EXERCISE 16-8 (10–15 minutes)

SANDS COMPANY

Journal Entry

September 1, 2014

Cash ……………………………………………………………….. 4,220,000

Unamortized Bond Issue Costs…………………………. 30,000

Bonds Payable (4,000 X $1,000) ………………….. 4,000,000

Schedule 1

Premium on Bonds Payable and Value of Stock Warrants

Sales price (4,000 X $1,040) $4,160,000

Less: Face value of bonds 4,000,000

160,000

Schedule 2

Accrued Bond Interest to Date of Sale

Face value of bonds $4,000,000

Interest rate X 9%

Annual interest $ 360,000

Accrued interest for 3 months – ($360,000 X 3/12) $ 90,000

EXERCISE 16-9 (Continued)

(b) Market value of bonds without warrants $1,960,000

($2,000,000 X .98)

Market value of warrants (2,000 X $30) 60,000

Total market value $2,020,000

EXERCISE 16-10 (15–25 minutes)

1/2/15 No entry (total compensation cost is $450,000)

1/3/17 Cash (20,000 X $40) ……………………………… 800,000

Paid-in Capital—Stock Options …………….. 300,000

($450,000 X 20,000/30,000)

EXERCISE 16-10 (Continued)

(Note to instructor: The market price of the stock has no relevance in the

prior entry and the following one.)

5/1/17 Cash (10,000 X $40) ……………………………………. 400,000

Paid-in Capital—Stock Options …………………… 150,000

EXERCISE 16-11 (15–25 minutes)

1/1/15 No entry

12/31/15 Compensation Expense ……………………………… 175,000

compensation expense for 2015)

4/1/16 Paid-in Capital—Stock Options …………………… 17,500

Compensation Expense ……………………. 17,500

($175,000 X 2,000/20,000)

(To record termination of stock

options held by resigned employees)

Note: There are 6,000 options unexercised as of 3/31/17 (20,000 – 2,000 –

12,000).

EXERCISE 16-12 (15–25 minutes)

1/1/13 No entry

12/31/13 Compensation Expense ……………………….. 200,000

Paid-in Capital—Stock Options ………. 200,000

($400,000 X 1/2)

1/1/17 Paid-in Capital—Stock Options …………….. 80,000

Paid-in Capital—Expired Stock

Options ($400,000 – $320,000) …….. 80,000

EXERCISE 16-13 (10–15 minutes)

(a) 1/1/14 Unearned Compensation …………………………. 120,000

Common Stock (4,000 X $5) ……………….. 20,000

Paid-in Capital Excess of Par—

Common stock ……………………………….. 100,000

EXERCISE 16-14 (10–15 minutes)

(a) 1/1/14 Unearned Compensation …………………………. 500,000

Common Stock ($10 X 10,000) ……………. 100,000

Paid-in Capital in Excess of Par—

Common Stock ………………………………. 400,000

EXERCISE 16-15 (15–25 minutes)

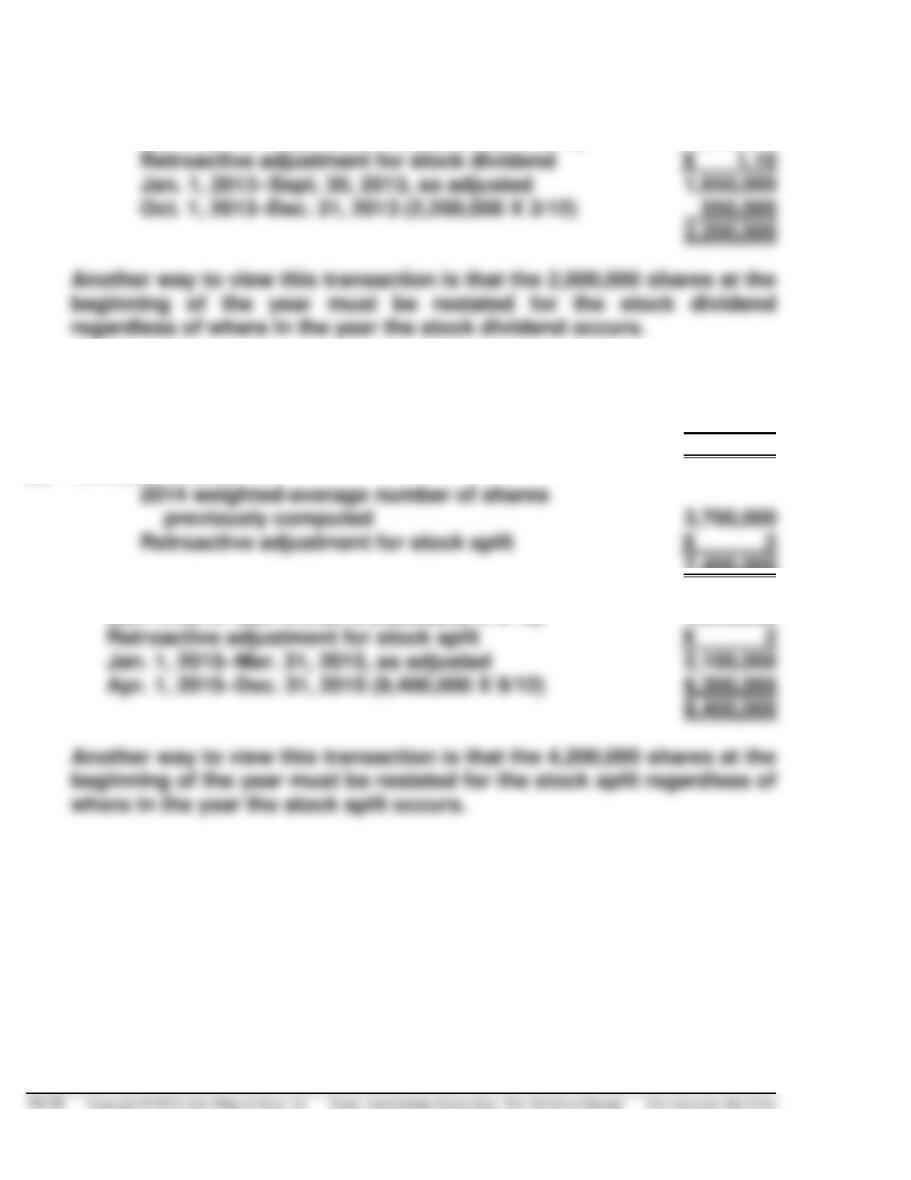

(a) 2,200,000 shares

Jan. 1, 2013–Sept. 30, 2013 (2,000,000 X 9/12) 1,500,000

(b) 3,700,000 shares

Jan. 1, 2014–Mar. 31, 2014 (2,200,000 X 3/12) 550,000

Apr. 1, 2014–Dec. 31, 2014 (4,200,000 X 9/12) 3,150,000

3,700,000

(c) 7,400,000 shares

7,400,000

(d) 8,400,000 shares

Jan. 1, 2015–Mar. 31, 2015 (4,200,000 X 3/12) 1,050,000

EXERCISE 16-16 (10–15 minutes)

(a)

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

Beginning balance

Jan. 1–Feb. 1

480,000

1.1 X 3.0

1/12

132,000

Stock dividend

Mar. 1–May 1

660,000

2/12

330,000

Stock split

June 1–Oct. 1

4/12

560,000

Reissued shares

Oct. 1–Dec. 31

3/12

435,000

1,762,000

(b)

Earnings Per Share =

$3,456,000 (Net Income)

= $1.96

1,762,000 (Weighted-average Number

Shares Outstanding)

(d) Income from continuing operationsa $1.72

Loss from discontinued operationsb (.25)

Income before extraordinary item 1.47

Extraordinary gainc .49

Net income $1.96

EXERCISE 16-17 (12–15 minutes)

Event

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

Beginning balance

Jan. 1–May 1

200,000

4/12

66,667

Issued shares

May 1–Oct. 31

208,000

6/12

Reacquired shares

Oct. 31–Dec. 31

194,000

2/12

Weighted-average number of shares outstanding

EXERCISE 16-18 (10–15 minutes)

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

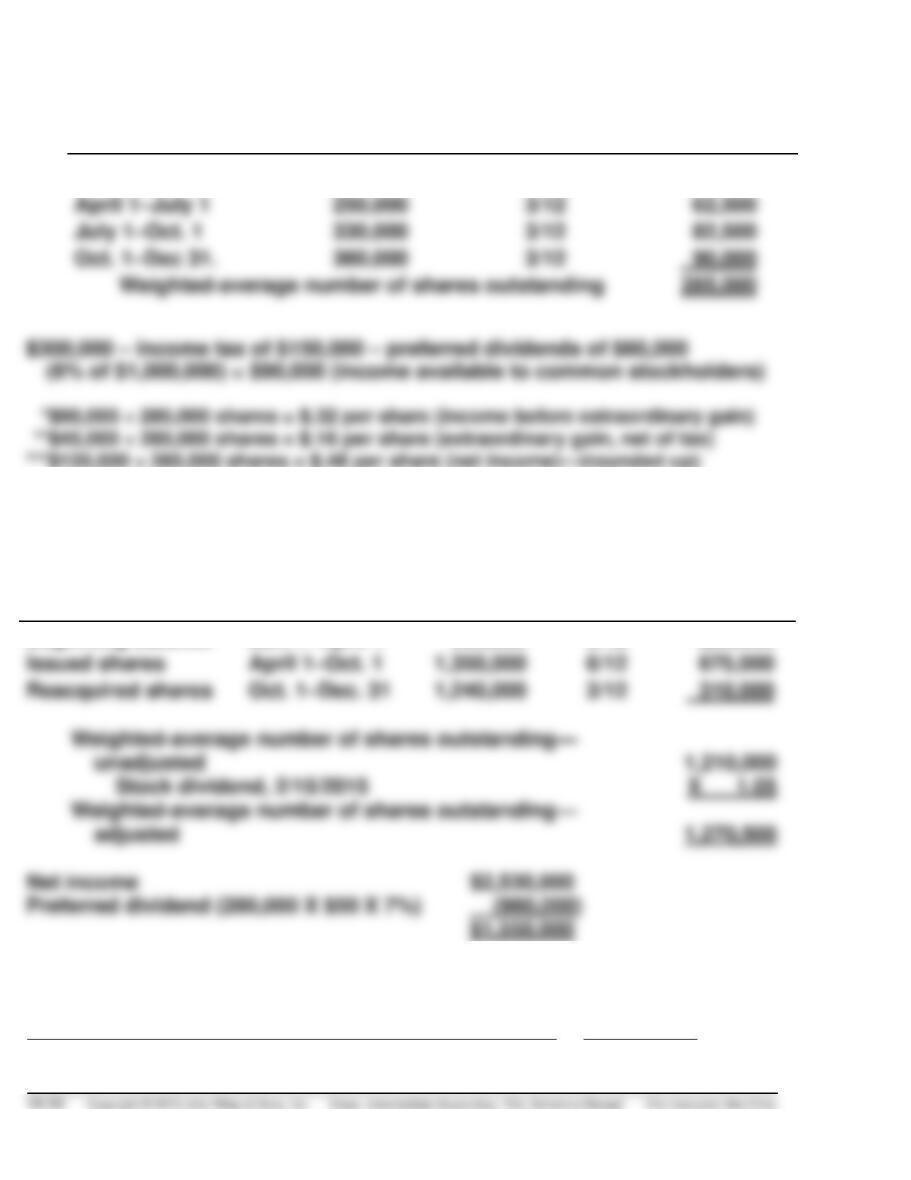

Net income $2,500,000

Preferred dividend (50,000 X $100 X 8%) (400,000)

$2,100,000

$2,100,000

EXERCISE 16-19 (20–25 minutes)

Earnings per share of common stock:

Income data:

Income before extraordinary item $15,000,000

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

January 1–April 1

7,500,000

3/12

1,875,000

April 1–December 31

8,500,000

9/12

6,375,000

Weighted-average number of shares outstanding

8,250,000

EXERCISE 16-20 (10–15 minutes)

Income before income tax and extraordinary items $300,000

Income taxes 150,000

EXERCISE 16-20 (Continued)

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

January 1–April 1

200,000

3/12

50,000

April 1–July 1

250,000

3/12

62,500

July 1–Oct. 1

330,000

3/12

82,500

Oct. 1–Dec 31.

