CHAPTER 21

SOLUTIONS TO B PROBLEMS

PROBLEM 21-1B

(a) This is a capital lease to Pro since the lease term is equal to or greater

than 75% of the economic life of the leased asset. The lease term is

75% (6 ÷ 8) of the asset’s economic life.

This is a capital lease to Rookie Leasing because collectibility of the

(b) Calculation of annual rental payment:

(c) Computation of present value of minimum lease payments:

PV of annual payments: $73,806 X 4.79079** = $353,589

PV of guaranteed residual value: $50,000 X 0.56447** = 28,224

$381,813

PROBLEM 21-1B (Continued)

12/31/14 Depreciation Expense ……………………. 55,302

Accumulated Depreciation—

Capital Leases

($381,813 – $50,000) ÷ 6……….. 55,302

Interest Payable ……………………… 26,500

[($381,813 – $73,806 –

$43,005) X 0.10]

(e) 1/1/14 Lease Receivable ………………………….. 400,000

Cost of Goods Sold ……………………….. 300,000

PROBLEM 21-2B

(a) The lease is an operating lease to the lessee and lessor because:

1. it does not transfer ownership,

2. it does not contain a bargain-purchase option,

At least one of the four criteria would have had to be satisfied for the

lease to be classified as other than an operating lease.

(b) Lessee’s Entries

Rent Expense …………………………..……………………….. 30,000

Cash …………………………………………………………… 30,000

PROBLEM 21-2B (Continued)

(c) Fort Construction as lessee must disclose in the income statement the

$30,000 of rent expense and in the notes the future minimum rental

payments required as of January 1 (in total, $120,000) and for each of

the succeeding four years: 2015—$30,000; 2016—$30,000; 2017—

$30,000; 2018— $30,000. Nothing relative to this lease would appear on

the lessee’s balance sheet.

PROBLEM 21-3B

(a) The lease should be treated as a capital lease by Manatee Industries

requiring the lessee to capitalize the leased asset. The lease qualifies for

capital lease accounting by the lessee because: (1) title to the boats

transfers to the lessee, (2) the lease term is equal to the estimated life

of the asset, and (3) the present value of the minimum lease payments

exceeds 90% of the fair value of the leased engines. The transaction

represents a purchase financed by installment payments over a 8-year

period.

Present Value of Lease Payments

$84,591 X 6.20637* ……………………………………………. $525,000

*Present value of an annuity due at 8% for 8 years, rounded by $3.

(c) Lease Receivable ………………………………………. 525,000

Cost of Goods Sold …………………………..………. 450,000

Sales Revenue ……………………………………. 525,000

Inventory ……………………………………………. 450,000

PROBLEM 21-3B (Continued)

(e) MANATEE INDUSTRIES

Lease Amortization Schedule

Date

Annual

Lease

Receipt/

Payment

Interest on

Receivable/

Liability at 8%

Reduction in

Receivable/

Liability

Lease

Receivable/

Liability

1/1/14

525,000

1/1/14

84,591

84,591

440,409

1/1/15

84,591

49,358

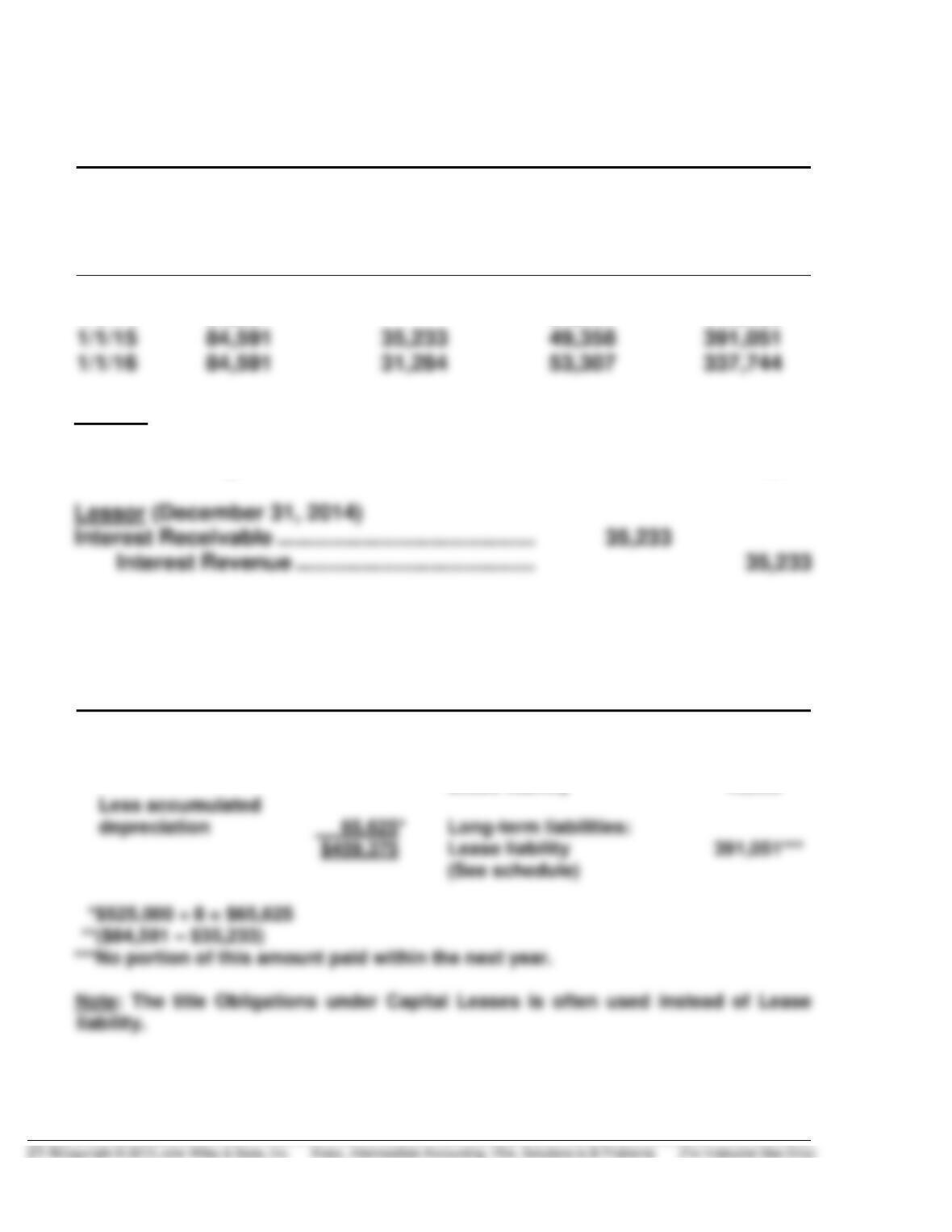

Lessee (December 31, 2014)

Interest Expense ………………………………………. 35,233

Interest Payable …………………………………. 35,233

(f) MANATEE INDUSTRIES

Balance Sheet

December 31, 2014

Property, plant, and equipment:

Current liabilities:

Leased property

$525,000

Interest payable

$ 35,233

Lease liability

49,358**

PROBLEM 21-3B (Continued)

SEA COW INC.

Balance Sheet

December 31, 2014

Assets

Current assets:

Interest receivable …………………………………………….. $ 35,233

Lease receivable ……………………………………………….. 49,358

PROBLEM 21-4B

2. Current liabilities:

$ 29,401 Lease liability

$ 10,599 Interest payable

3. $ 8,247 Interest expense (See amortization schedule)

$ 4,000 Lease executory expense

$ 34,497 Depreciation expense ($172,485 ÷ 5 = $34,497)

4. Current liabilities:

$ 31,753 Lease liability

$ 8,247 Interest payable

PROBLEM 21-4 (Continued)

2. Current liabilities:

$ 29,401 Lease liability

$ 4,416 Interest payable

3. $ 9,619 Interest expense

[($10,599 – $4,416) + ($8,247 X 5/12) =

[$6,183 + $3,436 = $9,619]

$ 4,000 Lease executory expense

$ 34,497 Depreciation expense ($172,485 ÷ 5 = $34,497)

4. Current liabilities:

$ 31,753 Lease liability

$ 3,436 Interest payable ($8,247 X 5/12 = $3,436)

PROBLEM 21-5B

(a) 1. $ 10,599 Interest revenue

2. Current assets:

$ 40,000 Lease receivable $29,401

Interest receivable $10,599

(b) 1. $ 4,416 Interest revenue ($10,599 X 5/12 = $4,416)

2. Current assets:

$ 33,817 Lease receivable $29,401

Interest receivable $4,416

4. Current assets:

$ 35,189 Lease receivable $31,753

PROBLEM 21-6B

Note: This lease is a capital lease to the lessee because the lease term

(5 years) exceeds 75% of the remaining economic life of the asset (6 years).

Also, the present value of the minimum lease payments exceeds 90% of the

fair value of the asset.

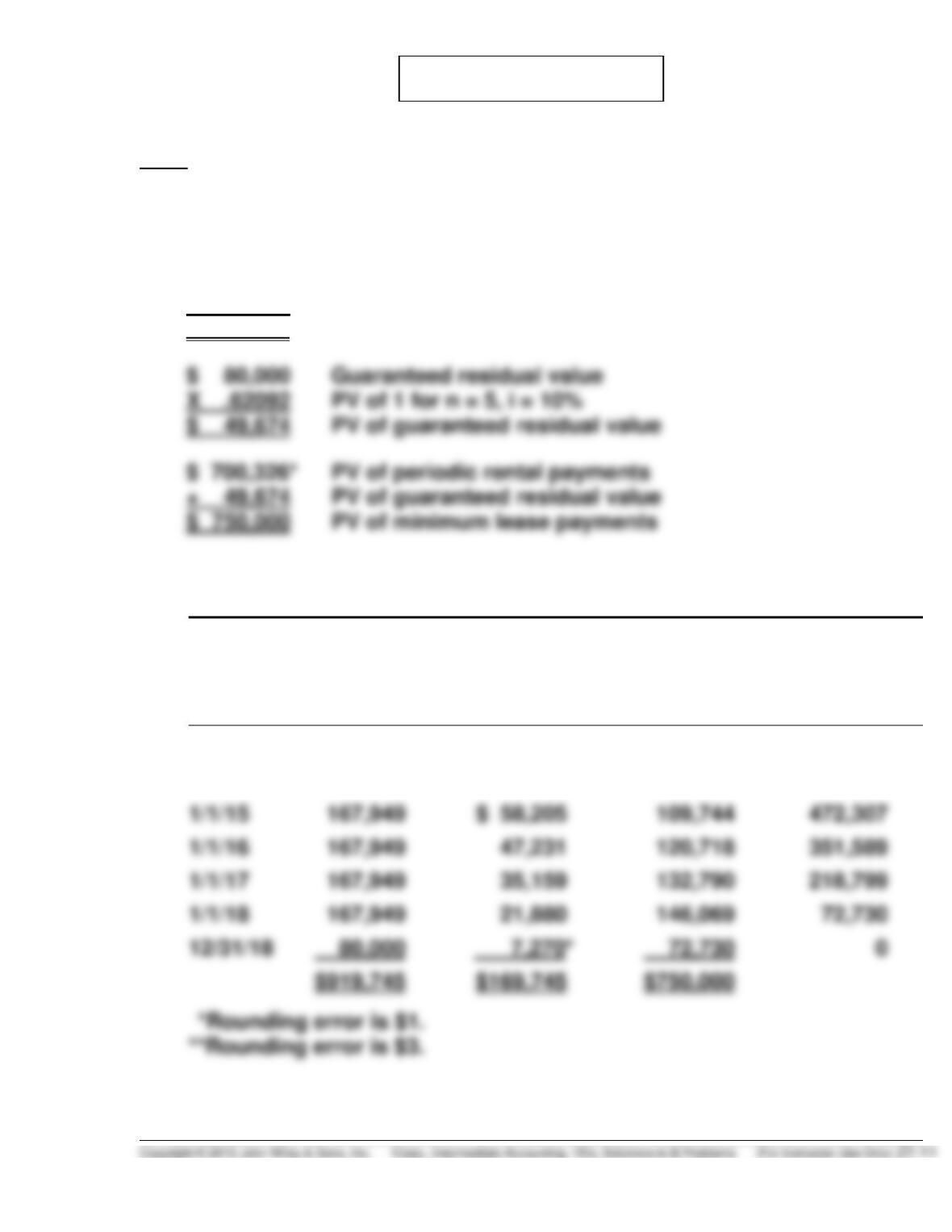

$ 167,949 Annual rental payment

X 4.16987 PV of an annuity due of 1 for n = 5, i = 10%

$ 700,326* PV of periodic rental payments

(a) VANCE COMPANY (Lessee)

Lease Amortization Schedule

Date

Annual

Lease

Payment

Plus GRV

Interest (10%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/14

$750,000

1/1/14

$167,949

$167,949

582,051

1/1/15

167,949

472,307

1/1/16

167,949

1/1/17

167,949

12/31/18

$919,745

$750,000

PROBLEM 21-6B (Continued)

(b) January 1, 2014

Leased Equipment …………………………………………. 750,000

Lease Liability …………………………………………. 750,000

December 31, 2014

Interest Expense ……………………………………………. 58,205

Interest Payable ………………………………………. 58,205

January 1, 2015

Interest Payable …………………………………………….. 58,205

Interest Expense ……………………………………… 58,205

Interest Expense ……………………………………………. 58,205

Lease Liability ……………………………………………….. 109,744

Cash ……………………………………………………….. 167,949

PROBLEM 21-6B (Continued)

(Note to instructor: The guaranteed residual value was subtracted for

purposes of determining the depreciable base. The reason is that at

PROBLEM 21-7B

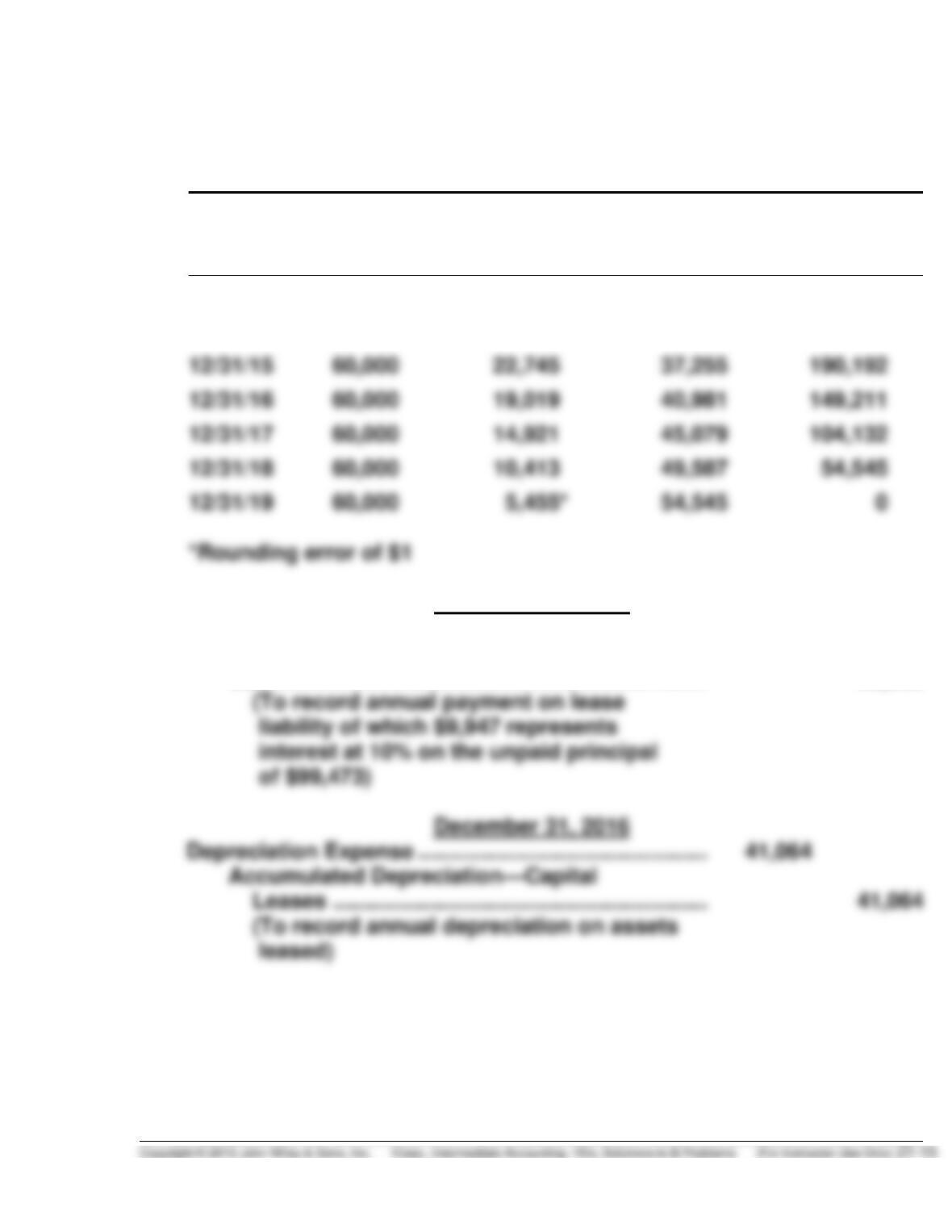

(a) December 31, 2014

Leased Equipment …………………………………………. 287,447

Lease Liability …………………………………………. 287,447

(b) December 31, 2015

Depreciation Expense ……………………………………. 41,064

Accumulated Depreciation—Capital

December 31, 2015

Interest Expense ……………………………………………. 22,745

Lease Liability ……………………………………………….. 37,255

PROBLEM 21-7B (Continued)

Blue Ocean COMPANY (Lessee)

Lease Amortization Schedule

(Annuity Due Basis)

Date

Annual

Lease

Payment

Interest (10%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

12/31/14

—

—

—

$287,447

12/31/14

$60,000

$ 0

$60,000

227,447

12/31/17

104,132

12/31/19

(c) December 31, 2016

Interest Expense ……………………………………………….. 19,019

Lease Liability …………………………………………………… 40,981

Cash …………………………………………………………… 60,000

PROBLEM 21-7B (Continued)

(d) BLUE OCEAN COMPANY

Balance Sheet

December 31, 2016

Property, plant, and equipment:

Current liabilities:

PROBLEM 21-8B

(a) The $420,000 is the present value of the 5 annual lease payments of

$105,400 less the $8,000 attributable to the payment for taxes, insurance,

and maintenance. In other words, it is the present value of five $97,400

payments to be made at the beginning of each year discounted at 8%,

(b) Leased Equipment ………………………………………….. 420,000

(c) Depreciation Expense …………………………………….. 168,000

Accumulated Depreciation—Capital

Leases …………………………………………………. 168,000

($420,000 X 40% = $168,000)

PROBLEM 21-8B (Continued)

OAK FURNITURE COMPANY (Lessee)

Lease Amortization Schedule

Date

Annual

Lease

Payment

Interest (8%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/14

$420,000

322,600

(f) OAK FURNITURE COMPANY

Balance Sheet

December 31, 2014

Assets

Liabilities

Property, plant, and equipment:

Current:

Noncurrent: