CHAPTER 4

SOLUTIONS TO B EXERCISES

E4-1B (18–20 minutes)

Computation of net income

Change in assets:

$252,800 + $144,000 + $406,400 – $150,400 = $652,800 Increase

Change in liabilities:

$ 262,400 – $163,200 = 99,200 Increase

Change in stockholders’ equity:

$553,600 Increase

Change in stockholders’ equity accounted

for as follows:

Net increase ………………………………………………….

Increase in common stock ……………………..

Increase in additional paid-in capital ………

dividend declaration …………………………..

(60,800)

Net increase accounted for …………………………….

income ………………………………………………………

E4-2B (25–35 minutes)

Sales revenue …………………………………………………

$536,000

Less:

Cost of goods sold …………………………..……..

$363,000

Selling and administrative expenses ………..

110,500

473,500

(a)

Income form operations

Interest expense ……………………………………..

Loss on sale of investments …………………….

(b)

Net income ……………………………………………………..

Allocation to non-controlling interest ……….

controlling shareholders ………………………………….

E4-3B (25–35 minutes)

(a)

Total net revenue:

Sales ………………………………………………………

$312,000

Less: Sales discounts …………………………….

$ 6,240

Sales returns ………………………………..

9,920

Net sales …………………………………………………

Dividend revenue …………………………………….

Rental revenue ………………………………………..

Total net revenue …………………………….

(b)

Net income:

Total net revenue (from a) ………………………..

$357,840

Expenses:

Cost of goods sold ……………………………..

Selling expenses ………………………………..

79,520

Administrative expenses …………………….

66,000

Interest expense …………………………………

Total expenses ……………………………..

Income before taxes …………………………..……

54,640

Income taxes …………………………..………………

Net income …………………………………………

$ 29,840

(c)

Dividends declared:

Ending retained earnings …………………………

$107,200

Beginning retained earnings …………………….

91,520

Net increase …………………………………………………….

Less: Net income ……………………………………………

(29,840)

Dividends declared ………………………………………….

$ 14,160

(d)

Net income (from b above) ……………………………….

$ 29,840

Allocation to non-controlling interest ………………..

E4-3B (Continued)

ALTERNATE SOLUTION for part (c)

Beginning retained earnings …………………………...

$ 91,520

Add: Net income …………………………………………….

29,840

Deduct: Dividends declared…………………………….

?

Ending retained earnings …………………………………

$107,200

Dividends declared must be $14,160

($121,360 – $107,200)

E4-4B (20–25 minutes)

LEON PAUL INC.

Income Statement

For Year Ended December 31, 2014

Sales …………………………………………………………………………

$2,500,000

Less: Sales discounts ……………………………………………….

34,000

Net sales …………………………………………………………

Cost of goods sold……………………………………………

Selling expenses ………………………………………………

Interest expense ……………………………………………….

40,000

Total expenses …………………………………………

Income taxes ……………………………………………………

127,800

Determination of amounts:

Administrative expenses

=

20% of cost of good sold

=

20% of $1,000,000

=

$200,000

Gross sales X 8%

=

administrative expenses = $200,000

Gross sales

=

$2,500,000

Selling expenses

=

4 times administrative expenses.

(operating expenses consist of selling

and administrative expenses; since

selling expenses are 4/5 of operating

expenses, selling expenses are 4

times administrative expenses.)

=

4 X $200,000

=

$800,000

Per share $14.91 ($298,200 ÷ 20,000)

E4-5B (30–35 minutes)

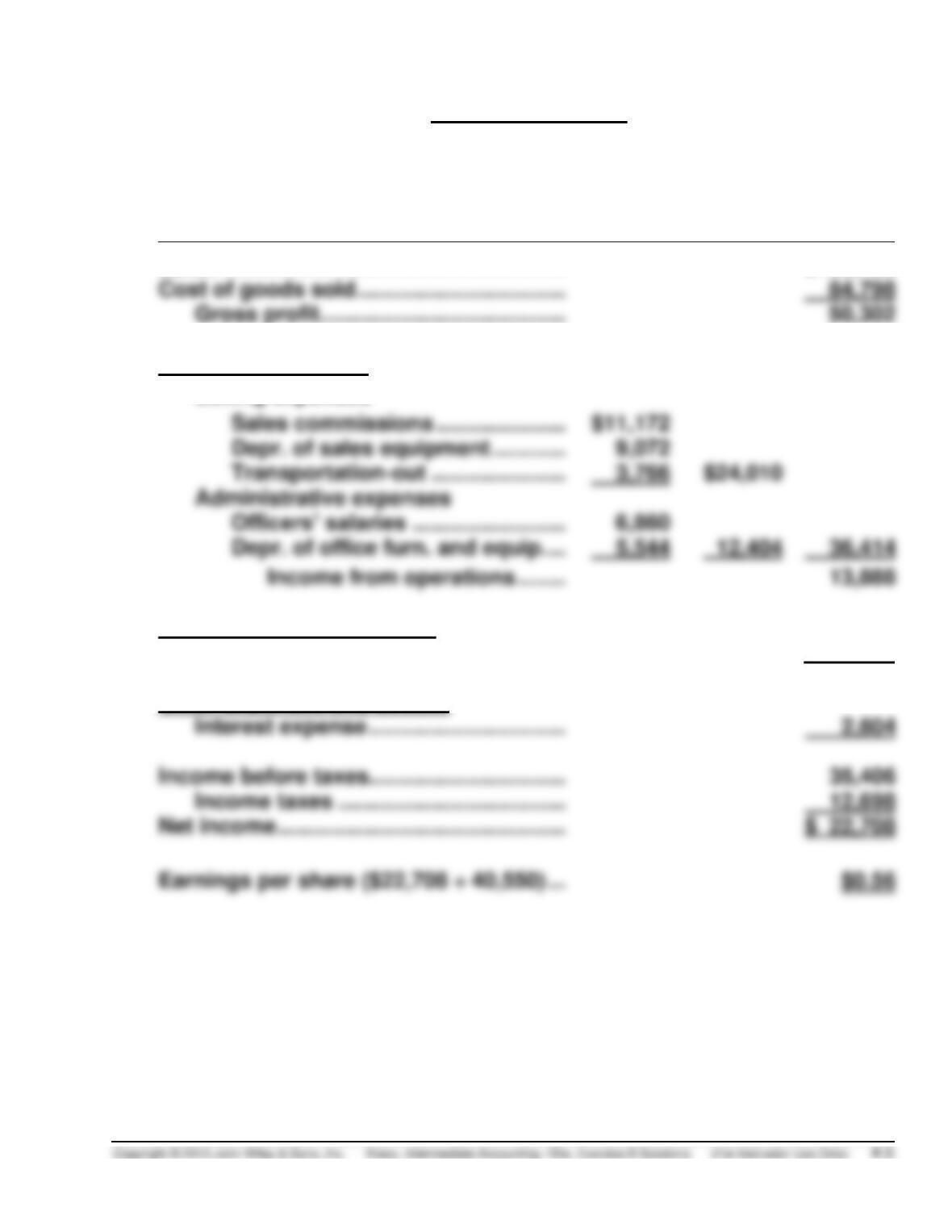

(a) Multiple-Step Form

SAGHIR COMPANY

Income Statement

For the Year Ended December 31, 2014

(In thousands, except earnings per share)

Sales ………………………………………………..

$135,100

Cost of goods sold …………………………….

84,798

Gross profit ………………………………….

Operating Expenses

Selling expenses

Sales commissions …………………

Depr. of sales equipment …………

Transportation-out ………………….

Administrative expenses

Officers’ salaries …………………….

Depr. of office furn. and equip. …

Income from operations ……..

13,888

Other Revenues and Gains

Rental revenue …………………………….

24,122

38,010

Other Expenses and Losses

Interest expense …………………………..

2,604

Income before taxes…………………………..

Income taxes ……………………………….

12,698

Net income ………………………………………..

Earnings per share ($22,708 ÷ 40,550) …

E4-5B (Continued)

(b) Single-Step Form

SAGHIR COMPANY

Income Statement

For the Year Ended December 31, 2014

(In thousands, except earnings per share)

Revenues

Net sales ……………………………………………

Rental revenue …………………………………..

Total revenues………………………………

Expenses

Cost of goods sold …………………………….

84,798

Selling expenses ………………………………..

Administrative expenses …………………….

Interest expense ………………………………..

Total expenses ……………………………..

Income before taxes ………………………………..

35,406

Income taxes …………………………………………..

(c) Single-step:

1. Simplicity and conciseness.

2. Probably better understood by user.

Multiple-step:

1. Provides more information through segregation of operating and

nonoperating items.

2. Expenses are matched with related revenue.

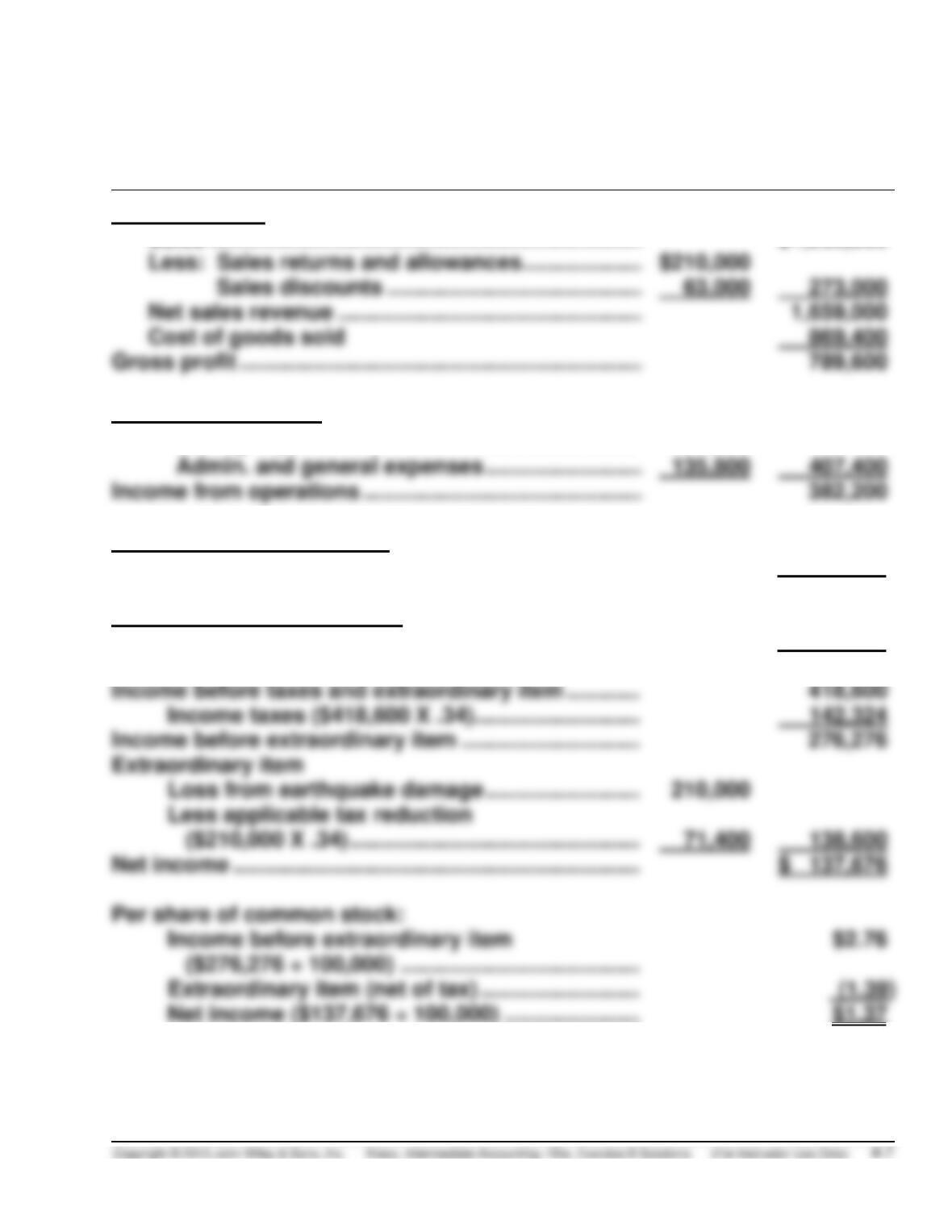

E4-6B (30–35 minutes)

SCHIMANK CORP.

Income Statement

For the Year Ended December 31, 2014

Sales Revenue

Sales ……………………………………………………………..

$1,932,000

Less: Sales returns and allowances ………………..

Net sales revenue …………………………………………..

Cost of goods sold

869,400

789,600

Operating Expenses

Selling expenses ………………………………………..

271,600

Admin. and general expenses ……………………..

407,400

Income from operations ……………………………………….

Other Revenues and Gains

Interest revenue ………………………………………….

120,400

502,600

Other Expenses and Losses

Interest expense …………………………………………

84,000

Income before taxes and extraordinary item …………

Income taxes ($418,600 X .34)………………………

142,324

Income before extraordinary item ………………………..

276,276

Extraordinary item

Loss from earthquake damage …………………….

($210,000 X .34) ………………………………………..

138,600

Net income …………………………………………………………

$ 137,676

Per share of common stock:

($276,276 ÷ 100,000) …………………………………

Extraordinary item (net of tax) ……………………..

E4-7B (30–40 minutes)

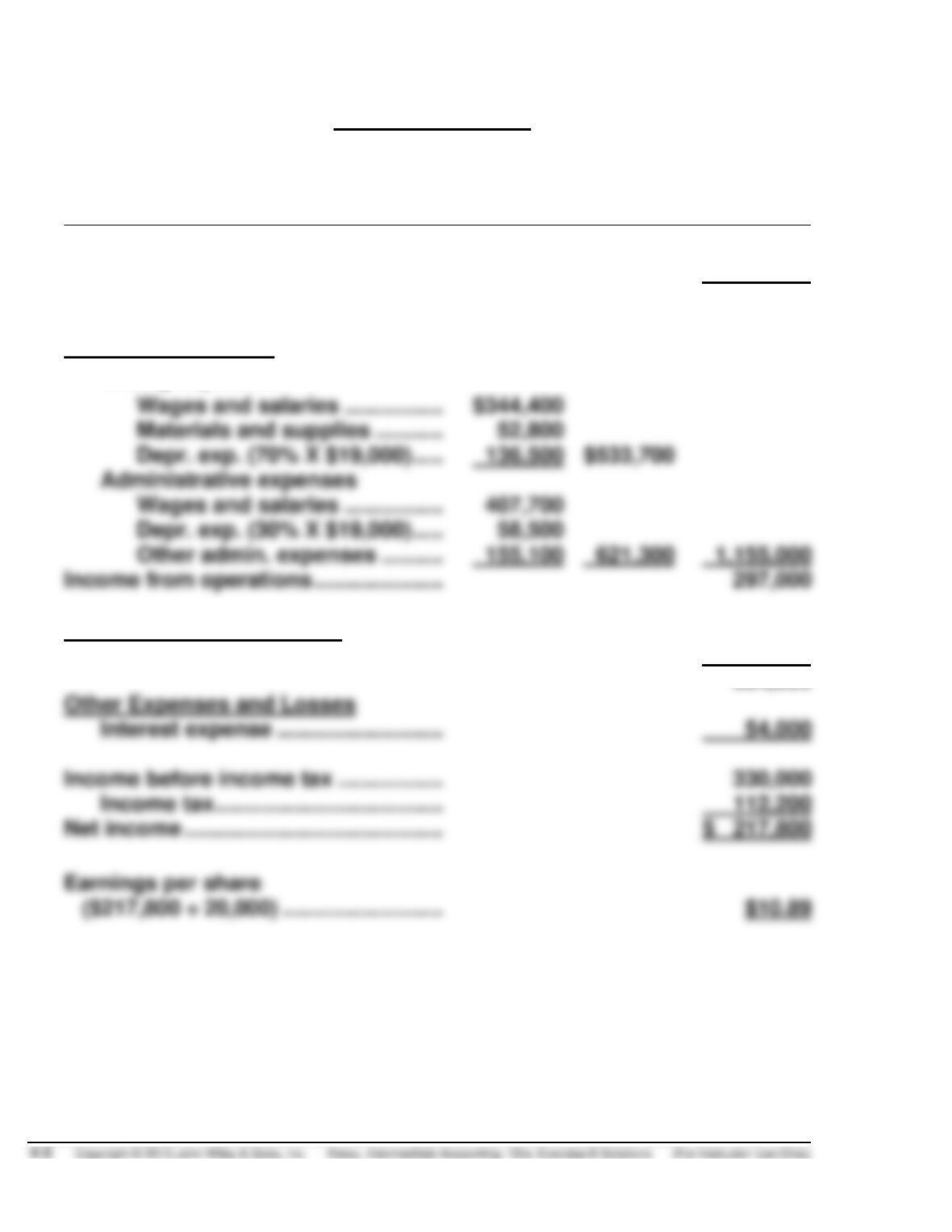

(a) Multiple-Step Form

TABEL SHOE CO.

Income Statement

For the Year Ended December 31, 2014

Net sales ……………………………………….

$2,940,000

Cost of goods sold ………………………..

1,488,000

Gross profit …………………………………..

1,452,000

Operating Expenses

Selling expenses

Wages and salaries …………….

Materials and supplies ………..

Depr. exp. (70% X $19,000) …..

Administrative expenses

Wages and salaries …………….

Depr. exp. (30% X $19,000) …..

Other admin. expenses ……….

1,155,000

Income from operations …………………

Other Revenues and Gains

Rental revenue …………………………

87,000

384,000

Other Expenses and Losses

Interest expense ………………………

54,000

Income before income tax ……………..

Income tax ……………………………….

112,200

E4-7B (Continued)

(b) Single-Step Form

TABEL SHOE CO.

Income Statement

For the Year Ended December 31, 2014

Revenues

Net sales …………………………………………….

$2,940,000

Rental revenue ……………………………………

87,000

Total revenues ……………………………….

3,027,000

Expenses

Cost of goods sold ……………………………..

Selling expenses …………………………………

Administrative expenses ……………………..

621,300

Interest expense …………………………………

54,000

Total expenses ………………………………

Income before taxes …………………………………

330,000

Income taxes ………………………………………

112,200

Net income ………………………………………………

$ 217,800

(c)

Single-step:

1. Simplicity and conciseness.

2. Probably better understood by user.

3. Emphasis on total costs and expenses and net income.

4. Does not imply priority of one expense over another.

Multiple-step:

1. Provides more information through segregation of operating and

nonoperating items.

2. Expenses are matched with related revenue.

E4-8B (15–20 minutes)

(a) Net sales …………………………..………………………………………… $1,350,000

Less: Cost of goods sold …………………………………………….. (525,000)

(b) Income from continuing operations before income tax ….. $375,000*

Income tax ($375,000 X .30) ……………………………………….. 112,500

Earnings per share:

Income from continuing operations

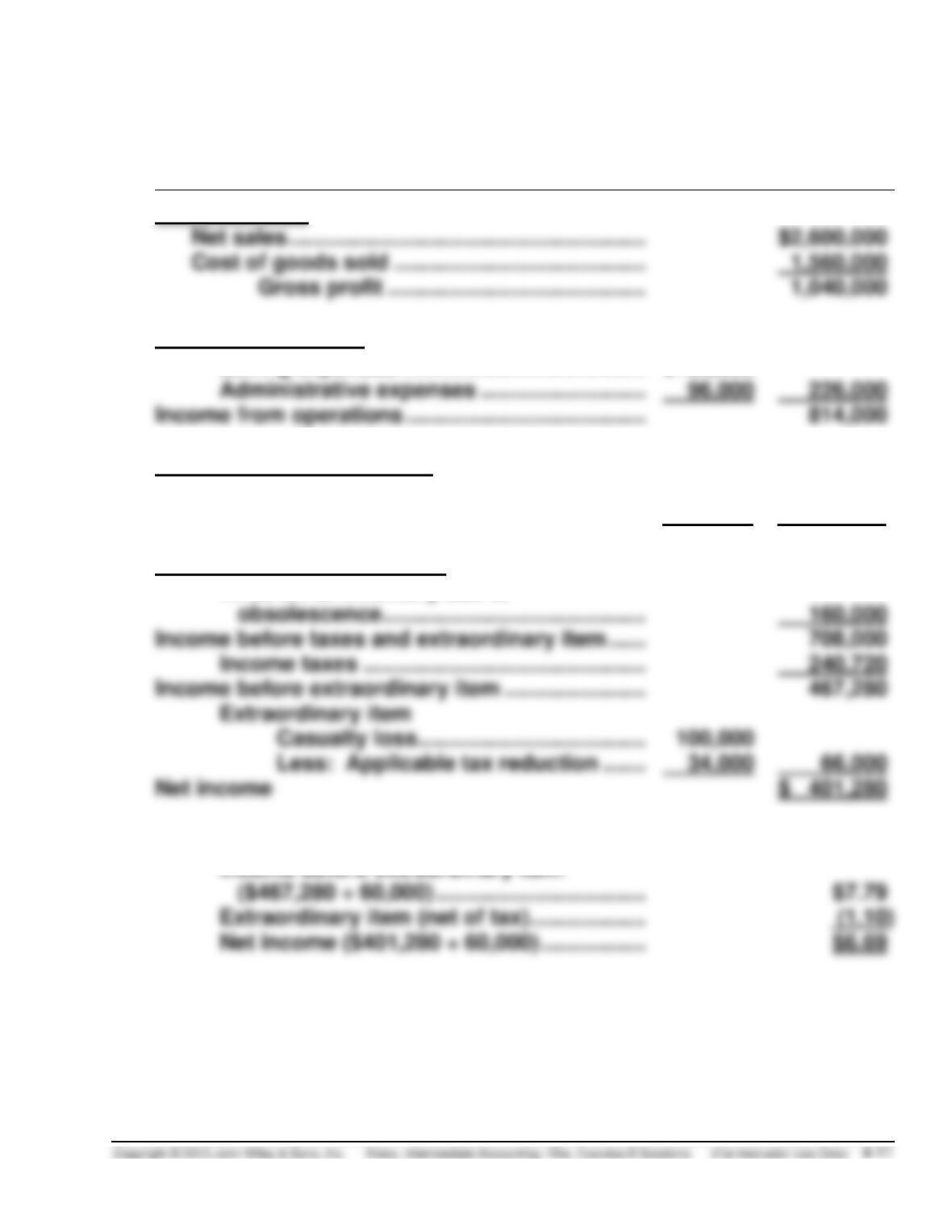

E4-9B (30–35 minutes)

(a) TRIEU CORP.

Income Statement

For the Year Ended December 31, 2014

Sales Revenue

Net sales ………………………………………………….

$2,600,000

Cost of goods sold …………………………………..

Gross profit ……………………………………

Operating Expenses

Selling expenses ………………………………….

$130,000

Administrative expenses ………………………

Income from operations …………………………………

Other Revenues and Gains

Dividend revenue …………………………………

40,000

Interest revenue ……………………………………

14,000

54,000

868,000

Other Expenses and Losses

obsolescence…………………………………….

Income taxes ……………………………………….

240,720

Income before extraordinary item …………………..

467,280

Extraordinary item

Casualty loss …………………………..…..

Less: Applicable tax reduction …….

Write-off of inventory due to

Per share of common stock:

($467,280 ÷ 60,000) …………………………….

Extraordinary item (net of tax) ……………….

E4-9B (Continued)

(b) TRIEU CORP.

Retained Earnings Statement

For the Year Ended December 31, 2014

Balance, Jan. 1, as reported ……………………………………………………..

$1,960,000

Correction for overstatement of net income in prior period

E4-10B (20–25 minutes)

Computation of net income:

2014 net income after tax ………………………….

$ 6,600,000

2014 net income before tax

Add back: Major casualty loss ………………….

3,600,000

Income from operations ……………………… ……………………….

Income before extraordinary item ……………..

Extraordinary item:

Less: Applicable income tax reduction …

2,376,000

Net income ……………………………………………………

$ 6,600,000

Less: Provision for preferred dividends

Income available for common …………………..

E4-10B (Continued)

Income statement presentation

Per share of common stock:

E4-11B (20–25 minutes)

Vu CORPORATION

Income Statement

For the Year Ended December 31, 2014

Net sales …………………………………………………………

$2,081,000

Cost of goods sold ………………………………………….

1,332,500

Gross profit ……………………………………………….

748,500

Selling expenses ……………………………………………..

$318,000

Administrative expenses ………………………………….

563,500

Income from operations ……………………………..

185,000

Other revenue …………………………………………………

Other expense …………………………………………………

32,000

Income before taxes

217,000

Income taxes ($217,000 X .34) ……………………..

Income before extraordinary item …………………….

Extraordinary loss, net of $11,900 taxes ……………

Earnings per share ($450,000 ÷ $10 par value = 45,000 shares)

Income before extraordinary item ($143,220 ÷ 45,000) ….

$3.18

E4-11B (Continued)

Supporting computations:

Net sales:

Cost of goods sold:

Selling expenses:

Administrative expenses:

E4-12B (20–25 minutes)

(a) JASON WOO CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2014

Balance, January 1, as reported …………………………….

$ 900,000*

Cumulative effect of change in inventory methods

(net of $56,000 tax) …………………………..………………..

(84,000)

Add: Net income ………………………………………………….

E4-12B (Continued)

(b) Total retained earnings would still be reported as $932,000. A restriction

does not affect total retained earnings; it merely labels part of the retained

E4-13B (15–20 minutes)

Net income:

Income from continuing operations

before income tax ……………………………………………………….….

$61,500,000

Income tax (40% X $161,500,000) …………………………………………

Income from continuing operations …………………………………….

Discontinued operations

Gain before income tax …………………………………………………

Less: Applicable income tax (40%) ………………………………..

3,900,000

Net income ………………………………………………………………………..

Preferred dividends declared: ………………………………………………….

$ 2,020,000

Weighted average common shares

outstanding …………………………………………………………………………

4,000,000

Earnings per share

Income from continuing operations …………………………………….

Discontinued operations, net of tax …………………………………….

Net income ………………………………………………………………………..

Retained earnings:

Appropriated ………………………………………………….

Unappropriated ………………………………………………

E4-14B (15–20 minutes)

(a) Depreciation expense for 2014

E4-15B (15–20 minutes)

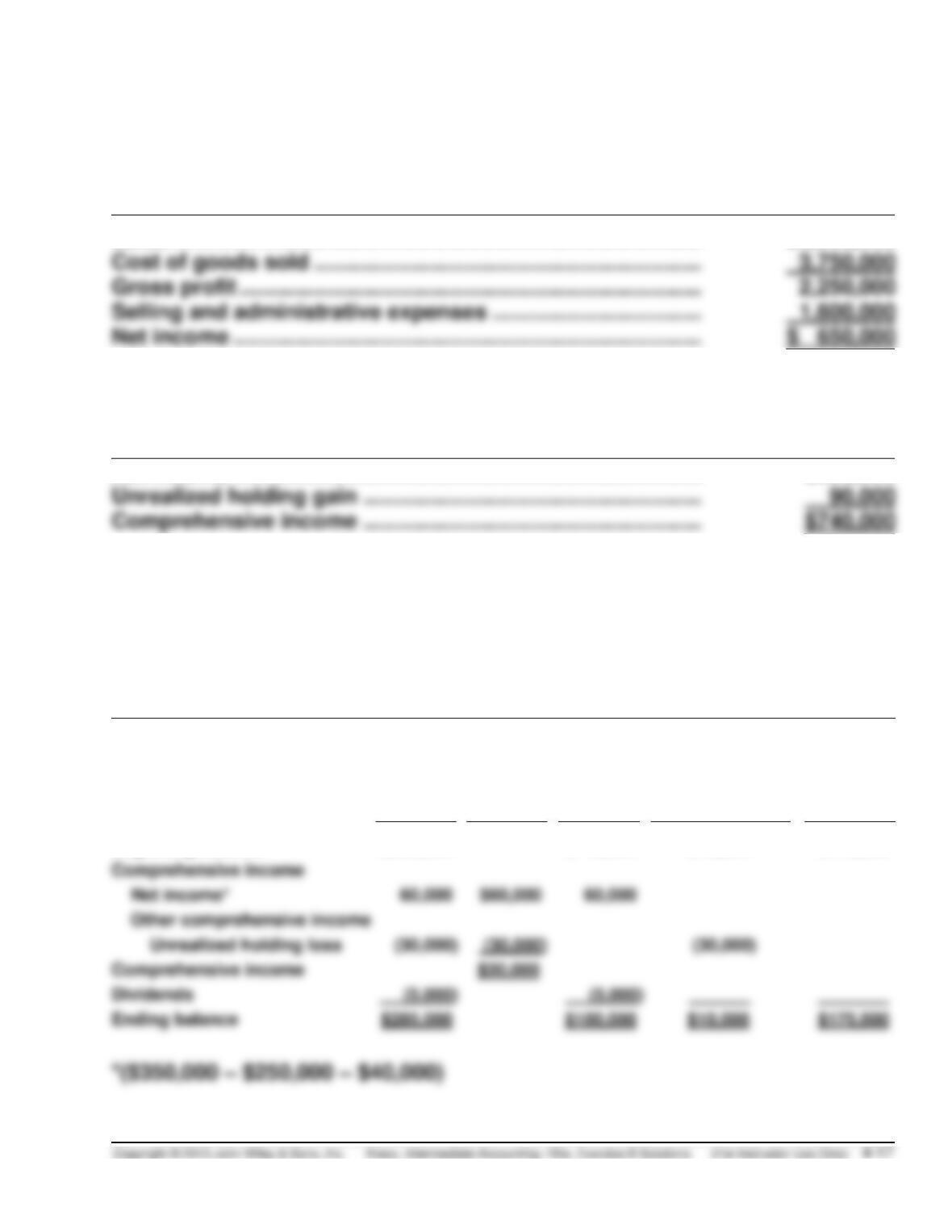

(a)

ARI CORPORATION

Income Statement and Statement of Comprehensive Income

For the Year Ended December 31, 2014

Sales ……………………………………………………………………………

$6,000,000

Cost of goods sold …………………………..…………………………..

3,750,000

Net income ……………………………………………………….………….

$ 650,000

Unrealized holding gain ………………………………………………..

E4-15B (Continued)

(b)

ARI CORPORATION

Income Statement

For the Year Ended December 31, 2014

Sales …………………………………………………………………………..

$6,000,000

Selling and administrative expenses …………………………….

ARI CORPORATION

Statement of Comprehensive Income

For the Year Ended December 31, 2014

Net income ………………………………………………………………….

$650,000

E4-16B (15–20 minutes)

CALVO CO.

Statement of Stockholders’ Equity

For the Year Ended December 31, 2014

Total

Compre-

hensive

Income

Retained

Earnings

Accumulated

Other

Comprehensive

Income

Common

Stock

Beginning balance

$260,000

$ 45,000

$40,000

$175,000

E4-17B (30–35 minutes)

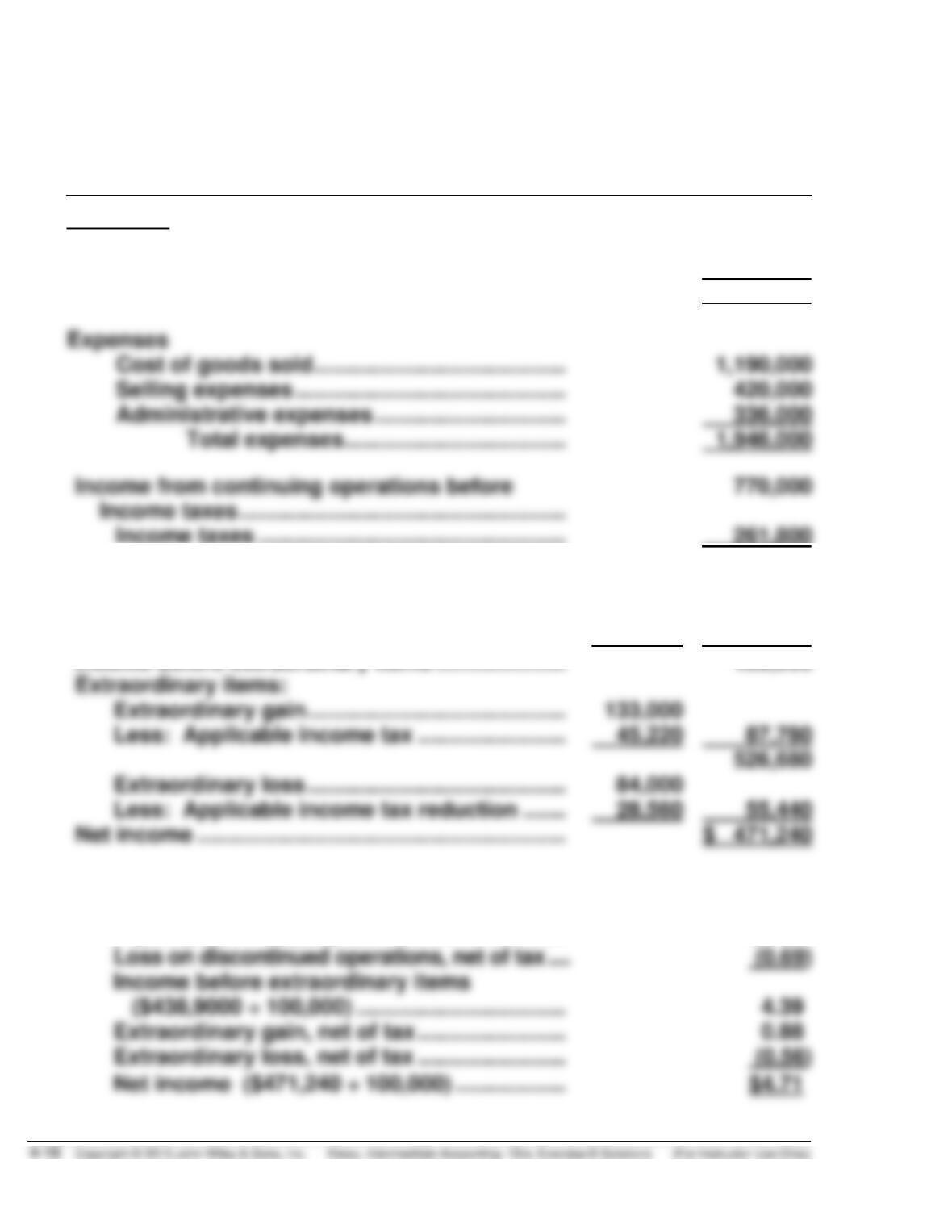

(a) CANTU INC.

Income Statement

For the Year Ended December 31, 2014

Revenues

Sales ……………………………………………………………..

$2,660,000

Rent revenue ………………………………………………….

56,000

Total revenues …………………………………………

2,716,000

Expenses

Cost of goods sold …………………………………..

Selling expenses ……………………………………..

420,000

Administrative expenses ………………………….

336,000

Total expenses ………………………………

Income taxes ……………………………………………..

Income taxes …………………………………………..

261,800

Income from continuing operations ………………..

508,200

Discontinued operations

Loss on discontinued operations ……………..

$105,000

Less: Applicable income tax reduction …….

35,700

69,300

Income before extraordinary items …………………

438,900

Extraordinary items:

Extraordinary gain ……………………………………

Less: Applicable income tax ……………………

45,220

87,780

Extraordinary loss ……………………………………

Less: Applicable income tax reduction …….

28,560

55,440

Per share of common stock:

Income from continuing operations

($508,200 ÷ 100,000) ………………………………

$5.08

Loss on discontinued operations, net of tax ….

Income before extraordinary items

($438,9000 ÷ 100,000) …………………………....

Extraordinary gain, net of tax ……………………

Extraordinary loss, net of tax ……………………

E4-17B (Continued)

(b) CANTU INC.

Statement of Comprehensive Income

For the Year Ended December 31, 2014

Net income …………………………………………………….

$471,240

Other comprehensive income

Unrealized holding gain ……………………………..

(c) CANTU INC.

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1, 2014 ………………….

$ 840,000

2014 Net income ……………………………………………..

471,240

Dividends declared …………………………………………

Retained earnings, December 31, 2014 …………….

$1,101,240