FINANCIAL STATEMENT ANALYSIS CASE

($ millions)

(b) The total rental expense for Walmart in fiscal 2011 (ending 1/31/2012)

was $2.4 billion.

(c) To estimate the present value of the operating leases, the same portion

FINANCIAL STATEMENT ANALYSIS CASE (Continued)

Total operating lease payments due ………………………….. $16,415

Less estimated interest …………………………………………….. 7,108

Estimated present value of net operating

lease payments …………………………..………………………… $9,307

This answer is an approximation. This answer is somewhat incorrect

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

There are four lease capitalization criteria. They are (1) transfer of title,

(2) bargain-purchase option, (3) the lease term is 75% or more of the

economic life of the leased asset, and (4) the present value of the minimum

lease payments is 90% or more of the leased asset’s fair value.

This lease does not transfer title. The option to purchase at the end of the

lease is clearly not a bargain. The lease term is (3 ÷ 5) = 0.6 or 60% of the

economic life, so the economic life test is not met. The recovery of

investment test is as follows:

Minimum lease payments

Therefore, the recovery of investment test is not met either. Consequently,

this lease is accounted for as an operating lease. Therefore the journal

entry that Salaur makes on January 1, 2014 is:

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Analysis

When companies structure leases to avoid capitalization, both the leased

assets and the obligation for the noncancelable lease payments are “off–

Principles

The element of the fundamental quality is faithful representation. The lease

criteria are designed to report leases according to their economic

PROFESSIONAL RESEARCH

(a) According to FASB ASC 840-10–10-1 the objective of the lease

classification criteria in this Subtopic derives from the concept that a

(b) According to the Glossary at FASB ASC 840–10–20, “substantially all”

relates to the concepts underlying the lease classification criteria. A 90

percent recovery test in the minimum-lease-payments criterion in

(c) Lease Term (Codification String: Broad Transactions > 840 Leases > 10

Overall > 20 Glossary)

The lease term is the fixed noncancelable lease term plus all of the

following, except as noted in the following paragraph:

a. All periods, if any, covered by bargain renewal options.

PROFESSIONAL RESEARCH (Continued)

(2) A loan from the lessee to the lessor directly or indirectly related

to the leased property is expected to be outstanding.

(d) According to FASB ASC 840–10–25-9, a lease provision requiring the

lessee to make up a residual value deficiency that is attributable to

PROFESSIONAL SIMULATION 1

Note: This assignment is available on the Kieso website.

Resources

Note: This lease is a capital lease to the lessee because the lease term

(six years) exceeds 75% of the economic life of the asset (six years). Also, the

PROFESSIONAL SIMULATION 1 (Continued)

Journal Entries

January 1, 2014

Leased Equipment ………………………………………………… 400,000

Lease Liability ………………………………………………… 400,000

Depreciation Expense ……………………………………………. 58,333

Accumulated Depreciation—Capital

Leases ([$400,000 – $50,000] ÷ 6) …………………. 58,333

January 1, 2015

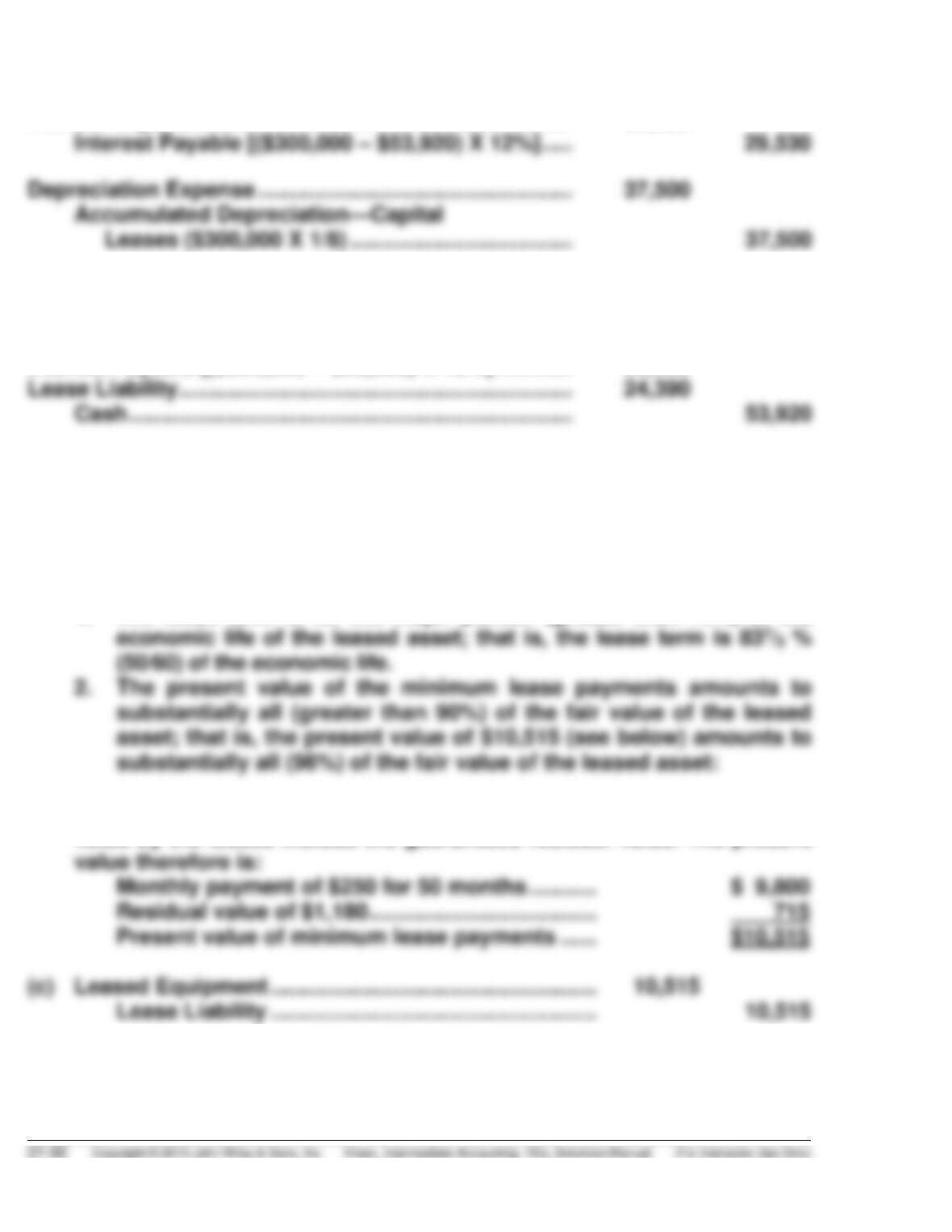

Interest Payable …………………………………………………….. 38,236

Interest Expense …………………………………………….. 38,236

PROFESSIONAL SIMULATION 1 (Continued)

(Note to instructor: The guaranteed residual value was subtracted for

purposes of determining the depreciable base. The reason is that at the

end of the lease term, hopefully, this balance can offset the remaining lease

PROFESSIONAL SIMULATION 2

Explanation

This is a capital lease to Dexter Labs since the lease term (5 years) is

Measurement

Computation of present value of minimum lease payments:

Journal Entries

1/1/14 Leased Equipment ………………………………….. 36,144

Lease Liability ………………………………….. 36,144

IFRS CONCEPTS AND APPLICATION

IFRS21-1

The IFRS leasing standard is IAS 17, first issued in 1982. This standard is

IFRS21-2

Both U.S. GAAP and IFRS share the same objective of recording leases by

IFRS21-3

Lease accounting is one of the areas identified in the IASB/FASB

Memorandum of Understanding and also a topic recommended by the SEC

IFRS21-4

Under the operating method, rent expense (and a compensating liability)

accrues day by day to the lessee as the property is used. The lessee

IFRS21-5

Under the finance lease method, the lessee treats the lease transactions as

if the asset were being purchased on an installment basis: a financial

transaction in which an asset is acquired and an obligation is created. The

asset and the obligation are stated in the lessee’s balance sheet at the

IFRS21-6

From the standpoint of the lessor, leases may be classified for accounting

purposes as: (a) operating leases, (b) direct-financing leases, and (c) sales-

type leases.

