PROBLEM 10-6

INTEREST CAPITALIZATION

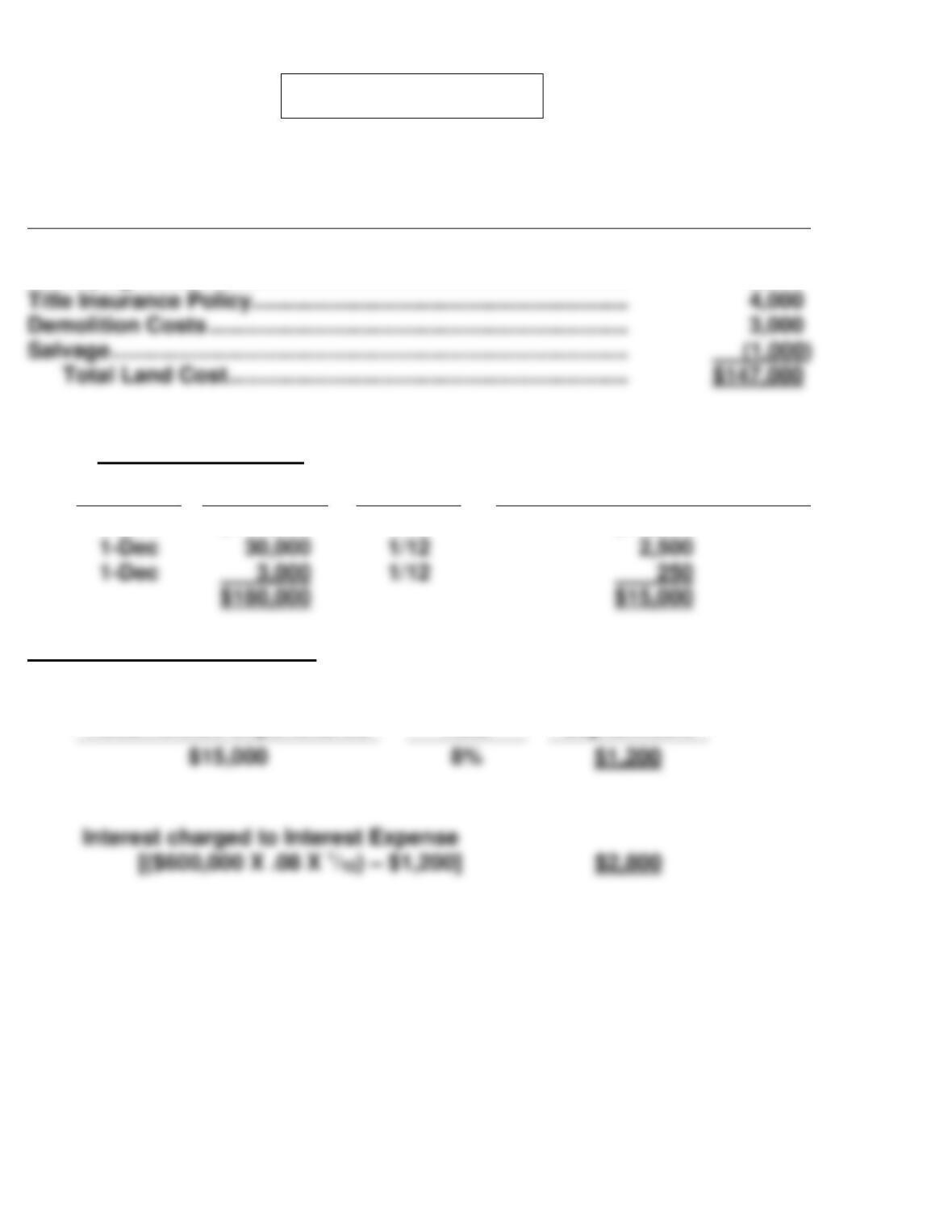

Balance in the Land Account

Purchase Price ……………………………………………………………..

$139,000

Surveying Costs ……………………………………………………………

2,000

Expenditures (2012)

Weighted—Average

Accumulated Expenditures

Date

Amount

Fraction

1-Dec

$147,000

1/12

$12,250

Interest Capitalized for 2012

Weighted—Average

Accumulated Expenditures

Interest

Rate

Amount

Capitalizable

Title Insurance Policy …………………………………………………….

4,000

Salvage …………………………………………………………………………

PROBLEM 10-6 (Continued)

Expenditures (2013)

Fraction

Weighted

Expenditure

Date

Amount

1-Jan

$180,000

6/12

$ 90,000

Interest Capitalized for 2013

Weighted-

Average

Expenditure

Interest

Rate

Amount

Capitalizable

$225,600

(a) Balance in Land Account—2012 and 2013 …….. 147,000

(b) Balance in Building—2012 …………………………... 34,200*

4/12

80,000

PROBLEM 10-7

(a) Computation of Weighted-Average Accumulated Expenditures

Expenditures

Date

Amount

X

Capitalization

Period

=

Weighted-Average

Accumulated Expenditures

(b)

Weighted-Average

Accumulated Expenditures

X

Weighted-Average

Interest Rate

=

Avoidable

interest

$1,250,000

11.2%*

$140,000

(c) (1) and (2)

Total actual interest cost

$560,000

Total interest capitalized

$140,000

Total interest expensed

$420,000

July 30, 2012

January 30, 2013

PROBLEM 10-8

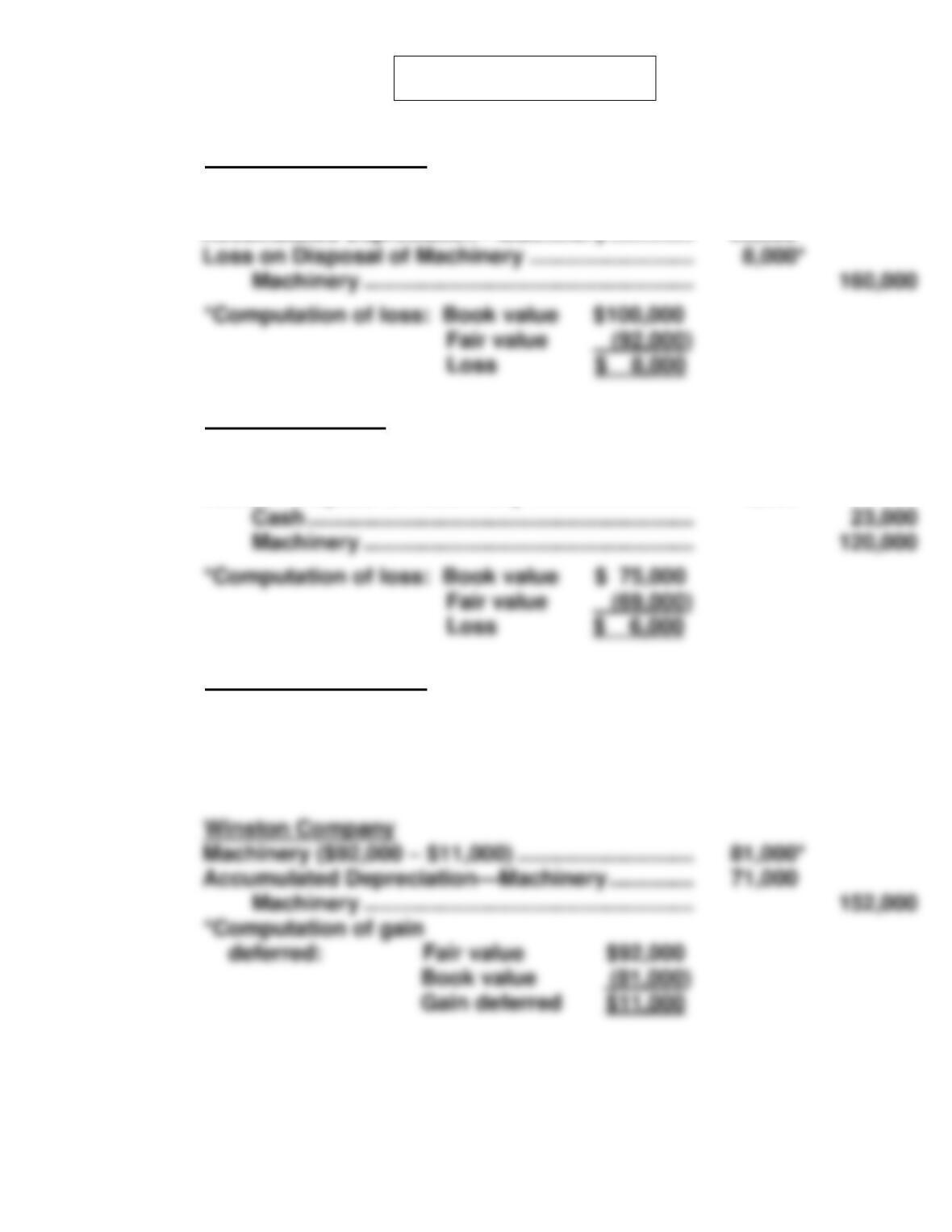

1.

Holyfield Corporation

Cash ………………………………………………………………

23,000

Machinery ………………………………………………………

69,000

Accumulated Depreciation—Machinery ……………

60,000

Dorsett Company

Machinery ………………………………………………………

92,000

Accumulated Depreciation—Machinery ……………

45,000

Loss on Disposal of Machinery ……………………….

6,000*

Cash ……………………………………………………….

Machinery ……………………………………………….

Fair value

2.

Holyfield Corporation

Machinery ………………………………………………………

92,000

Accumulated Depreciation—Machinery ……………

60,000

Loss on Disposal of Machinery ……………………….

8,000

Machinery ……………………………………………….

160,000

Winston Company

Machinery ($92,000 – $11,000) …………………………

81,000*

Accumulated Depreciation—Machinery ……………

71,000

Book value

Loss on Disposal of Machinery ……………………….

Machinery ……………………………………………….

Fair value

PROBLEM 10-8 (Continued)

3.

Holyfield Corporation

Machinery ………………………………………………………

95,000

Liston Company

Machinery ………………………………………………………

92,000

Accumulated Depreciation—Machinery ……………

75,000

Cash ………………………………………………………………

Machinery ……………………………………………….

*Fair value

Book value

Because the exchange has commercial substance, the entire gain

should be recognized.

4.

Holyfield Corporation

Machinery ………………………………………………………

185,000

Accumulated Depreciation—Machinery ……………

60,000

Loss on Disposal of Machinery ………………………..

Machinery ……………………………………………….

Cash ……………………………………………………….

Greeley Company

Cash ………………………………………………………………

93,000

Inventory ……………………………………………………….

92,000

Sales Revenue …………………………………………

Cost of Goods Sold …………………………………………

Inventory …………………………..…………………….

Accumulated Depreciation—Machinery ……………

60,000

Loss on Disposal of Machinery ………………………..

Machinery ……………………………………………….

Cash ……………………………………………………….

PROBLEM 10-9

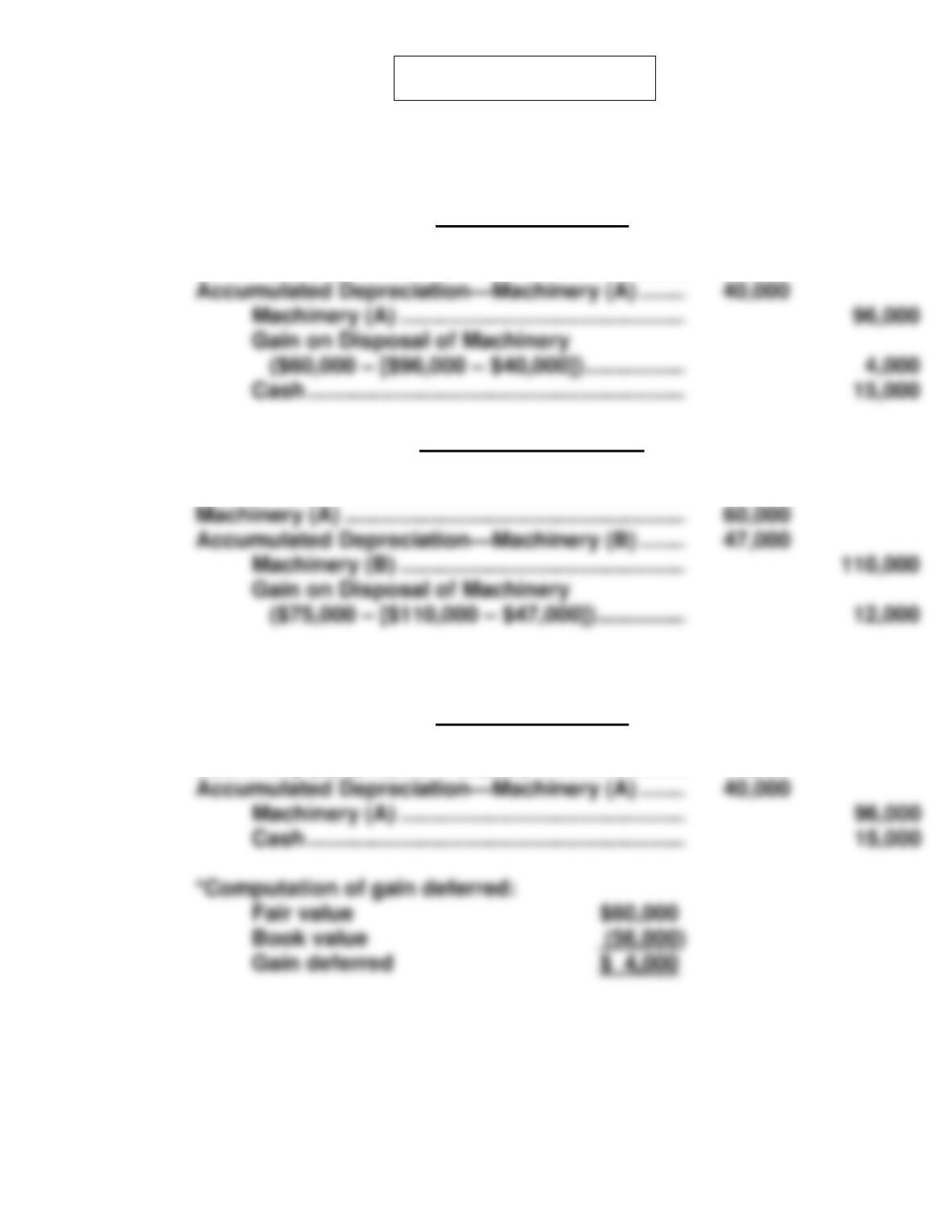

(a) Exchange has commercial substance:

Hyde, Inc.’s Books

Machinery (B) ………………………………………………….

75,000

Wiggins, Inc.’s Books

Cash ……………………………………………………………….

15,000

Accumulated Depreciation—Machinery (B) ……….

47,000

Machinery (B) …………………………..……………..

($75,000 – [$110,000 – $47,000]) ……………..

(b) Exchange lacks commercial substance:

Hyde, Inc.’s Books

Machinery (B) ($75,000 – $4,000) ………………………

71,000*

Accumulated Depreciation—Machinery (A) ……….

40,000

Cash ……………………………………………………….

Fair value

Book value

Machinery (A) …………………………..……………..

Gain on Disposal of Machinery

Cash ……………………………………………………….

PROBLEM 10-9 (Continued)

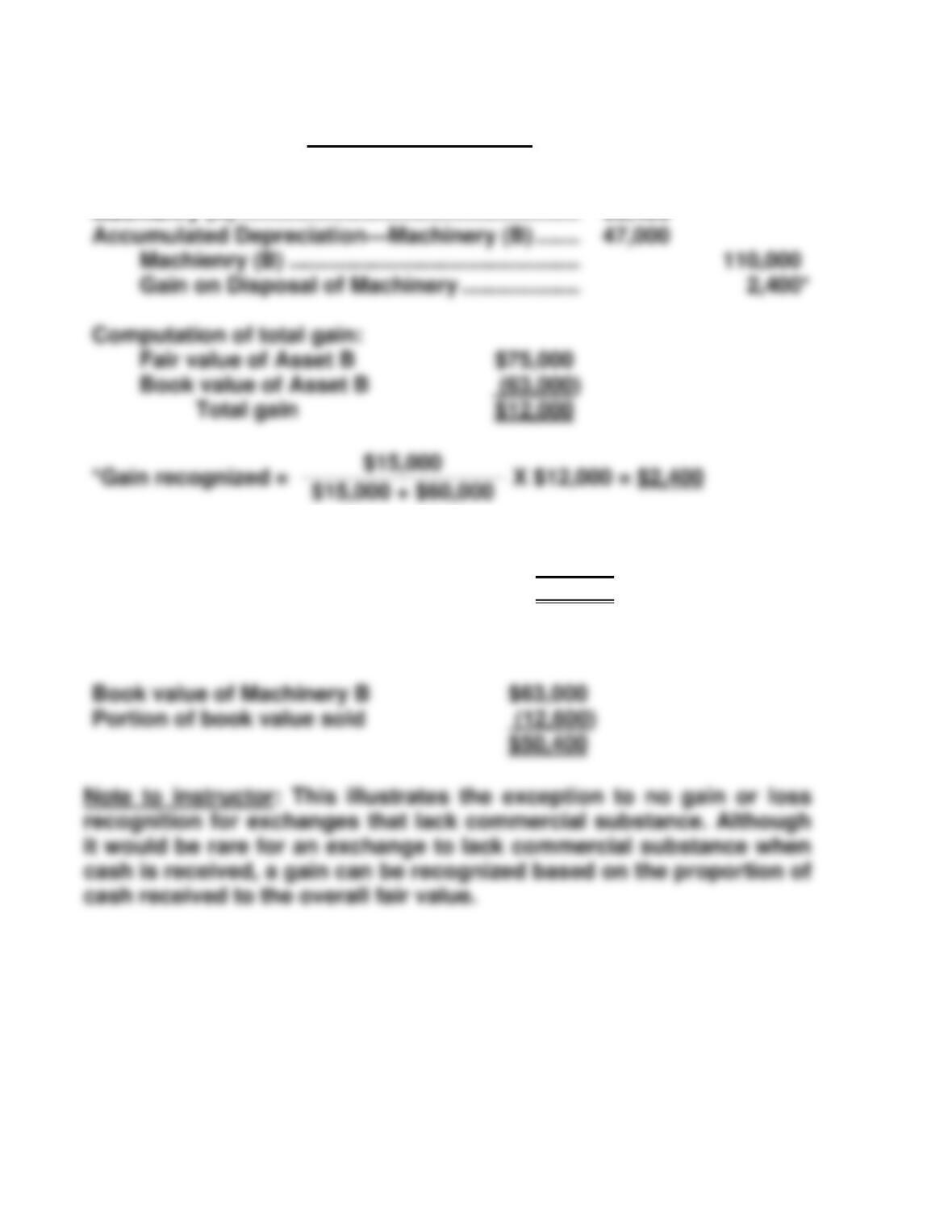

Wiggins, Inc.’s Books

Cash ………………………………………………………………

15,000

Machienry (A) …………………………………………………

50,400**

**Fair value of asset acquired

$60,000

Less: Gain deferred ($12,000 – $2,400)

9,600

Basis of Machinery A

$50,400

OR

Book value of Machinery B

Portion of book value sold

Accumulated Depreciation—Machinery (B) ………

47,000

Machienry (B) ………………………………………….

Gain on Disposal of Machinery …………………

Computation of total gain:

Fair value of Asset B

Book value of Asset B

Total gain

PROBLEM 10–10

(a) Has Commercial Substance

Marshall Construction

1.

Equipment ($82,000 + $118,000)………………….

200,000

Accumulated Depreciation—Equipment ……..

50,000

Brigham Manufacturing

2.

Cash …………………………………………………………

118,000

Inventory …………………………………………………..

82,000

Sales Revenue …………………………………..

Cost of Goods Sold ……………………………………

Inventory …………………………………………..

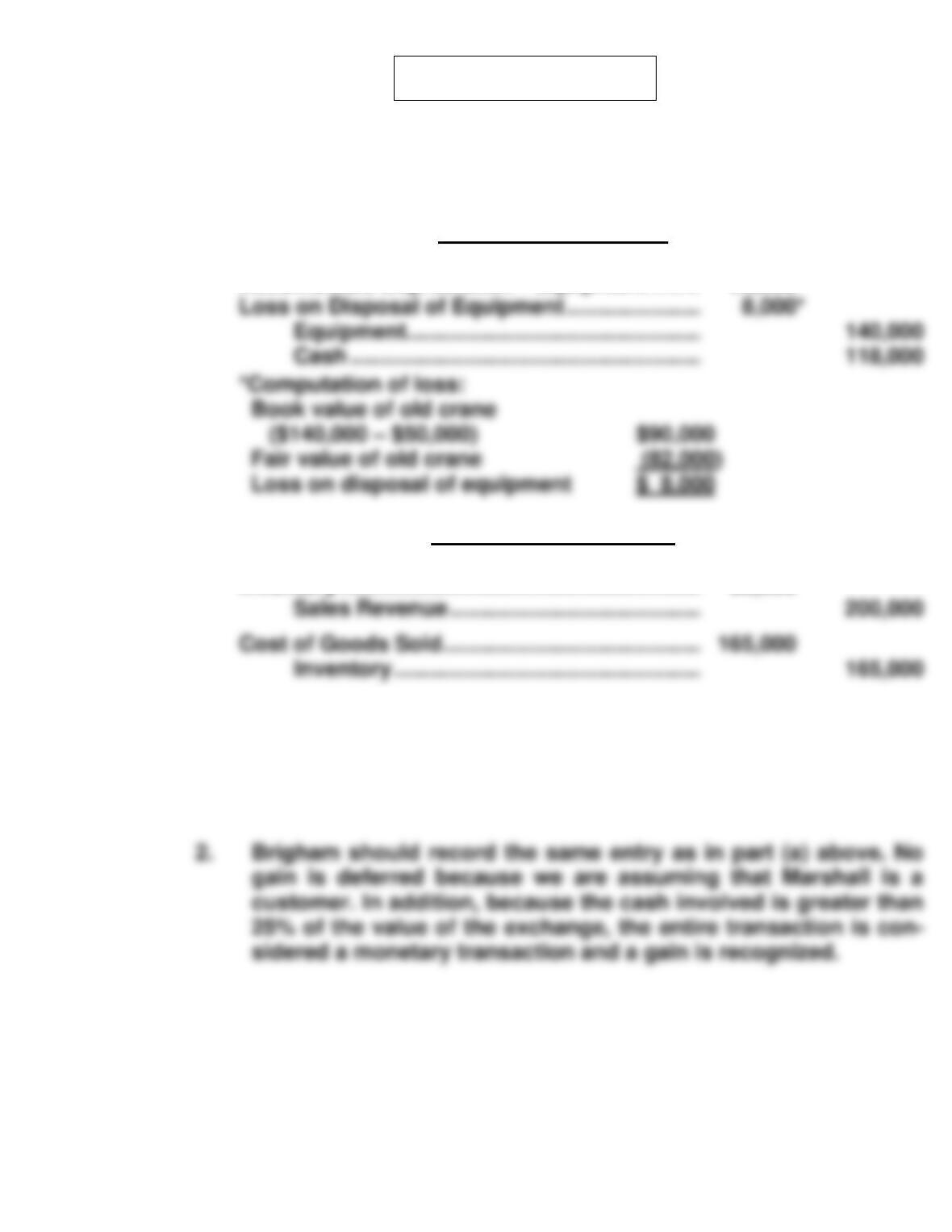

(b) Lacks Commercial Substance

1. Marshall Construction should record the same entry as in part (a)

above, since the exchange resulted in a loss.

Loss on Disposal of Equipment ………………….

Equipment…………………………………………

Cash …………………………………………………

PROBLEM 10-10 (Continued)

(c) Has Commercial Substance

Marshall Construction

1.

Equipment ($98,000 + $102,000) ………………….

200,000

Accumulated Depreciation—Equipment ……..

50,000

Equipment …………………………………………

140,000

Brigham Manufacturing

2.

Cash ………………………………………………………..

102,000

Inventory ………………………………………………….

98,000

Sales Revenue ………………………………….

200,000

Cost of Goods Sold …………………………………..

165,000

Inventory ………………………………………….

165,000

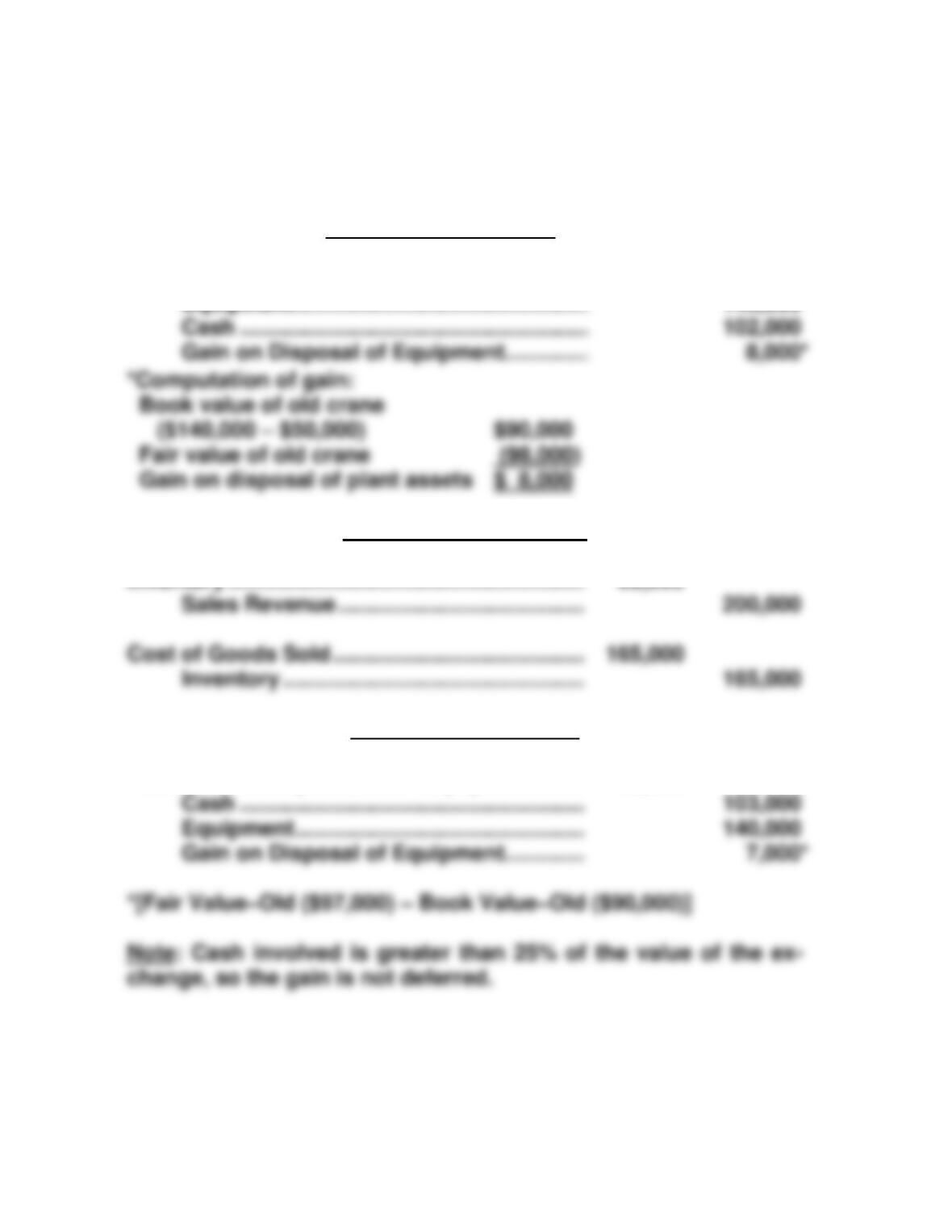

(d)

Marshall Construction

1.

Equipment ………………………………………………..

200,000

Accumulated Depreciation—Equipment …….

50,000

Cash ………………………………………………..

Equipment ………………………………………..

140,000

Gain on Disposal of Equipment ………….

change, so the gain is not deferred.

Cash …………………………………………………

Gain on Disposal of Equipment …………..

PROBLEM 10-10 (Continued)

Brigham Manufacturing

2.

Cash ……………………………………………………….

103,000

Inventory ………………………………………………….

97,000

Sales Revenue ………………………………….

200,000

Cost of Goods Sold …………………………………..

Inventory ………………………………………….

165,000

PROBLEM 10-11

(a) The major characteristics of plant assets, such as land, buildings, and

equipment, that differentiate them from other types of assets are

presented below.

1. Plant assets are acquired for use in the regular operations of the

enterprise and are not for resale.

2. Property, plant, and equipment possess physical substance or

(b) Transaction 1. To properly reflect cost, assets purchased on deferred

payment contracts should be accounted for at the present value of the

consideration exchanged between the contracting parties at the date

of the consideration. When no interest rate is stated, interest must

be imputed at a rate that approximates the rate that would be negoti–

ated in an arm’s-length transaction. In addition, all costs necessary to

PROBLEM 10-11 (Continued)

Transaction 2. The lump-sum purchase of a group of assets should be

accounted for by allocating the total cost among the various assets

on the basis of their relative fair values. The $8,000 of interest

expense incurred for financing the purchase is a period cost and is

not a factor in determining asset cost.

(c) 1. A building purchased for speculative purposes is not a plant

asset as it is not being used in normal operations. The building

is more appropriately classified as an investment.

2. The two-year insurance policy covering plant equipment is not a

plant asset because it has no physical substance and is not