EXERCISE 15-6 (25–30 minutes)

(a) Cash [(5,000 X $45) – $7,000] ……………………………… 218,000

Common Stock (5,000 X $5) ………………………… 25,000

Paid-in Capital in Excess of Par—

Common Stock …………………………..……………. 193,000

(b) Land (1,000 X $46) …………………………………………….. 46,000

(c) Treasury Stock (500 X $43) ………………………………… 21,500

Cash …………………………..……………………………… 21,500

EXERCISE 15-7 (15–20 minutes)

#

Assets

Liabilities

Stockholders’

Equity

Paid-in

Capital

Retained

Earnings

Net

Income

1

D

NE

NE

NE

3

I

NE

I

D

NE

NE

EXERCISE 15-8 (15–20 minutes)

(a) $1,000,000 X 8% = $80,000; $80,000 X 3 = $240,000. The cumulative

dividend is disclosed in a note to the stockholders’ equity section; it is

not reported as a liability.

(b) Preferred Stock (4,000 X $100)…………………………. 400,000

(c) Paid-in capital

Preferred stock, $100 par 8%, 10,000 shares issued $1,000,000

Paid-in capital in excess of par (10,000 X $7) 70,000

EXERCISE 15-9 (15–20 minutes)

May 2 Cash ……………………………………………………… 192,000

Common Stock (12,000 X $5) …………… 60,000

Paid-in Capital in Excess of Par—

Common Stock (12,000 X $11) ……… 132,000

10 Cash ……………………………………………………… 600,000

15 Treasury Stock ………………………………………. 15,000

Cash ………………………………………………. 15,000

EXERCISE 15-10 (20–25 minutes)

(a) (1) The par value is $2.50. This amount is obtained from either of the

following: 2014—$545 ÷ 218 or 2013—$540 ÷ 216.

(b) Stockholders’ equity (in millions of dollars)

Paid-in capital

Common stock, $2.50 par value, 500,000,000

EXERCISE 15-11 (15–20 minutes)

Item

Assets

Liabilities

Stockholders’

Equity

Paid-in

Capital

Retained

Earnings

Net

Income

1.

I

NE

I

NE

I

I

2.

NE

I

D

NE

D

NE

3.

NE

NE

NE

NE

4.

NE

NE

NE

NE

5.

NE

D

NE

D

6.

NE

NE

7.

NE

I

D

NE

D

8.

NE

NE

D

NE

9.

NE

NE

NE

NE

EXERCISE 15-12 (10–15 minutes)

(a)

6/1

Retained Earnings …………………………..

8,000,000

Dividends Payable …………………………..

8,000,000

6/14

No entry on date of record.

6/30

Dividends Payable …………………………..

8,000,000

Cash ……………………………………………………….

8,000,000

EXERCISE 15-13 (10–15 minutes)

(a) No entry—simply a memorandum note indicating the number of shares

has increased to 18 million and par value has been reduced from

$10 to $5 per share.

(b)

Retained Earnings ($10 X 9,000,000) ………………………..

Common Stock Dividend Distributable ………………..

(c) Stock dividends and splits serve the same function with regard to the

securities markets. Both techniques allow the board of directors to

increase the quantity of shares and reduce share prices into a desired

“trading range.”

EXERCISE 15-14 (10–12 minutes)

(a)

Retained Earnings (15,000 X $37) …………………………..

555,000

Common Stock Dividend Distributable …………………

150,000

Paid-in Capital in Excess of Par—

Common Stock ………………………………………………..

405,000

Common Stock Dividend Distributable …………………….

Common Stock …………………………………………………..

(b)

Retained Earnings (300,000 X $10) …………………………..

Common Stock Dividend Distributable …………………

Common Stock Dividend Distributable …………………….

Common Stock …………………………………………………..

EXERCISE 15-15 (10–15 minutes)

(a)

Retained Earnings ………………………………………………….

97,500

Common Stock Dividend Distributable …………….

25,000

Paid-in Capital in Excess of Par—

Common Stock…………………………………………….

72,500

(50,000 shares X 5% X $39 = $97,500)

Common Stock Dividend Distributable …………………….

Common Stock ………………………………………………

25,000

(b) No entry, memorandum note to indicate that par value is reduced to

$2 and shares outstanding are now 250,000 (50,000 X 5).

(c)

January 5, 2014

Debt Investments ……………………………………………………

35,000

Unrealized Holding Gain or Loss—

Income ……………………………………………………….

35,000

Retained Earnings ………………………………………………….

Property Dividends Payable …………………………..

Property Dividends Payable …………………………..

135,000

Debt Investments ……………………………………………

EXERCISE 15-16 (5–10 minutes)

Total income since incorporation

$317,000

Less: Total cash dividends paid

$60,000

90,000

Current balance of retained earnings

$227,000

EXERCISE 15-17 (20–25 minutes)

BRUNO CORPORATION

Stockholders’ Equity

December 31, 2014

Capital stock

Preferred stock, $4 cumulative, par value $50

per share; authorized 60,000 shares, issued

and outstanding 10,000 shares

$ 500,000

Common stock, par value $1 per share;

authorized 600,000 shares, issued 200,000

shares, and outstanding 190,000 shares

200,000

Total capital stock

Additional paid-in capital—

In excess of par—common

From sale of treasury stock

160,000

Total paid-in capital

Retained earnings

301,000

Total paid-in capital and retained earnings

Less: Treasury stock, 10,000 shares at cost

170,000

EXERCISE 15-18 (30–35 minutes)

(a)

1.

Dividends Payable—Preferred (2,000 X $10) ………………….

20,000

Dividends Payable—Common (20,000 X $2) ………………….

40,000

Cash …………………………..…………………………..

60,000

2.

Treasury Stock ……………………………………………………….

68,000

Cash (1,700 X $40) …………………………………………..

68,000

3.

Land ………………………………………………………………………

30,000

Treasury Stock (700 X $40) …………………………..

28,000

Paid-in Capital From Treasury Stock ………………..

EXERCISE 15-18 (Continued)

4.

Cash (500 X $105) …………………………………………………..

52,500

Preferred Stock (500 X $100) …………………………..

50,000

Paid-in Capital in Excess of Par—

Preferred Stock ……………………………………………

2,500

5.

Retained Earnings (1,900* X $45) …………………………..

85,500

Common Stock Dividend Distributable

(1,900 X $5) ………………………………………………….

9,500

Paid-in Capital in Excess of Par—

Common Stock …………………………………………….

Common Stock Dividend Distributable …………………….

Common Stock ……………………………………………….

9,500

Retained Earnings ………………………………………………….

Dividends Payable—Preferred

(2,500 X $10) ………………………………………………..

25,000

Dividends Payable—Common

(20,900* X $2) ……………………………………………….

41,800

*(19,000 + 1,900)

(b) ANNE CLEVES COMPANY

Stockholders’ Equity

December 31, 2014

Capital stock

Preferred stock, 10%, $100 par, 10,000 shares

authorized, 2,500 shares issued and

outstanding

$250,000

Common stock, $5 par, 100,000 shares

authorized, 21,900 shares issued, 20,900

shares outstanding

Total capital stock

Additional paid-in capital

Total paid-in capital

Retained earnings

EXERCISE 15-18 (Continued)

Total paid-in capital and retained earnings

1,192,700

Less: Cost of treasury stock (1,000 shares common)

40,000

Total stockholders’ equity

$1,152,700

Computations:

Preferred stock $200,000 + $50,000 = $250,000

EXERCISE 15-19 (20–25 minutes)

(a) Mary Ann Benson Company is the more profitable in terms of return

on total assets. This may be shown as follows:

It should be noted that these returns are based on net income related

to total assets, where the ending amount of total assets is con–

sidered representative. If the return on total assets uses net income

before interest but after taxes in the numerator, the rates of return on

total assets are the same as shown below:

=

EXERCISE 15-19 (Continued)

