PROBLEM 20-9

(a) See worksheet on next page.

(b) December 31, 2014

(c) See worksheet on next page. The entry is below.

December 31, 2015

Other Comprehensive Income (PSC) ……………….. 510,000

(d) Financial Statements—2015

Income Statement

Pension expense ……………………………………… $432,440

PROBLEM 20-9 (Continued)

20–62 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

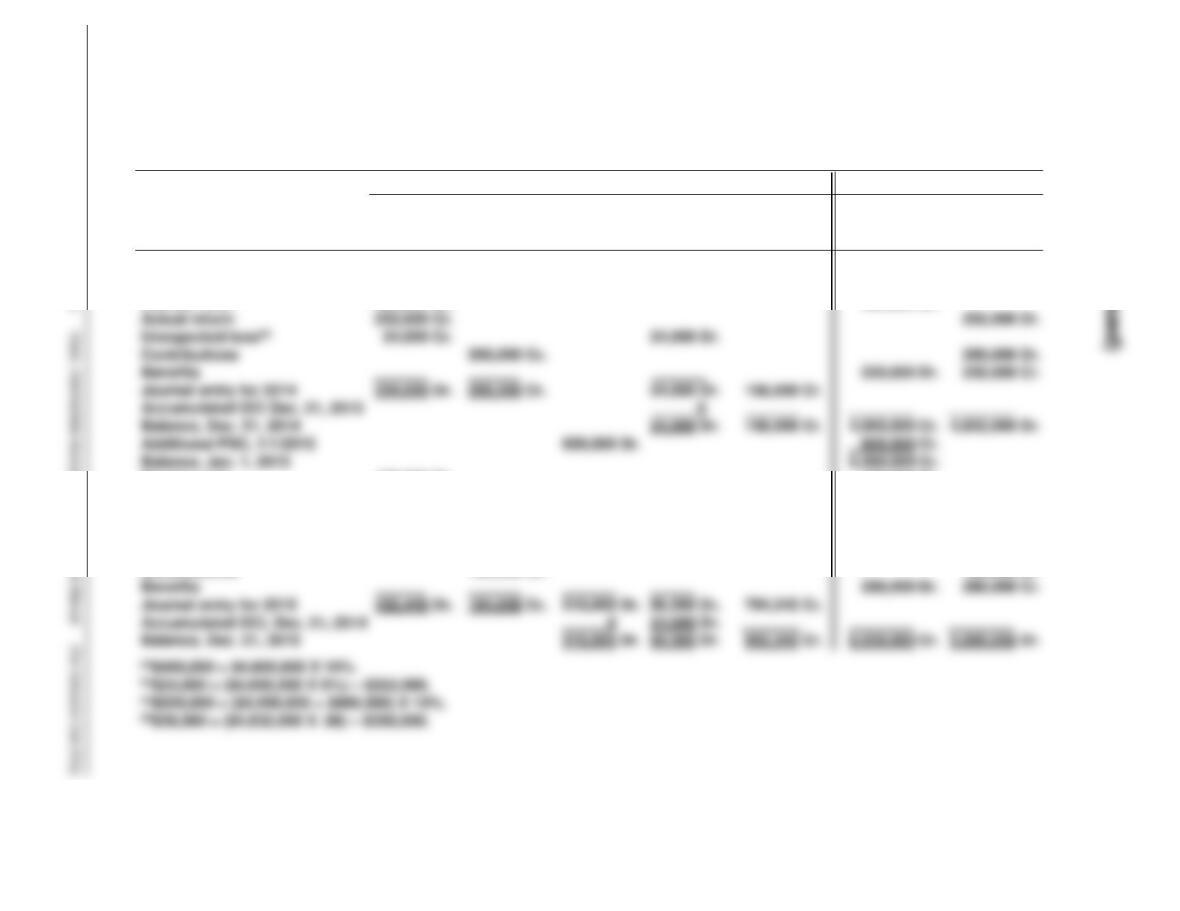

(a) HOBBS COMPANY

Pension Worksheet—2014 and 2015

General Journal Entries Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

4,600,000 Cr.

4,600,000 Dr.

Service cost

150,000 Dr.

150,000 Cr.

Interest cost(a)

460,000 Dr.

460,000 Cr.

Service cost

170,000 Dr.

170,000 Cr.

Interest cost(c)

559,000 Dr.

559,000 Cr.

Actual return

350,000 Cr.

350,000 Dr.

Unexpected loss(d)

36,560 Cr.

36,560 Dr.

Amortization of PSC

90,000 Dr.

90,000 Cr.

Contributions

184,658 Cr.

184,658 Dr.

Benefits

280,000 Dr.

280,000 Cr.

Journal entry for 2015

432,440 Dr.

184,658 Cr.

Accumulated OCI, Dec. 31, 2014

24,000 Dr.

Balance, Dec. 31, 2015

60,560 Dr.

6,039,000 Cr.

5,086,658 Dr.

Actual return

252,000 Cr.

252,000 Dr.

Unexpected loss(b)

24,000 Cr.

24,000 Dr.

Contributions

200,000 Cr.

200,000 Dr.

Benefits

220,000 Dr.

220,000 Cr.

Journal entry for 2014

334,000 Dr.

200,000 Cr.

24,000 Dr.

Accumulated OCI Dec. 31, 2013

Balance, Dec. 31, 2014

24,000 Dr.

4,990,000 Cr.

4,832,000 Dr.

Additional PSC, 1/1/2015

Balance, Jan. 1, 2015

5,590,000 Cr.

KRAMER COMPANY

(a) Completed Worksheet—2014

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

120,000 Cr.

325,000 Cr.

205,000 Dr.

Service cost

20,000 Dr.

20,000 Cr.

Interest cost

26,000 Dr.

26,000 Cr.

(b) 2014

Pension Expense …………………………………………………………………… 60,500

(c) 1. Settlement Rate: $26,000 ÷ $325,000 = 8%

2. Expected return on assets: ($18,000 + $2,500) ÷ $205,000 = 10%

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 20–63

Actual return

Unexpected loss

Amortization of PSC

35,000 Dr.

Contributions

Benefits

15,000 Dr.

Increase in PBO

43,500 Cr.

Journal entry for 2014

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

KRAMER COMPANY

(a) Completed Worksheet—2015

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2015

150,500 Cr.

399,500 Cr.

249,000 Dr.

Service cost

59,000 Dr.

59,000 Cr.

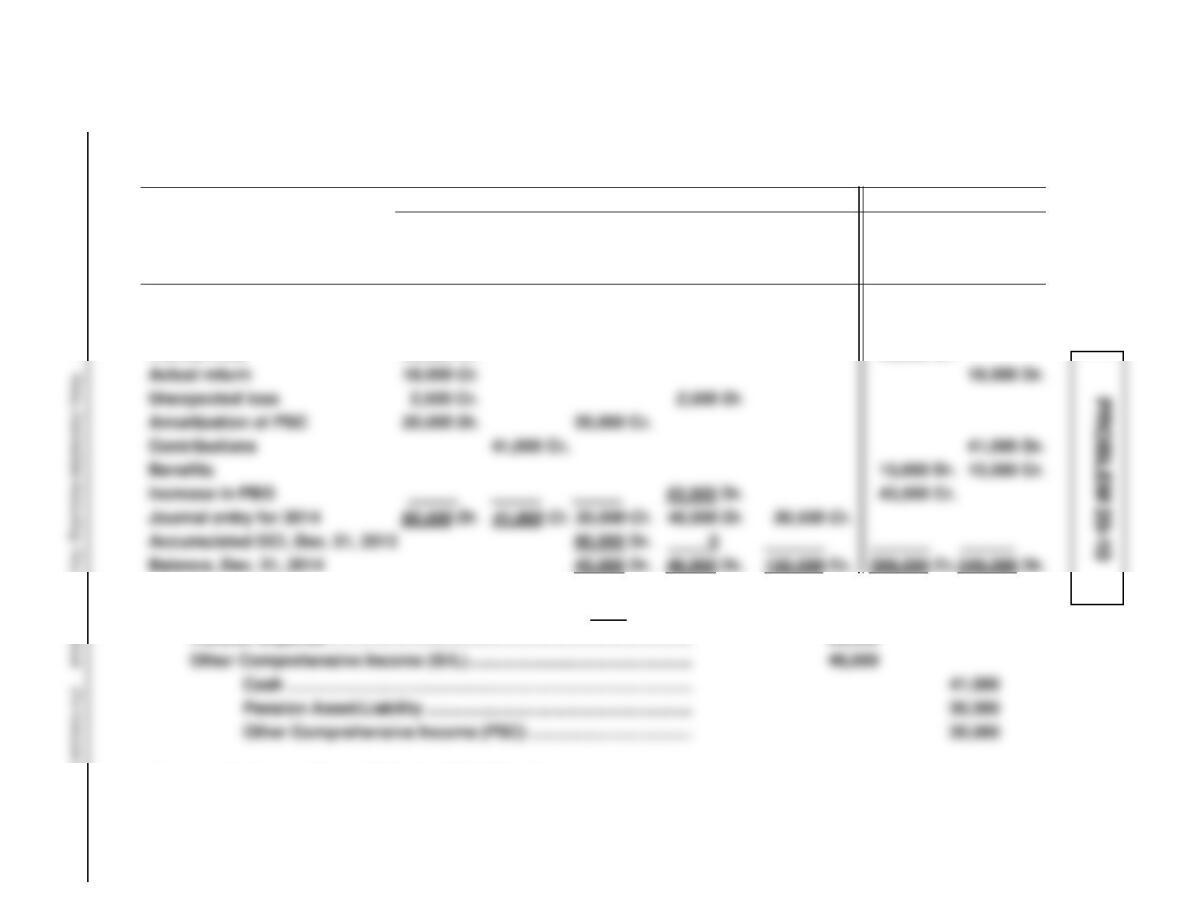

PROBLEM 20-11

20–64 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

Interest cost

39,950 Dr.

39,950 Cr.

Unexpected gain

Amortization of PSC

28,000 Dr.

28,000 Cr.

Contributions

51,000 Cr.

Benefits

27,000 Dr.

Accumulated OCI, Dec. 31, 2014

Balance, Dec. 31, 2015

PROBLEM 20-11 (Continued)

Worksheet computations:

Interest cost: $39,950 = $399,500 X 10%

Unexpected gain: $7,100 = ($249,000 X 10%) – $32,000; actual return

exceeds expected return.

(b) 2015

Pension Expense ……………………………………………….. 102,292

Pension Asset/Liability …………………………………. 15,950

Other Comprehensive Income (PSC) …………….. 28,000

Other Comprehensive Income (G/L) ………………. 7,342

Cash …………………………..……………………………….. 51,000

(c) Financial Statements—2015

Income Statement

Pension expense …………………………………………. $102,292

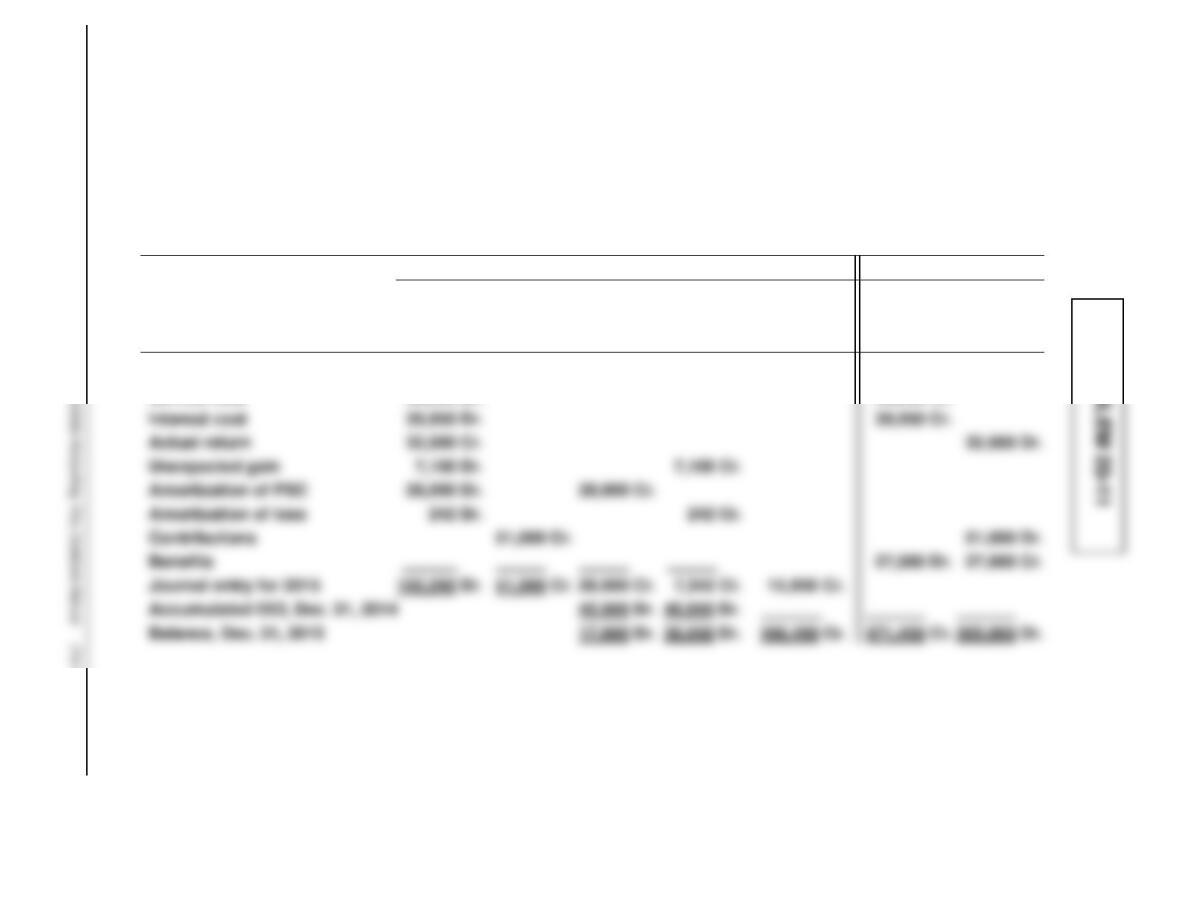

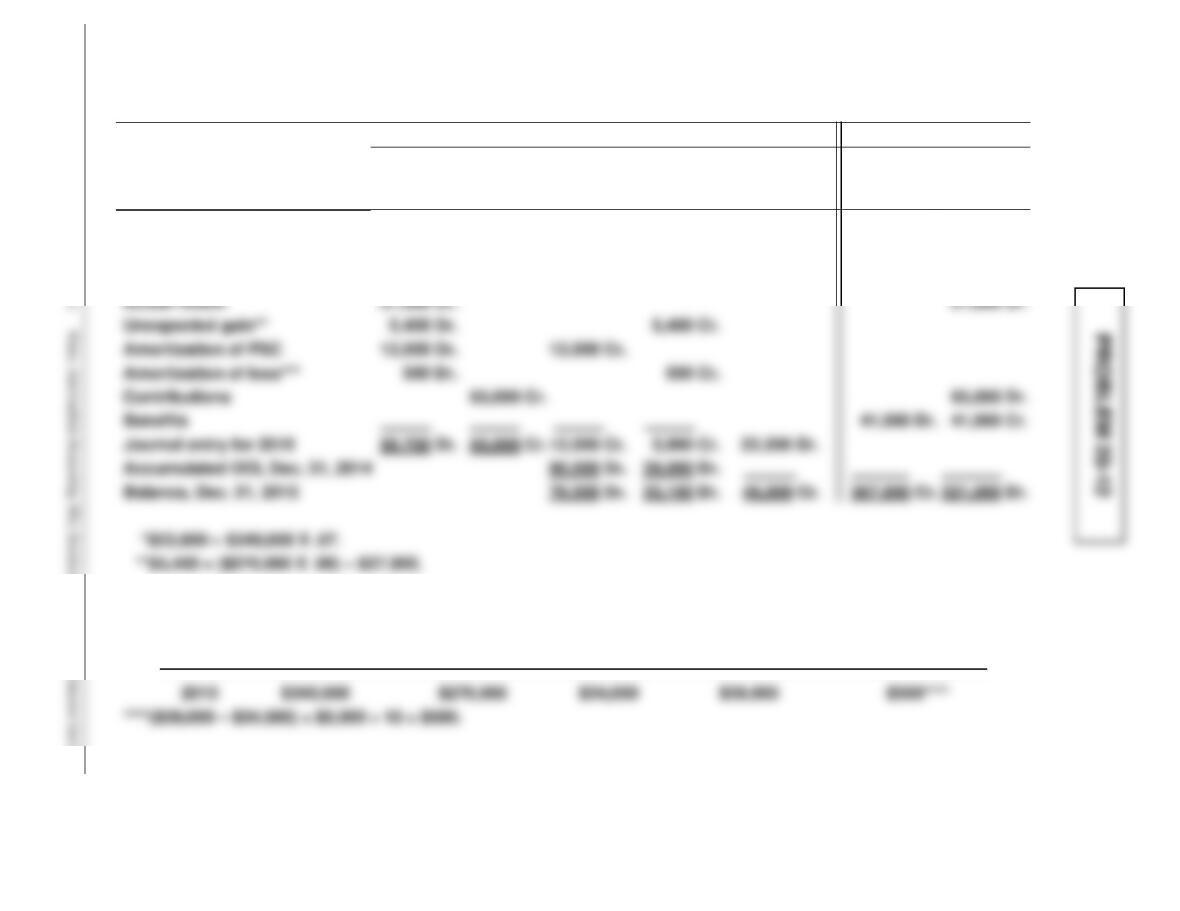

(a) LARSON CORP.

Pension Worksheet—2015

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2015

70,000 Cr.

340,000 Cr.

270,000 Dr.

Service cost

45,000 Dr.

45,000 Cr.

Interest cost*

23,800 Dr.

23,800 Cr.

***

Year

1/1 Projected

Benefit

Obligation

Value of 1/1

Plan Assets

10%

Corridor

Accumulated

OCI (G/L), 1/1

Minimum

Amortization of

Loss for 2015

20–66 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

Actual return

27,000 Cr.

Unexpected gain**

Amortization of PSC

12,000 Dr.

Amortization of loss***

Contributions

65,000 Cr.

Benefits

41,000 Dr.

Journal entry for 2015

59,700 Dr.

65,000 Cr.

Accumulated OCI, Dec. 31, 2014

39,000 Dr.

Balance, Dec. 31, 2015

33,100 Dr.

46,800 Cr.

321,000 Dr.

PROBLEM 20-12 (Continued)

(b) 2015

Pension Expense …………………………………………….. 59,700

(c) Financial Statements—2015

Income Statement

Pension expense ………………………………………. $59,700

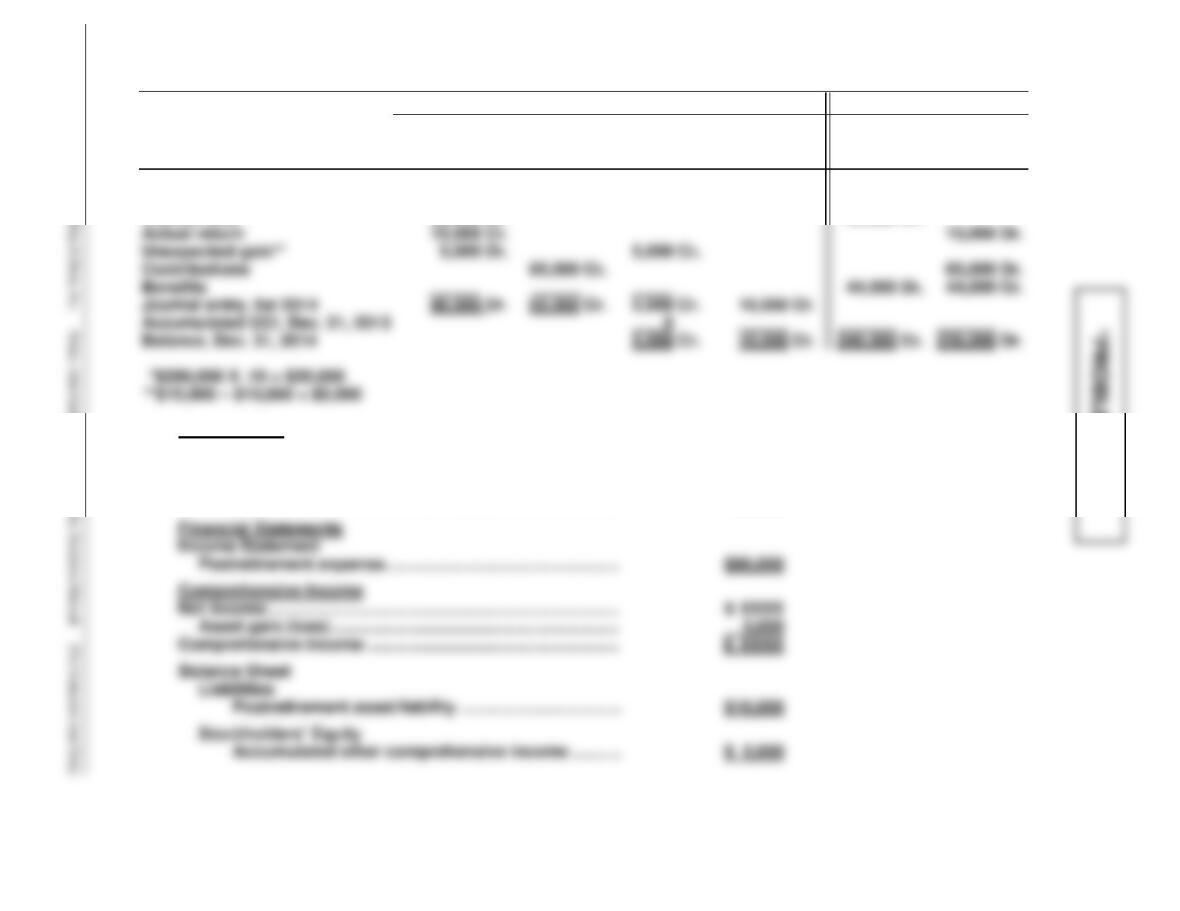

(a) HOLLENBECK FOODS INC.

Postretirement Benefit Worksheet—2014

General Journal Entries

Memo Record

Items

Annual

Postretirement

Expense

Cash

OCI—Gain/

Loss

Postretirement

Asset/Liability

APBO

Plan Assets

Balance, Jan. 1, 2014

200,000 Cr.

200,000 Dr.

Service cost

70,000 Dr.

70,000 Cr.

Interest cost*

20,000 Dr.

20,000 Cr.

(b) Journal Entry

Postretirement Expense …………………………………………. 80,000

Other Comprehensive Income (G/L) ………………….. 5,000

Postretirement Asset/Liability …………………………... 10,000

Cash ……………………………………………………………….. 65,000

20–68 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

Actual return

15,000 Cr.

Unexpected gain**

Contributions

Benefits

44,000 Dr.

Journal entry, for 2014

80,000 Dr.

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

246,000 Cr.

236,000 Dr.

*PROBLEM 20-14

(a) See worksheet on next page.

(b) December 31, 2014

Postretirement Expense ……………………………….. 120,000

(c) See worksheet on next page. The entry is below.

December 31, 2015

Other Comprehensive Income (PSC) ……………… 163,000

(d) Financial Statements—2015

Income Statement

Postretirement expense …………………………. $221,800

Balance Sheet

Liabilities

Postretirement liability ……………………………………. $488,500

General Journal Entries Memo Record

Annual

Expense

Cash

OCI—Prior

Service Cost

OCI—

Gain/Loss

Postretirement

Asset/Liability

APBO

Plan

Assets

Balance, Jan. 1, 2014

0

2,250,000 Cr.

2,250,000 Dr.

Service cost

75,000 Dr.

75,000 Cr.

Interest costa

225,000 Dr.

225,000 Cr.

Actual return

140,000 Cr.

140,000 Dr.

*PROBLEM 20-14 (Continued)

20–70 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

Unexpected lossb

40,000 Cr.

40,000 Dr.

Contributions

45,000 Cr.

Benefits

40,000 Dr.

Journal entry for 2014

120,000 Dr.

45,000 Cr.

40,000 Dr.

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

40,000 Dr.

2,510,000 Cr.

2,395,000 Dr.

Additional PSC, 1/1/2015

Balance, Jan. 1, 2015

2,685,000 Cr.

Service cost

85,000 Dr.

85,000 Cr.

268,500 Dr.

268,500 Cr.

Actual return

120,000 Cr.

120,000 Dr.

Unexpected lossd

23,700 Cr.

23,700 Dr.

Amortization of PSC

12,000 Dr.

Contributions

35,000 Cr.

Benefits

45,000 Dr.

Journal entry for 2015

221,800 Dr.

35,000 Cr.

Accumulated OCI, Dec. 31, 2014

40,000 Dr.

Balance, Dec. 31, 2015

63,700 Dr.

2,993,500 Cr.

2,505,000 Dr.

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 20-1 (Time 30–35 minutes)

Purpose—to provide the student with the opportunity to discuss some of the more traditional issues

CA 20-2 (Time 25–30 minutes)

Purpose—to provide the student with the opportunity to discuss the terminology employed in GAAP

related to pension accounting.

CA 20-3 (Time 20–25 minutes)

CA 20-4 (Time 30–35 minutes)

Purpose—to provide the student with the opportunity to study some of the implications of GAAP as it

CA 20-5 (Time 50–60 minutes)

CA 20-6 (Time 30–40 minutes)

Purpose—to provide the student with the opportunity to explain gains and losses, including the use of

corridor amortization.

CA 20-7 (Time 20–30 minutes)

CA 20-1

(b) The employer is the organization sponsoring the pension plan. The employer incurs the costs

(c) (1) Relative to the pension fund the term “funded” refers to the relationship between pension

funded.

(2) Relative to the pension fund, the pension liability is an actuarial concept representing an

economic liability under the pension plan for future cash payments to retirees. From the

viewpoint of the employer, the pension liability is an accounting credit that results from an

excess of amounts expensed over amounts contributed (funded) to the pension fund.

(d) (1) The theoretical justification for accrual recognition of pension costs is based on the matching

concept. Pension costs are incurred during the period over which an employee renders

(2) Although cash (pay-as-you-go) accounting is highly objective for the final determination of

actual pension costs, it provides no measurement of annual pension costs as they are

incurred. Accrual accounting provides greater objectivity in the annual measurement of

CA 20-1 (Continued)

(e) Terms and their definitions as they apply to accounting for pension plans follow:

(1) Service cost is the actuarial present value of benefits attributed by the pension benefit formula

to employee service during that period. The service cost component is a portion of the

projected benefit obligation and is unaffected by the funded status of the plan.

(2) Prior service costs are the retroactive benefits granted in a plan amendment (or initiation).

(3) Vested benefits are benefits that are not contingent on the employee continuing in the service

of the employer. In some plans the payment of the benefits will begin only when the

employee reaches the normal retirement date; in other plans the payment of the benefits

CA 20-2

1. Pension asset/liability in the asset section is the excess of the fair value of pension plan assets

over the projected benefit obligation.

2. Pension asset/liability in the liability section is the excess of the projected benefit obligation over

the fair value of the pension plan assets.

3. Accumulated OCI—PSC arises when an additional liability is recognized in the PBO due to prior

4. Pension expense is the amount recognized in an employer’s financial statements as the expense

for a pension plan for the period. Components of pension expense are service cost, interest cost,

CA 20-3

(a) (1) The theoretical justification for accrual recognition of pension costs is based on the matching

(2) Although cash (pay-as-you-go) accounting is highly objective for the final determination of

(b) Terms and their definitions as they apply to accounting for pensions follow:

(1) Market-related asset value, when based on a calculated value, is a moving average of

pension plan asset values over a period of time. Considerable flexibility is permitted in

(2) The projected benefit obligation is the present value of vested and nonvested employee

benefits accrued to date based on employees’ future salary levels. This is the pension

liability required by GAAP.

(3) The corridor approach was developed by the FASB as the method for determining when to

(c) The following disclosures about a company’s pension plans should be made in financial

statements or their notes:

1. A description of the plan including employee groups covered, type of benefit formula,

funding policy, types of assets held, and the nature and effect of significant matters affecting

comparability of information for all periods presented.

2. The components of net periodic pension expense for the period.

CA 20-4

(a) Pension benefits are part of the compensation received by employees for their services. The

actual payment of these benefits is deferred until after retirement. The net periodic pension

expense measures this compensation and consists of the following five elements:

1. The service cost component is the present value of the benefits earned by the employees

during the current period.

2. Since a pension represents a deferred compensation agreement, a liability is created when

the plan is adopted. The interest cost component is the increase in that liability, the projected

benefit obligation, due to the passage of time.

(b) The major similarity between the accumulated benefit obligation and the projected benefit

obligation is that they both represent the present value of the benefit attributed by the pension

benefit formula to employee service rendered prior to a specific date. All things being equal,

when an employee is about to retire, the accumulated benefit obligation and the projected benefit

obligation would be the same.

The major difference between the accumulated benefit obligation and the projected benefit

(c) (1) Pension gains and losses, sometimes called actuarial gains and losses, result from changes

in the value of the projected benefit obligation or the fair value of the plan assets. These

(2) In order to decrease the volatility of the reporting of the pension gains or losses, the FASB

had adopted what is referred to as the “corridor approach.” This approach achieves the

CA 20-5

1. This situation can exist because companies vary as to whether they are using an implicit or

explicit set of assumptions when interest rates are disclosed. In the implicit approach, two or

more assumptions do not individually represent the best estimate of the plan’s future experience

with respect to these assumptions, but the aggregate effect of their combined use is presumed to

be approximately the same as that of an explicit approach. In the explicit approach, each

2. This situation will occur because the net funded position of the plan is required to be reported.

That is, companies are required to report as a liability the excess of their projected benefit

obligation over the fair value of plan assets. In the past, the basic liability companies reported

was the excess of the amount expensed over the amount funded.

3. This statement is questionable. If a financial measure purports to represent a phenomenon that is

volatile, the measure must show that volatility or it will not be representationally faithful. Never–

the-less, many argue that volatility is inappropriate when dealing with such long-term measures

4. (a) In a defined-contribution plan, the amount contributed is the amount expensed. No significant

reporting problems exist here. On the other hand, defined benefit plans involve many difficult

reporting issues which may lead to additional expense and liability recognition.

Significant amendments will generally increase prior service cost which may lead to

5. The corridor method is an approach which requires that only gains and losses in excess of 10%

of the greater of the projected benefit obligation or market related plan asset value be allocated.

CA 20-6

To: Vickie Plato, Accounting Clerk

From: Good Student, Manager of Accounting

Date: January 3, 2016

Subject: Amortization of gains and losses in pension expense

Pension expense includes several components; one occasionally included is the amortization of

To decide whether or not you should include gains/losses in annual pension expense, calculate 10 percent

of either the PBO or the PA (whichever is greater) as a “corridor.” Amortize the amount of any gain or

loss falling outside the corridor over the average remaining service life of the active employees. Note: these

gains/losses must exist at the beginning of the year for which amortization takes place [see (a) on the

schedule below].

Thus, in the attached schedule, no amortization of the $280,000 loss in 2013 was required because the

balance in the gain/loss account at the beginning of that year was zero. However, at the beginning

of 2014, the balance in that account was $280,000. The 10 percent corridor is $250,000, so the loss

Finally, if the losses from 2015 are added to the unamortized portion of the loss from prior years, the

sum ($368,000) falls within the 2016 corridor ($390,000) and does not need to be amortized at all.

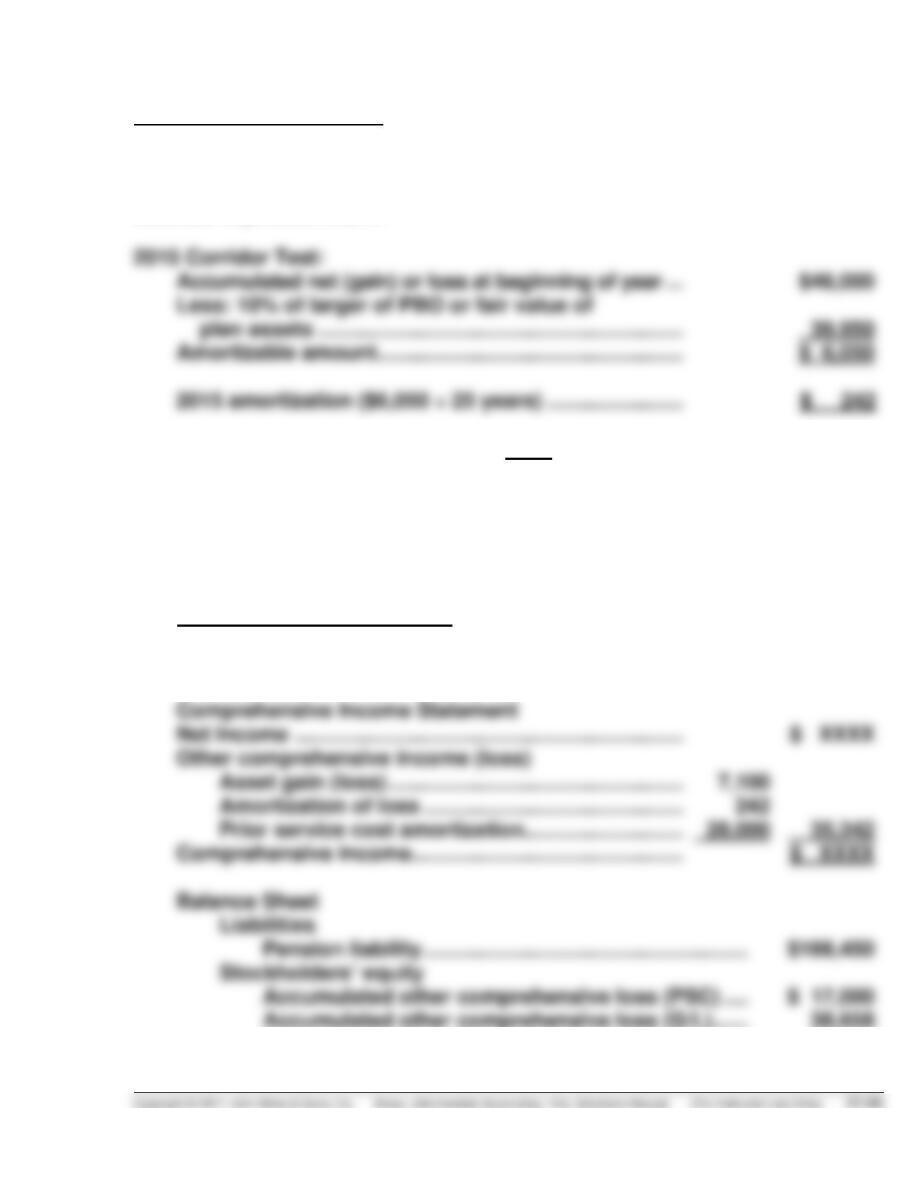

Corridor and Minimum Loss Amortization Schedule

Year

Projected Benefit

Obligation (a)

Plan Assets

Value (a)

10% Corridor

Accumulated

OCI (G/L) (a)

Minimum

Amortization

of Loss

2013

$2,200,000

$1,900,000

$220,000

$ 0

$ 0

CA 20-6 (Continued)

(a) As of the beginning of the year.

(b) ($280,000 – $250,000) ÷ 10 years = $3,000

CA 20-7

While Habbe may be correct in assuming that the termination of nonvested employees would decrease its

pension-related liabilities and associated expenses, she is callous to suggest that firing employees is a

FINANCIAL REPORTING PROBLEM

(a) P&G offers various postretirement benefits to its employees. The most

prevalent employee benefit plans offered are defined contribution plans,

(b)

2011

Pension expense

$538,000,000

2010

Pension expense

$469,000,000

2009

Pension expense

$341,000,000

(c) In 2011, P&G reports a $4,388,000,000 Accrued Pension Cost on its

balance sheet. It reports $538,000,000 as pension expense on its income

statement. It also reports a postretirement liability of $1,516,000,000

classified as non-current.

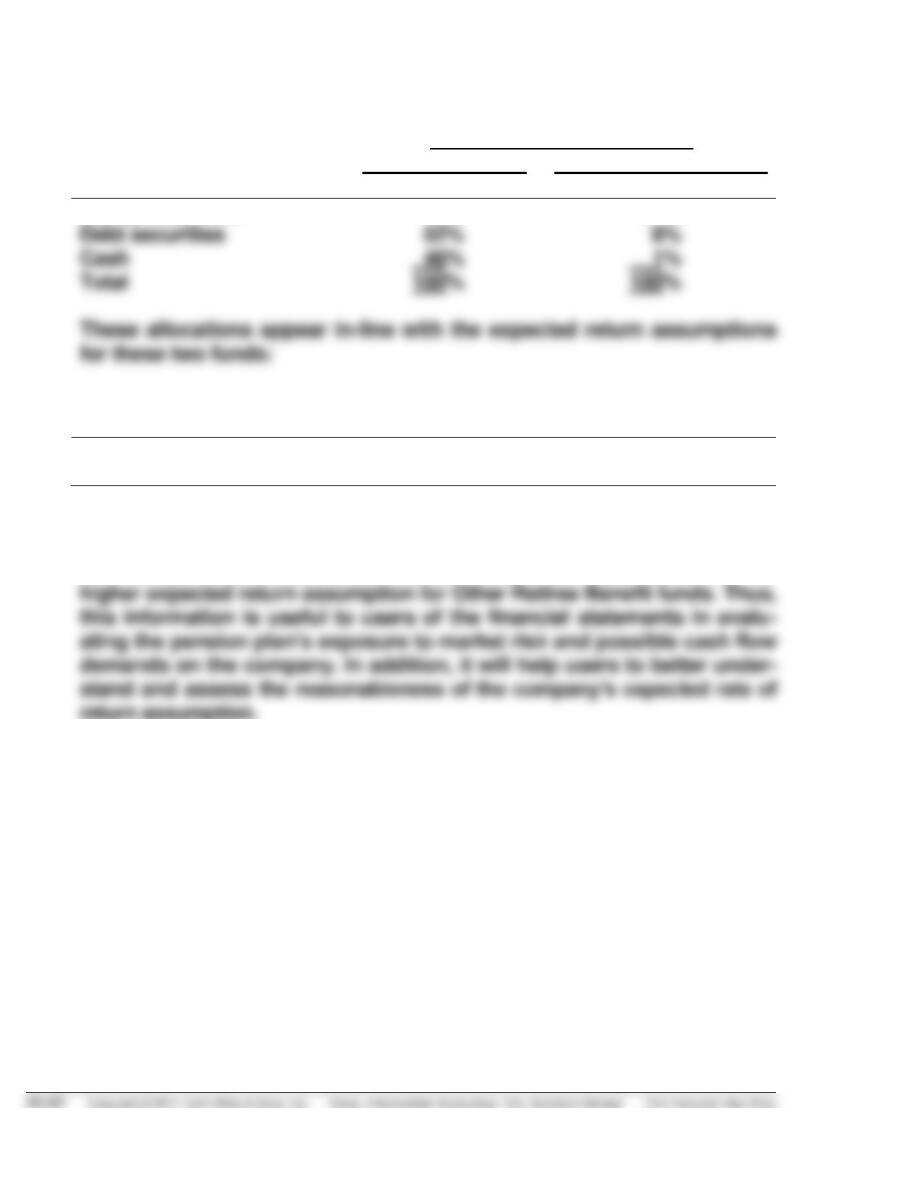

FINANCIAL REPORTING PROBLEM (Continued)

Asset Allocation at June 30

Pension Benefits

Other Retiree Benefits

Asset Category

2011

2011

Equity securities

2%

91%

Debt securities

Total

2011 Assumptions used to

determine net periodic cost

Pensions

Other Retiree

Expected return on

plan assets

7.0%

9.2%

As indicated, almost all of the assets in the Other Retiree Benefit fund

are equity investments, which should earn higher (if not also riskier)

returns than debt investments. The differences are consistent with the