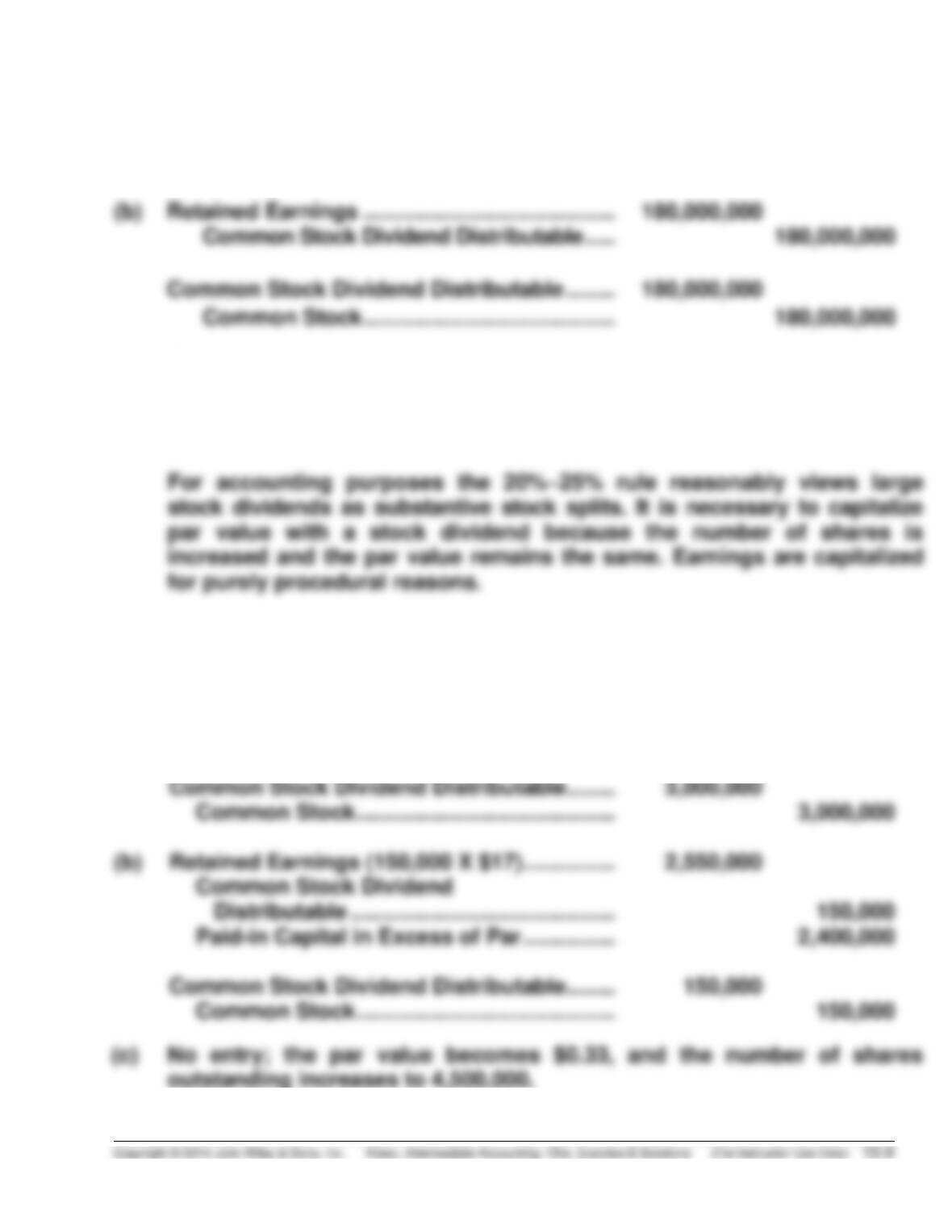

CHAPTER 15

SOLUTIONS TO B EXERCISES

E15-1B (15–20 minutes)

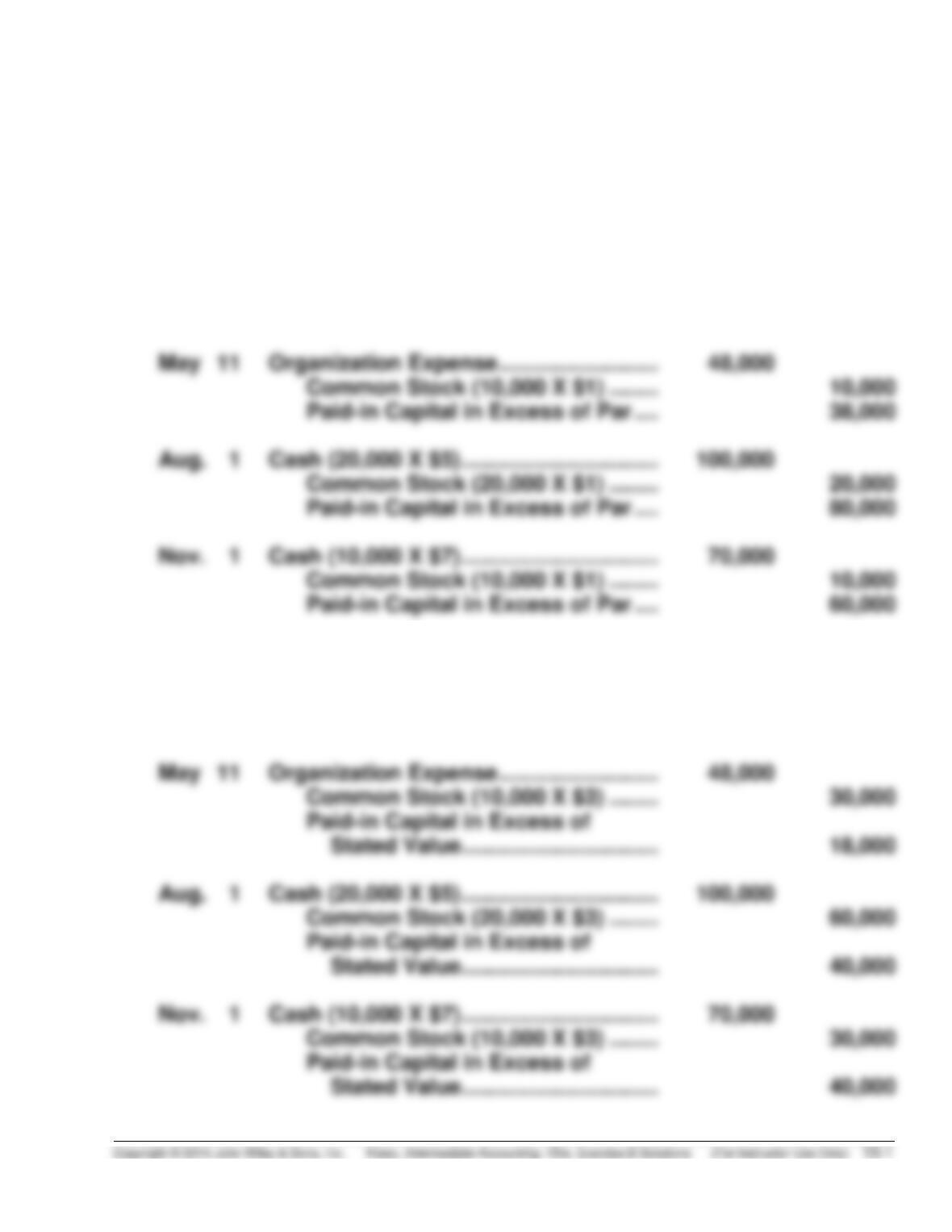

(a) Apr. 26 Cash (15,000 X $4.50) ……………………… 67,500

Common Stock (15,000 X $1) …….. 15,000

Paid-in Capital in Excess of Par …. 52,500

(b) Apr. 26 Cash (15,000 X $4.50) ……………………… 67,500

Common Stock (15,000 X $3) …….. 45,000

Paid-in Capital in Excess of

Stated Value ………………………….. 22,500

E15-2B (15–20 minutes)

