Extensive detail and information is contained within the help function of Microsoft Excel and in the provided text.

You should enter your name, date, instructor’s name, and course into the cells at the top of the page. This information will be

printed on the top of each page if the template requires more than one page.

And information or data which may be required by the solution will be entered in cells with borders to help identify them.

Be advised, the template workbooks and worksheets are not protected.

Overtyping any data may remove it.

Each template is set to print with File Name, Page # of # Page(s), the print date, and the print time to assist in assembly

of multiple pages.

Where a highlighted cell shows “Date” enter the appropriate date for that step of the challenge. This may be any date format that

Microsoft Excel accepts. Some of these formats include “1/1/12″, “01/01/12”, and “01/01/2012.” All of these will return January

01, 2012, in the format set in the template.

cells with borders or in other yellow highlighted cells. The formula may be a simple “Look to” formula, an equal sign and a cell

reference, “=E27” or more complex as “=E27*5,” or something similar to the time-value-of-money formula. These are addressed in

the tutorial text provided for Microsoft Excel.

Where a highlighted cell shows “Acct Nbr” enter the appropriate account number, provided in the template and in the text for that

step of the challenge. This is entry may be a “Look to” formula to another cell where that information has been provided or

previously entered.

Check with your instructor to see if abbreviated account titles are acceptable. For example “A/R” for Accounts Receivable, “A/P”

for Accounts Payable. If your instructor is using a comparison process between workbooks for grading, these abbreviates may not

be acceptable.

Where a highlighted cell shows titles such as “Values,” “Amounts,” or “Quantities” enter the appropriate numerical value for that

step of the challenge. The cell is formatted for proper presentation of the entered information. If a dollar sign is appropriate, it

should not be entered, Microsoft Excel will place it there through formatting. Commas and significant digits (decimals) are also set

through formatting for common presentation. Since the formatting of the templates is not protected by any password, you may

change any of the formatting found in the templates to meet your desires.

text requires one, two, or three significant digits in a presentation, the template has been set for that presentation in the

appropriate cells.

Where a highlighted cell shows titles such as “Journal Number” or “Journ #” you should enter the appropriate number provided in

the template and in the text for that step of the challenge. In general this will appear in instances such as “Record the following

events in General Journal number six.”

Where a highlighted cell shows “Text” enter the appropriate text for that step of the challenge. This may be a memorandum entry

for a journal entry or a lengthy text answer discussing the results of an analysis of a company‘s financials. These titles can simply be

typed over.

The print area is defined to fit onto 8 1/2″ × 11″ sheets in portrait or landscape mode as required. Margins are generally set to no

less than 1/2″ so most printers can print them without a problem. If you printer cannot accept margins less than 1″ you may have to

reformat the margins through Page Setup.

negative value if both cells E10 and E11 contain positive values.

Name: Date:

Instructor: Course:

$72,000

$440,000

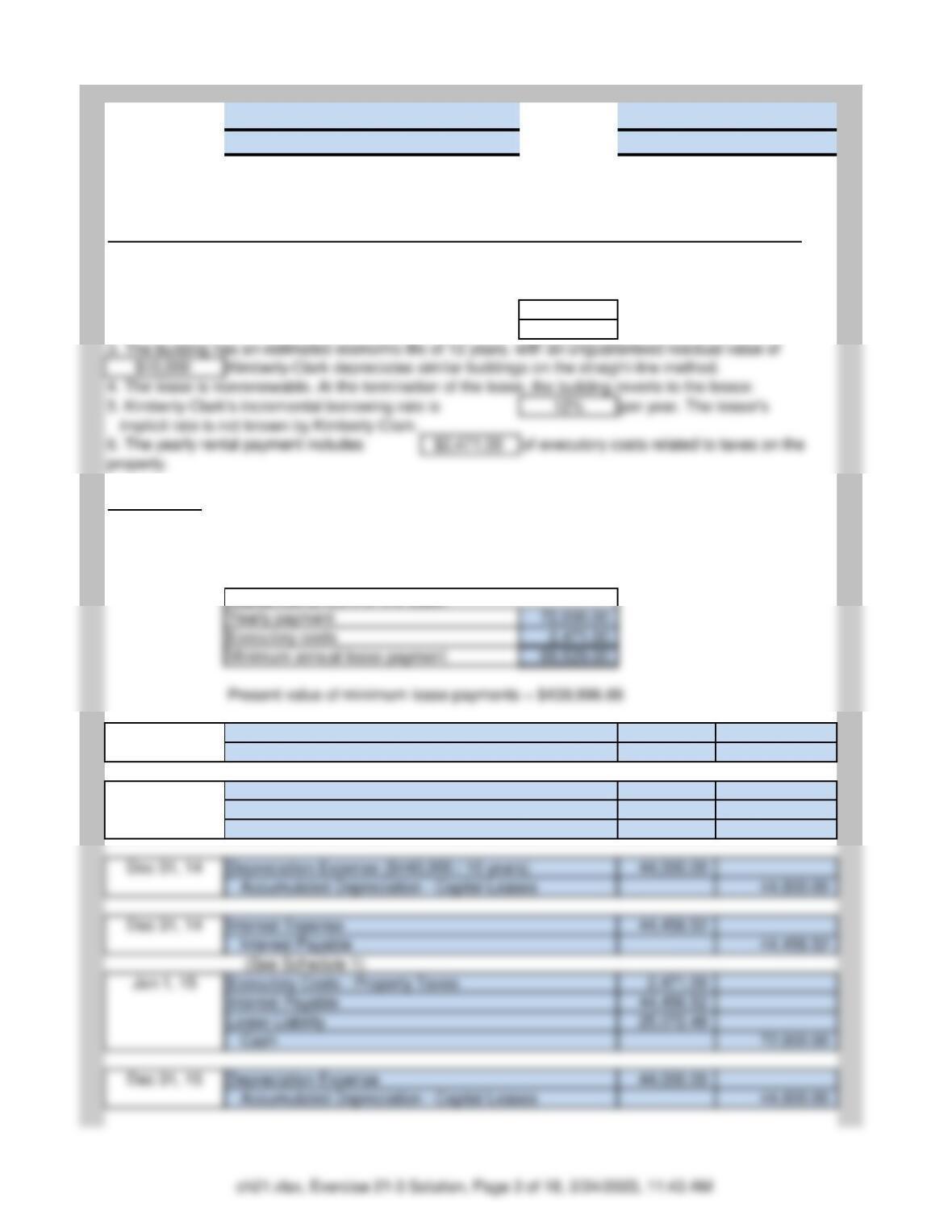

Yearly payment

Executory costs

Minimum annual lease payment

Present value of minimum lease payments = $439,996.88

Depreciation Expense ($440,000 / 10 years)

Accumulated Depreciation – Capital Leases

Interest Expense

Interest Payable

(See Schedule 1)

Executory Costs – Property Taxes

Lease Liability

Interest Payable

Cash

Depreciation Expense

Accumulated Depreciation – Capital Leases

440,000.00

440,000.00

2,471.00

69,529.00

72,000.00

Solution

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

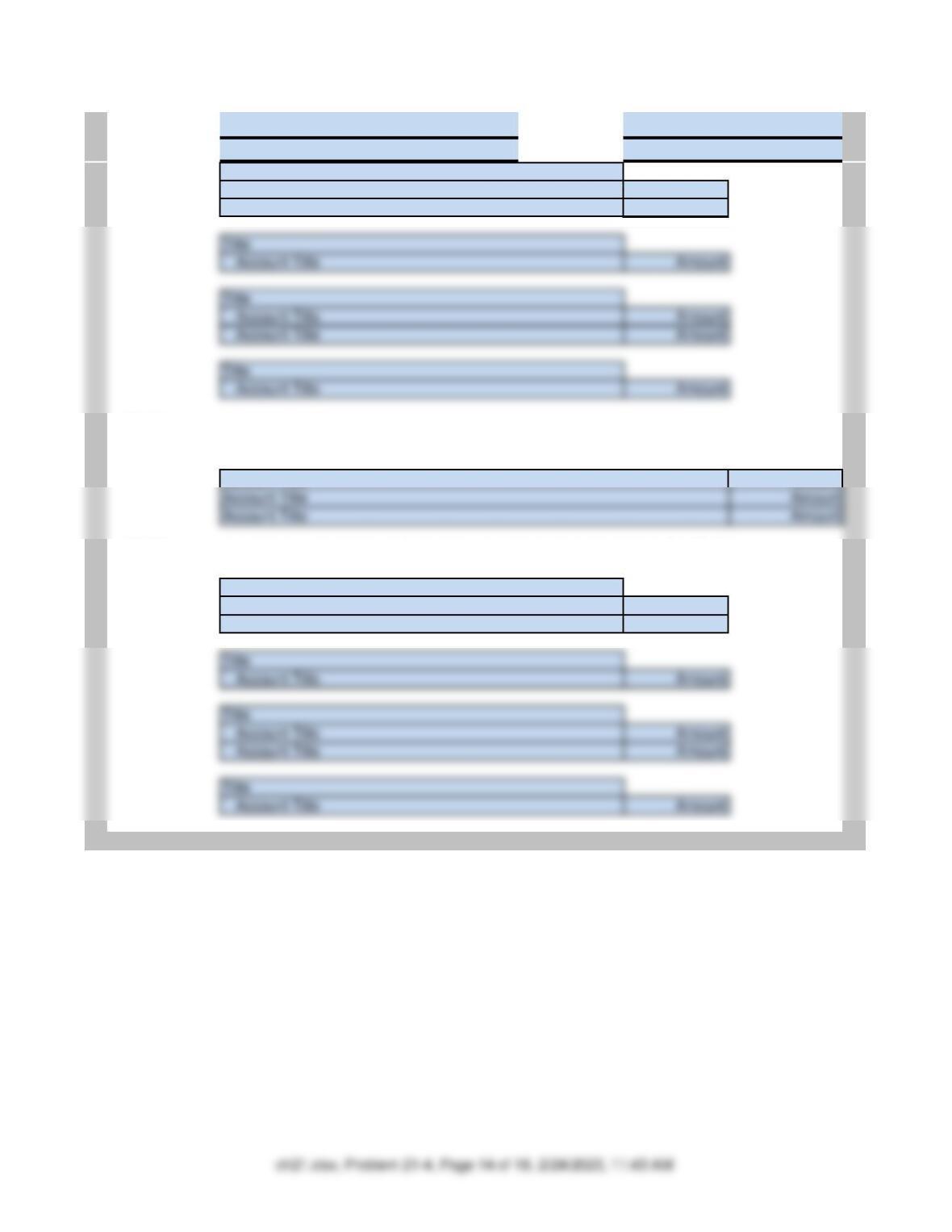

E21-3 (Lessee Entries, Capital Lease with Executory Costs and Unguaranteed Residual Value)

Assume that on January 1, 2014, Kimberly-Clark Corp. signs a 10-year noncancelable lease agreement to

lease a storage building from Trevino Storage Company. The following information pertains to this lease

agreement.

1. The agreement requires equal rental payments of

beginning on January 1, 2014.

2. The fair value of the building on January 1, 2014, is

Instructions:

Prepare the journal entries on the lessee’s books to reflect the signing of the lease agreement and to

record the payments and expenses related to this lease for the years 2014 and 2015. Kimberly-Clark’s

corporate year end is December 31.

Jan 1, 14

Leased Building

Lease Liability

Jan 1, 14

Executory Costs

Lease Liability

Cash

Capitalized amount of the lease:

3. The building has an estimated economic life of 12 years, with an unguaranteed residual value of

Kimberly-Clark depreciates similar buildings on the straight-line method.

4. The lease is nonrenewable. At the termination of the lease, the building reverts to the lessor.

of executory costs related to taxes on the

5. Kimberly-Clark’s incremental borrowing rate is

per year. The lessor’s

implicit rate is not known by Kimberly-Clark.

Name: Date:

Instructor: Course:

Solution

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

41,447.82

41,447.82

Schedule 1:

Date

Annual

Payment

Less

Executory

Costs

Interest

(12%)

on Liability

Reduction

of

Lease

Liability

Lease

Liability

Lease Amortization Schedule

Annual Payment Less Executory Costs

Dec 31, 15

Interest Expense

Interest Payable

KIMBERLY-CLARK CORPORATION (Lessee)

ch21.xlsx, Exercise 21-3 Solution, Page 4 of 18, 2/24/2023, 11:43 AM

Name: Date:

Instructor: Course:

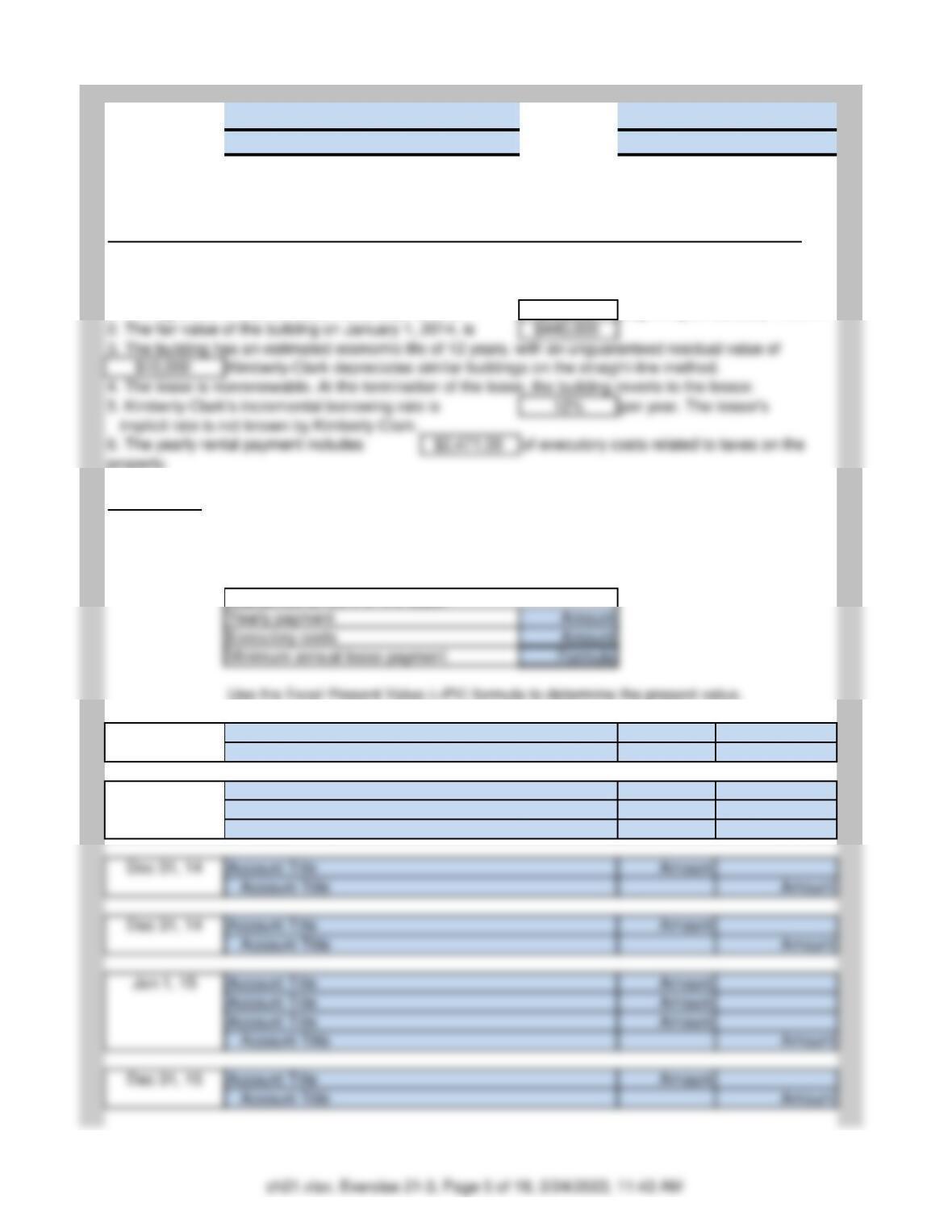

$72,000

Yearly payment

Executory costs

Minimum annual lease payment

Account Title

Account Title

Account Title

Account Title

Account Title

Account Title

Account Title

Account Title

Account Title

Account Title

Amount

Amount

Amount

Amount

Amount

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

E21-3 (Lessee Entries, Capital Lease with Executory Costs and Unguaranteed Residual Value)

Assume that on January 1, 2012, Kimberly-Clark Corp. signs a 10-year noncancelable lease agreement to

lease a storage building from Trevino Storage Company. The following information pertains to this lease

agreement.

1. The agreement requires equal rental payments of

beginning on January 1, 2014.

property.

Instructions:

Prepare the journal entries on the lessee’s books to reflect the signing of the lease agreement and to

record the payments and expenses related to this lease for the years 2012 and 2015. Kimberly-Clark’s

corporate year end is December 31.

Use the Excel Present Value (=PV) formula to determine the present value.

Jan 1, 14

Account Title

Account Title

Jan 1, 14

Account Title

Account Title

Account Title

Capitalized amount of the lease:

2. The fair value of the building on January 1, 2014, is

3. The building has an estimated economic life of 12 years, with an unguaranteed residual value of

Kimberly-Clark depreciates similar buildings on the straight-line method.

4. The lease is nonrenewable. At the termination of the lease, the building reverts to the lessor.

of executory costs related to taxes on the

5. Kimberly-Clark’s incremental borrowing rate is

per year. The lessor’s

implicit rate is not known by Kimberly-Clark.

Name: Date:

Instructor: Course:

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

Amount

Amount

Schedule 1:

Date

Annual

Payment

Less

Executory

Costs

Interest

(12%)

on Liability

Reduction

of

Lease

Liability

Lease

Liability

Jan 1, 14 Amount

Lease Amortization Schedule

Annual Payment Less Executory Costs

Dec 31, 15

Account Title

Account Title

KIMBERLY-CLARK CORPORATION (Lessee)

ch21.xlsx, Exercise 21-3, Page 6 of 18, 2/24/2023, 11:43 AM

Name: Date:

Instructor: Course:

8 -year period

$35,013

Solution

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

Instructions:

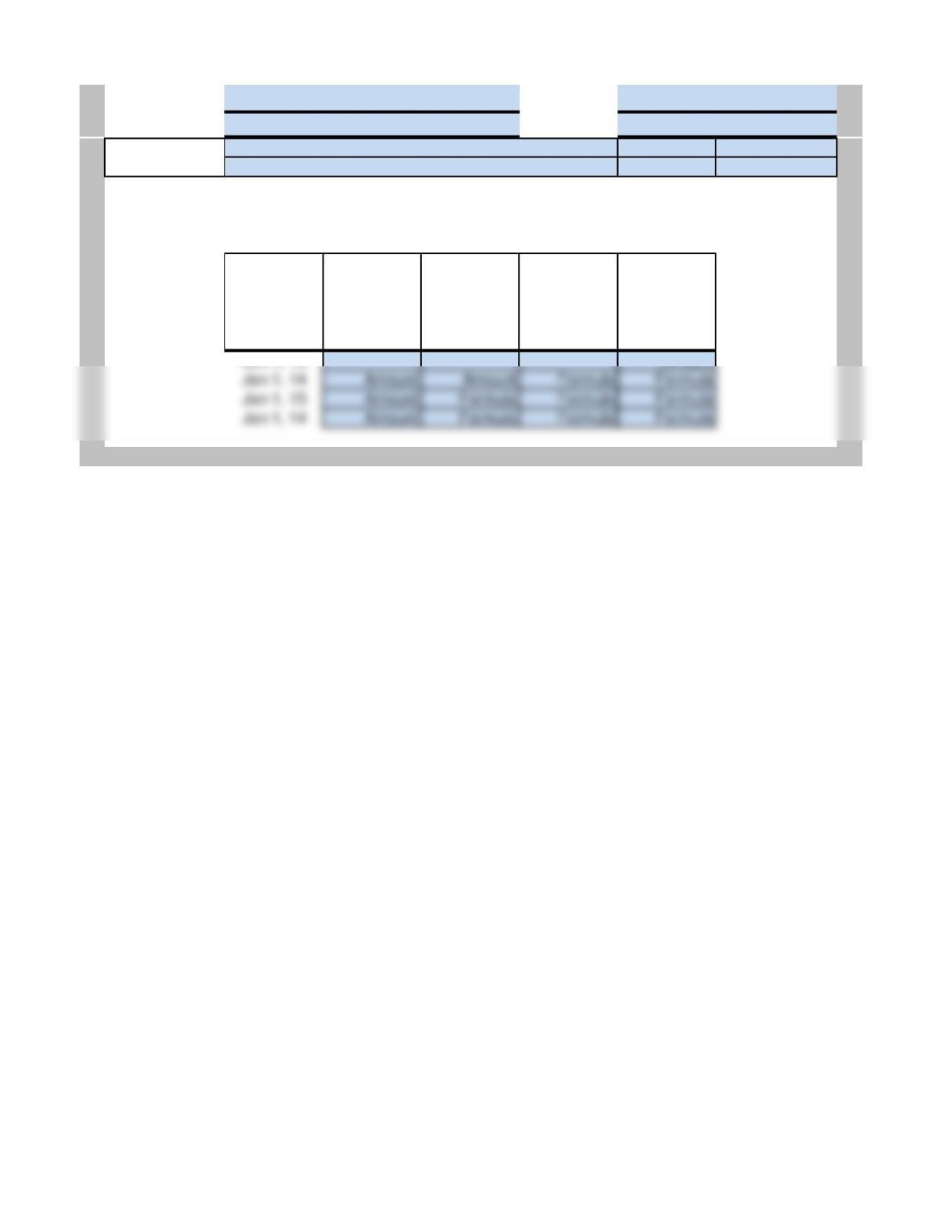

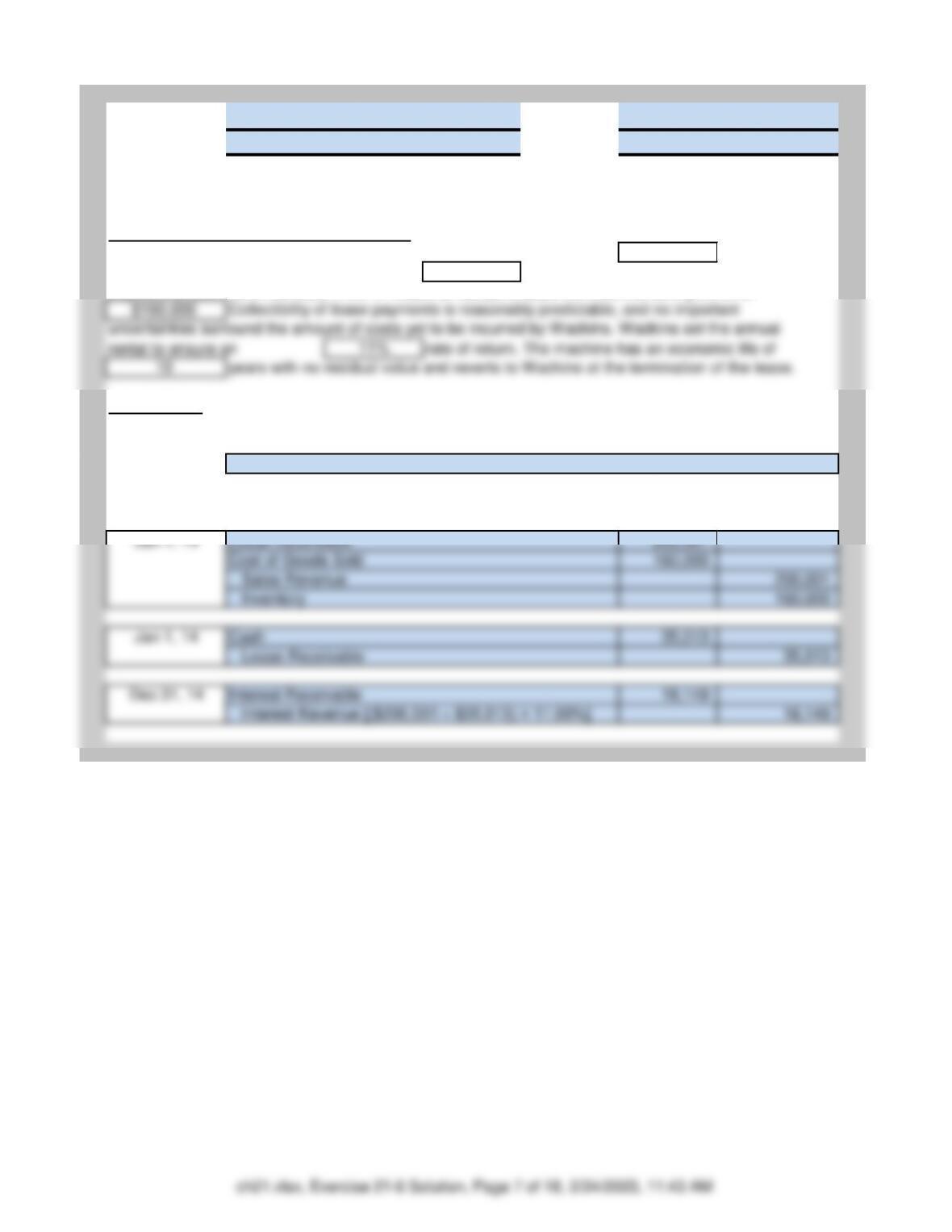

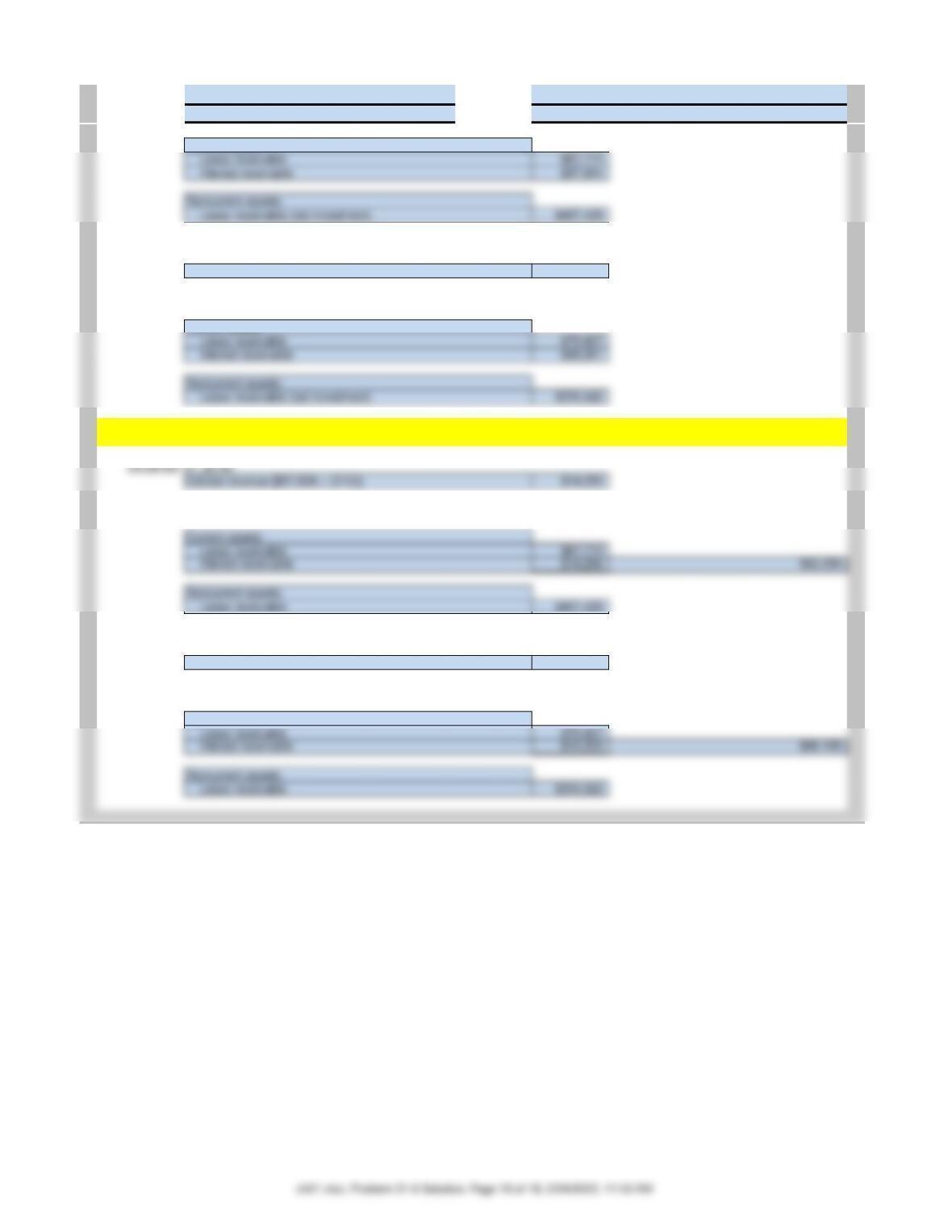

E21-6 (Lessor Entries, Sales-Type Lease) Crosley Company, a machinery dealer, leased a

(a) Compute the amount of the lease receivable. (Use the Excel Present Value formula “=PV(” to solve.)

The present value of the lease receivable is = $200,001

(b) Prepare all necessary journal entries for Wadkins for 2014.

machine to Romero Corporation on January 1, 2014. The lease is for an

and requires equal annual payments of

at the beginning of each year. The first

payment is received on January 1, 2014. Wadkins had purchased the machine during 2013 for

Name: Date:

Instructor: Course:

8 -year period

Account Title

Account Title

$35,013

Amount

Amount

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

Instructions:

E21-6 (Lessor Entries, Sales-Type Lease) Crosley Company, a machinery dealer, leased a

(a) Compute the amount of the lease receivable. (Use the Excel Present Value formula “=PV(” to solve.)

Use this area to enter the Present Value formula

(b) Prepare all necessary journal entries for Crosley for 2014.

Jan 1, 14

Account Title

Account Title

machine to Dexter Corporation on January 1, 2014. The lease is for an

and requires equal annual payments of

at the beginning of each year. The first

ch21.xlsx, Exercise 21-6, Page 8 of 18, 2/24/2023, 11:43 AM

payment is received on January 1, 2014. Wadkins had purchased the machine during 2013 for

rental to ensure an

rate of return. The machine has an economic life of

years with no residual value and reverts to Crosley at the termination of the lease.

Name: Date:

Instructor: Course:

October 1, 2014

6 years

Date:

Annual lease

Payment /

Receipt:

Interest (10%)

on Unpaid

Liabililty /

Receivable:

Reduction of

Lease Liability /

Receivable:

Balance of

Lease Liability /

Receivable:

10/01/14 300,383

10/01/14 62,700 62,700 237,683

Solution

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

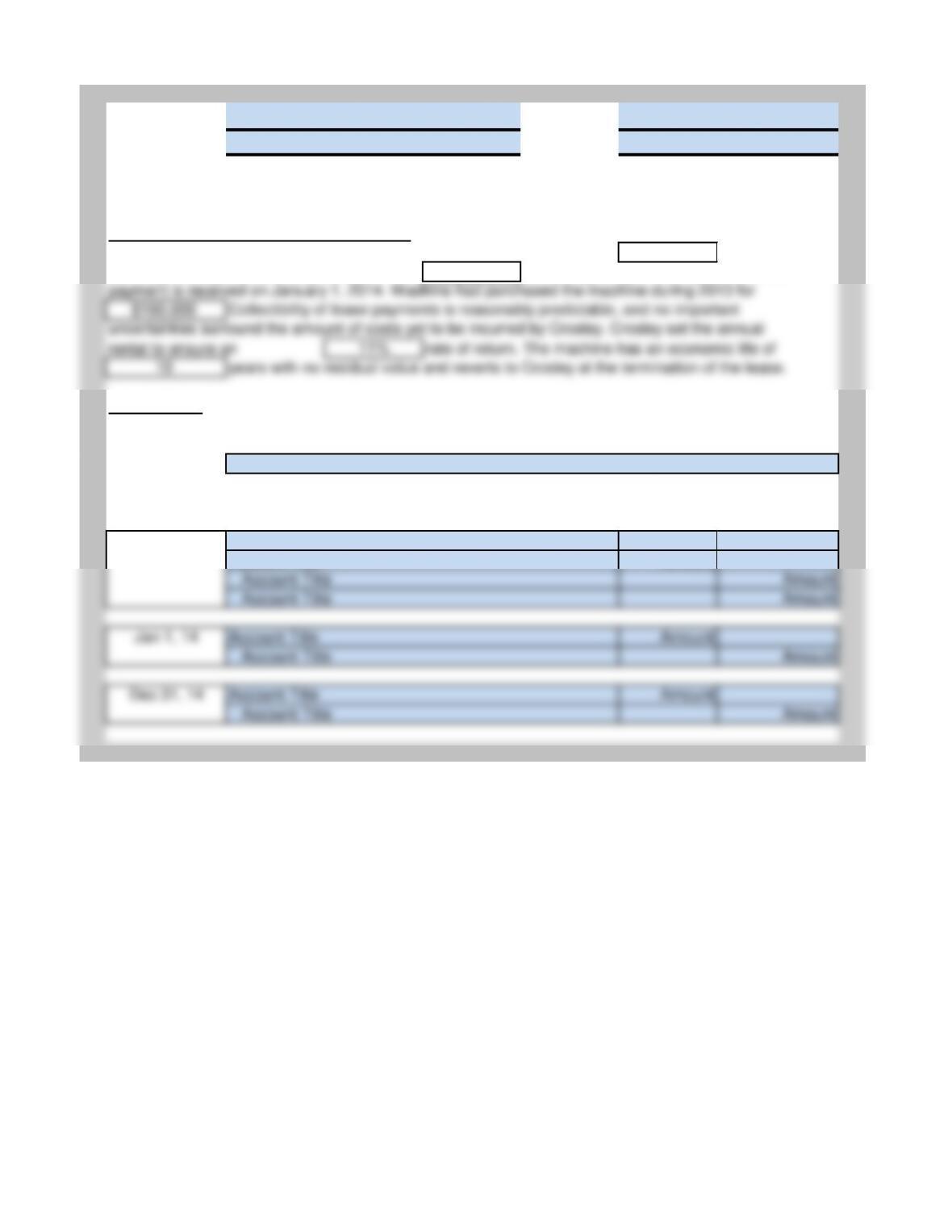

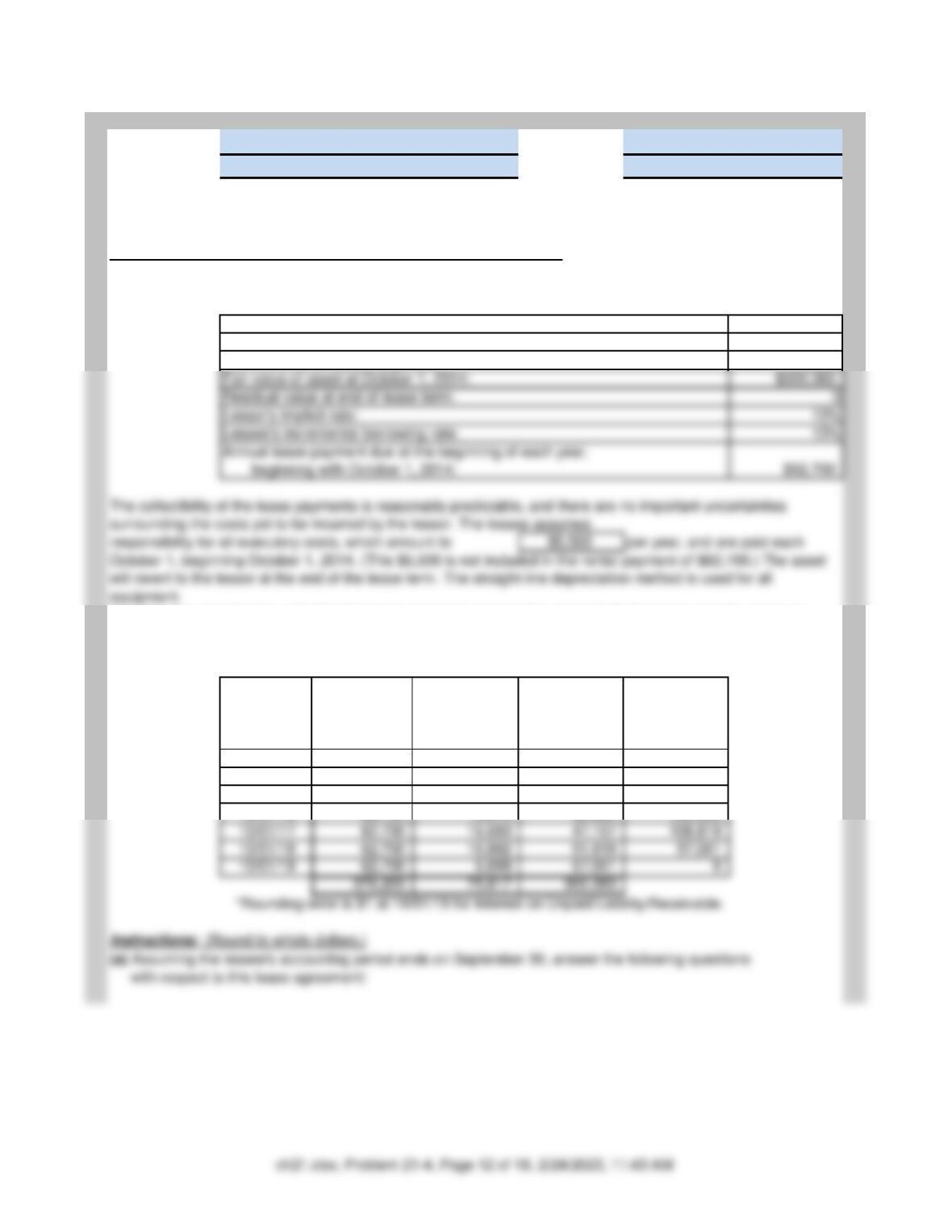

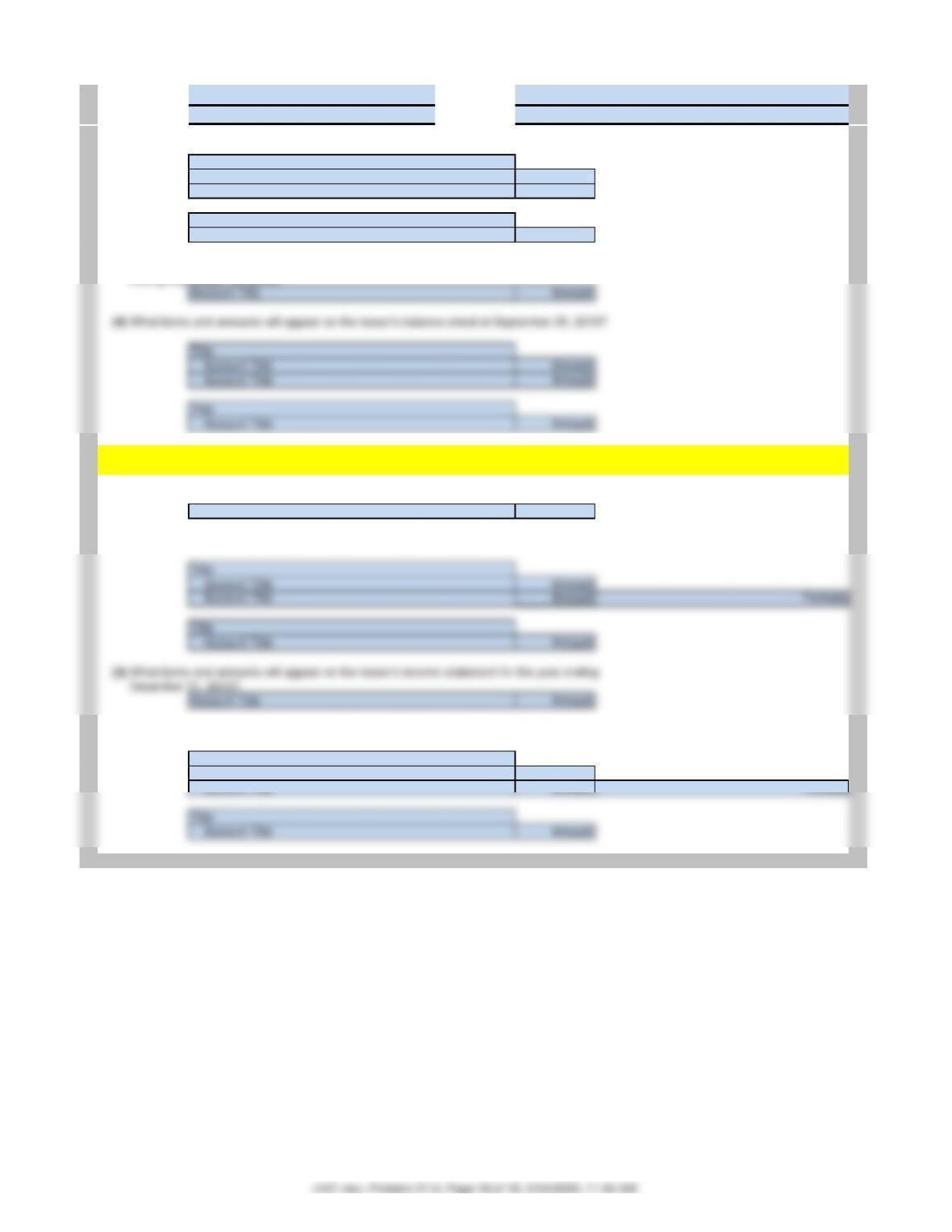

P21-4 (Balance Sheet and Income Statement Disclosure—Lessee) The following facts pertain to a

noncancelable lease agreement between Alschuler Leasing Company and McKee Electronics, a lessee, for a

computer system.

Inception date:

Lease term:

October 1, beginning October 1, 2014. (This $5,500 is not included in the rental payment of $62,700.) The asset

will revert to the lessor at the end of the lease term. The straight-line depreciation method is used for all

equipment.

The following amortization schedule has been prepared correctly for use by both the lessor and the lessee in

accounting for this lease. The lease is to be accounted for properly as a capital lease by the lessee and as a

direct-finance lease by the lessor.

Instructions: (Round to whole dollars.)

(a) Assuming the lessee’s accounting period ends on September 30, answer the following questions

with respect to this lease agreement:

Fair value of asset at October 1, 2014:

Residual value at end of lease term:

Lessor’s implicit rate:

Lessee’s incremental borrowing rate:

Annual lease payment due at the beginning of each year,

Economic life of lease equipment:

The collectibility of the lease payments is reasonably predictable, and there are no important uncertainties

surrounding the costs yet to be incurred by the lessor. The lessee assumes

responsibility for all executory costs, which amount to

per year, and are paid each

Name: Date:

Instructor: Course:

Solution

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

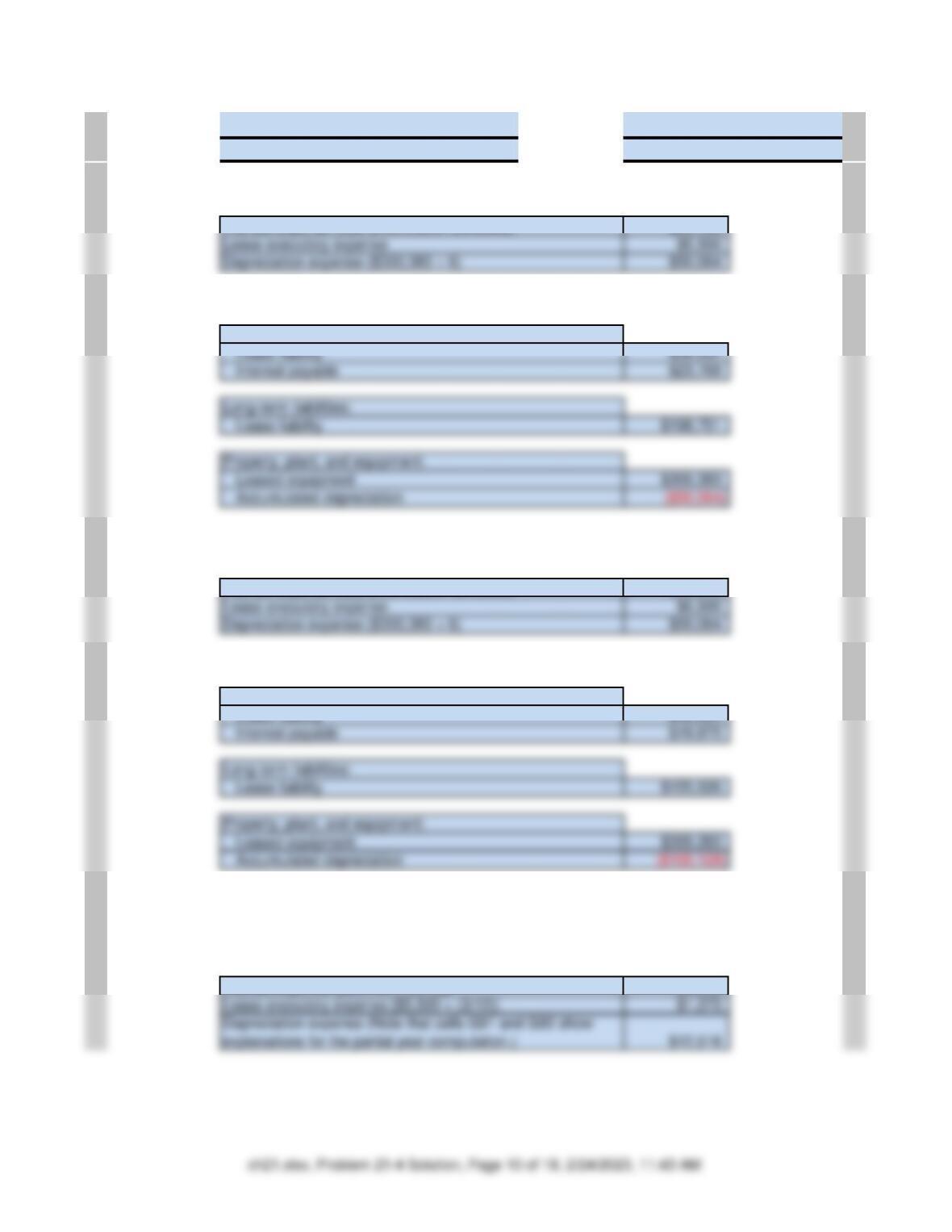

$23,768

Long-term liabilities:

Property, plant, and equipment:

$19,875

Lease executory expense

Depreciation expense ($300,383 ÷ 6)

Property, plant, and equipment:

Long-term liabilities:

$5,942

Lease executory expense [$5,500 × (3/12)]

Interest expense (See amortization schedule)

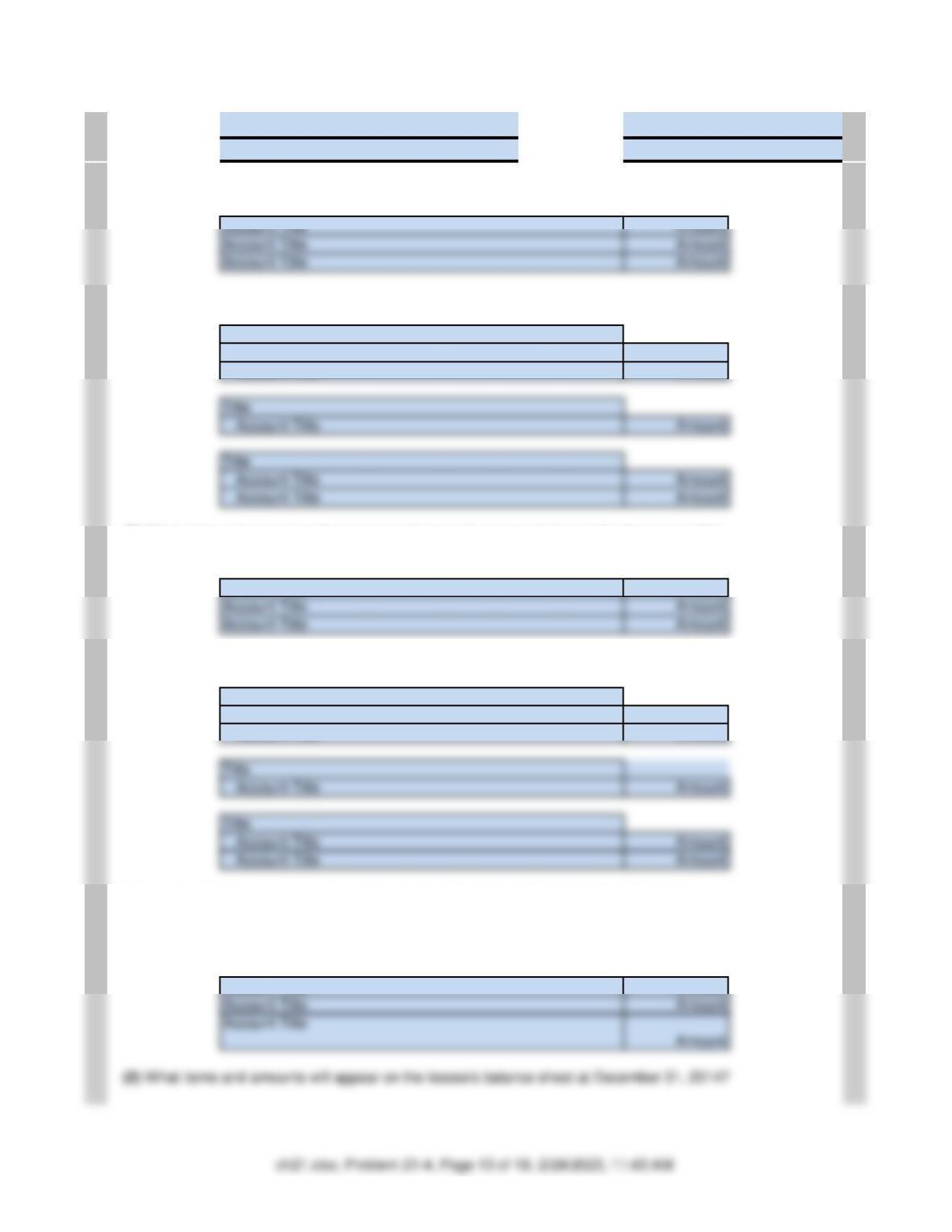

(1) What items and amounts will appear on the lessee’s income statement for the year ending

September 30, 2015?

(2) What items and amounts will appear on the lessee’s balance sheet at September 30, 2015?

Current liabilities:

(3) What items and amounts will appear on the lessee’s income statement for the year ending

September 30, 2016?

Interest expense (See amortization schedule)

(4) What items and amounts will appear on the lessee’s balance sheet at September 30, 2016?

Current liabilities:

(b) Assuming the lessee‘s accounting period ends on December 31, answer the following questions

with respect to this lease agreement:

(1) What items and amounts will appear on the lessee’s income statement for the year ending

December 31, 2014?

Interest expense [$23,768 × (3/12)]

Lease executory expense

Depreciation expense ($300,383 ÷ 6)

Name: Date:

Instructor: Course:

Solution

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

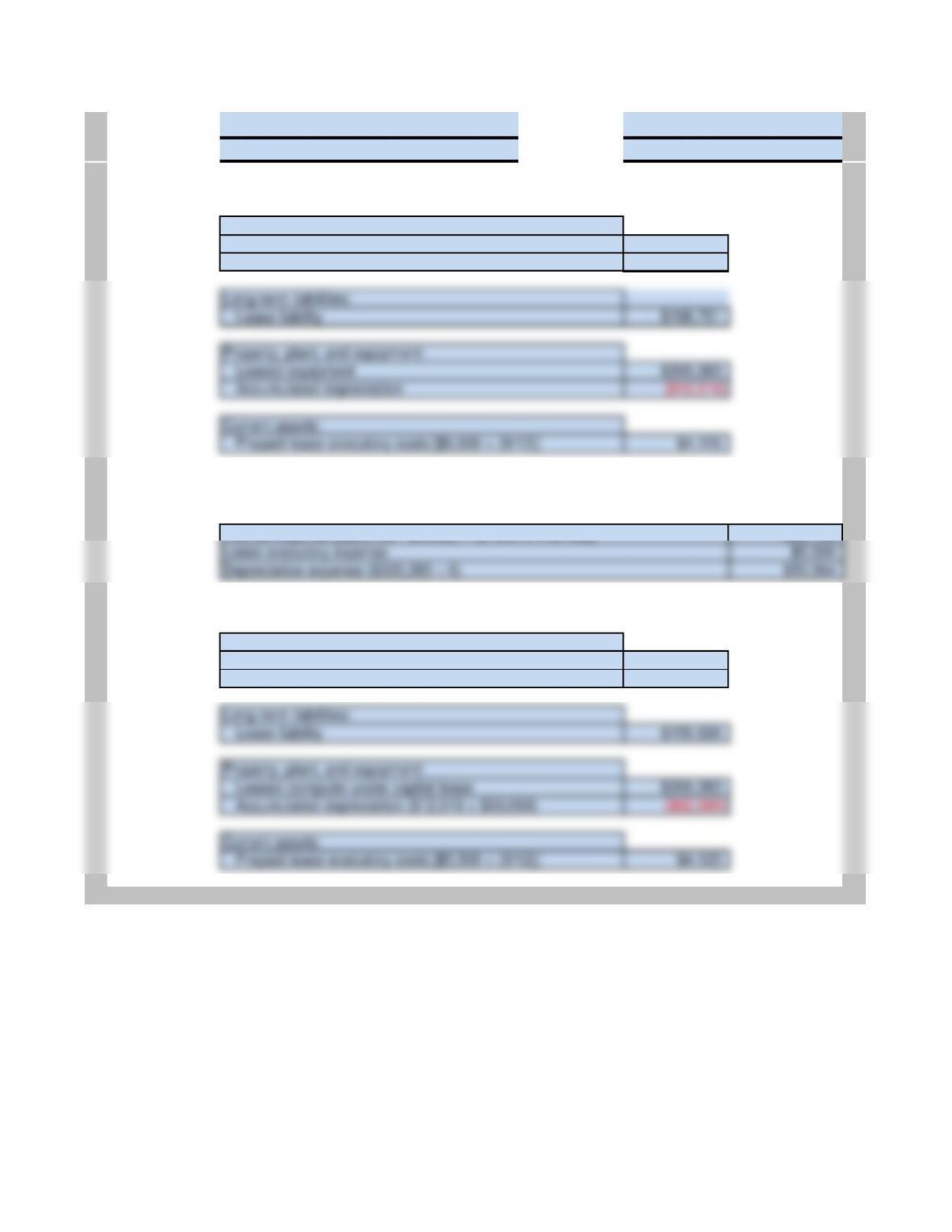

$38,932

$5,942

$22,795

Depreciation expense ($300,383 ÷ 6)

Lease executory expense

Current assets:

Prepaid lease executory costs [$5,500 × (9/12)]

Property, plant, and equipment:

Leased computer under capital lease

Accumulated depreciation ($12,516 + $50,064)

Long-term liabilities:

Lease liability

$42,825

$4,969

(2) What items and amounts will appear on the lessee’s balance sheet at December 31, 2014?

Current liabilities:

Lease liability

Interest payable

Current liabilities:

Lease liability

Interest expense [$19,875 × (3/12)]

(3) What items and amounts will appear on the lessee’s income statement for the year ending

December 31, 2015?

Interest expense [($23,768 – $5,942) + ($19,875 × (3/12))]

(4) What items and amounts will appear on the lessee’s balance sheet at December 31, 2015?

ch21.xlsx, Problem 21-4 Solution, Page 11 of 18, 2/24/2023, 11:43 AM

Property, plant, and equipment:

Leased equipment

Accumulated depreciation

Long-term liabilities:

Lease liability

Current assets:

Prepaid lease executory costs [$5,500 × (9/12)]

Name: Date:

Instructor: Course:

October 1, 2014

6 years

6 years

Date:

Annual lease

Payment /

Receipt:

Interest (10%)

on Unpaid

Liabililty /

Receivable:

Reduction of

Lease Liability /

Receivable:

Balance of

Lease Liability /

Receivable:

10/01/14 300,383

10/01/14 62,700 62,700 237,683

10/01/15 62,700 23,768 38,932 198,751

10/01/16 62,700 19,875 42,825 155,926

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

P21-4 (Balance Sheet and Income Statement Disclosure—Lessee) The following facts pertain to a

noncancelable lease agreement between Alschuler Leasing Company and McKee Electronics, a lessee, for a

computer system.

Inception date:

Lease term:

Economic life of lease equipment:

The following amortization schedule has been prepared correctly for use by both the lessor and the lessee in

accounting for this lease. The lease is to be accounted for properly as a capital lease by the lessee and as a

direct-finance lease by the lessor.

Fair value of asset at October 1, 2014:

Residual value at end of lease term:

Lessor’s implicit rate:

Lessee’s incremental borrowing rate:

surrounding the costs yet to be incurred by the lessor. The lessee assumes

responsibility for all executory costs, which amount to

per year, and are paid each

Name: Date:

Instructor: Course:

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

Title

Account Title

Title

Account Title

Account Title

Amount

Amount

Amount

Account Title

Account Title

Title

Account Title

Account Title

Title

Account Title

Amount

Amount

Amount

(2) What items and amounts will appear on the lessee’s balance sheet at December 31, 2014?

Account Title

(1) What items and amounts will appear on the lessee’s income statement for the year ending

September 30, 2015?

(2) What items and amounts will appear on the lessee’s balance sheet at September 30, 2015?

Title

Account Title

Account Title

(3) What items and amounts will appear on the lessee’s income statement for the year ending

September 30, 2016?

Account Title

(4) What items and amounts will appear on the lessee’s balance sheet at September 30, 2016?

Title

Account Title

Account Title

(b) Assuming the lessee‘s accounting period ends on December 31, answer the following questions

with respect to this lease agreement:

(1) What items and amounts will appear on the lessee’s income statement for the year ending

December 31, 2014?

Account Title

Amount

Account Title

Account Title

Account Title

Name: Date:

Instructor: Course:

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

Amount

Amount

Amount

Account Title

Account Title

Title

Account Title

Title

Account Title

Account Title

Title

Account Title

Amount

Amount

Title

Account Title

Account Title

Title

Account Title

Account Title

(3) What items and amounts will appear on the lessee’s income statement for the year ending

December 31, 2015?

Account Title

(4) What items and amounts will appear on the lessee’s balance sheet at December 31, 2015?

Title

Account Title

Account Title

Title

Account Title

Title

Account Title

Name: Date:

Instructor: Course:

January 1, 2014

6 years

6 years

(a) Prepare an amortization

schedule

would be suitable for

lease term.

Date:

Annual lease

Payment /

Receipt:

Interest (12%) on

Unpaid Liability /

Receivable:

Reduction of

Lease Liability

/ Receivable:

Balance of

Lease Liability

/ Receivable:

10/01/14 600,000.00

10/01/14 124,798.00 124,798.00 475,202.00

$57,024

P21-5 (Balance Sheet and Income Statement Disclosure—Lessor) The following facts pertain to a noncancelable lease agreement between

Faldo Leasing Company and Vance Electronics, a lessee, for a computer system.

Inception date:

Lease term:

Economic life of lease equipment:

Solution

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

The following amortization schedule has been prepared correctly for use by both the lessor and the lessee in accounting for this lease. The lease is

to be accounted for properly as a capital lease by the lessee and as a direct-finance lease by the lessor.

Instructions: (Round to whole dollars.)

Interest revenue

ch21.xlsx, Problem 21-6 Solution, Page 15 of 18, 2/24/2023, 11:43 AM

Fair value of asset at October 1, 2014:

Residual value at end of lease term:

Lessor’s implicit rate:

Lessee’s incremental borrowing rate:

October 1, beginning October 1, 2014. (This $5,000 is not included in the rental payment of $124,798.) The asset will revert to the lessor at the end

Name: Date:

Instructor: Course:

Solution

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

$48,891

Noncurrent assets:

$14,256

Interest revenue [$57,024 × (3/12)]

December 31, 2014?

Current assets:

Noncurrent assets:

$54,991

Noncurrent assets:

(2) What items and amounts will appear on the lessor’s balance sheet at September 30, 2015?

Current assets:

(3) What items and amounts will appear on the lessor’s income statement for the year

ending September 30, 2016?

Interest revenue

(4) What items and amounts will appear on the lessor’s balance sheet at September 30, 2016?

Current assets:

Assuming the lessor’s accounting period ends on December 31, answer the following questions

with respect to this lease agreement:

(1) What items and amounts will appear on the lessor’s income statement for the year ending

(2) What items and amounts will appear on the lessor’s balance sheet at December 31, 2014?

(3) What items and amounts will appear on the lessor’s income statement for the year ending

December 31, 2015?

Interest revenue [($57,024 – $14,256) + ($48,891 × (3/12))]

(4) What items and amounts will appear on the lessor’s balance sheet at December 31, 2015?

Current assets:

Noncurrent assets:

Name: Date:

Instructor: Course:

January 1, 2014

6 years

(a) Prepare an amortization schedule that

would be

lease term.

Date:

Annual lease

Interest (12%)

Reduction of

Balance of

10/01/14 600,000.00

10/01/14

related to the lease. Assume the lessee’s annual accounting period ends on December 31 and reversing entries are used when appropriate.

Account Title

P21-6 (Lessee Entries with Residual Value) The following facts pertain to a noncancelable lease agreement between Faldo Leasing

Company and Vance Company, a lessee, for a computer system.

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

Inception date:

Lease term:

Instructions: (Round to whole dollars.)

The following amortization schedule has been prepared correctly for use by both the lessor and the lessee in accounting for this lease. The

lease is to be accounted for properly as a capital lease by the lessee and as a direct-finance lease by the lessor.

(b) Prepare all of the journal entries for the lessee for 2014 and 2015 to record the lease agreement, the lease payments, and all expenses

(1) What items and amounts will appear on the lessor’s income statement for the year ending

September 30, 2015?

ch21.xlsx, Problem 21-6, Page 17 of 18, 2/24/2023, 11:43 AM

Fair value of asset at January 1, 2014:

Residual value of equipment at end of lease term, guaranteed by the lessee

Lessor’s implicit rate:

Lessee’s incremental borrowing rate:

Economic life of lease equipment:

Annual lease payment due at the beginning of each year,

The asset will revert to the lessor at the end of the lease term. The lessee has guaranteed the lessor a residual value of $50,000. The lessee

uses the straight-line depreciation method for all equipment.

Name: Date:

Instructor: Course:

Intermediate Accounting, 15th Edition by Kieso, Weygandt, and Warfield

Amount

Amount

Amount

Amount

Amount

Title

Account Title

Title

Account Title

December 31, 2015?

Account Title

Title

Account Title

Account Title

Amount

Title

Account Title

(2) What items and amounts will appear on the lessor’s balance sheet at September 30, 2015?

Account Title

Title

Account Title

(3) What items and amounts will appear on the lessor’s income statement for the year

ending September 30, 2016?

Assuming the lessor’s accounting period ends on December 31, answer the following questions

with respect to this lease agreement:

(1) What items and amounts will appear on the lessor’s income statement for the year ending

December 31, 2014?

Account Title

(2) What items and amounts will appear on the lessor’s balance sheet at December 31, 2014?

(4) What items and amounts will appear on the lessor’s balance sheet at December 31, 2015?

Title

Account Title

Amount

(4) What items and amounts will appear on the lessor’s balance sheet at September 30, 2016?

Title

Account Title

Account Title

Title

Account Title

Account Title