PROBLEM 23-5B (Continued)

(3) Funds to redeem bonds ($300,000 X 1.01) ………..

$303,000

Face value of bonds ………………………………………..

$300,000

Unamortized discount 12/31/13 ………………………..

$6,075

Amortization to 5/31/14 not requiring cash

($9,000 ÷ 40) X 5/12 ………………………………………

Balance at date of redemption ………………….

Loss on redemption

(4) Face amount of bonds issued ………………………….

$400,000

Premium on $400,000 of bonds sold

($400,000 X 0.02) …………………………………………

$8,000

Expense of issuance ……………………………………….

1,200

Total ………………………………………………………

Amortization for seven months, which

did not require cash ……………………………..

(238)*

Amortization for seven months, which

did not require cash ……………………………..

*($8,000/235 months (a)) X 7 months = $238

**($1,200/235 months (a)) X 7 months = $35

(a) (20 years X 12 months) – 5

(5) Purchase of stock requiring cash …………………….

$146,000

60% of subsidiary’s income for year

($90,000), which did not provide

cash but was credited to income …………………..

54,000

PROBLEM 23-5B (Continued)

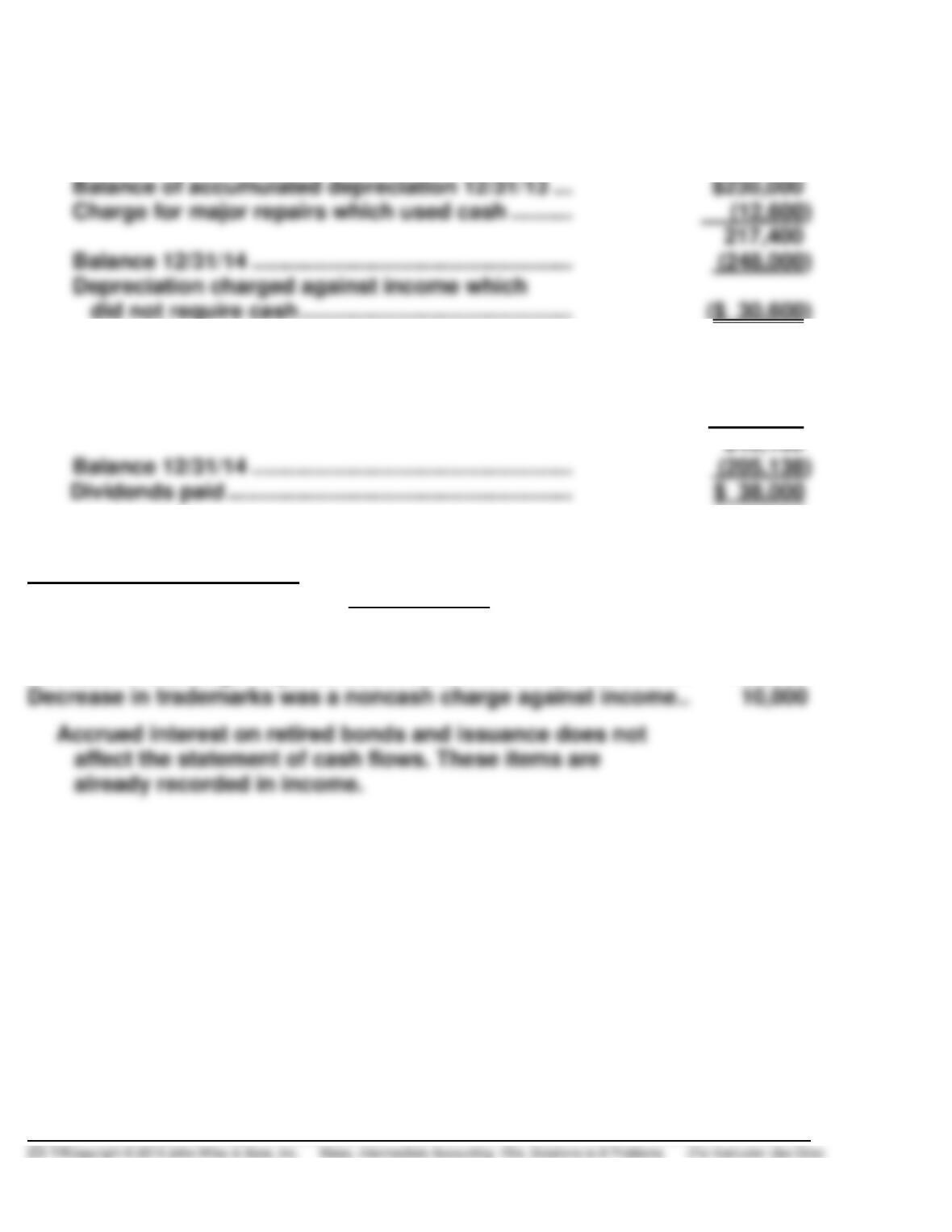

(6) Analysis of accumulated depreciation—

Building

Balance of accumulated depreciation 12/31/13 …

Charge for major repairs which used cash ……….

(12,600)

Balance 12/31/14 …………………………………………….

(248,000)

Depreciation charged against income which

did not require cash ……………………………………..

(7) Analysis of retained earnings

Balance of retained earnings 12/31/13 ………………

$166,600

Net income for current year ……………………………..

76,538

Balance 12/31/14 …………………………………………….

(205,138)

Dividends paid ………………………………………………..

Comments on Other Items

(not required)

Increase in cash surrender value of insurance required cash ……

$ 1,610

Increase in buildings required cash …………………………………………

125,000

Decrease in trademarks was a noncash charge against income ..

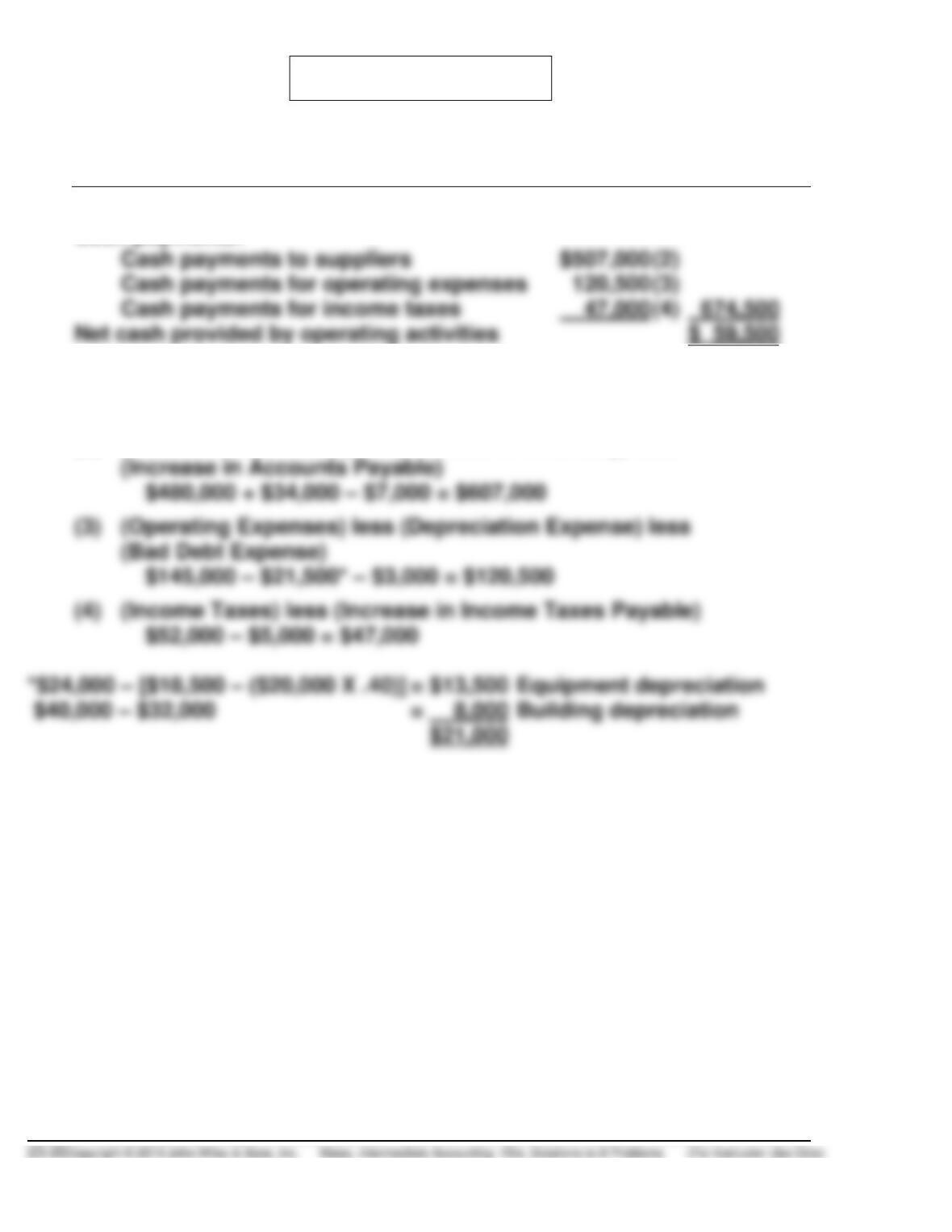

PROBLEM 23-6B

(a)

Net Cash Flow from Operating Activities

Cash received from customers ………………………..

$827,6001

Cash payments:

Cash payments to suppliers ………………………..

$541,3002

Cash payments for operating expenses ……….

*Writeoff of accounts receivable.

PROBLEM 23-6B (Continued)

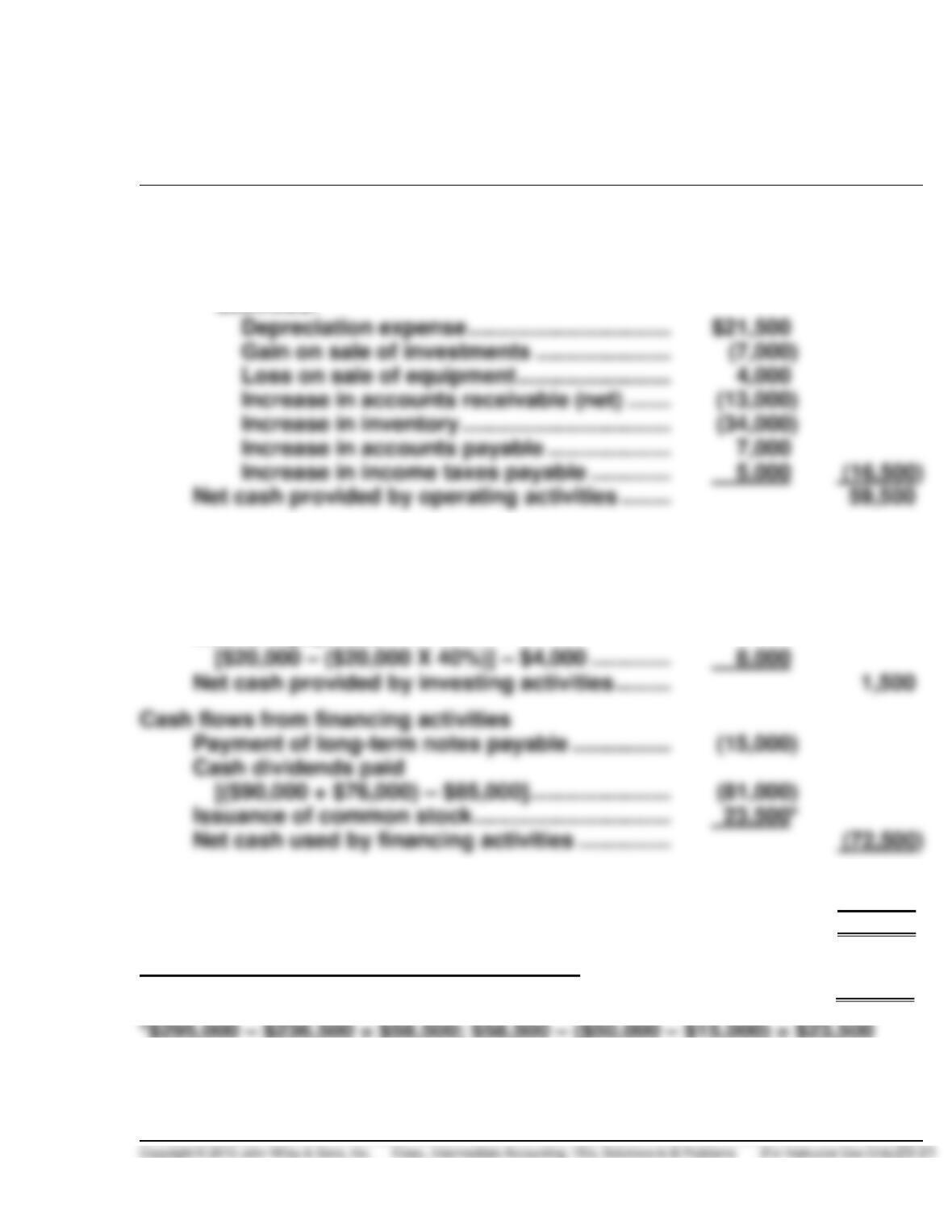

(b) EASTON INC.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………….

$71,400

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense ………………………….

Gain on sale of investments ………………..

(5,500)

Gain on sale of equipment …………………..

Increase in accounts receivable (net) …..

Decrease in inventory ………………………….

Increase in accounts payable ………………

Decr. in salaries and wages payables …..

Net cash provided by operating activities …..

Cash flows from investing activities

Purchase of equipment

$60,800 – ($41,000 – $5,400) ……………………

(25,200)

Sale of investments …………………………………..

Sale of equipment ……………………………………..

Net cash used by investing activities ………….

Reduction in long-term note payable …………

Cash dividends paid …………………………………

Net cash used by financing activities …………

Net increase in cash ……………………………………….

6,900

Cash, January 1, 2014 …………………………………….

33,600

Cash, December 31, 2014 ………………………………..

$40,500

PROBLEM 23-7B

(a) Both the direct method and the indirect method for reporting cash

flows from operating activities are acceptable in preparing a statement

of cash flows according to GAAP; however, the FASB encourages the use

(b) The Statement of Cash Flows for Cooper Company, for the year ended

October 31, 2014, using the direct method, is presented below.

COOPER COMPANY

Statement of Cash Flows

For the Year Ended October 31, 2014

Cash flows from operating activities

Cash received from customers ………………….

$1,588,800

Cash payments:

To suppliers ……………………………………..

$995,800

To employees …………………………………..

For other expenses …………………………..

For interest ……………………………………….

For income taxes ………………………………

Net cash provided by operating activities …..

Cash flows from investing activities

Purchase of plant assets…………………………...

Cash flows from financing activities

Cash received from common stock issue …..

$ 13,000

Proceeds from long-term debt ……………………

45,000

Cash paid for dividends …………………………….

Net cash used by financing activities …………

Net increase in cash ………………………………………….

Cash, November 1, 2013 ……………………………………

12,000

Cash, October 31, 2014 ……………………………………..

PROBLEM 23-7B (Continued)

Note 1: Noncash investing and financing activities:

Issuance of common stock for plant assets $25,000.

Supporting Calculations:

Cash collected from customers

Sales ……………………………………………………….

$1,600,800

Less: Increase in accounts receivable ………

12,000

Cash collected from customers ……….

$1,588,800

Cash paid to suppliers

Cost of merchandise sold …………………………

$ 980,200

Add: Increase in merchandise inventory…..

Less: Increase in accounts payable ………….

4,000

Cash paid to suppliers …………………….

$ 995,800

Cash paid to employees

Salary expense …………………………………………

$ 346,100

Add: Decrease in salaries and

wages payable …………………………………

4,800

Cash paid to employees …………………..

$ 350,900

Cash paid for other expenses

Other expenses ………………………………………..

$ 12,900

Less: Decrease in prepaid expenses ………….

5,000

Cash paid for other expenses …………..

Cash paid for interest

Interest expense ……………………………………….

$ 11,000

Less: Increase in interest payable …………….

1,800

Cash paid for interest ……………………..

$ 9,200

Cash paid for income taxes:

Income tax expense (given)……………………….

$ 73,600

PROBLEM 23-7B (Continued)

(c) The calculation of the cash flow from operating activities for Cooper

Company, for the year ended October 31, 2014, using the indirect

method, is presented below.

COOPER COMPANY

Statement of Cash Flows

For the Year Ended October 31, 2014

Cash flows from operating activities

Net income ………………………………………………..

$152,000

Depreciation expense ………………………..

Increase in accounts payable ……………..

Increase in interest payable ………………..

Decrease in prepaid expenses ……………

Increase in inventory ………………………….

Increase in accounts receivable ………….

PROBLEM 23-8B

(a) Net Cash Provided by Operating Activities

Cash receipts from customers

$734,000 (1)

Cash payments:

Cash payments to suppliers

Cash payments for operating expenses

Cash payments for income taxes

Net cash provided by operating activities

(1) (Sales) less (Increase in Accounts Receivables)

$750,000 – $16,000 = $734,000

(3) (Operating Expenses) less (Depreciation Expense) less

(2) (Cost of Goods Sold) plus (Increase in Inventory) less

PROBLEM 23-8B (Continued)

(b) HAMBLIN COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ………………………………………………….

$76,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………...

Gain on sale of investments ………………….

Loss on sale of equipment …………………….

Increase in accounts receivable (net) …….

Increase in inventory …………………………….

Increase in accounts payable ………………..

Increase in income taxes payable ………….

Net cash provided by operating activities ……..

Cash flows from investing activities

Purchase of equipment

[$60,000 – ($41,500 – $20,000)] …………………..

(38,500)

Sale of investments ($25,000 + $7,000) ………….

32,000

Net cash provided by investing activities ………

Cash flows from financing activities

Payment of long-term notes payable …………….

Issuance of common stock …………………………..

Net cash used by financing activities ……………

Sale of equipment

Net decrease in cash ……………………………………………

(11,500)

Cash, January 1, 2014 ………………………………………….

71,500

Cash, December 31, 2014 …………………………………….

$60,000

Noncash investing and financing activities

Issuance of common stock for land ………………

$35,000

PROBLEM 23-9B

(a) DINGEL CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………………. $26,000(a)

Adjustments to reconcile net income to net

cash provided by operating activities:

Cash flows from investing activities

Sale of investments …………………………………….. 12,000

Sale of equipment ………………………………………. 2,000

Purchase of equipment (cash) …………………….. (26,000)

Increase in cash ……………………………………………… 21,500

Cash, January 1, 2014 …………………………………….. 18,000

Cash, December 31, 2014 ………………………………… $39,500

Supplemental disclosures of cash flow information:

Cash paid during the year for:

PROBLEM 23-9B (Continued)

Noncash investing and financing activities:

Retired note payable by issuing common stock …….. $ 13,000

Purchased equipment by issuing notes payable …….. 23,000

Supporting Computations:

(a) Ending retained earnings ……………………………………… $45,000

Beginning retained earnings …………………………………. (35,000)

Add: Cash dividends declared ($10,000 + $6,000) …… 16,000

Net income ……………………………………………………. $26,000

(b) (1) For a severely financially troubled firm:

Operating: Probably a small cash inflow or a cash outflow.

ing funds) as a source of cash at high interest cost.

(2) For a recently formed firm which is experiencing rapid growth: