CHAPTER 19

SOLUTIONS TO B PROBLEMS

PROBLEM 19-1B

(a) X (0.30) = $270,000 taxes due for 2014

X = $270,000 ÷ 0.30

X = $900,000 taxable income for 2014

(c) 2014

Income Tax Expense

($270,000 + $30,000 – $12,000) ………………………. 288,000

2015

Income Tax Expense

($304,000 + $6,000 – $10,000) ………………………… 300,000

Deferred Tax Liability [($75,000 ÷ 3) X 0.40] ……….. 10,000

PROBLEM 19-2B

(a) Before deferred taxes can be computed, the amount of temporary

difference originating (reversing) each period and the resulting cumula-

tive temporary difference at each year-end must be computed:

2014

2015

2016

2017

Cumulative Temporary

Difference At End of Year

2014

$200,000

2014

Income Tax Expense ……………………………………….. 126,000

Income Taxes Payable ………………………………. 66,000

Deferred Tax Liability ………………………………… 60,000

PROBLEM 19-2B (Continued)

The deferred taxes at the end of 2014 would be computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$200,000

30%

$60,000

2015

Income Tax Expense ……………………………………….. 10,000*

Deferred Tax Liability ………………………………… 10,000

(To record the adjustment for the

increase in the enacted tax rate)

*The adjustment due to the change in the tax rate is computed as

follows:

Cumulative temporary difference at the end

PROBLEM 19-2B (Continued)

Taxable income for 2015 ………………………………………………. $200,000

The deferred taxes at December 31, 2015, are computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

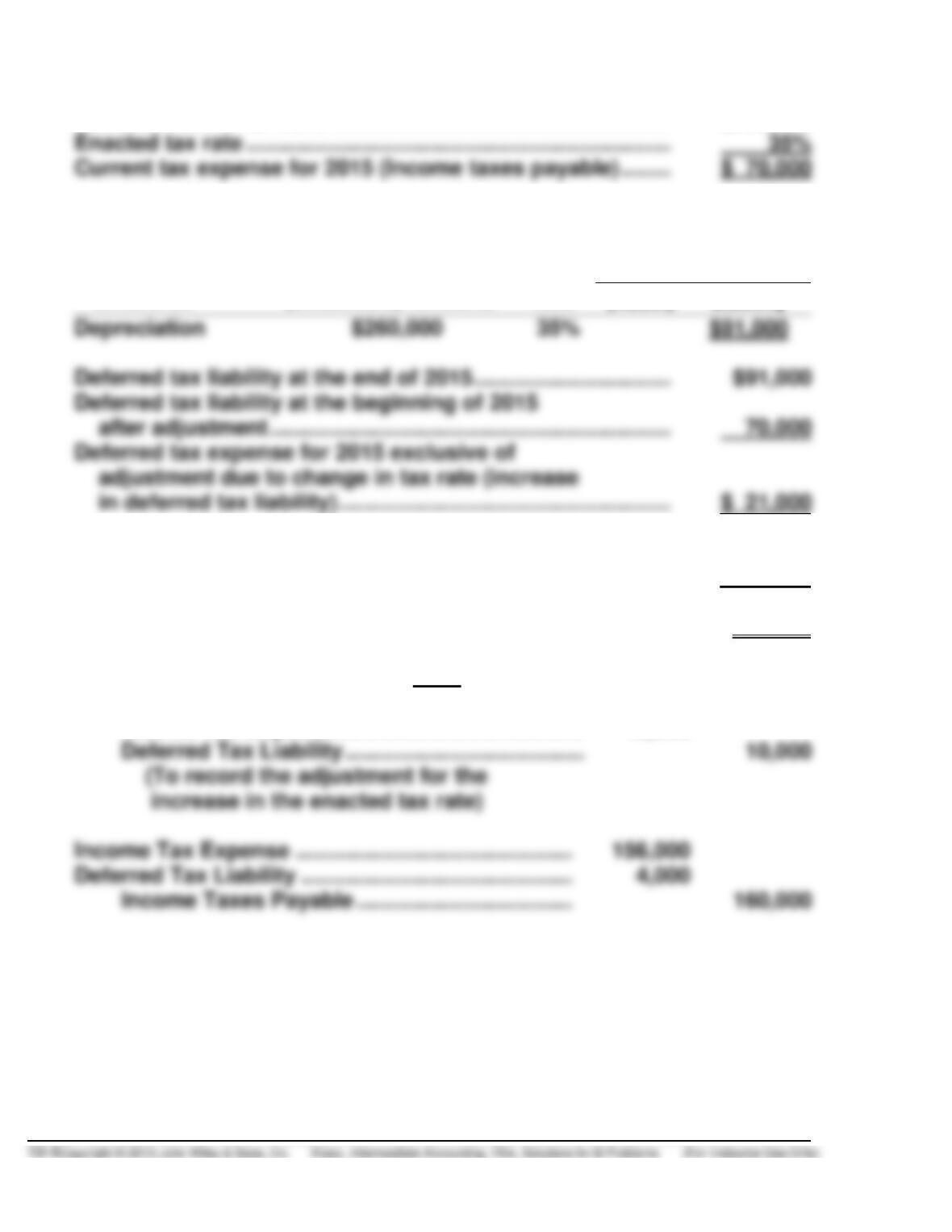

Deferred tax expense for 2015 ………………………………………. $ 21,000

Current tax expense for 2015 (Income taxes payable) …….. 70,000

Income tax expense (total) for 2015, exclusive

of adjustment due to change in tax rate ……………………… $91,000

2016

Income Tax Expense …………………………………. 10,000**

PROBLEM 19-2B (Continued)

**The adjustment due to the change in the tax rate is computed as

follows:

Cumulative temporary difference at the end

of 2015 ……………………………………………………………………. $260,000

The deferred taxes at December 31, 2016, are computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Depreciation

$250,000

40%

$100,000

Deferred tax liability at the end of 2016 ………………………….. $100,000

PROBLEM 19-2B (Continued)

