PROBLEM 7-10B

(a) PAWNS INC.

Long-Term Receivables Section of Balance Sheet

December 31, 2014

8% note receivable from sale of division, due

in annual installments of $1,000,000 to

July 1, 2018, less current installment……………..

$ 3,000,000

(1)

6% note receivable from officer, due Oct. 31,

2017, collateralized by 20,000 shares

of Pawns, Inc., common stock

with a fair value of $820,000 ………………………….

Zero-interest-bearing note from sale of patent,

net of 14% imputed interest, due

April 1,2017 ………………………………………………….

(2)

Installment contract receivable, due in annual

installments of $45,125 to July 1, 2016,

less current installment ………………………………..

(3)

Total long-term receivables ………………………..

$3,912,613

(b) PAWNS INC.

Selected Balance Sheet Balances

December 31, 2014

Current portion of long-term receivables:

Note receivable from sale of division ………………………..

$1,000,000

(1)

Installment contract receivable …………………………..

(3)

Accrued interest receivable:

Note receivable from sale of division ………………………..

(4)

Installment contract receivable …………………………..

Total accrued interest receivable …………………………

PROBLEM 7-10B (Continued)

(c) PAWNS INC.

Interest Revenue from Long-Term Receivables

For the Year Ended December 31, 2014

Interest income:

Note receivable from sale of division …………………………

$360,000

(6)

Note receivable from sale of patent …………………………..

(2)

Note receivable from officer ………………………………………

(7)

Installment contract receivable from sale of land ………..

(5)

Total interest income for year ended 12/31/2014 …….

$426,719

Explanation of Amounts

(1)

Long-term Portion of 8% Note Receivable at 12/31/2014

Face amount, 12/31/2013 ………………………………….

$5,000,000

Less: Installment received 7/1/2014 …………………

Balance, 12/31/2014 …………………………………………

Less: Installment due 7/1/2015 ………………………..

Long-term portion, 12/31/2014 ………………………….

$3,000,000

(2)

Zero-interest-bearing Note, Net of Imputed Interest

at 12/31/2014

Face amount 4/1/2014………………………………………

$ 250,000

Less: Imputed interest

Balance, 4/1/2014 …………………………………………….

Add: Interest earned to 12/31/2014

Balance, 12/31/2014 …………………………………………

PROBLEM 7-10B (Continued)

(3)

Long-term Portion of Installment Contract

Receivable at 12/31/2014

Contract selling price, 3/1/2014 ………………………..

Less: Down payment, 3/1/2014 ……………………….

Balance, 12/31/2014 ………………………………………..

Less: Installment due, 3/1/2015

Long-term portion, 12/31/2014 …………………………

$ 94,144

(4)

Accrued Interest—Note Receivable, Sale of

Division at 12/31/2014

Interest accrued from 7/1 to 12/31/2014

($4,000,000 X 8% X 6/12) ……………………………….

$ 160,000

(5)

Accrued Interest—Installment Contract at 12/31/2014

Interest accrued from 3/1 to 12/31/2014

($120,000 X 10% X 10/12) ………………………………

$ 10,000

(6)

Interest Revenue—Note Receivable, Sale of

Division, for 2014

Interest earned from 1/1 to 7/1/2014

($5.000,000 X 8% X 6/12) ……………………………….

Interest earned from 7/1 to 12/31/2014

($4,000,000 X 8% X 6/12) ……………………………….

Interest income ………………………………………………

$ 360,000

(7)

Interest Revenue—Note Receivable, Officer, for 2014

Interest earned 1/1 to 12/31/2014

($650,000 X 6%) ……………………………………………

$ 39,000

PROBLEM 7-11B

EDK COMPANY

Income Statement Effects

For the Year Ended December 31, 2014

Expenses resulting from accounts receivable

Schedule 1

Computation of Expense

for Accounts Receivable Assigned

Assignment expense:

*PROBLEM 7-12B

(a)

Petty Cash ……………………………………………………….

300.00

Cash …………………………..……………………………..

300.00

Postage Expense ……………………………………………….

61.50

Supplies …………………………………………………………….

31.00

Accounts Receivable (Employees) ………………………

25.00

Freight Out ……………………………………………………….

79.36

Advertising Expense …………………………………………..

38.00

Misc. Expense …………………………..……………………….

12.80

Cash ($300.00 – $52.34) ………………………………

247.66

Petty Cash ……………………………………………………….

100.00

Cash …………………………..……………………………..

(b)

Balances per bank: …………………………..………………..

$12,302

Add:

Cash on hand …………………………………………….

$ 425

Deposit in transit ………………………………………..

1,560

1,985

14,287

Deduct: Checks outstanding ……………………………….

1,800

Balance per books: …………………………………………….

Add: Note receivable (collected with interest) ……..

Deduct: Bank Service Charges …………………………..

20

*($12,172 + $36,200 – $37,450)

Cash …………………………..……………………………………..

1,585

Notes Receivable ……………………………………….

1,540

Interest Revenue ………………………………………..

45

Office Expense (Bank Charges) …………………………..

Cash …………………………..……………………………..

20

*PROBLEM 7-13B

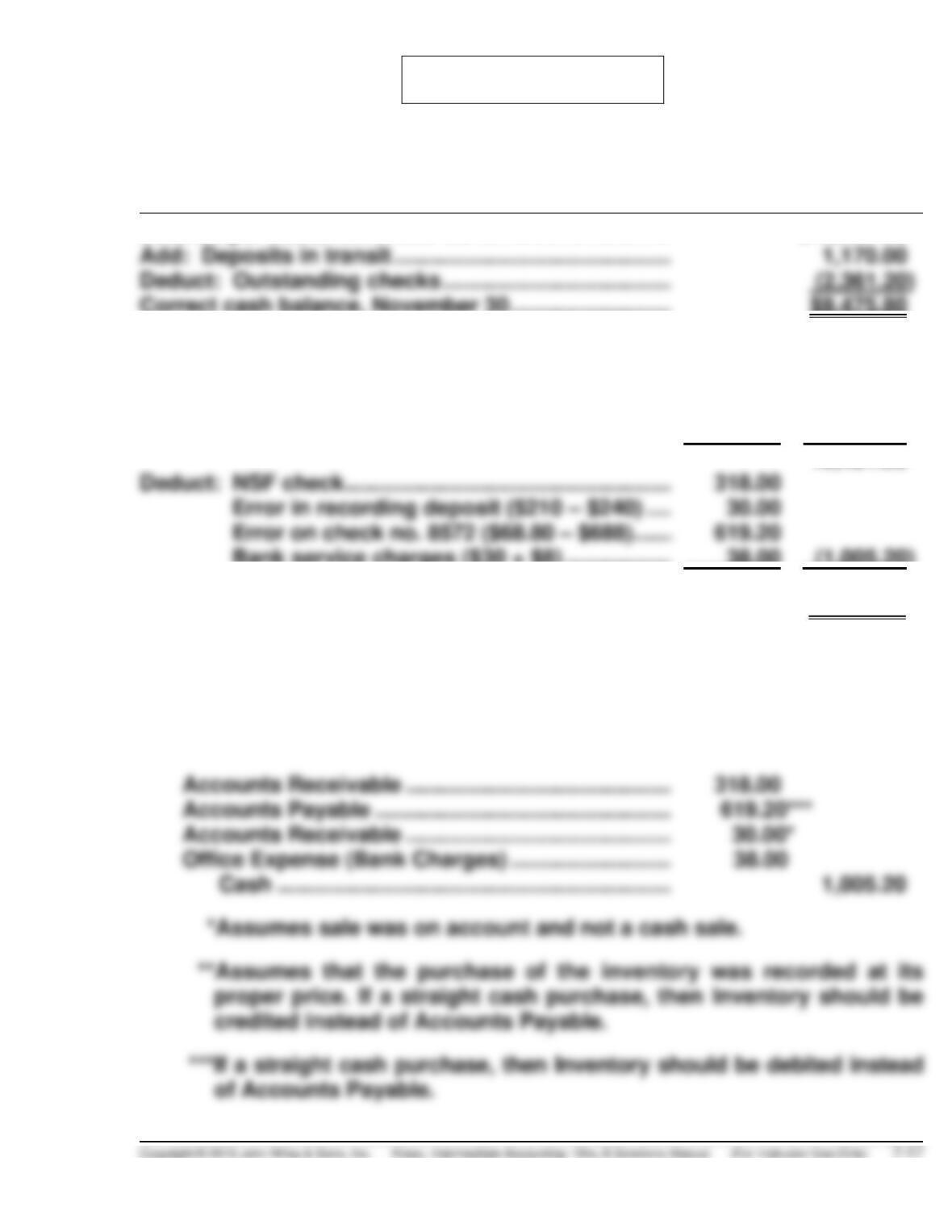

(a) GREEN CO.

Bank Reconciliation

November 30, 2014

Balance per bank, November 30 …………………………..

$10,667.00

Add: Deposits in transit ……………………………………………

Deduct: Outstanding checks …………………………………….

(2,361.20)

Correct cash balance, November 30 …………………………..

$9,475.80

Balance per books, November 30 …………………………..

$8,650.90

Add: Error on check no. 8560

($850 – $580) ………………………………………………..

$ 270.00

Note collection ($1,500 + $61) …………………………..

1,561.00

1,831.00

10,481.00

Deduct: NSF check …………………………………………………..

Error in recording deposit ($210 – $240) …..

Error on check no. 8572 ($68.80 – $688)…….

Bank service charges ($30 + $8) …………………..

38.00

(1,005.20)

Correct cash balance, November 30 …………………………..

$9,475.80

(b) Cash …………………………..………………………………….

1,831.00

Accounts Payable………………………………………

270.00**

Notes Receivable ……………………………………….

1,500.00

Interest Revenue ……………………………………….

61.00

Accounts Receivable ………………………………………

Accounts Payable …………………………………………..

Accounts Receivable ………………………………………

Office Expense (Bank Charges) ……………………….

Cash ……………………………………………………….

*PROBLEM 7-14B

(a) WIZARDS INC.

Bank Reconciliation

September 30

Balance per bank statement, September 30 ……………..

$17,780.63

Add:

Cash on hand, not deposited …………………………..

1,680.91

19,461.54

Deduct:

Outstanding checks

#5641 …………………………..…………………………..

#5642 …………………………..…………………………..

#5644 …………………………..…………………………..

#5645 …………………………..…………………………..

Balance per books, September 30 …………………………..

$13,661.12*

Add:

Bond interest collected by bank …………………………

900.00

14,561.12

Deduct:

Bank charges not recorded in books ………………….

$ 31.00

Customer’s check returned NSF …………………………

*Computation of balance per books,

September 30

*PROBLEM 7-14B (Continued)

(b)

September 30

Cash …………………………………………………………………

900.00

Interest Revenue ……………………………………….

900.00

Office Expense (Bank Charges) ………………………….

Cash …………………………………………………………

Accounts Receivable …………………………………………

Cash …………………………………………………………

*PROBLEM 7-15B

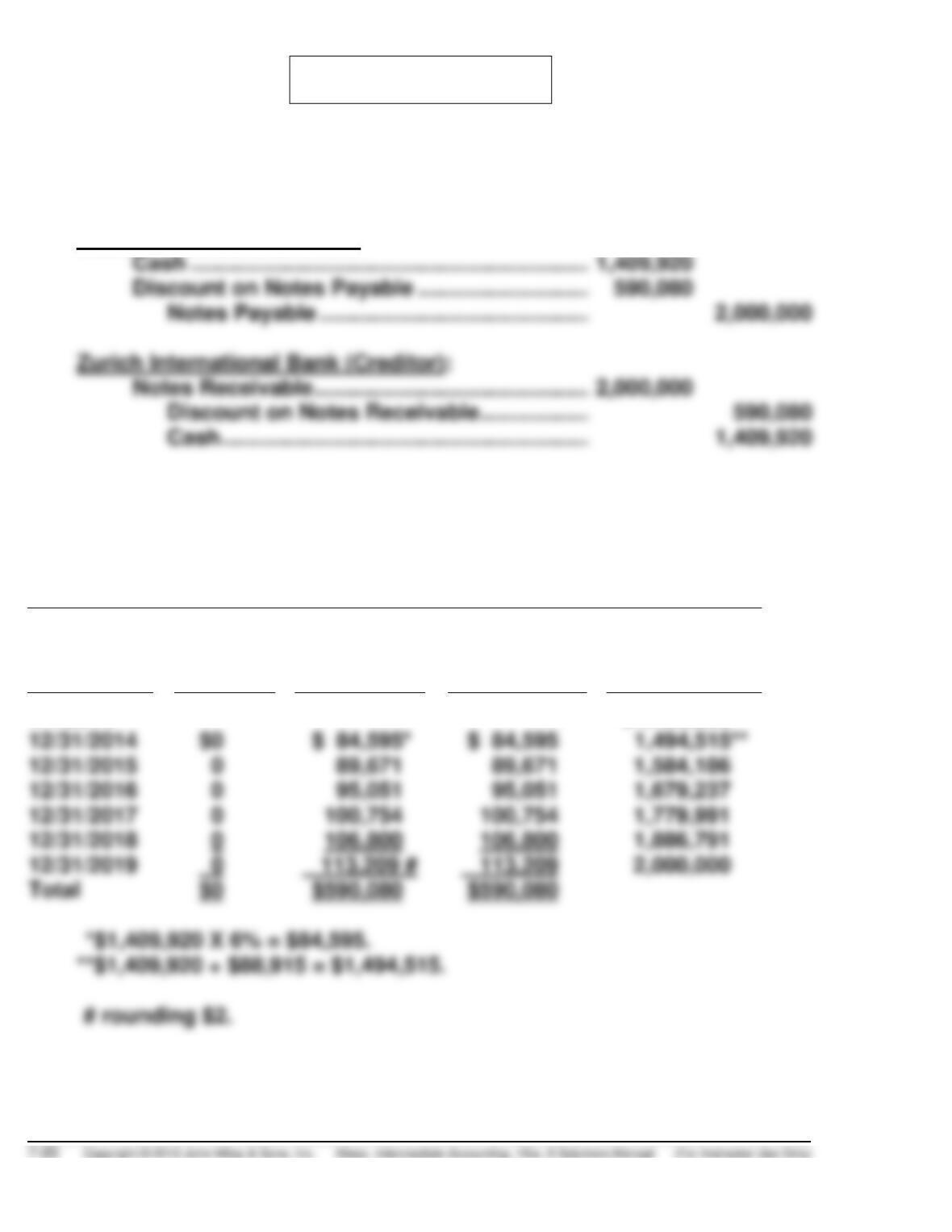

(a) The entries for the issuance of the note on January 1, 2014:

The present value of the note is: $2,000,000 X 0.70496 = $1,409,920.

Octopus Company (Debtor):

Discount on Notes Payable …………………………..

Notes Payable …………………………..……………….

Zurich International Bank (Creditor):

Notes Receivable …………………………………………….

Cash ……………………………………………………….

(b) The amortization schedule for this note is:

SCHEDULE FOR INTEREST AND DISCOUNT AMORTIZATION—

EFFECTIVE-INTEREST METHOD

$2,000,000 Note Issued to Yield 6%

Date

Cash

Paid

Interest

Expense

Discount

Amortized

Carrying

Amount of

Note

1/1/2014

$1,409,920

12/31/2014

12/31/2018

Total

*PROBLEM 7-15B (Continued)

(c) The note can be considered to be impaired only when it is probable

(d)

The loss is computed as follows:

Carrying amount of loan (12/31/2015) ……………………….

$1,584,186a

Loss due to impairment …………………………………………..

December 31, 2015

Zurich International Bank (Creditor):

Bad Debt Expense …………………………………….

831,700

Allowance for Doubtful Accounts …………