest

Revenue

Change in

Carrying

Amount

Carrying

Amount of

Note

12/31/14

$350,000

12/31/15

$ 35,000a

$35,000b

$ 0

350,000c

12/31/16

12/31/17

0

12/31/18

0

12/31/18

(d)

Skilhill Corp. entries:

December 31, 2014

Interest Payable ………………………………………………………

32,000

Notes Payable ………………………………………………..

32,000

December 31, 2015

Interest Expense …………………………………………………….

Notes Payable ……………………………………………………….

Cash ……………………………………………………….

35,000

*PROBLEM 14-14B (Continued)

December 31, 2016

Interest Expense …………………………………………………….

14,959

Notes Payable ……………………………………………………….

20,041

Cash ……………………………………………………….

305,000

December 31, 2014

(e)

Bad Debt Expense ………………………………………………….

Allowance for Doubtful Accounts …………………….

Cash ………………………………………………………………………

Interest Revenue …………………………………………….