FINANCIAL STATEMENT ANALYSIS CASES

CASE 1

(a) Management might purchase treasury stock to provide to stockholders

a tax-efficient method for receiving cash from the corporation. In

addition, it might have to repurchase shares to have them available to

(b) Earnings per share is calculated by dividing net income by the weighted–

average number of shares outstanding during the year.

If shares are reduced by treasury stock purchases, the denominator

(c) One measure of solvency is the ratio of debt divided by total assets.

This ratio shows how many dollars of assets are backing up each dollar

of debt, should the company become financially troubled. For 2011 and

2010, this can be calculated as follows:

2011

2010

FINANCIAL STATEMENT ANALYSIS CASES (Continued)

CASE 2

(a) The date of record marks the time when ownership of the outstanding

shares is determined for dividend purposes. This in turn identifies

(b) The purpose of a stock split is to increase the marketability of the

stock by lowering its market price per share. This may make it easier

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

January 13, 2014

Retained Earnings ($1.05 X 60,000) ………………………….

63,000

Cash ………………………………………………………………

63,000

April 15, 2014

Retained Earnings [(10% X 60,000) X $14] ………………..

84,000

May 15, 2014

Treasury Stock (2,000 X $15) ……………………………………

30,000

Cash ………………………………………………………………

30,000

November 15, 2014

Cash ($18 X 1,000) …………………………………………………..

18,000

Paid-in Capital from Treasury Stock …………………

Treasury Stock ……………………………………………….

15,000

December 31, 2014

Income Summary ……………………………………………………

Retained Earnings …………………………………………..

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

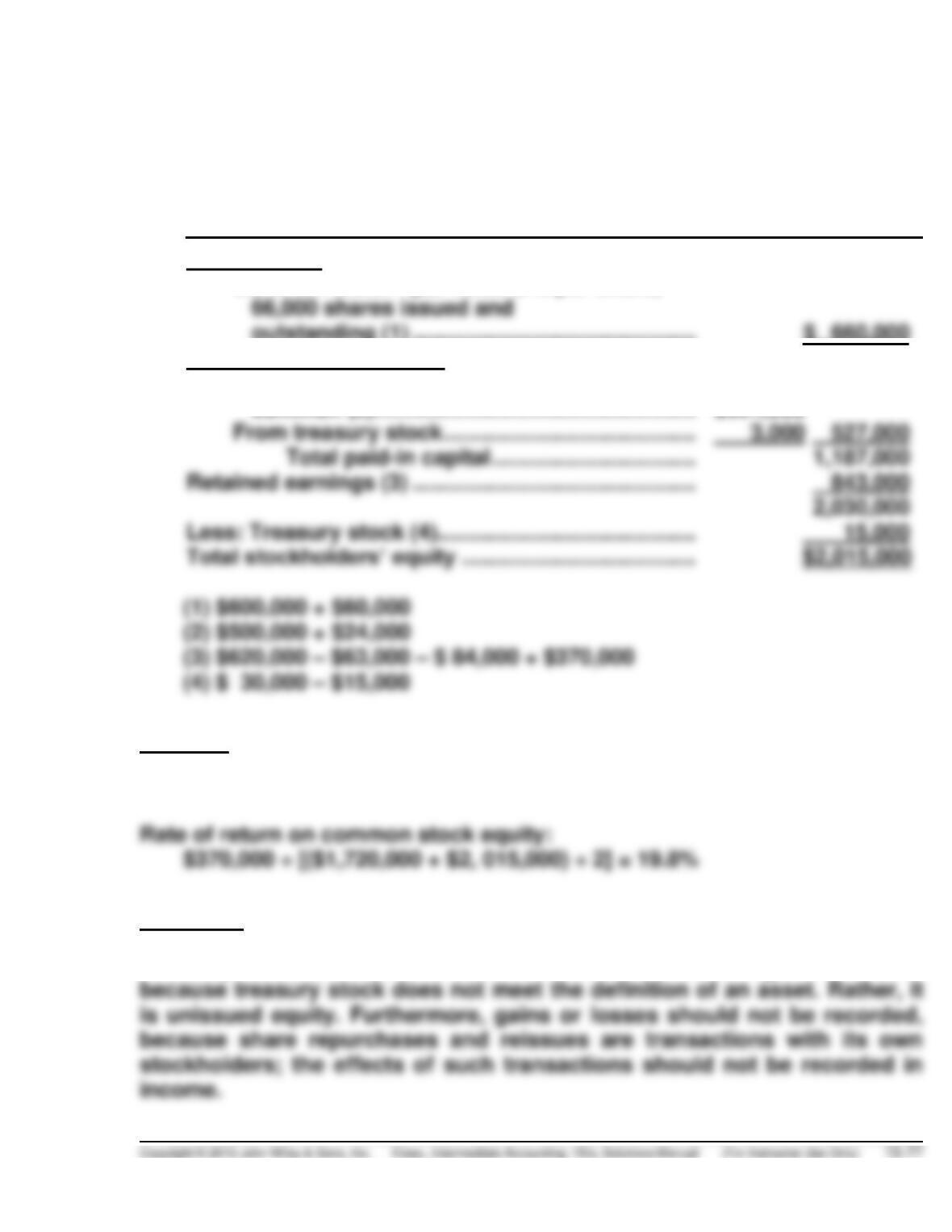

The ending balances are indicated in the following partial balance sheet:

AGASSI CORPORATION

Balance Sheet

December 31, 2014

Capital stock

Common stock—par value $10 per share,

outstanding (1) ………………………………………. $ 660,000

Additional paid-in capital

In excess of par—

common (2) ……………………………………………. $524,000

Analysis

Payout ratio: $63,000 ÷ $ 370,000 = 17%

Principles

Treasury stock sold above or below cost does not result in gains or losses

PROFESSIONAL RESEARCH

(a) See FASB ASC 505-10–50.

(b) (FASB ASC 505-10–20.—Glossary)

1. Security—is defined as evidence of debt or ownership or a related

right. It includes options and warrants as well as debt and stock.

(c) FASB ASC 505-10–50-3. An entity shall explain, in summary form within

its financial statements, the pertinent rights and privileges of the

various securities outstanding. Examples of information that shall be

disclosed are dividend and liquidation preferences, participation rights,

PROFESSIONAL SIMULATION

Note: This assignment is available on the Kieso website.

Explanation

(a) Common stock represents an owner’s claim against a portion of the

total assets of the corporation. As a result, it is a residual interest. It

therefore is part of stockholders’ equity.

(d) The accumulated deficit is larger in the current year because AMR, like

many other major airlines, reported a net loss of $761 million. AMR did

not pay dividends in the current year, which would reduce retained

earnings.

Analysis

IFRS CONCEPTS AND APPLICATION

IFRS15-1

The primary IFRS reporting standards related to stockholders’ equity are

IFRS15-2

Key similarities between IFRS and GAAP for transactions related to

stockholders’ equity pertain to (1) issuance of shares, (2) purchase of

Major differences relate to terminology used, introduction of items such as

revaluation surplus, and presentation of stockholders equity information.

In addition, the accounting for treasury stock retirements differs between

IFRS and GAAP. Under GAAP a company has the option of charging the

IFRS15-3

It is likely that the statement of stockholders’ equity and its presentation

will be examined closely in the financial statement presentation project. In

addition the options of how to present other comprehensive income under

GAAP will change in any converged standard in this area.

IFRS15-4

No, Mary should not make that conclusion. While IFRS allows unrealized

IFRS15-5

Authorized ordinary shares—the total number of shares authorized by the

country of incorporation for issuance.

IFRS15-6

The answers are summarized in the table below:

Account Classification

(a) Share Capital—Ordinary Share capital

(b) Retained Earnings Retained earnings

IFRS15-7

Cash ………………………………………………………………………. 4,500

IFRS15-8

WILCO CORPORATION

Equity

December 31, 2014

Share Capital—Ordinary, $5 par value ………………………. $ 510,000

IFRS15-9

Cash ………………………………………………………………………. 13,500

Share Capital—Preference (100 X $50)……………….. 5,000

Allocated to ordinary

$15,000

$6,000

X $13,500 = $ 5,400

$15,000

$9,000

IFRS15-10

(a) $1,000,000 X 6% = $60,000; $60,000 X 3 = $180,000. The cumulative

dividend is disclosed in a note to the equity section; it is not reported

as a liability.

(b) Share Capital—Preference (3,000 X $100) …….. 300,000

IFRS15–11

TELLER CORPORATION

Partial Statement of Financial Position

December 31, 2014

Equity

Share capital—preference, cumulative,

par value $50 per share; authorized

IFRS15-12

(a) IAS 1 addresses disclosure of information about capital structure.

(b) An entity shall disclose the following, either in the statement of

financial position or the statement of changes in equity, or in the notes:

(a) for each class of share capital:

(i) the number of shares authorised;

(ii) the number of shares issued and fully paid, and issued but

not fully paid;

(b) a description of the nature and purpose of each reserve within

equity (para. 79).

An entity shall present, either in the statement of changes in equity or in

the notes, the amount of dividends recognised as distributions to owners

during the period, and the related amount per share (para. 107).

IFRS15-12 (Continued)

IAS 8 requires retrospective adjustments to effect changes in accounting

policies, to the extent practicable, except when the transition provisions in

another IFRS require otherwise. IAS 8 also requires restatements to correct

IFRS15–13

(a) M&S’s does not have any preference shares.

(b) M&S’s ordinary shares have a par value of 25p per share. Like many

companies, the par value of M&S’s ordinary shares is small relative to

its market value.

(f) Return on ordinary share equity:

2012: £489.6/[£2,790.2 + £2,673.5/2] = 17.9%

(g) Payout ratio: