E21-9B (20–30 minutes)

Note: The lease agreement has a bargain purchase option. The collectibility of

the lease payments is reasonably predictable, and there are no important

uncertainties surrounding the costs yet to be incurred by the lessor. The

lease, therefore, qualifies as a capital lease from the viewpoint of the lessor.

(a) The lease receivable is computed as follows:

$ 31,415.63 Annual rental payment

X 4.99271 PV of annuity due of 1 for n = 6, i = 8%

$156,849.13 PV of periodic rental payments

E21-9B (Continued)

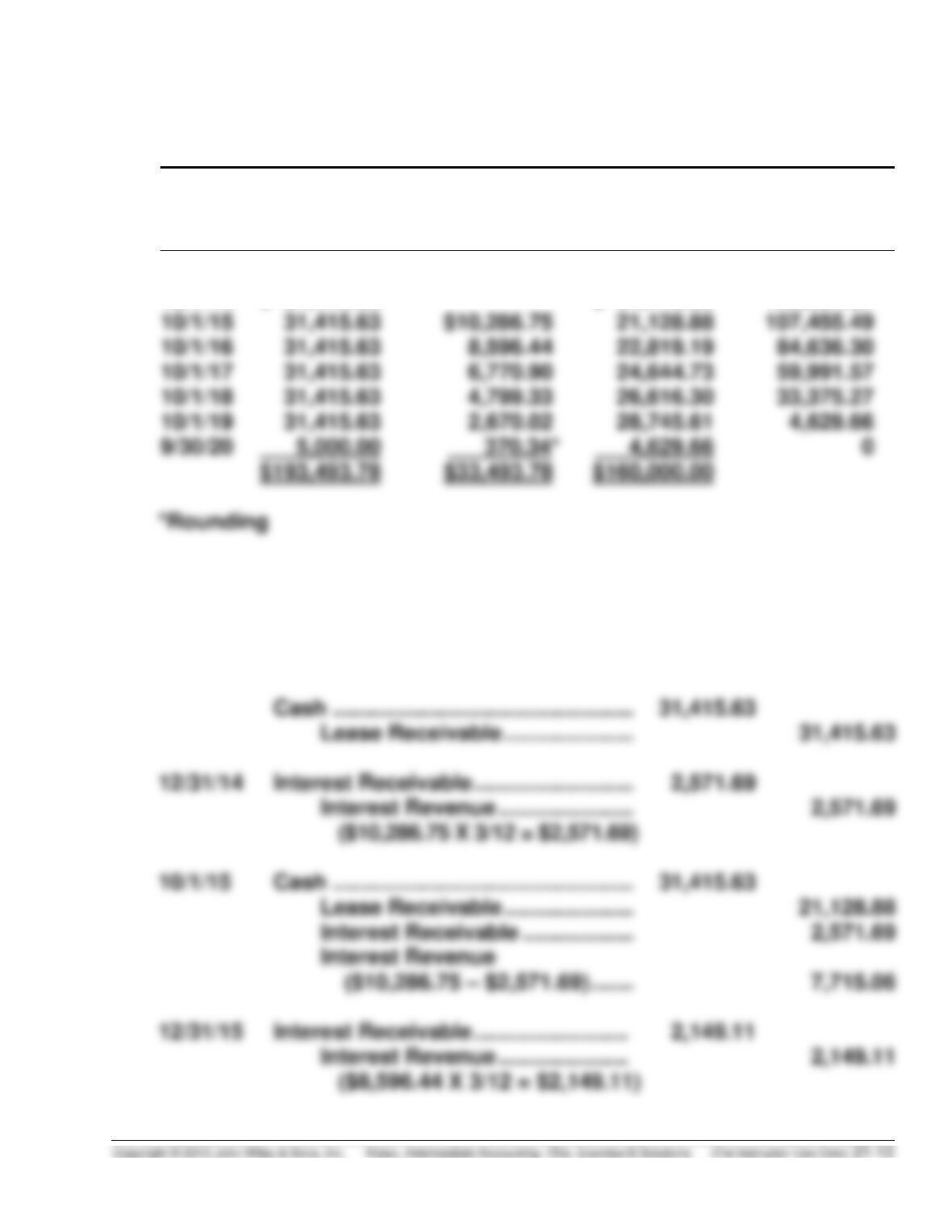

(b) EARTH LEASING CORPORATION (Lessor)

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

BPO

Interest (8%)

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

10/1/14

$160,000.00

10/1/14

$ 31,415.63

$ 31,415.63

128,584.37

10/1/15

10/1/16

10/1/17

10/1/18

10/1/19

5,000.00

$160,000.00

(c) 10/1/14 Lease Receivable ……………………….. 160,000.00

Cost of Goods Sold ……………………. 120,000.00

Sales ………………………………….. 160,000.00

Inventory …………………………….. 120,000.00

E21-9B (Continued)

10/1/14 Cash …………………………………………… 31,415.63

Lease Receivable ………………….. 22,819.19

Interest Receivable ……………….. 2,149.11

E21-10B (15–25 minutes)

(a) Fair market value of leased asset to lessor …………………. $850,000

Less: Present value of unguaranteed

residual value $92,547 X .54027

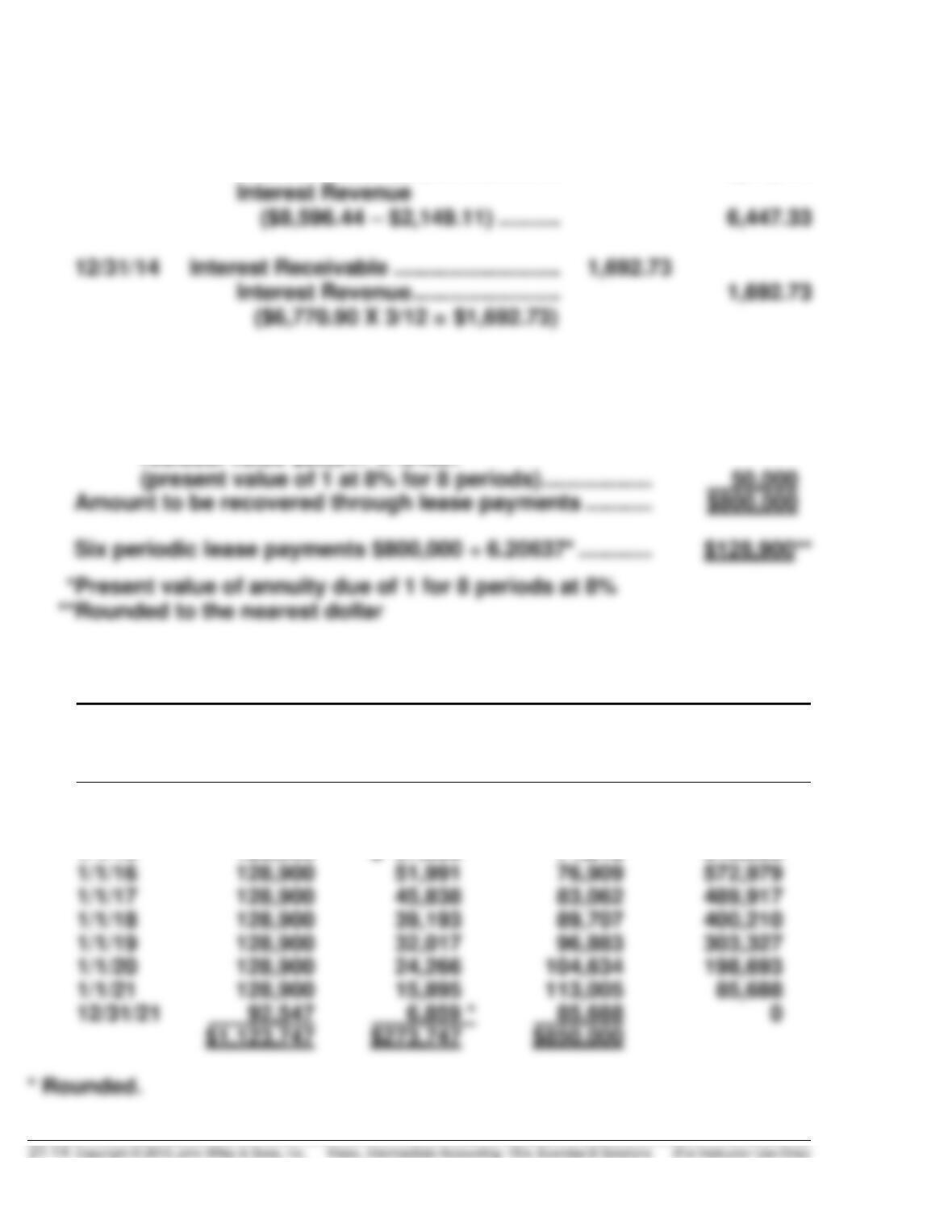

(b) HORIZON LEASING INC. (Lessor)

Lease Amortization Schedule

Date

Annual Lease

Payment Plus

URV

Interest (8%)

on Lease

Receivable

Recovery of

Lease

Receivable

Lease

Receivable

1/1/14

$850,000

1/1/14

$ 128,900

$128,900

721,100

1/1/15

128,900

$ 57,688

71,212

649,888

1/1/16

128,900

76,909

572,979

1/1/17

128,900

83,062

489,917

1/1/18

128,900

89,707

400,210

1/1/19

128,900

96,883

303,327

128,900

198,693

128,900

6,859 *

$1,123,747

$273,747

$850,000

E21-10B (Continued)

(c) 1/1/14 Lease Receivable ………………………… 71,212

Equipment …………………………... 71,212

E21-11B (20–30 minutes)

Note: This lease is a capital lease to the lessee because the lease term

(6 years) exceeds 75% of the remaining economic life of the asset (7 years).

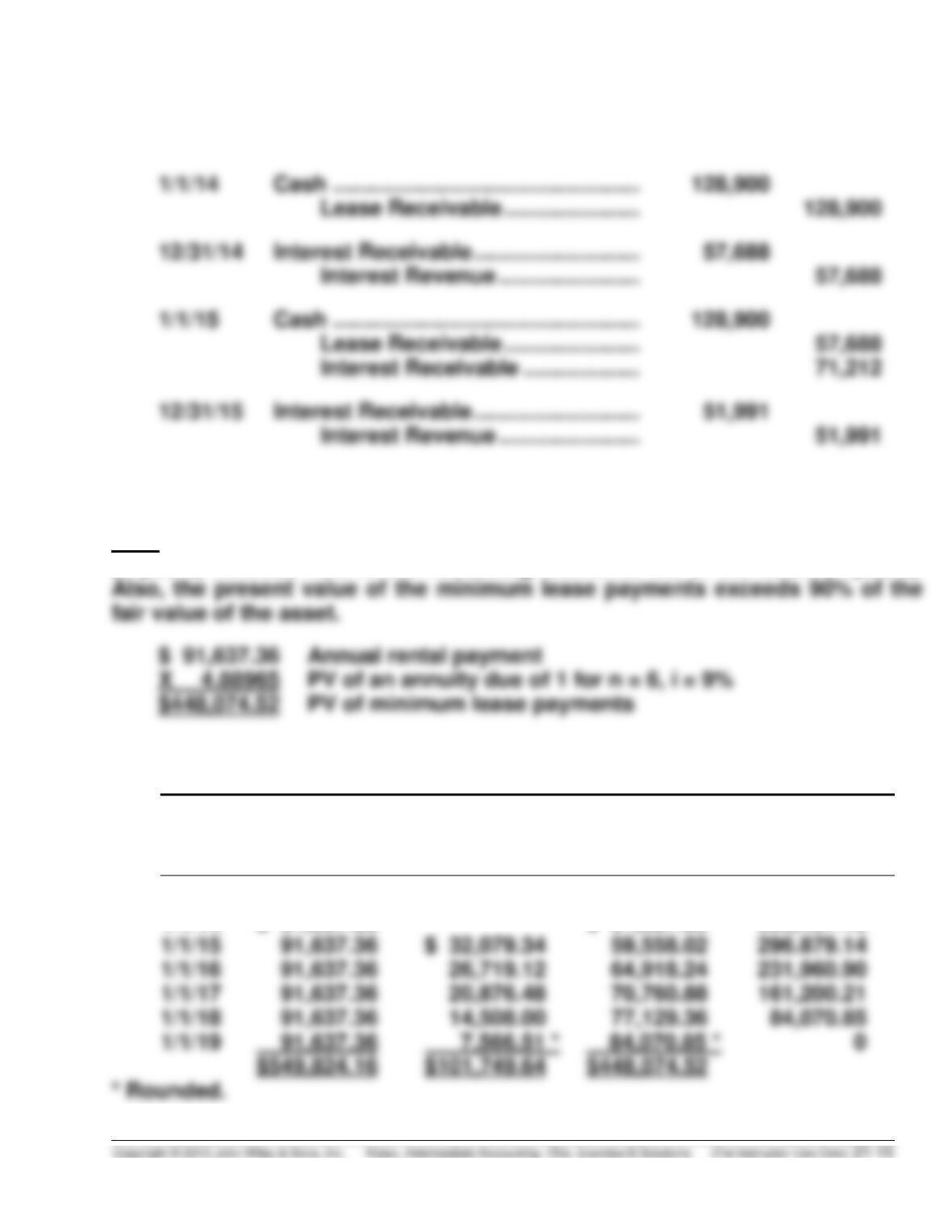

(a) CHELLS, INC. (Lessee)

Lease Amortization Schedule

Date

Annual Lease

Payment

Interest (9%)

on Liability

Reduction

of Lease

Liability

Lease Liability

1/1/14

$448,074.52

1/1/14

$ 91,637.36

$ 91,637.36

356,437.16

1/1/15

1/1/16

1/1/18

1/1/19

91,637.36

E21-11B (Continued)

(b) 1/1/14 Leased Equipment Under

Capital Leases ……………………….. 448,074.52

Lease Liability …………………….. 448,074.52

12/31/14 Interest Expense ……………………….. 32,079.34

Interest Payable ………………….. 32,079.34

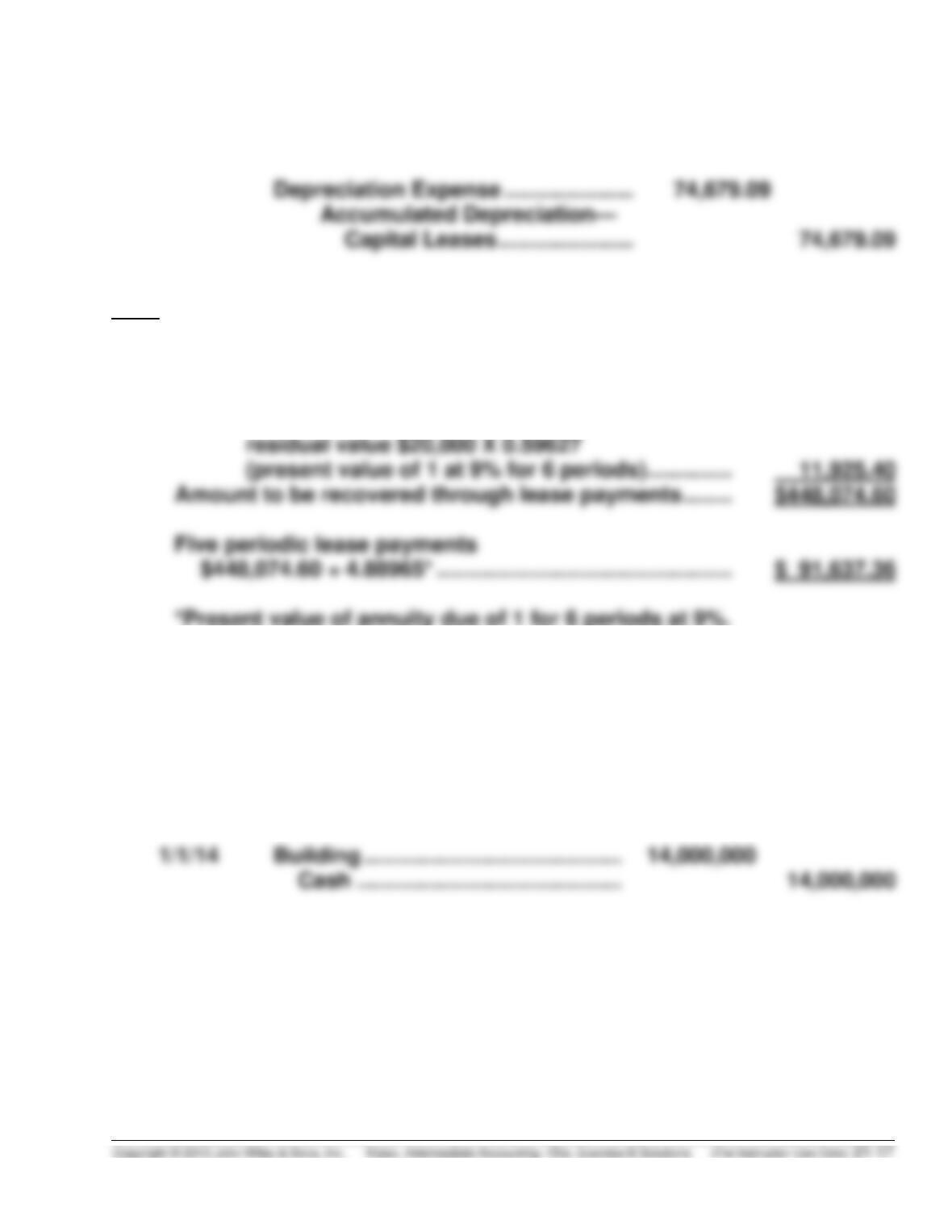

Depreciation Expense ………………… 74,679.09

Accumulated Depreciation—

Capital Leases …………………. 74,679.09

($448,074.52 ÷ 6 = $74,679.09)

E21-11B (Continued)

12/31/15 Interest Expense ………………………… 26,719.12

Interest Payable ………………….. 26,719.12

Note:

1. The lessor sets the annual rental payment as follows:

Fair market value of leased asset to lessor ………………. $460,000.00

Less: Present value of unguaranteed

2. The unguaranteed residual value is not subtracted when depreciating

the leased asset.

E21-12B (10–20 minutes)

(a) Entries for Alphabet Company are as follows:

E21-12B (Continued)

12/31/14 Cash …………………………………………….. 600,000

Rental Revenue ………………………. 600,000

(b) Entries for Numbers, Inc. are as follows:

12/31/14 Rent Expense ……………………………….. 600,000

Cash ……………………………………… 600,000

E21-13B (15–20 minutes)

(a) Annual rental revenue …………………………………………………… $260,000

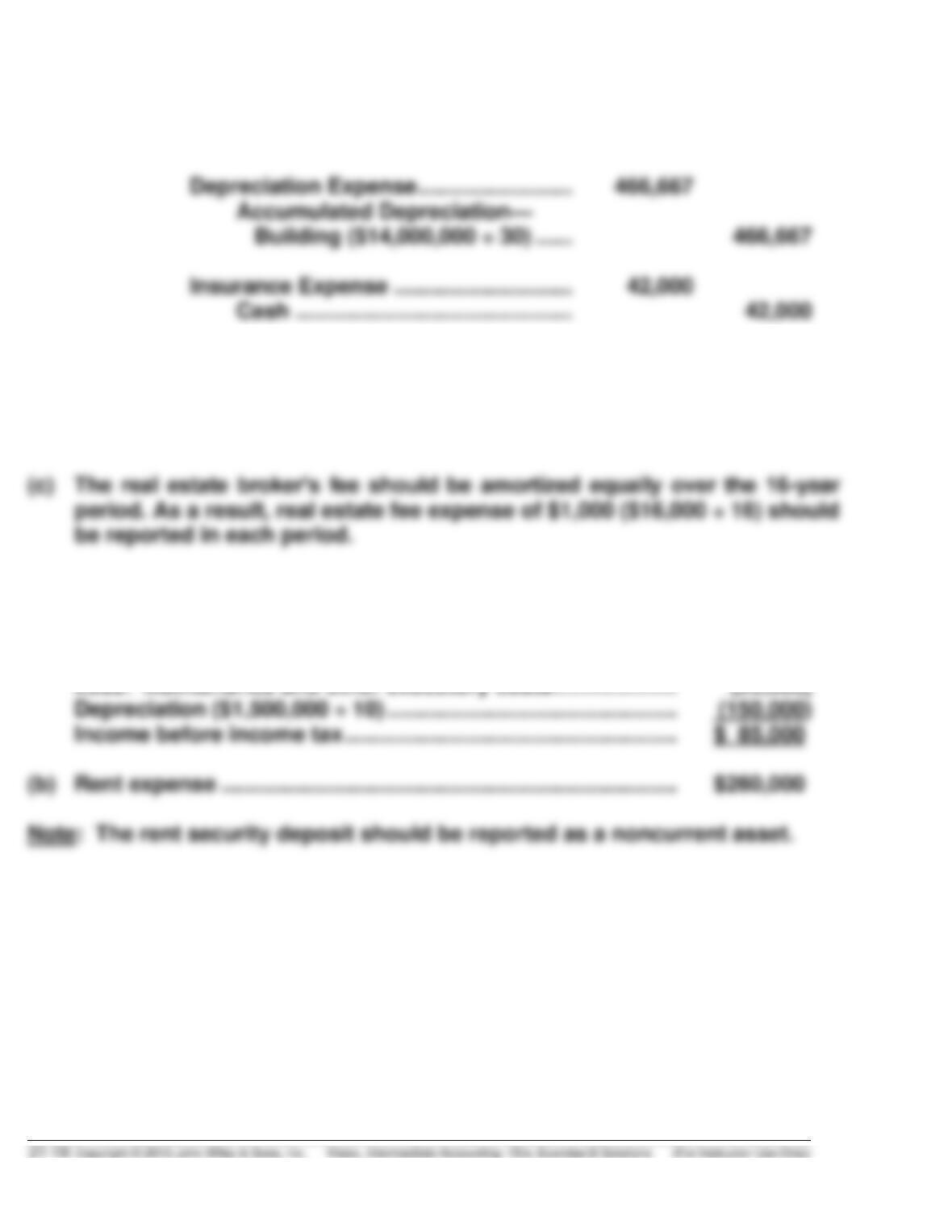

E21-14B (15–20 minutes)

(a) COUPONS FOR EVERYONE, INC.

Rent Expense

For the Year Ended December 31, 2014

$166,667

(b) KINGS FINANCIAL

Income or Loss from Lease before Taxes

For the Year Ended December 31, 2014

Rental revenue ($500,000 X 4/12) …………….. $166,667

Less expense

Depreciation…………………………………….. $153,333**

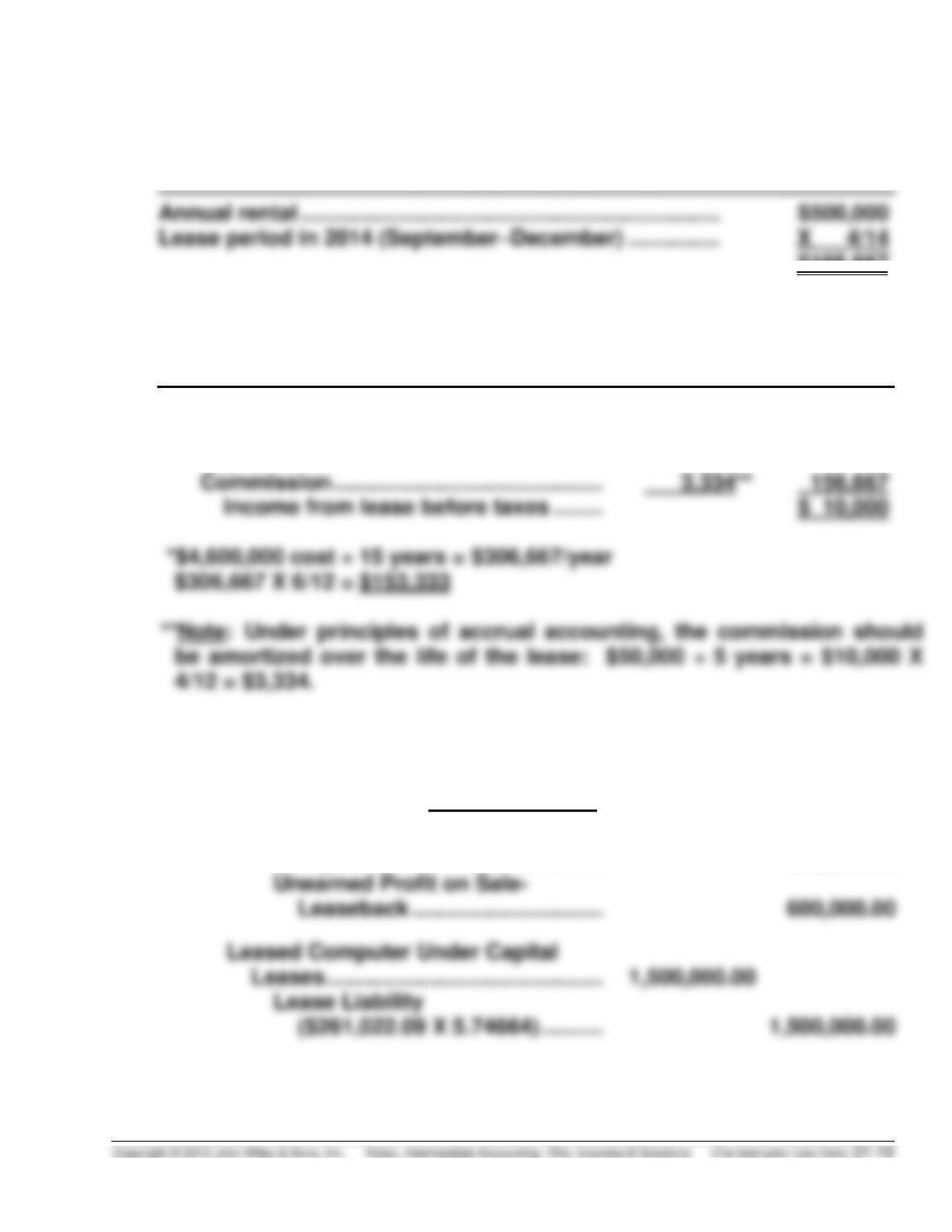

*E21-15B (20–30 minutes)

N-Tech (Lessee)*

1/1/14 Cash ……………………………………………. 1,500,000.00

Computer ……………………………… 900,000.00

*E21-15B (Continued)

Throughout 2014

Executory Costs ………………………….. 15,000.00

Accounts Payable or Cash …….. 15,000.00

12/31/14 Depreciation Expense ………………………. 187,500.00

Accumulated Depreciation

($1,500,000 ÷ 8) ………………….. 187,500.00

**The credit could also be to a revenue account.

Note:

1. The present value of an ordinary annuity at 8% for 8 periods should be

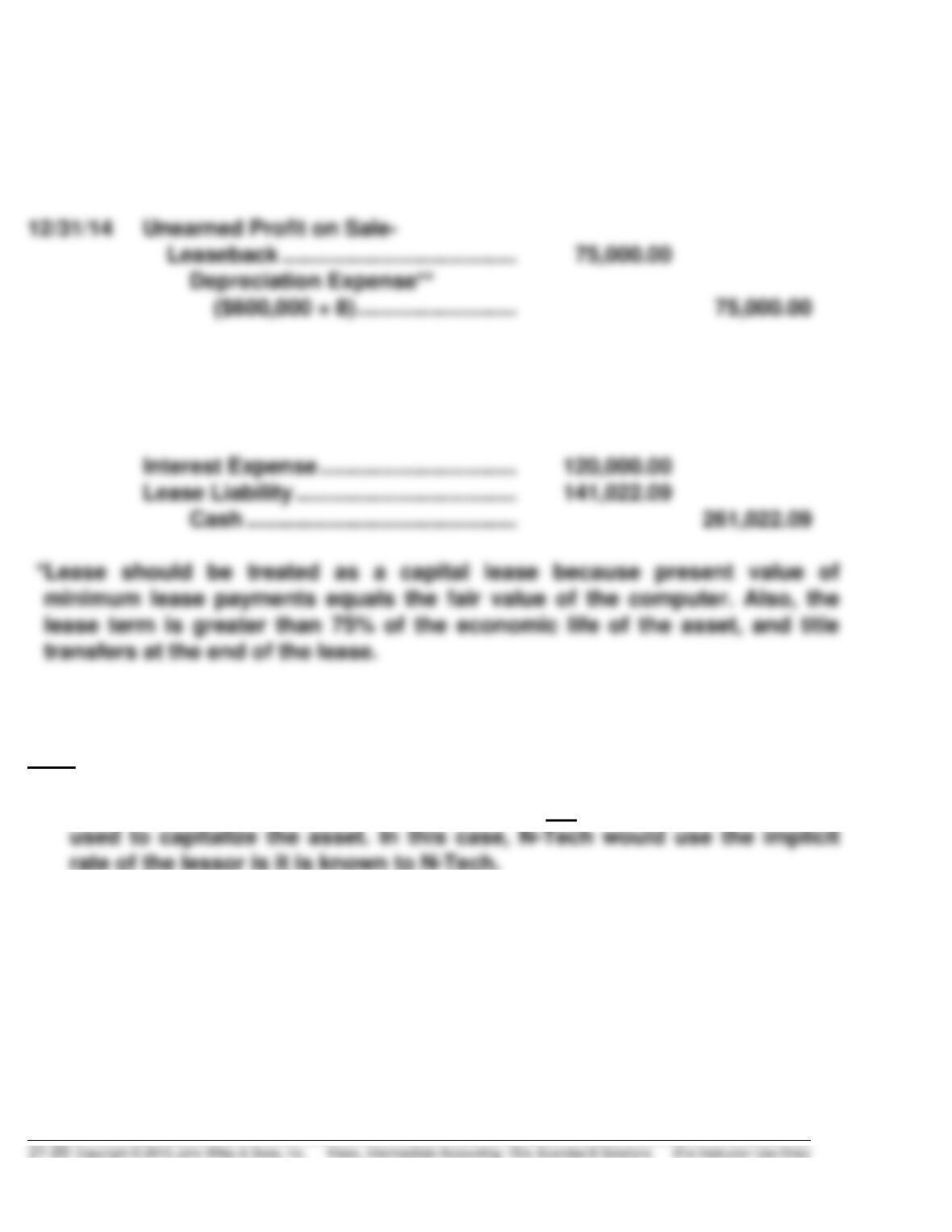

*E21-15B (Continued)

2. The unearned profit on the sale-leaseback should be amortized on the

same basis that the asset is being depreciated.

Partial Lease Amortization Schedule

Date

Annual Lease

Payment

Interest (8%)

Amortization

Balance

1/1/14

$1,500,000.00

12/31/14

$261,022.09

$120,000.00

$141,022.09

1,358,977.91

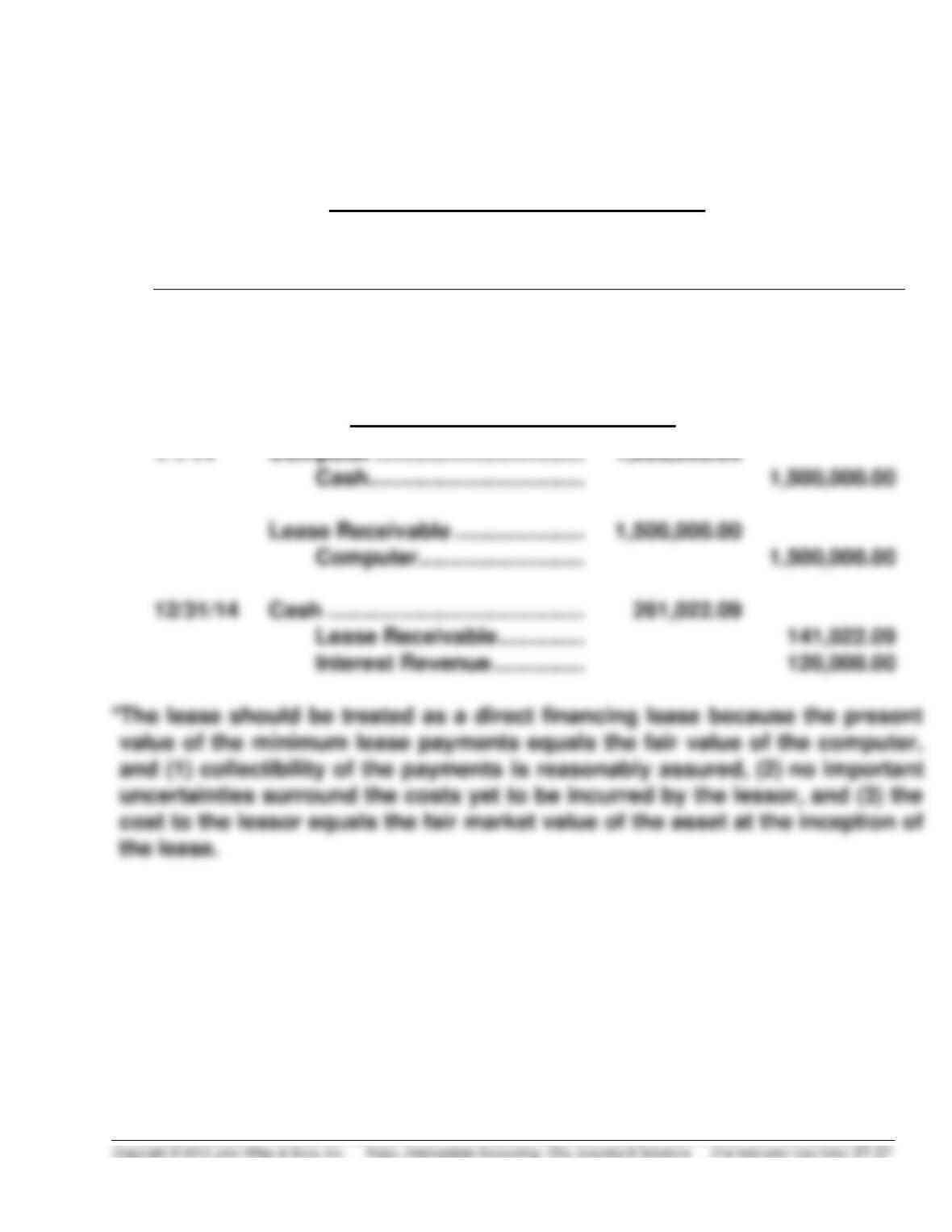

First Tech Leasing Co. (Lessor)*

*E21-16B (20–30 minutes)

(a) Sale-leaseback arrangements are treated as though two transactions

(b) The profit on the sale of $115,000 should be deferred and amortized over

the lease term. Since the leased asset is being depreciated using the

(c) In this case, Olympia would report a loss of $35,000 ($85,000 – $120,000) for

(d) A sale-leaseback is usually treated as a single financing transaction in

which any profit on the sale is deferred and amortized by the seller.

However, GAAP has an exception to this general rule when either only a