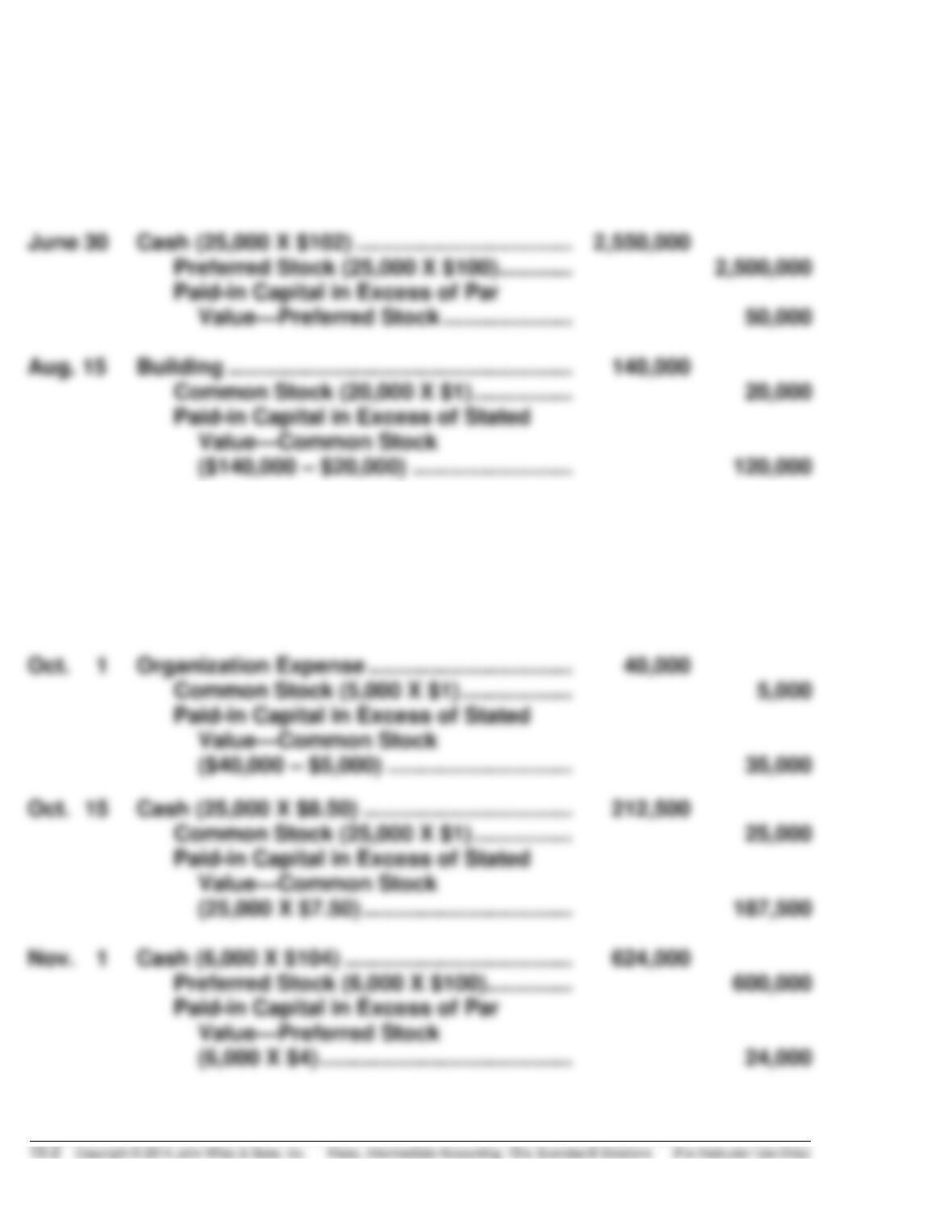

June 15 Cash (165,000 X $5) ………………………………. 825,000

Common Stock (165,000 X $1) ………….. 165,000

Paid-in Capital in Excess of Stated

Value—Common Stock ………………… 660,000

Sept. 1 Cash (200,000 X $7) ………………………………. 1,400,000

Common Stock (200,000 X $1) ………….. 200,000

Paid-in Capital in Excess of Stated

Value—Common Stock

(200,000 X $6) ………………………………. 1,200,000

E15-3B (10–15 minutes)

(a) Land ($176 X 20,000) …………………………………. 3,520,000

Treasury Stock ($153 X 20,000) …………… 3,060,000

Paid-in Capital from Treasury Stock ……. 460,000

(b) One might use the cost of treasury stock. However, this is not a relevant

measure of this economic event. Rather, it is a measure of a prior,

E15-4B (20–25 minutes)

(a) 1. Bond Issue Costs

($575,000 X $1,000/$1,150) …………………… 500,000

Cash ($1,150 X 9,500) ……………………………… 10,925,000

E15-4B (Continued)

2. Cash ……………………………………………………. 10,925,000

Bond Issue Costs …………………………………. 511,111

Bonds Payable

($5,000,000 – $4,888,889) ………………… 10,000,000

(b) One is not better than the other. This question is presented to stimulate

some thought and class discussion.

E15-5B (10–15 minutes)

(a) FMV of common (2,500 X $95) ………………………………………… $237,500

FMV of preferred (1,000 X $60) …………………………..……………. 60,000

$297,500

E15-5B (Continued)

(b) Lump-sum receipt ………………………………………….. $275,000

Allocated to common (2,500 X $90) …………………. 225,000

E15-6B (25–30 minutes)(a)Cash [(55,000 X $76) – $27,000] 4,153,000

Common Stock (55,000 X $1) ……………………. 55,000

Paid-in Capital in Excess of Par ……………….. 4,098,000

(b) Land (10,000 X $78) ………………………………………… 780,000

Common Stock (10,000 X $1) ……………………. 10,000

(c) Treasury Stock (6,000 X $74) ……………………………… 444,000

Cash ………………………………………………………….. 444,000

E15-7B (15–20 minutes)

#

Assets

Liabilities

Stockholders’

Equity

Paid-in

Capital

Retained

Earnings

Net

Income

1

D

NE

D

NE

NE

NE

3

NE

NE

NE

E15-8B (15–20 minutes)

(a) 10% Preferred stock (30,000 shares X $75) …………………… 2,450,000

Paid-in capital in excess of par (30,000 x [$83 – $75]) ……. 240,000

E15-9B (15–20 minutes)

Oct. 5 Cash ………………………………………………………. 39,000

Common Stock (1,000 X $1) ……………… 1,000

E15-9B (Continued)

13 Treasury Stock ………………………………………. 20,000

E15-10B (20–25 minutes)

2. The average cost of treasury shares at December 31, 2014, was $6.35

per share ($400 ÷ 63); the average cost at December 31, 2013, was

$7.00 per share ($595 ÷ 85).

(b) Stockholders’ equity (in millions of dollars)

Paid-in capital

E15-11B (15–20 minutes)

Item

Assets

Liabilities

Stockholders’

Equity

Paid-in

Capital

Retained

Earnings

Net

Income

1.

D

D

NE

NE

NE

NE

2.

NE

NE

NE

NE

NE

NE

3.

I

NE

I

NE

I

I

4.

D

NE

NE

NE

5.

NE

I

NE

6.

NE

I

NE

NE

7.

NE

NE

8.

I

NE

I

NE

NE

E15-12B (10–15 minutes)

(a)

8/31

Retained Earnings …………………………………………………..

30,000,000

Dividends Payable …………………………………………..

30,000,000

9/5

No entry on date of record.

9/30

Dividends Payable…………………………………………………..

Cash ………………………………………………………………

E15-13B (10–15 minutes)

(a) No entry—simply a memorandum indicating the number of shares has

increased to 60 million and par value has been reduced from $4 to $1 per

share.

(b)

180,000,000

(c) Stock dividends and splits serve the same function with regard to the

securities markets. Both techniques allow the board of directors to

increase the quantity of shares and channel share prices into the

“popular trading range.”

E15-14B (10–12 minutes)

(a)

Retained Earnings (3,000,000 X $1) …………………………..

3,000,000

Common Stock Dividend

Distributable …………………………………………………….

3,000,000

Common Stock Dividend Distributable ……………………..

Common Stock ……………………………………………………

3,000,000

(b)

Retained Earnings (150,000 X $17) …………………………...

Common Stock Dividend

Distributable …………………………………………………….

Paid-in Capital in Excess of Par …………………………...

2,400,000

Common Stock Dividend Distributable ……………………..

Common Stock ……………………………………………………

E15-15B (10–15 minutes)

(a) No entry; company uses a memorandum note to indicate that par value is

reduced to $0.50 and shares outstanding are now 140,000.

(b)

Retained Earnings …………………………………………………..

175,000

Common Stock Dividend

Distributable …………………………..……………………

Paid-in Capital in Excess of Par ……………………….

(70,000 shares X 10% X $25= $175,000

Common Stock Dividend Distributable …………………….

Common Stock ……………………………………………….

(c)

September 12, 2014

Investments (Equity) ……………………………………………….

155,000

Gain on Appreciation of Investments

(Equity) ……………………………………………………….

155,000

Retained Earnings …………………………………………………..

205,000

Property Dividends Payable …………………………….

205,000

Property Dividends Payable …………………………………….

205,000

Investments (Equity) …………………………..…………..

205,000

E15-16B (5–10 minutes)

Total income since incorporation …………………………….

$466,000

Less: Total cash dividends paid ……………………………..

Current balance of retained earnings ……………………….

$204,000

E15-17B (20–25 minutes)

CAPITAL NORTHEAST CORPORATION

Stockholders’ Equity

December 31, 2014

Capital stock

Preferred stock, 6% cumulative, par value

$100 per share; authorized 1,000,000

shares, issued and outstanding 65,000

shares …………………………………………………………….

$6,500,000

Common stock, par value $1 per share;

authorized 2,500,000 shares, issued

500,000 shares, and outstanding 490,000

shares …………………………………………………………….

500,000

Total capital stock ………………………………………………………

7,000,000

Additional paid-in capital—

In excess of par value—common ………………………..

1,900,000

From sale of treasury stock …………………………..……

35,000

Total paid-in capital …………………………………………………….

8,935,000

Retained earnings ……………………………………………………….

982,000

Total paid-in capital and retained earnings …………………..

9,917,000

Less: Treasury stock, 10,000 shares at cost ………………..

125,000

E15-18B (30–35 minutes)

(a)

1.

Dividends Payable—Preferred

(25,000 X $100 X 12%) …………………………………………..

300,000

Dividends Payable—Common

(300,000 X $0.50) …………………………………………………..

150,000

Cash ………………………………………………………………

2.

Treasury Stock ……………………………………………………….

8,000

Cash (1,000 X $8) …………………………………………….

8,000

3.

Land (1,000 X $8.50) ………………………………………………..

8,500

Treasury Stock (1,000 X $8) ……………………………..

8,000

Paid-in Capital From Treasury Stock ………………..

4.

Cash (50,000 X $9) …………………………………………………..

450,000

Common Stock (50,000 X $1) …………………………...

Paid-in Capital in Excess of Par—

Common ………………………………………………………

5.

No entry, memorandum note to indicate that

par value is reduced to $0.50 and shares

issued are now 700,000.

6.

Retained Earnings …………………………………………………..

650,000

Dividends Payable—Preferred

(25,000 X $100 X 12%) …………………………………..

Dividends Payable—Common

(700,000 X $0.50) …………………………………………..

E15-18B (Continued)

(b) FOCUS FOOT COMPANY

Stockholders’ Equity

December 31, 2014

Capital stock

Preferred stock, 12%, $100 par, 100,000

shares authorized, 25,000 shares issued and

outstanding ………………………………………………….

Common stock, $0.50 par, 2,000,000 shares

authorized, 700,000 shares issued and

outstanding ………………………………………………….

Total capital stock ……………………………………

2,850,000

Additional paid-in capital—Common ………………..

1,350,000

Additional paid-in capital—Treasury ………………..

Total additional paid-in capital ………………….

Total paid-in capital …………………………………………

Retained earnings …………………………………………………..

1,380,000

Total stockholders’ equity ……………………………………….

$5,580,500

Computations:

E15-19B (20–25 minutes)

(a) Honey Dew Inc. is the more profitable in terms of rate of return on total

assets. This may be shown as follows:

Istar Company

$96,000

= 9.6%

$1,000,000

Honey Dew Inc.

= 12.0%

$1,000,000

= 12.0%

$1,000,000

It should be noted that these returns are based on net income related to

total assets, where the ending amount of total assets is considered

representative. If the rate of return on total assets uses net income

before interest but after taxes in the numerator, the rates of return on

total assets are those shown below:

(b) Istar Company is the more profitable in terms of return on stockholders’

equity. This may be shown as follows:

E15-19B (Continued)

ISTAR COMPANY

Fund Supplies

Funds

Supplied

Rate of Return

on Funds at

12.0%*

Cost of

Funds

Accruing to

Common

Stock

Current liabilities

$ 100,000

$ 12,000

$ 0

$12,000

Long-term debt

400,000

48,000

24,000

**

24,000

Common stock

200,000

24,000

0

24,000

Retained earnings

300,000

36,000

0

(c) Istar Company earned a net income per share of $4.80 ($96,000 ÷ 20,000),

while Honey Dew Inc. had an income per share of $2.00 ($120,000 ÷

60,000). Istar Company has borrowed a substantial portion of its assets

(d) Yes, from the point of view of income it is advantageous for the

(e) Book value per share:

Istar Company

$200,000 + $300,000

= $25.00

20,000

$600,000 + $300,000

E15-20B (15 minutes)

Rate of return on common stock equity:

*E15-21B (10–15 minutes)

Preferred

Common

Total

(a)

Preferred stock is noncumulative,

participating

$241,935

$8,065

$250,000

(b)

Preferred stock is cumulative,

nonparticipating

(c)

Preferred stock is cumulative,

participating

$5,645

$250,000*

*Dividends in arrears

$ 75,000

$ 75,000

Current dividend

75,000

75,000

Pro rata share to common

($25,000 X 10%)

Balance dividend pro rata

750/775 X $97,500**

94,355

94,355

25/775 X $97,500**

3,145

$244,355

$5,645

*E15-22B (10–15 minutes)

Preferred

Common

Total

(a)