360,000

3/12

Weighted-average number of shares outstanding

EXERCISE 16-21 (10–15 minutes)

Event

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

Beginning balance

Jan. 1–April 1

900,000

3/12

225,000

Issued shares

April 1–Oct. 1

6/12

675,000

Reacquired shares

Oct. 1–Dec. 31

3/12

Earnings per share for 2014:

Net income applicable to common stock

=

$1,550,000

= $1.22

Weighted-average number of shares outstanding

1,270,500

EXERCISE 16-22 (20–25 minutes)

(a) Revenues $17,500

Expenses:

(b) Revenues $17,500

Expenses:

Other than interest $8,400

(c) Revenues $17,500

Expenses:

Other than interest $8,400

Bond interest (60 X $1,000 X .08 X 1/2) 2,400

EXERCISE 16-23 (15–20 minutes)

(a) (1) Number of shares for basic earnings per share.

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

Jan. 1–April 1

200,000

April 1–Dec. 1

(2) Number of shares for diluted earnings per share:

Dates

Outstanding

Shares

Outstanding

Fraction

of Year

Weighted

Shares

Jan. 1–April 1

800,000

3/12

200,000

July 1–Dec. 31

6/12

(b) (1) Earnings for basic earnings per share:

After-tax net income $1,540,000

(2) Earnings for diluted earnings per share:

[Note to instructor: In this problem, the earnings per share computed for

basic earnings per share is $1.40 ($1,540,000 ÷ 1,100,000) and the diluted

EXERCISE 16-24 (20–25 minutes)