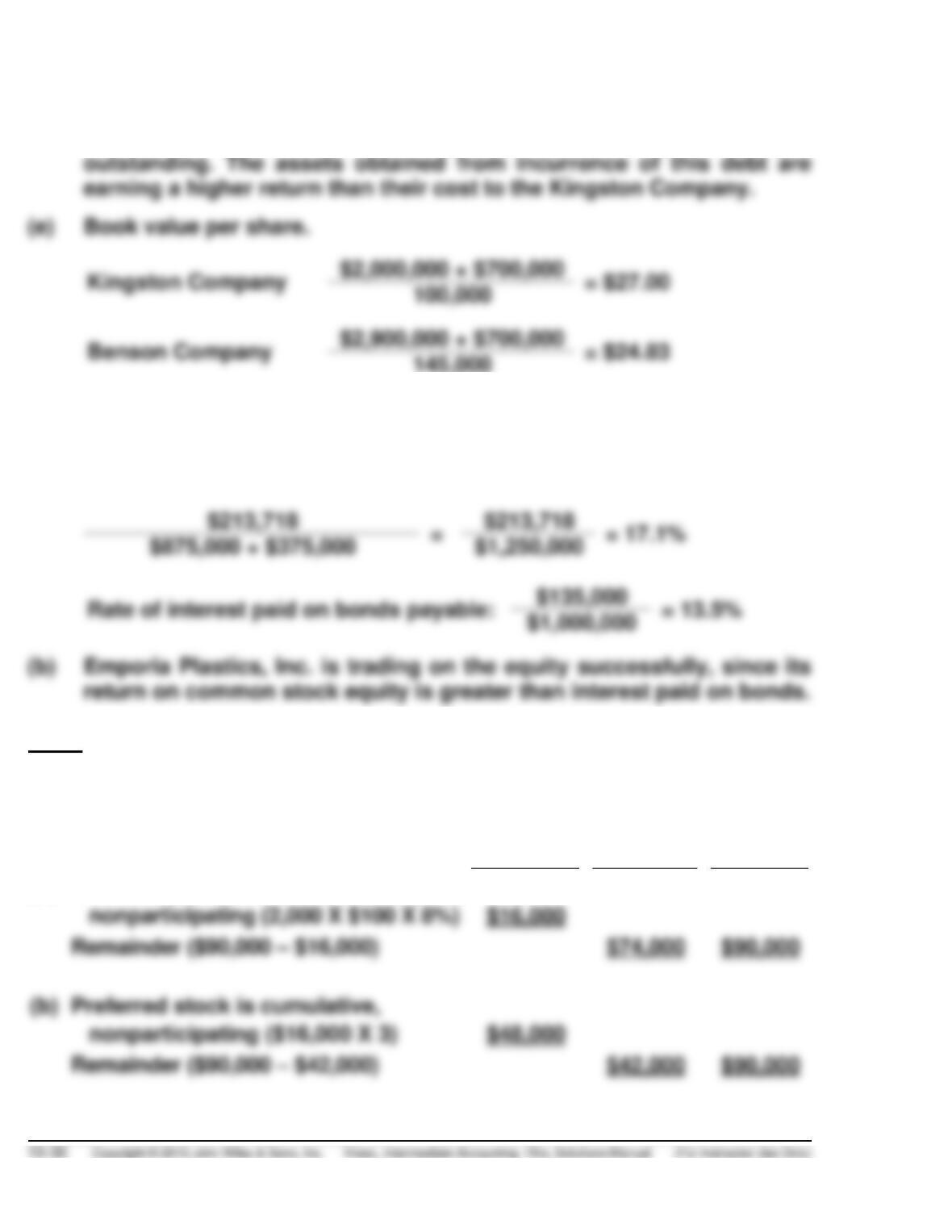

(b) Kingston Company is the more profitable in terms of return on

common stock equity. This may be shown as follows:

provided to the student.)

Kingston Company

Funds Supplied

Funds

Supplied

Rate of Return

on Funds at

15.71%*

Cost of

Funds

Accruing to

Common

Stock

Current liabilities

$ 300,000

$ 47,130

$ 0

$ 47,130

Common stock

The schedule indicates that the income earned on the total assets

(before interest cost) was $659,820. The interest cost (net of tax) of

this income was $66,000, which indicates a net return to the common

equity of $593,820.

(c) The Kingston Company earned a net income per share of $5.94

($594,000 ÷ 100,000) while Benson Company had an income per share

EXERCISE 15-19 (Continued)

(d) Yes, from the point of view of income it is advantageous for the

stockholders of the Kingston Company to have long-term debt

EXERCISE 15-20 (15 minutes)

(a) Rate of return on common stock equity:

Note: Some analysts use after-tax interest expense to compute the bond rate.

*EXERCISE 15-21 (10–15 minutes)

Preferred

Common

Total

(a)

Preferred stock is noncumulative,

(b)

Preferred stock is cumulative,

EXERCISE 15-21 (Continued)

Preferred

Common

Total

(c)

Preferred stock is cumulative,

participating

$57,778

$32,222

$90,000

The computation for these amounts is as follows:

Preferred

Common

Dividends in arrears (2 X $16,000)

$32,000

Current dividend

Pro-rata share to common

(5,000 X $50 X 8%)

Balance dividend pro-rata

9,778

*Additional amount available for participation

($90,000 – $32,000 – $16,000 – $20,000)

22,000

Par value of stock that is to participate

Preferred (2,000 X $100)

Common (5,000 X $50)

Rate of participation

$22,000 ÷ $450,000

4.8889%

Participating dividend

Preferred, 4.8889% X $200,000

Common, 4.8889% X $250,000

Note to instructor: Another way to compute the participating amount is as

follows:

$200,000

$450,000

$250,000

*EXERCISE 15-22 (10–15 minutes)

Preferred

Common

Total

(a)

Preferred stock is cumulative,

fully participating

$36,000

$330,000

$366,000

The computation for these amounts is as follows:

Preferred

$36,000

$330,000

$366,000

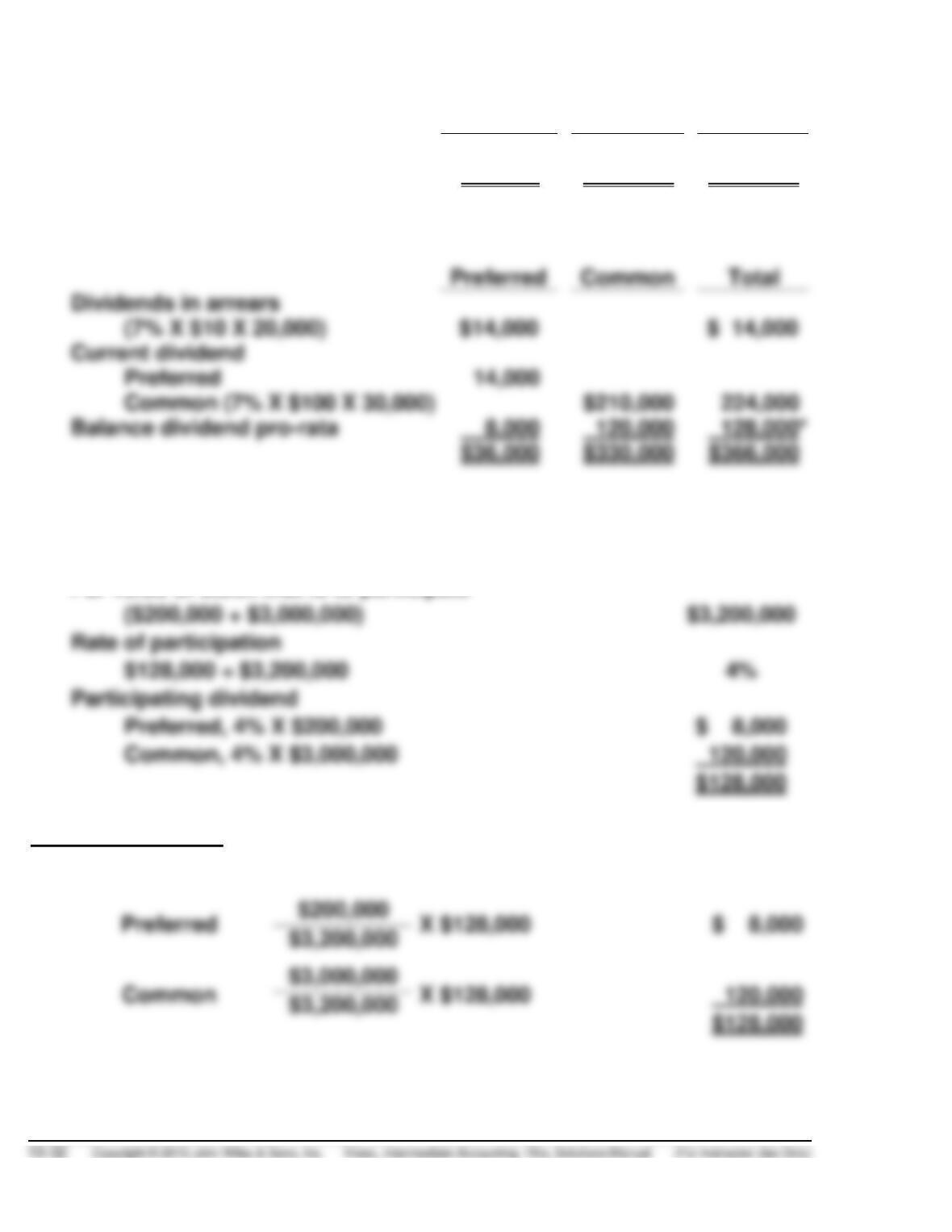

*Additional amount available for participation

($366,000 – $14,000 – $210,000)

$ 128,000

Par value of stock that is to participate

($200,000 + $3,000,000)

$128,000 ÷ $3,200,000

Participating dividend

Preferred, 4% X $200,000

Common, 4% X $3,000,000

Note to instructor: Another way to compute the participating amount is as

follows:

$128,000

*EXERCISE 15-22 (Continued)

Preferred

Common

Total

(b)

Preferred stock is cumulative

and participating

$14,000

$352,000

$366,000

The computation for these amounts is as follows:

Current dividend (preferred)

(7% X $10 X 20,000)

Remainder to common

($366,000 – $14,000)

Preferred

Common

Total

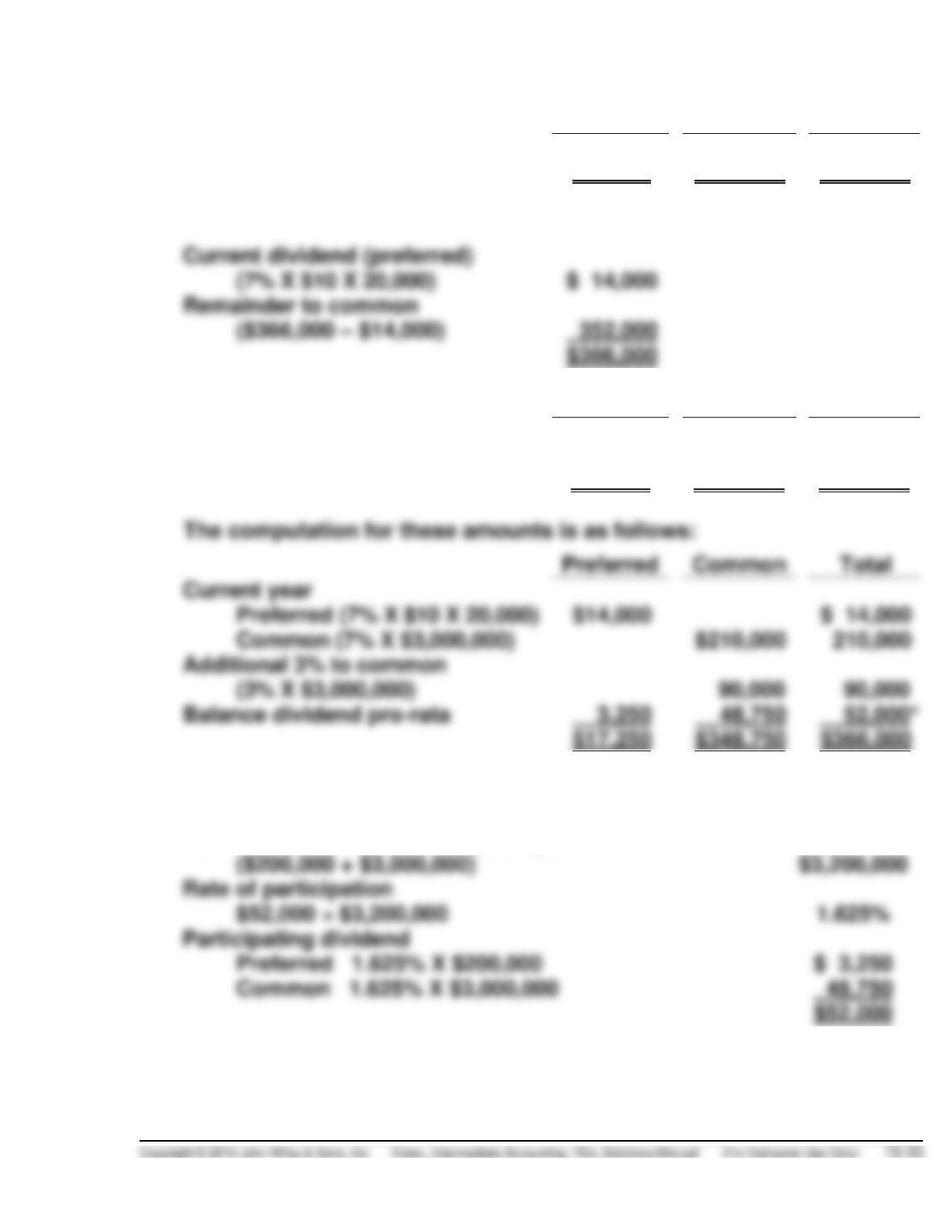

(c)

Preferred stock is noncumulative

and participating in distributions

in excess of 10%

$17,250

$348,750

$366,000

Preferred

Common

Total

Current year

Preferred (7% X $10 X 20,000)

$14,000

$ 14,000

Additional 3% to common

Balance dividend pro-rata

*Additional amount available for participation

($366,000 – $14,000 – $210,000 – $90,000)

$ 52,000

Par value of stock that is to participate

($200,000 + $3,000,000)

Rate of participation

Participating dividend

Preferred 1.625% X $200,000

Common 1.625% X $3,000,000

*EXERCISE 15-23 (10–15 minutes)

Assumptions

(a)

(b)

Preferred, noncumulative

and nonparticipating

Preferred, cumulative

and fully participating

Year

Paid-

out

Preferred

Common

Preferred

Common

2012

$13,000

$5.20

-0-

$ 5.20

-0-

2015

$76,000

$6.00

The computations for part (a) are as follows:

2012

Dividends paid

$13,000

Amount due preferred (2,500 X $100 X 6%)

$15,000

Preferred per share ($13,000 ÷ 2,500)

Common per share

2013

Dividends paid

$26,000

Amount due preferred

15,000

Amount due common

$11,000

Preferred per share ($15,000 ÷ 2,500)

Common per share ($11,000 ÷ 15,000)

2014

Dividends paid

$57,000

Amount due preferred

15,000

Amount due common

$42,000

Preferred per share ($15,000 ÷ 2,500)

Common per share ($42,000 ÷ 15,000)

*EXERCISE 15-23 (Continued)

2015

Dividends paid

$76,000

Amount due preferred

Amount due common

$61,000

Preferred per share ($15,000 ÷ 2,500)

Common per share ($61,000 ÷ 15,000)

The computations for part (b) are as follows:

2012

Dividends paid

$13,000

Amount due preferred (2,500 X $100 X 6%)

$15,000

Preferred per share ($13,000 ÷ 2,500)

Common per share

2013

Dividends paid

$26,000

Amount due preferred

In arrears ($15,000 – $13,000)

2,000

Current

$17,000

Amount due common ($26,000 – $17,000)

$ 9,000

Preferred per share ($17,000 ÷ 2,500)

Common per share ($9,000 ÷ 15,000)

*EXERCISE 15-23 (Continued)

2014

Dividends paid

$57,000

Amount due preferred

Current (2,500 X $100 X 6%)

$15,000

Amount due common

Current (15,000 X $10 X 6%)

$ 9,000

Amount available for participation

($57,000 – $15,000 – $9,000)

Par value of stock that is to participate

($250,000 + $150,000)

Rate of participation

$33,000 ÷ $400,000

8.25%

Participating dividend

Preferred (8.25% X $250,000)

$20,625

Common (8.25% X $150,000)

$12,375

Total amount per share—Preferred

Current $15,000

Participation 20,625

$35,625 ÷ 2,500

Total amount per share—Common

Current $ 9,000

Participation 12,375

$21,375 ÷ 15,000

*EXERCISE 15-23 (Continued)

2015

Dividends paid

$76,000

Amount due preferred

Current (2,500 X $100 X 6%)

$15,000

Amount due common

Current (15,000 X $10 X 6%)

$ 9,000

Amount available for participation

($76,000 – $15,000 – $9,000)

Par value that is to participate

($250,000 + $150,000)

Rate of participation

$52,000 ÷ $400,000

Participating dividend

Preferred (13% X $250,000)

$32,500

Common (13% X $150,000)

$19,500

Total amount per share—Preferred

Current $15,000

Participation 32,500

$47,500 ÷ 2,500

Total amount per share—Common

Current $ 9,000

Participation 19,500

$28,500 ÷ 15,000

*EXERCISE 15-24 (10–15 minutes)

(a)

Common

Preferred

Stockholders’ equity

Preferred stock

$500,000

Common stock

Retained earnings

Dividends in arrears (3 years at 8%)

Remainder to common*

Shares outstanding

750,000

Book value per share ($1,130,000 ÷ 750,000)

$1.51

*Balance in retained earnings

($800,000 – $40,000 – $260,000)

Less: Dividends to preferred

Available to common

(b)

Stockholders’ equity

Preferred stock

$500,000

Common stock

$ 750,000

Retained earnings

Dividends in arrears (3 years at 8%)

$120,000

Remainder to common*

Shares outstanding

750,000

Book value per share ($1,100,000 ÷ 750,000)

$1.47

*Balance in retained earnings

($800,000 – $40,000 – $260,000)

$500,000

Less: Liquidating premium to preferred

Dividends to preferred

Available to common

TIME AND PURPOSE OF PROBLEMS

Problem 15-1 (Time 50–60 minutes)

Purpose—to provide the student with an understanding of the necessary entries to properly account for

Problem 15-2 (Time 25–35 minutes)

Purpose—to provide the student with an opportunity to record the acquisition of treasury stock and its

sale at three different prices. In addition, a stockholders’ equity section of the balance sheet must be

prepared.

Problem 15-3 (Time 25–30 minutes)

Problem 15-4 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of the necessary entries to properly account for

Problem 15-5 (Time 30–40 minutes)

Purpose—to provide the student with an understanding of the proper entries to reflect the reacquisition,

and reissuance of a corporation’s shares of stock. The student is required to record these treasury stock

transactions under the cost method, assuming the FIFO method for purchase and sale purposes.

Problem 15-6 (Time 30–40 minutes)

Purpose—to provide the student with an understanding of the necessary entries to properly account for

Problem 15-7 (Time 15–20 minutes)

Purpose—to provide the student with an understanding of the proper accounting for the declaration and

Problem 15-8 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the accounting effects related to stock divi-

dends and stock splits. The student is required to analyze their effect on total assets, common stock,

paid-in capital, retained earnings, and total stockholders’ equity.

Problem 15-9 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the effect which a series of transactions

Time and Purpose of Problems (Continued)

Problem 15-10 (Time 35–45 minutes)

Purpose—to provide the student with an understanding of the differences between a stock dividend and

a stock split. Acting as a financial advisor to the Board of Directors, the student must report on each

option and make a recommendation.

Problem 15-11 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of the proper accounting for the declaration and

Problem 15-12 (Time 35–45 minutes)

Purpose—to provide the student a comprehensive problem involving all facets of the stockholders’