One year in arrears

$240,000

$240,000

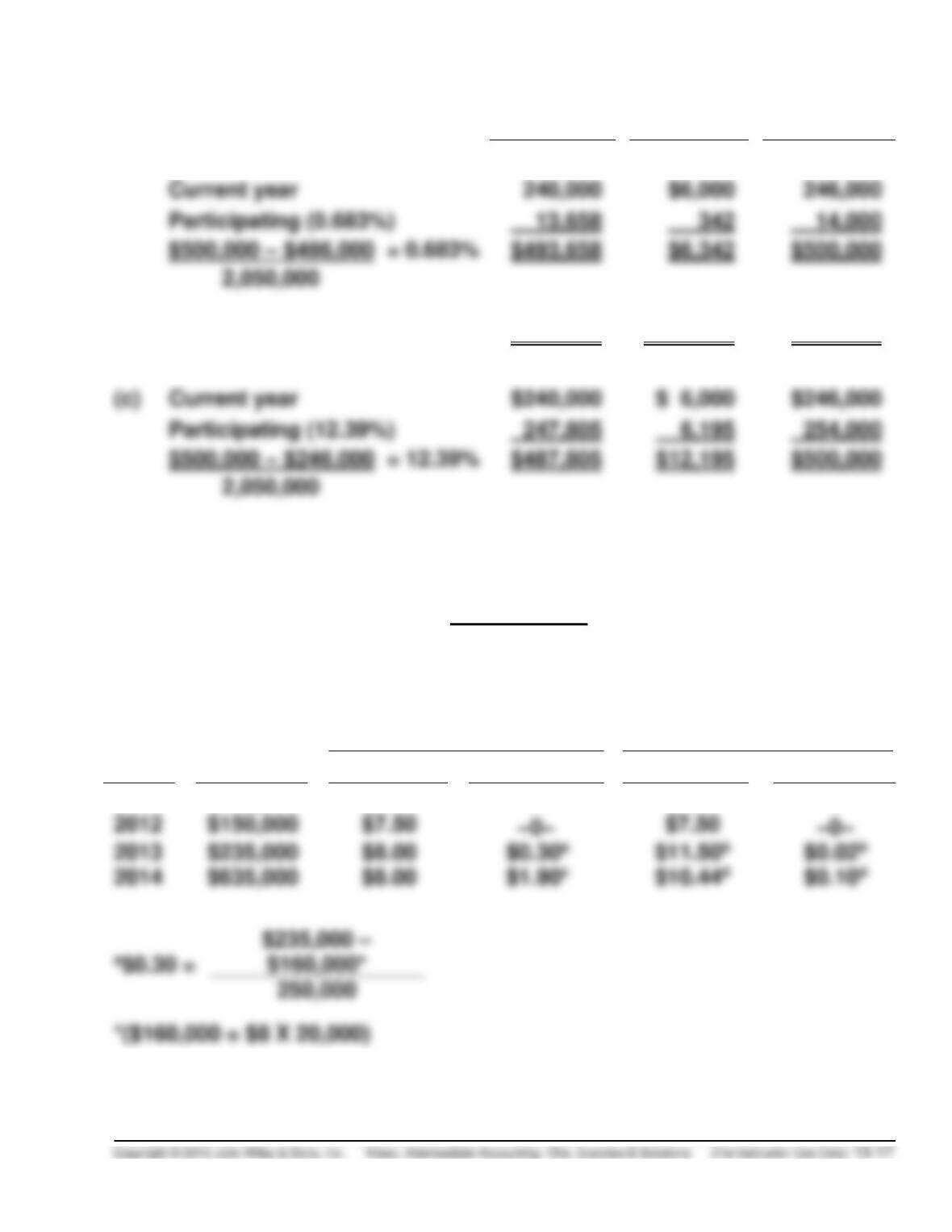

Current year

Participating (0.683%)

13,658

14,000

$493,658

(b)

$240,000

$260,000

$500,000

(c)

Current year

$240,000

$246,000

Participating (12.39%)

$487,805

*E15-23B (10–15 minutes)

Assumptions

(a)

(b)

Preferred,

noncumulative, and

nonparticipating

Preferred, cumulative,

and fully participating

Year

Paid-out

Preferred

Common

Preferred

Common

2011

$100,000

$5.00

–0–

$5.00

–0–

$150,000

–0–

–0–

2014

$635,000

$8.00

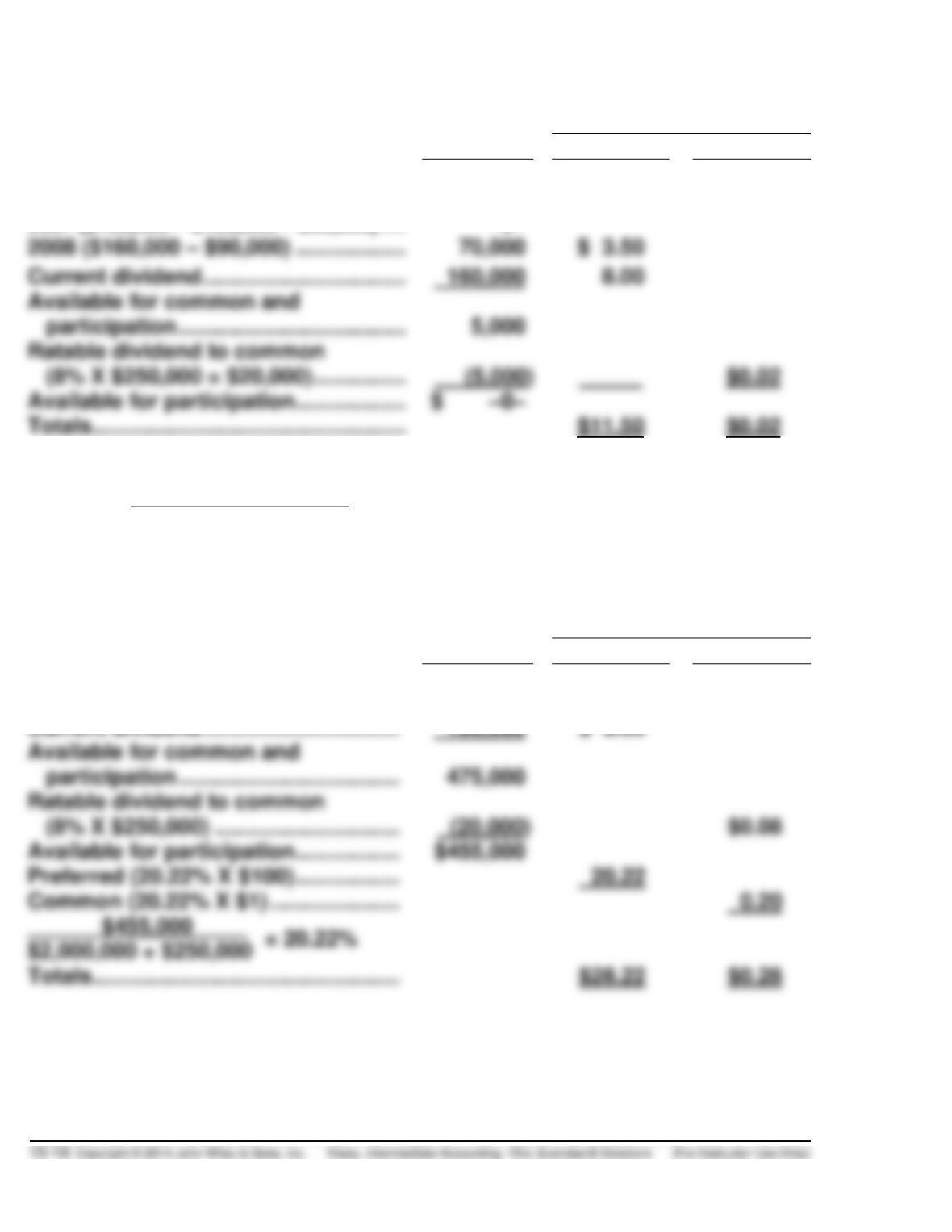

*E15-23B (Continued)

b

Per Share

Total

Preferred

Common

Total amount to be distributed ……….

$235,000

Preferred dividends in arrears

2007 ($160,000 – $100,000 – $60,000) ….

–0–

Current dividend …………………………...

Available for common and

participation ……………………………….

Ratable dividend to common

(8% X $250,000 = $20,000) ……………

(5,000)

Available for participation ………………

$ –0–

Totals ……………………………………………

c$1.90 =

$635,000 – $160,000*

250,000

*($160,000 = $8 X 20,000)

Per Share

Total

Preferred

Common

Total amount to be distributed ………

$635,000

Preferred dividends in arrears ……….

–0–

Current dividend …………………………..

Available for common and

participation ………………………………

Ratable dividend to common

(8% X $250,000) …………………………

Available for participation ……………..

$455,000

Preferred (20.22% X $100) ……………..

$455,000

$2,000,000 + $250,000

Totals …………………………………………..