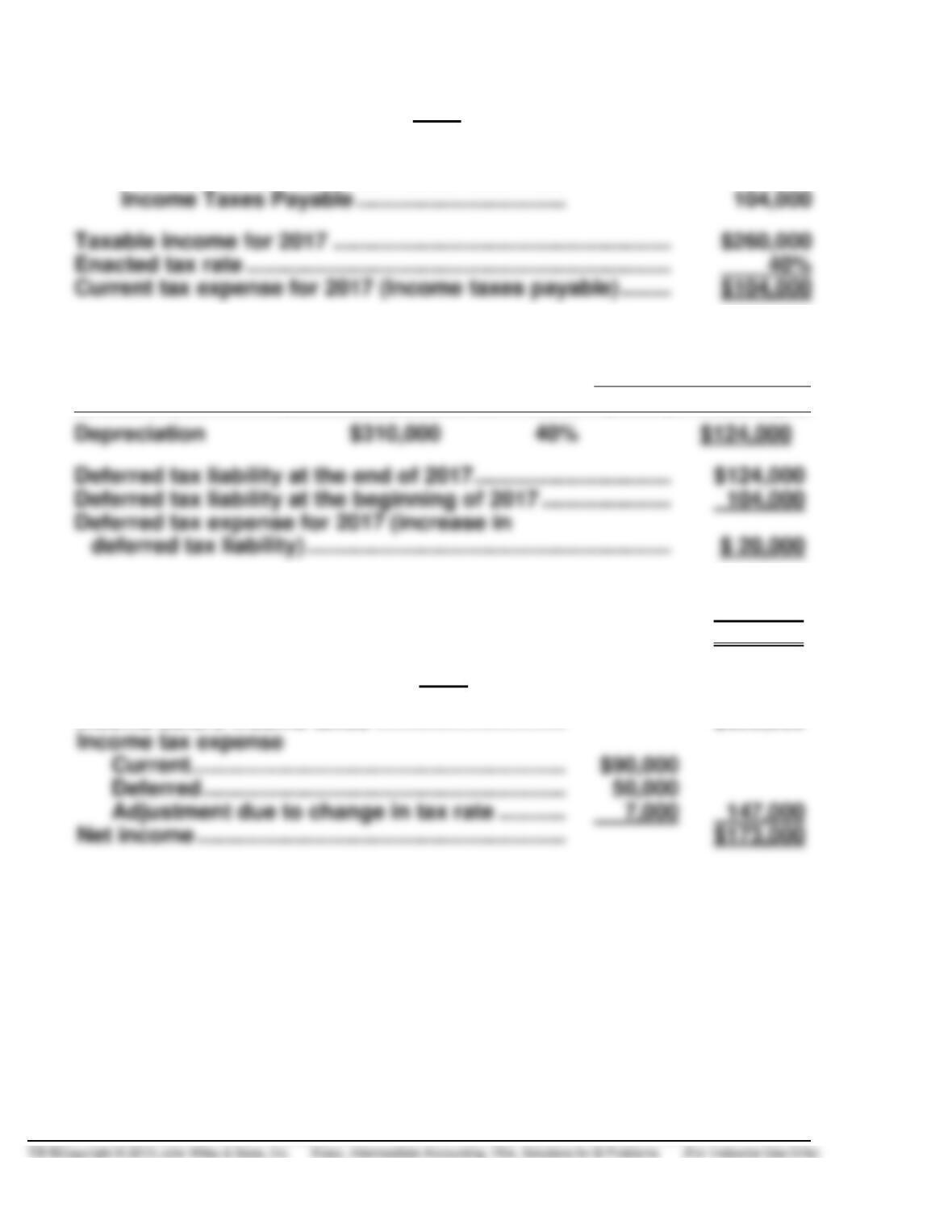

2017

Income Tax Expense …………………………………….. 124,000

Deferred Tax Liability ……………………………… 20,000

The deferred taxes at December 31, 2017, are computed as follows:

Temporary

Difference

Future Taxable

(Deductible) Amounts

Tax

Rate

Deferred Tax

(Asset)

Liability

Deferred tax expense for 2017 ………………………………………. $ 20,000

Current tax expense for 2017 (Income taxes payable) …….. 104,000

Income tax expense for 2017 …………………………..……………. $124,000

(b) 2015

Income before income taxes …………………………. $320,000

PROBLEM 19-3B

Book Depreciation

Tax Depreciation

Difference

2014

$ 112,500

$ 90,000*

($ 22,500

2015

112,500

180,000

(67,500)

2016

112,500

180,000

2017

112,500

180,000

2019

112,500

2020

112,500

2021

112,500

($ 0

(a) Pretax financial income for 2015 ……………………. $1,700,000

Nontaxable interest ………………………………………. (26,000)

(b) Income Tax Expense …………………………………….. 502,200

PROBLEM 19-3B (Continued)

Scheduling—End of 2015

Future Years

2016

2017

2018

Future taxable (deductible)

amounts

$(67,500)

$(67,500)

$(67,500)

Enacted tax rate

Deferred tax (asset) liability

$(20,250)

$(20,250)

$(20,250)

Future Years

2019

2020

2021

Future taxable (deductible)

amounts

Enacted tax rate

Deferred tax (asset) liability

The net deferred tax liability at December 31, 2015, is $13,500.

Scheduling—End of 2014

Future Years

2015

2016

2017

2018

Future taxable (deductible)

amounts

$(67,500)

$(67,500)

$(67,500)

$(67,500)

Enacted tax rate

Deferred tax (asset) liability

$(20,250)

$(20,250)

$(20,250)

$(20,250

Future Years

2019

2020

2021

Enacted tax rate

Deferred tax (asset) liability

PROBLEM 19-3 (Continued)

The net deferred tax asset at December 31, 2014, is $6,750.

Deferred tax liability at the end of 2015 …………………………... $ 13,500

Deferred tax liability at the beginning of 2015 …………………. 0

Deferred tax expense for 2015 (increase in

deferred tax liability) ………………………………………………….. $ 13,500

Current tax expense for 2015 (Income taxes payable) ……… $481,950

Deferred tax expense for 2015 …………………………..…………… 20,250

Income tax expense for 2015 …………………………………………. $502,200

(c) Income before income taxes and

extraordinary item …………………………………… $1,820,000a

Income tax expense

(d) Long-term liabilities

Deferred tax liability ……………………………………. $13,500

PROBLEM 19-4B

(a) Schedule of Pretax Financial Income

and Taxable Income for 2014

Pretax financial income ………………………………………………. $460,000

Permanent differences

Insurance expense ………………………………………………… 7,000

* Depreciation for books ($450,000/6) = $75,000

Depreciation tax return ($450,000 X 30%) = 135,000

Difference $60,000

PROBLEM 19-4B (Continued)

(b) The journal entry to record income taxes payable, income tax expense

and deferred income taxes is as follows:

Income Tax Expense ……………………………………… 142,200*

Deferred Tax Asset ……………………………………….. 19,800

Deferred Tax Liability ($18,000 + $30,000) ….. 48,000

PROBLEM 19-5B

(a) 2014

Income Tax Refund Receivable

[($10,000 X 30%) + ($45,000 X 40%)] ……………….. 21,000

Benefit Due to Loss Carryback …………………… 21,000

2016

Income Tax Expense ………………………………………… 18,000

Deferred Tax Asset [($85,000 – $30,000) X 30%] 16,500

Income Taxes Payable

[($60,000 – $55,000) X 30%) …………………….. 1,500

(b) The income tax refund receivable account totaling $21,000 will be

reported under current assets on the balance sheet at December 31, 2014.

This type of receivable is usually listed immediately above inventory in