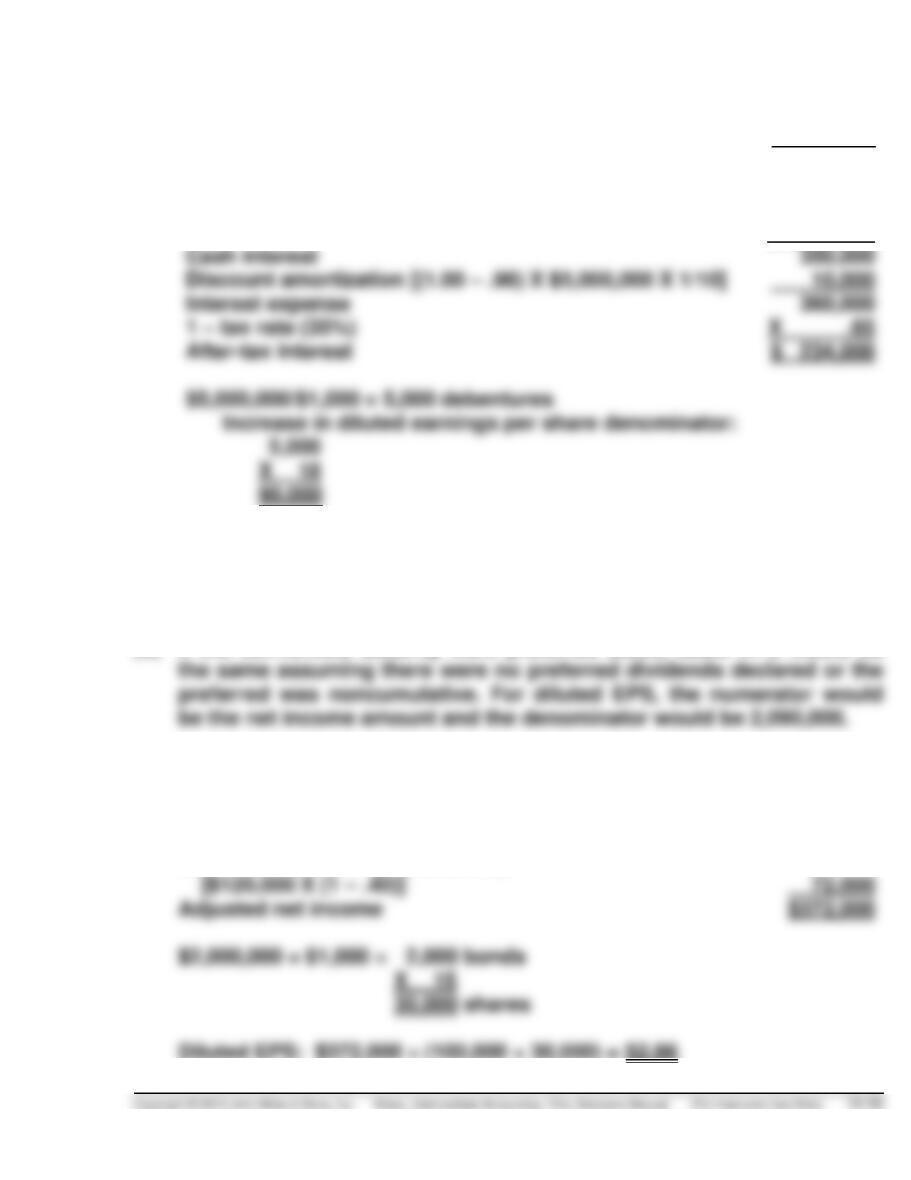

(a) Net income for year $9,500,000

Add: Adjustment for interest (net of tax) 234,000*

$9,734,000

*Maturity value $5,000,000

Stated rate X 7%

Earnings per share:

Basic EPS $9,500,000 ÷ 2,000,000 = $4.75

Diluted EPS $9,734,000 ÷ 2,090,000 = $4.66

(b) If the convertible security were preferred stock, basic EPS would be

EXERCISE 16-25 (10–15 minutes)

(a) Net income $300,000

Add: Interest savings (net of tax)

EXERCISE 16-25 (Continued)

(b) Shares outstanding 100,000

EXERCISE 16-26 (20–25 minutes)

(a) Diluted

Shares assumed issued on exercise 1,000

Proceeds (1,000 X $6 = $6,000)

(b) Diluted

Shares assumed issued on exercise 1,000

Proceeds = $6,000

EXERCISE 16-27 (10–15 minutes)

(a) The contingent shares would have to be reflected in diluted earnings

EXERCISE 16-28 (15–20 minutes)

(a) Diluted

The warrants are dilutive because the option price

($10) is less than the average market price ($15).

(b) Basic EPS = $3.60

($360,000 ÷ 100,000 shares)

16–36 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

(a) Schedule of Compensation Expense Stock Appreciation Rights (150,000)

Date

Fair

Value

Cumulative

Compensation

Recognizable

Percentage

Accrued

Compensation

Accrued to Date

Expense

2011

Expense

2012

Expense

2013

Expense

2014

12/31/11

$4

$600,000

25%

$ 150,000

$150,000

(75,000)

$(75,000)

12/31/12

1

150,000

50%

75,000

1,050,000

$1,050,000

12/31/13

10

75%

1,125,000

225,000

$225,000

12/31/14

100%

$1,350,000

*EXERCISE 16-30 (15–25 Minutes)

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 16–37

(a) Schedule of Compensation Expense Stock Appreciation Rights (30,000)

Date

Fair

Value

Cumulative

Compensation

Recognizable

Percentage

Accrued

Compensation

Accrued

to Date

Expense

2011

Expense

2012

Expense

2013

Expense

2014

Expense

2015

12/31/11

$ 6

$180,000

25%

$ 45,000

$45,000

(b)

2011

Compensation Expense ………………………………………………………….. 45,000

Liability Under Stock Appreciation Plan …………………………….. 45,000

12/31/12

50%

$202,500

12/31/13

15

75%

$(157,500)

12/31/14

100%

12/31/15

18

$540,000

TIME AND PURPOSE OF PROBLEMS

Problem 16-1 (Time 35–40 minutes)

Purpose—to provide the student with an opportunity to prepare entries to properly account for a series

Problem 16-2 (Time 45–50 minutes)

Problem 16-3 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of the entries to properly account for a stock-

Problem 16-4 (Time 25–30 minutes)

Purpose—to provide the student with an understanding of the entries to properly account for a stock

option and restricted stock plan. The student is asked to identify the important features of an employee

stock-purchase plan.

Problem 16-5 (Time 30–35 minutes)

Problem 16-6 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of the proper computation of the weighted–

Problem 16-7 (Time 35–45 minutes)

Purpose—to provide the student with an opportunity to calculate the number of shares used to compute

Problem 16-8 (Time 25–35 minutes)

Purpose—to provide the student with a problem with multiple dilutive securities which must be analyzed

to compute basic and diluted EPS.