Leases are classified as finance leases if they meet one or more of the

following four criteria:

1. The lease transfers ownership of the property to the lessee,

IFRS21-7

Interest Expense …………………………..………………………. 29,530

IFRS21-8

Interest Payable [($300,000 – $53,920) X 12%] ………… 29,530

IFRS21-9

(a) To Brecker, the lessee, this lease is a finance lease because the terms

satisfy the following criteria:

1. The lease term is for the major portion (greater than 75%) of the

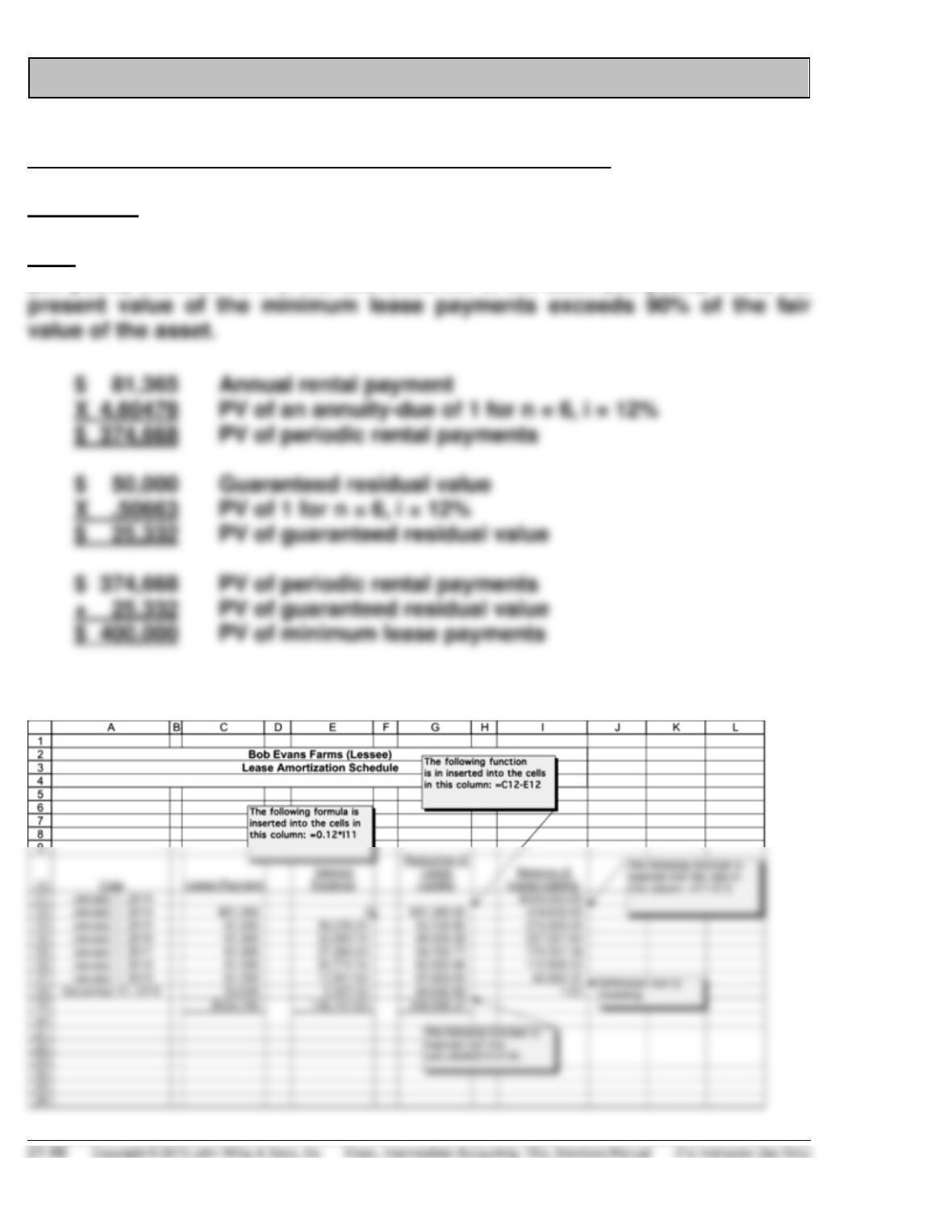

(b) The minimum lease payments in the case of a guaranteed residual

value by the lessee include the guaranteed residual value. The present

IFRS21-9 (Continued)

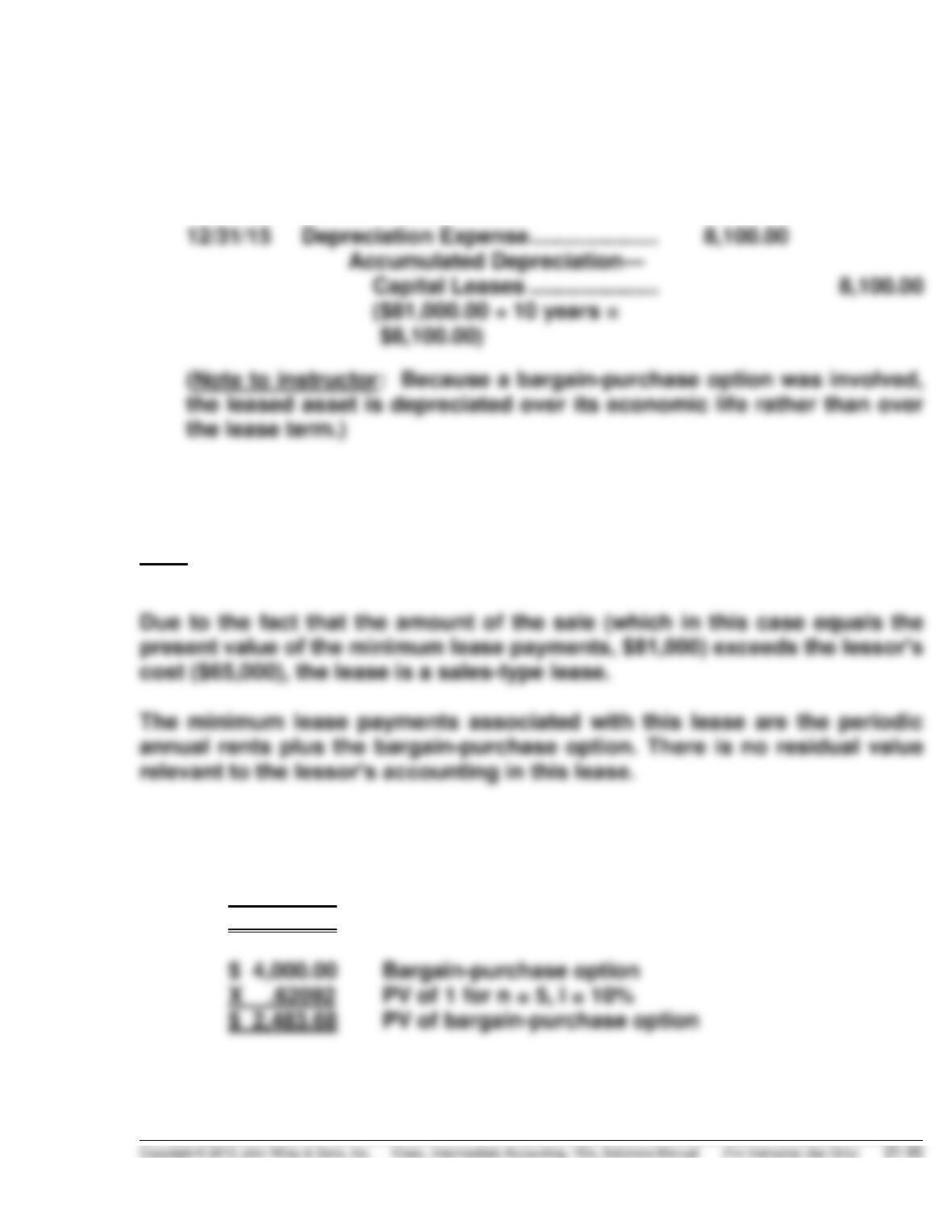

(d) Depreciation Expense ……………………………………….. 187

IFRS21-10

(a) The lease agreement has a bargain-purchase option and thus meets

the criteria to be classified as a finance lease from the viewpoint of the

(c) Computation of lease liability:

$18,829.49 Annual rental payment

X 4.16986 PV of an annuity-due of 1 for n = 5, i = 10%

$78,516.34 PV of periodic rental payments

IFRS21-10 (Continued)

GILL COMPANY (Lessee)

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

BPO

Interest

(10%) on

Liability

Reduction

of Lease

Liability

Lease

Liability

5/1/14

$81,000.00

5/1/14

$18,829.49

$ –0–

$18,829.49

62,170.51

5/1/15

18,829.49

6,217.05

12,612.44

49,558.07

5/1/16

35,684.39

5/1/17

20,423.34

5/1/18

18,829.49

16,787.16

3,636.18

4/30/19

4,000.00

3,636.18

$98,147.45

$81,000.00

(d) 5/1/14 Leased Equipment ……………………….. 81,000.00

Lease Liability ……………………….. 81,000.00

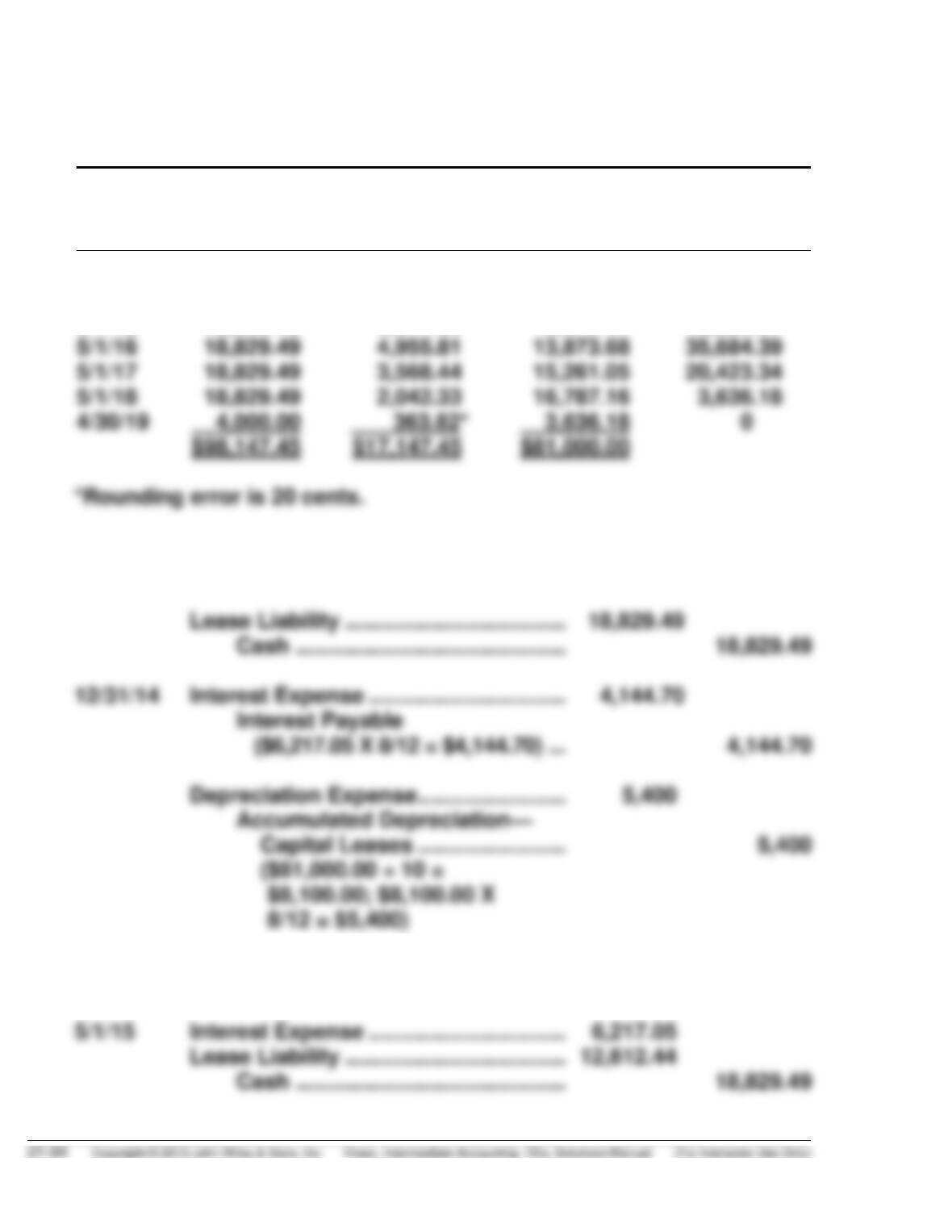

1/1/15 Interest Payable ……………………………. 4,144.70

Interest Expense ……………………. 4,144.70

IFRS21-10 (Continued)

12/31/15 Interest Expense ……………………….. 3,303.87

Interest Payable ………………….. 3,303.87

($4,955.81 X 8/12 =

($3,303.87)

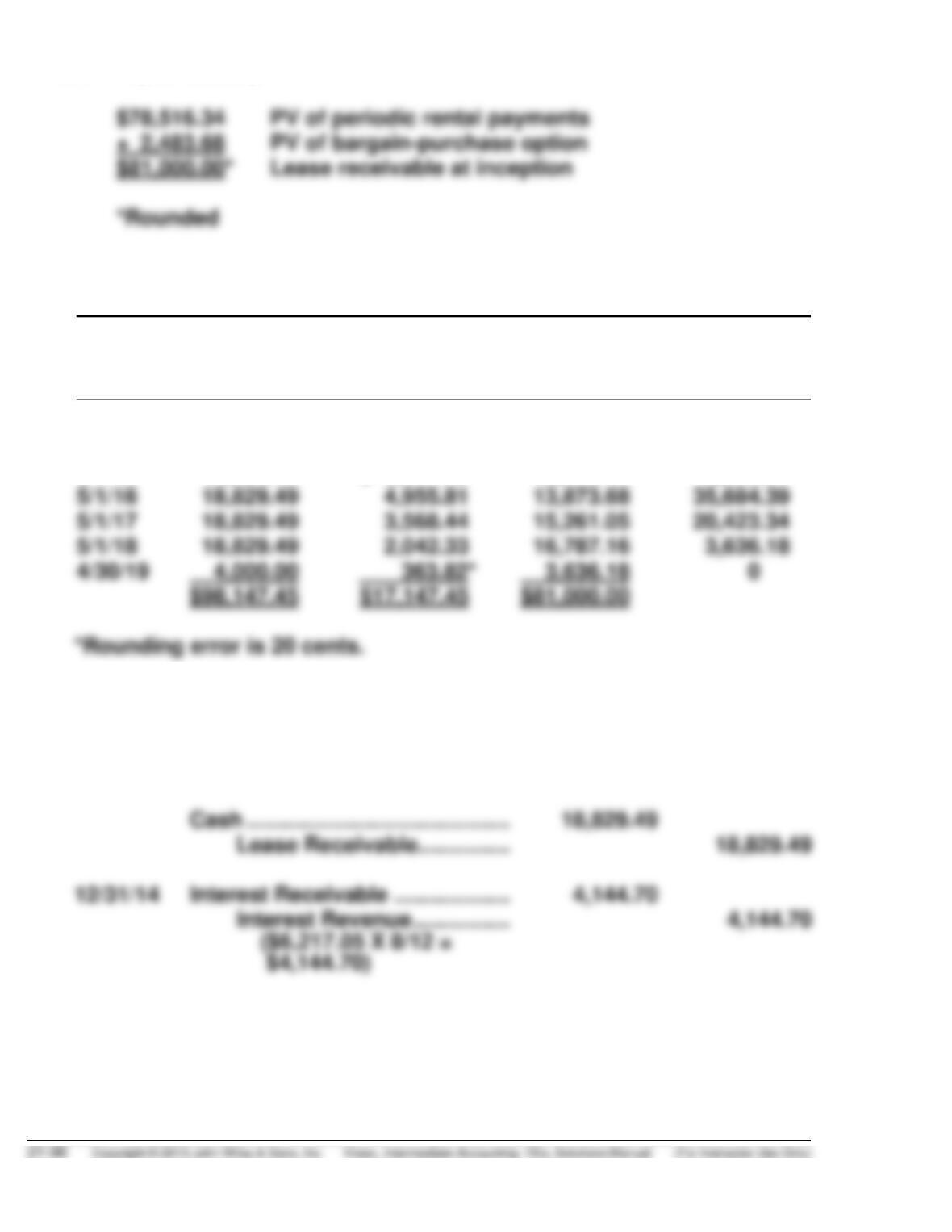

IFRS21-11

Note: The lease agreement has a bargain-purchase option. The lease,

therefore, qualifies as a finance lease from the viewpoint of the lessor.

(a) The lease receivable is computed as follows:

$18,829.49 Annual rental payment

X 4.16986 PV of an annuity-due of 1 for n = 5, i = 10%

$78,516.34 PV of periodic rental payments

IFRS21-11 (Continued)

(b) LENNOX LEASING COMPANY (Lessor)

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

BPO

Interest (10%)

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

5/1/14

$81,000.00

5/1/14

$18,829.49

$18,829.49

62,170.51

5/1/15

18,829.49

$ 6,217.05

12,612.44

49,558.07

5/1/16

35,684.39

5/1/17

20,423.34

5/1/18

18,829.49

16,787.16

4/30/19

4,000.00

3,636.18

$98,147.45

$81,000.00

(c) 5/1/14 Lease Receivable …………………. 81,000.00

Cost of Goods Sold ………………. 65,000.00

Sales Revenue ………………. 81,000.00

Inventory ………………………. 65,000.00

IFRS21-11 (Continued)

5/1/15 Cash ……………………………………. 18,829.49

Lease Receivable ………….. 12,612.44

Interest Receivable ………… 4,144.70

Interest Revenue …………… 2,072.35

($6,217.05 – $4,144.70)

IFRS21-12

(a) According to IAS 17, paragraph 7, “The classification of leases adopted

in this Standard is based on the extent to which risks and rewards

incidental to ownership of a leased asset lie with the lessor or the

lessee. Risks include the possibilities of losses from idle capacity or

IFRS21-12 (Continued)

(b) IAS 17 does not define “substantially all.”

(c) IAS 17 does not name other considerations in determining “lease term,”

IFRS21-13

(a) M&S uses both finance leases and operating leases.

(c) M&S disclosed future minimum rentals (in millions) under non-cancelable

operating lease agreements as of 31 March 2012, of:

Not later than one year ……………………………… £ 257.8