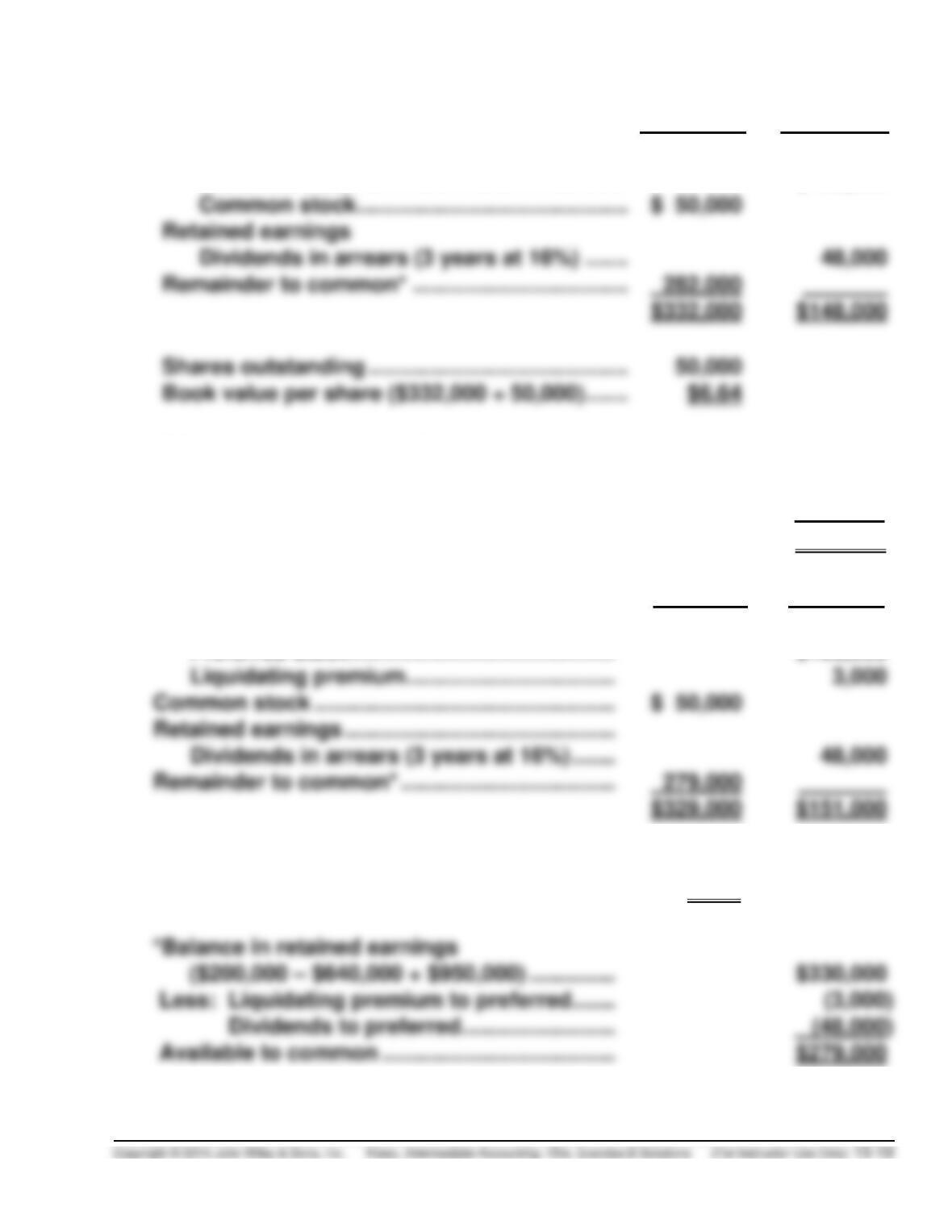

*E15-24B (10–15 minutes)

(a)

Common

Preferred

Stockholders’ equity

Preferred stock …………………………………….

$100,000

Common stock ……………………………………..

Retained earnings

Dividends in arrears (3 years at 16%) …….

Remainder to common* ……………………………..

$148,000

Shares outstanding ……………………………………

Book value per share ($332,000 ÷ 50,000) …….

*Balance in retained earnings

($200,000 – $640,000 + $950,000) …………….

$330,000

Less: Dividends to preferred …………………….

(48,000)

Available to common …………………………………

$282,000

(b)

Common

Preferred

Stockholders’ equity

Preferred stock …………………………………….

$100,000

Liquidating premium …………………………….

Common stock ………………………………………….

$ 50,000

Retained earnings ……………………………………..

Dividends in arrears (3 years at 16%) …….

Remainder to common* ……………………………..

Shares outstanding ……………………………………

50,000

Book value per share ($329,000 ÷ 50,000) ……

$6.58

*Balance in retained earnings

($200,000 – $640,000 + $950,000) …………..

$330,000

Less: Liquidating premium to preferred …….

Dividends to preferred …………………….

$279,000