Problem 16-9 (Time 30–40 minutes)

Purpose—to provide the student with an opportunity to calculate the weighted-average number of

SOLUTIONS TO PROBLEMS

PROBLEM 16-1

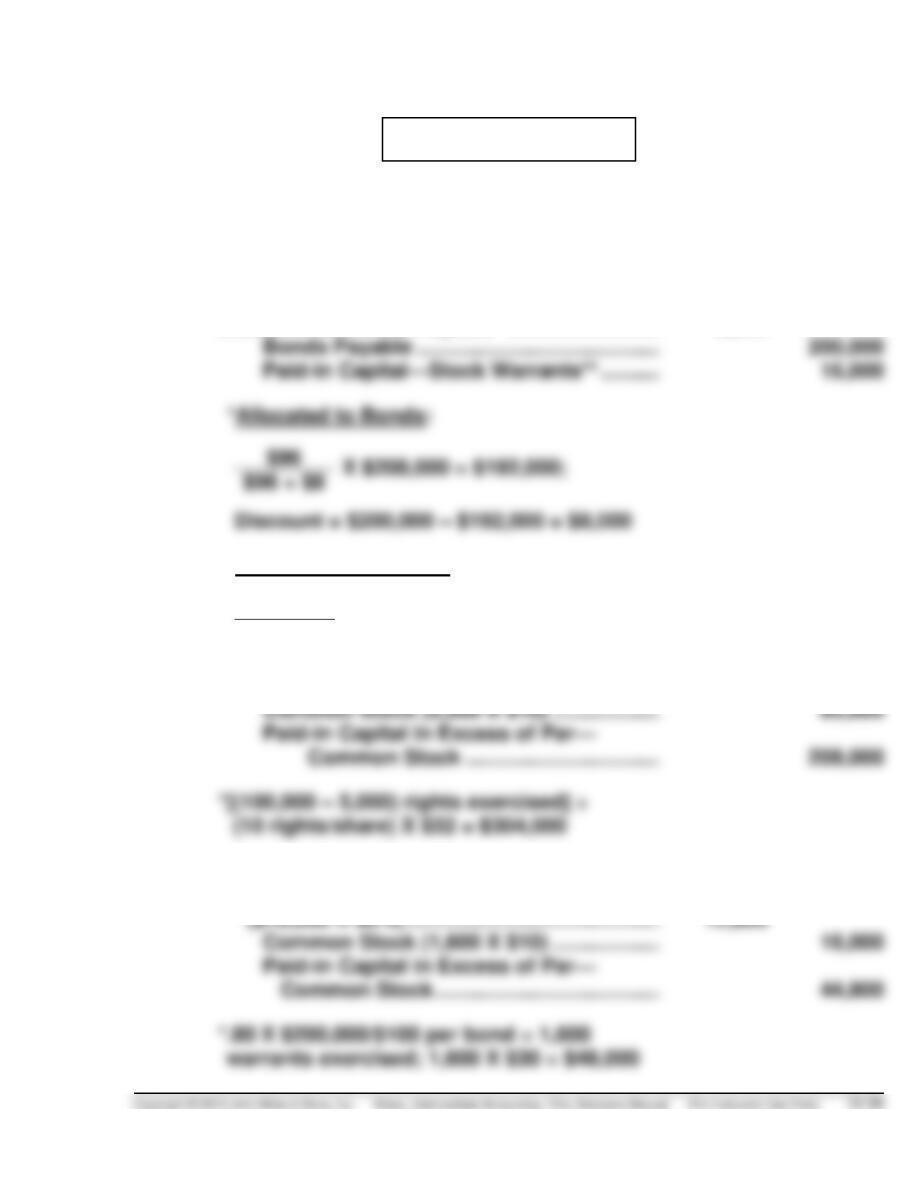

(a) 1. Memo Entry (memo entry made to indicate the number of rights

issued).

2. Cash ………………………………………………………… 208,000

Discount on Bonds Payable* …………………….. 8,000

X $208,000 = $192,000;

$96 + $8

**Allocated to Warrants:

$8

X $208,000 = $16,000

$96 + $8

3. Cash* ………………………………………………………. 304,000

4. Cash* ………………………………………………………. 48,000

Paid-in Capital—Stock Warrants

PROBLEM 16-1 (Continued)

5. Compensation Expense* ………………………….. 100,000

6. For options exercised:

Cash (9,000 X $30)……………………………………. 270,000

Paid-in Capital—Stock Options

(90% X $100,000) …………………………..………. 90,000

(b) Stockholders’ Equity:

Paid-in Capital:

Common Stock, $10 par value, authorized

1,000,000 shares, 320,100 shares

issued and outstanding ……………………. $3,201,000