CHAPTER 23

SOLUTIONS TO B PROBLEMS

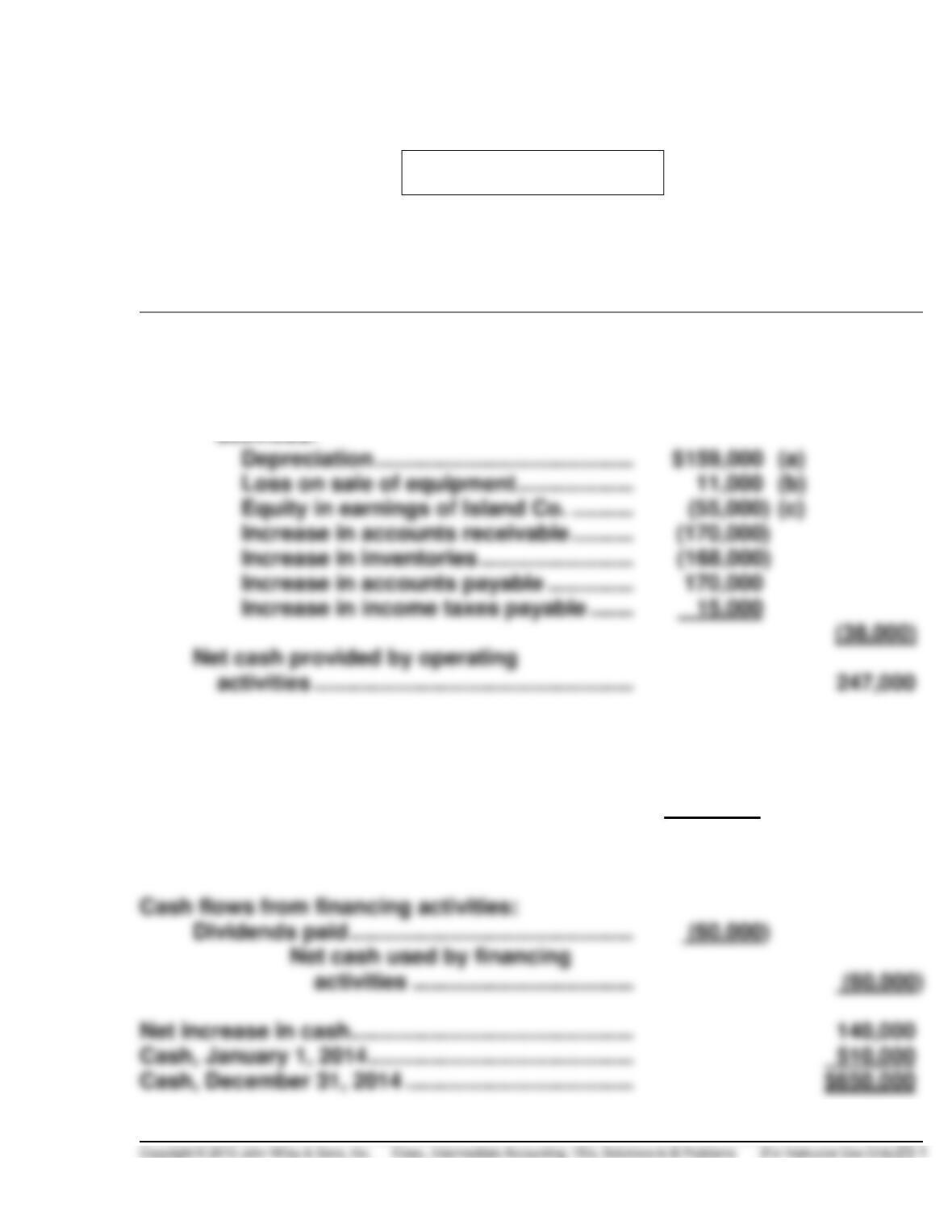

PROBLEM 23-1B

SANIBEL CORP.

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………….

$285,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation ……………………………………

(a)

Loss on sale of equipment ……………….

(b)

Equity in earnings of Island Co. ……….

(c)

Increase in accounts receivable ……….

(170,000)

Increase in inventories …………………….

Increase in accounts payable …………..

Net cash provided by operating

activities …………………………………………….

Cash flows from investing activities:

Purchase of equipment

(167,000)

(d)

Proceeds from sale of equipment ……………

20,000

Principal payment of loan receivable ……….

100,000

Net cash provided by investing

activities ………………………………

(47,000)

Cash flows from financing activities:

Dividends paid ……………………………………….

Net cash used by financing

activities ………………………………

Net increase in cash ……………………………………….

Cash, January 1, 2014 …………………………………….

PROBLEM 23-1B (Continued)

Schedule at bottom of statement of cash flows:

Noncash investing and financing activities:

Issuance of lease obligation for capital lease ….

$850,000

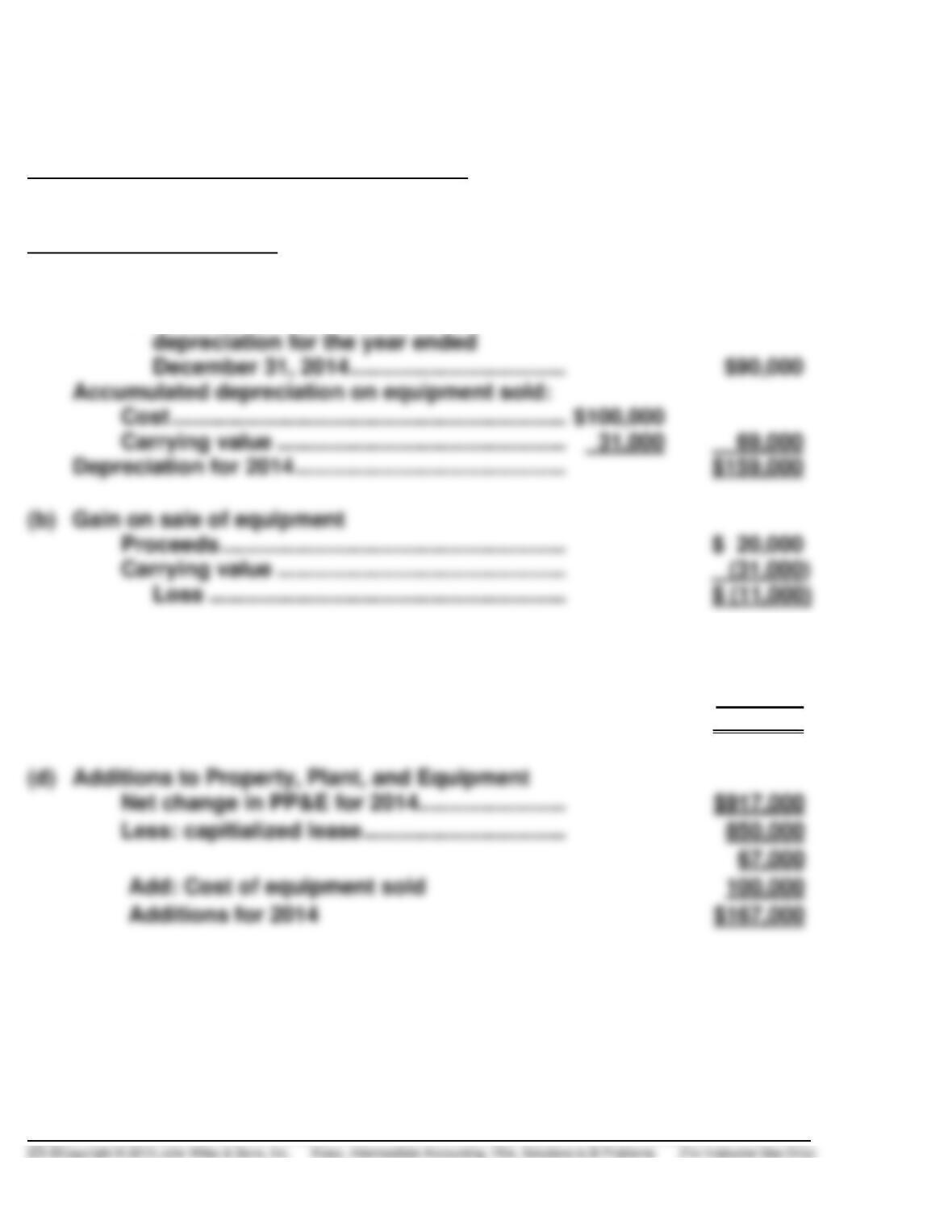

Explanation of Amounts

(a) Depreciation

Net increase in accumulated

depreciation for the year ended

December 31, 2014 ……………………………..

Accumulated depreciation on equipment sold:

Cost …………………………..…………………………..

Carrying value ………………………………………..

Depreciation for 2014 ……………………………………..

(b) Gain on sale of equipment

Proceeds ………………………………………………..

Carrying value ………………………………………..

Loss ………………………………………………….

(c) Equity in earnings of Island Co.

Myers’s net income for 2014 ……………………

$220,000

Sullivan’s ownership ……………………………….

X 25%

Undistributed earnings of Island Co ….

$ 55,000

(d) Additions to Property, Plant, and Equipment

Net change in PP&E for 2014……………………

$917,000

Less: capitialized lease …………………………...

Add: Cost of equipment sold

Additions for 2014

$167,000

PROBLEM 23-2B

QUEEN CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ……………………………………………..

$105,900 (a)

Adjustments to reconcile net income

to net cash provided by operating

activities:

Loss on sale of equipment ……………….

(b)

Gain from hurricane damage …………….

(133,000)

*

Depreciation expense ………………………

(c)

Patent amortization ………………………….

Loss on sale of investments ……………..

Increase in accounts receivable (net) ..

Decrease in inventory ………………………

Increase in accounts payable ……………

(82,300)

Net cash provided by operating activities …

Cash flows from investing activities

Sale of investments …………………………………

39,200

Sale of equipment …………………………………..

Purchase of equipment …………………………...

Proceeds from damage to building …………..

Net cash provided by investing activities …

Cash flows from financing activities

Payment of dividends ……………………………..

(12,000)

***

Payment of long-term notes payable ………..

(212,000)

(e)

Proceeds from short-term note payable ……

Increase in cash …………………………………………….

Cash, January 1, 2014 …………………………………….

PROBLEM 23-2B (Continued)

Supplemental disclosures of cash flow information:

Cash paid during the year for:

Interest

$1,000

Income taxes:

$23,600

Noncash investing and financing activities

Retired notes payable by issuing common stock

Purchased equipment by issuing notes payable

Supporting Computations:

(a) Ending retained earnings ………………………………..

$153,400

Beginning retained earnings …………………………...

(53,500)

Cash dividends declared …………………………………

6,000

Net income ……………………………………………………..

$105,900

(b) Cost ……………………………………………………………….

Accumulated depreciation (60% X $20,000) ………

Book value …………………………..…………………………

Proceeds from sale …………………………………………

Loss on sale …………………………………………………..

(c) Accumulated depreciation on equipment sold ….

$ 12,000

Increase in accumulated depreciation ………………

25,000

Depreciation expense ……………………………………..

$ 37,000

(d) Beginning equipment balance …………………………

$120,000

Cost of equipment sold …………………………………..

Remaining balance …………………………………………

Purchase of equipment with note …………………….

Adjusted balance ……………………………………………

Ending equipment balance ………………………………

Purchased with cash……………………………………….

PROBLEM 23-2B (Continued)

(e) Beginning long-term notes payable balance …….

$260,000

Retired notes by issuing common stock…………..

(18,000)

Remaining balance …………………………………………

242,000

Purchase of equipment with note …………………….

Adjusted balance ……………………………………………

Ending long-term notes payable balance ………….

(50,000)

Retired with cash ……………………………………………

PROBLEM 23-3B

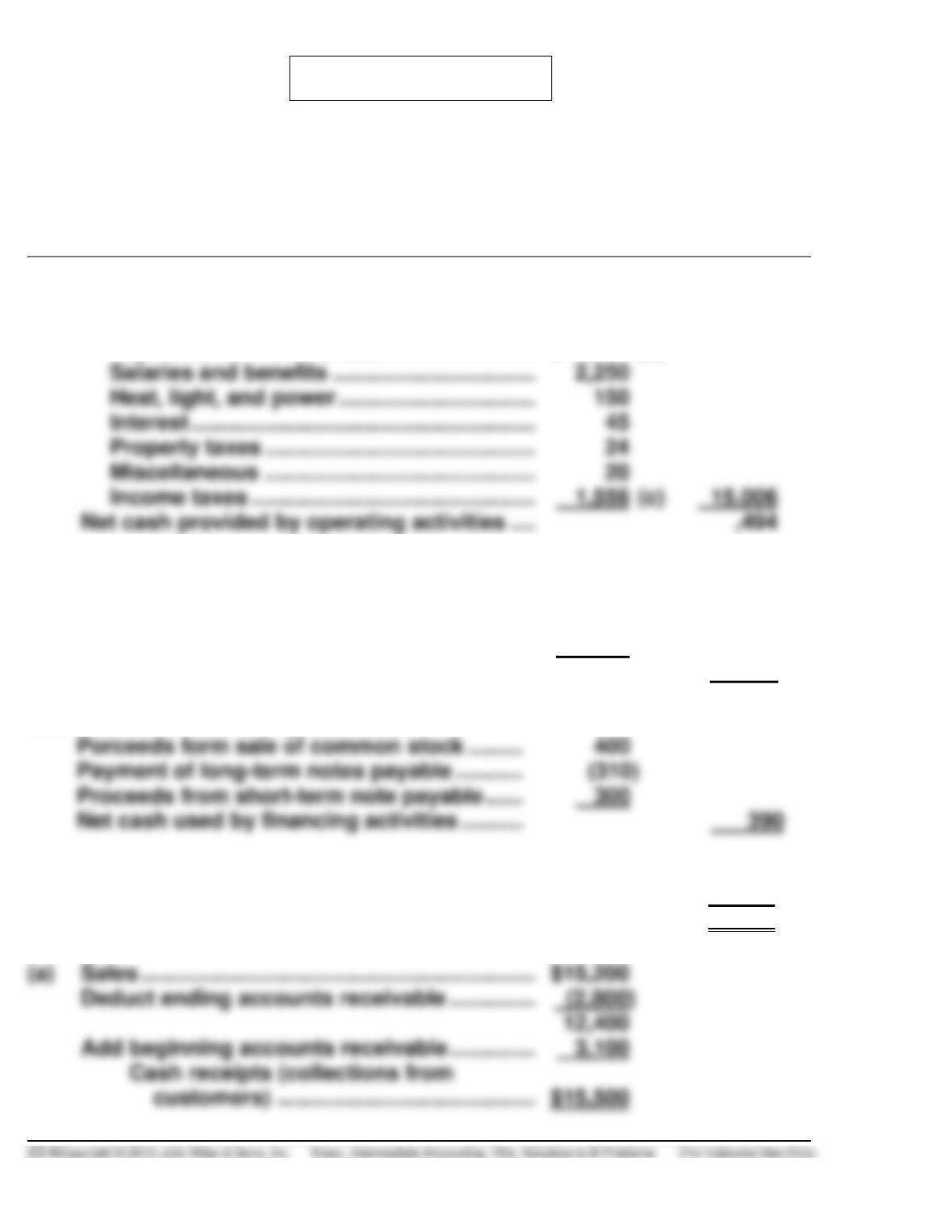

SEAHORSE INNS COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

($000 Omitted)

Cash flows from operating activities

Cash receipts from customers ………………….

$15,500 (a)

Cash payments:

Payments for merchandise …………………..

$10,961

(b)

Salaries and benefits …………………………...

Heat, light, and power …………………………..

Interest ………………………………………………..

45

Property taxes ……………………………………..

24

Miscellaneous ……………………………………..

Income taxes ……………………………………….

1,556

(c)

Net cash provided by operating activities ….

Cash flows from investing activities

Sale of available-for-sale investments ……….

35

Purchase of buildings and equipment ……….

(750)

Purchase of land ………………………………………

(180)

Net cash used by investing activities …………

(965)

Cash flows from financing activities

Porceeds form sale of common stock ………

Payment of long-term notes payable ………..

Proceeds from short-term note payable ……

Net cash used by financing activities ……….

Decrease in cash ……………………………………………..

(81)

Cash, January 1, 2014 …………………………..………….

210

Cash, December 31, 2014………………………………….

$ 129

(a) Sales ……………………………………………………….

Deduct ending accounts receivable …………..

Add beginning accounts receivable …………..

3,100

Cash receipts (collections from

PROBLEM 23-3B (Continued)

(b) Cost of goods sold…………………………………

$9,200

Add ending inventory …………………………….

2,860

Goods available for sale ………………….

Deduct beginning inventory ……………………

Purchases ………………………………………

Deduct ending accounts payable ……………

Add beginning accounts payable ……………

2,740

Cash purchases (payments for

(c) Income taxes …………………………………………

$ 1,336

Deduct ending income taxes payable ……..

(240)

Add beginning income taxes payable ……..

460

PROBLEM 23-4B

WIZARDS COMPANY

Statement of Cash Flows

For the Year Ended December 31, 2014

(Direct Method)

Cash flows from operating activities

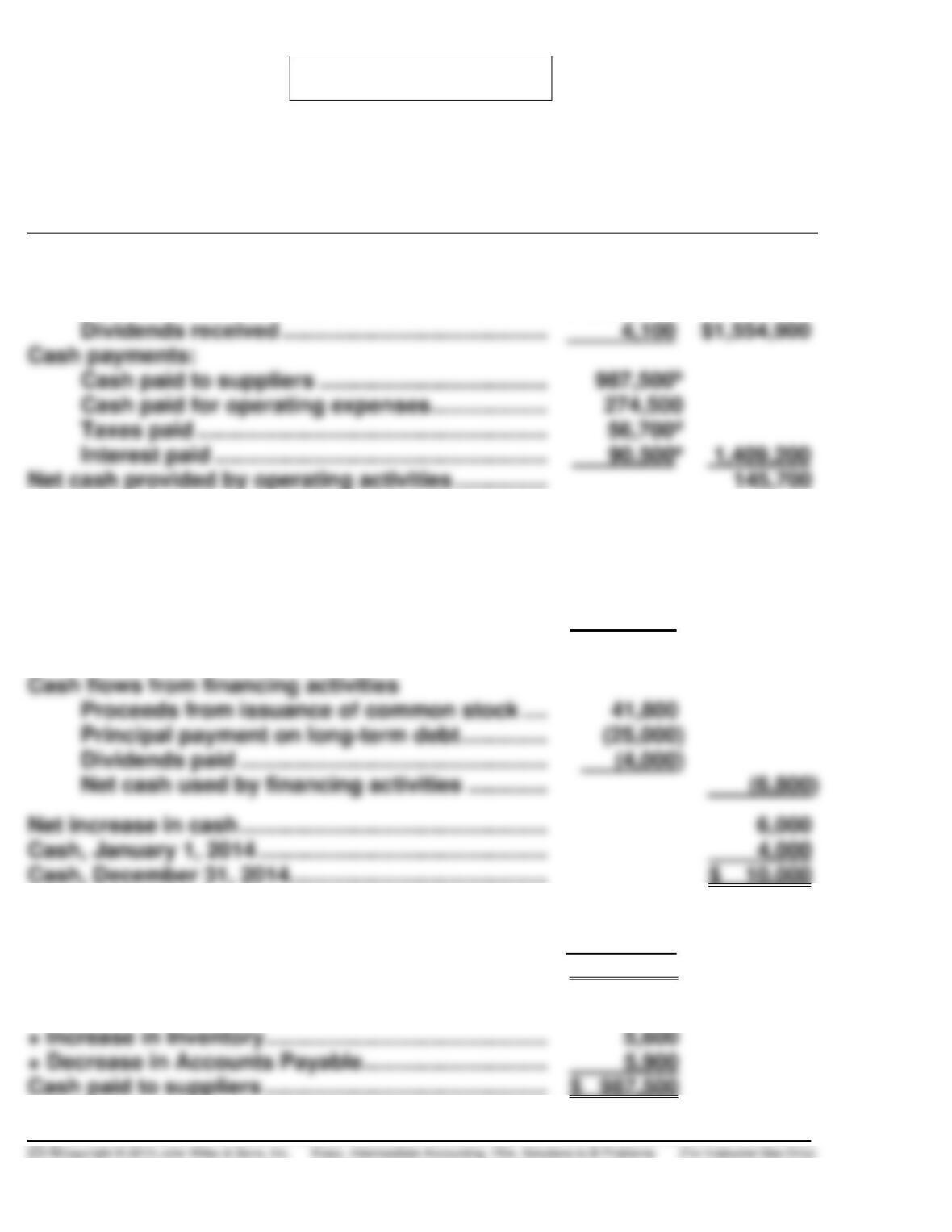

Cash receipts:

Cash received from customers …………………….

$1,550,800a

Dividends received …………………………..…………

Cash payments:

Cash paid for operating expenses ………………..

Taxes paid …………………………..……………………..

Interest paid ……………………………………………….

Net cash provided by operating activities …………….

Cash flows from investing activities

Sale of short-term investments

($8,500 – $8,000) ……………………………………….

500

Sale of land ($260,000 – $200,000) + $21,000 …

81,000

Purchase of equipment ……………………………….

(196,000)

Net cash used by investing activities ……………

(55,000)

Cash flows from financing activities

Proceeds from issuance of common stock …..

Principal payment on long-term debt ……………

Dividends paid ……………………………………………

Net cash used by financing activities …………..

Net increase in cash ……………………………………………

Cash, January 1, 2014 …………………………………………

Cash, December 31, 2014…………………………………….

aSales Revenue …………………………………………………..

$1,560,000

– Increase in Accounts Receivable ………………………

(9,200)

Cash received from customers …………………………..

$1,550,800

bCost of Goods Sold …………………………………………….

$ 976,000

+ Increase in Inventory …………………………………………

+ Decrease in Accounts Payable …………………………..

5,900

PROBLEM 23-4B (Continued)

cOperating Expenses ………………………………………

$339,900

– Depreciation/Amortization expense ……………….

(63,000)

– Decrease in prepaid expenses ………………………

(10,400)

+ Decrease in wages payable …………………………..

– Increase in income taxes payable ………………….

– Decrease in bond discount …………………………...

Reconciliation of Net Income to Net Cash

Provided by Operating Activities:

Net income ……………………………………………………..

$103,350

Adjustments to reconcile net income to net

cash provided by operating activities:

Depreciation/amortization expense ……………

$63,000

Decrease in prepaid expenses …………………..

10,400

Increase in income taxes payable ……………..

5,800

Decrease in salaries and wages payable ……

Increase in accounts receivable ………………..

Increase in inventory ………………………………..

Decrease in accounts payable …………………..

Gain on sale of land ………………………………….

(21,000)

Loss on sale of short-term investments …….

8,000

Amortization of bond discount ………………….

Total adjustments ……………………………..

PROBLEM 23-5B

CLARK CORPORATION

Statement of Cash Flows

For the Year Ended December 31, 2014

(Indirect Method)

Cash flows from operating activities

Net income ……………………………………………….

$76,538

Adjustments to reconcile net income

to net cash used by operating

activities:

Loss on sale of equipmemt …………………

$ 5,600

(2)

Loss on retirement of bonds ……………….

8,981

(3)

Depreciation of equipment ………………….

62,800

(2)

Depreciation of building ……………………..

(6)

Amortization of patents ………………………

(1)

Amortization of trademark ………………….

Amortization of bond discount ……………

(3)

Amortization of bond issue costs ………..

(4)

Amortization of bond premium ……………

(4)

Equity in earnings of subsidiary ………….

(54,000)

(5)

Increase in accounts receivable

(net) ………………………………………………..

(41,700)

Increase in inventory ………………………….

(59,265)

Increase in prepaid expenses ……………..

(8,000)

Increase in taxes payable ……………………

33,500

Increase in salaries and wages payable .

Increase in accounts payable ……………..

26,000

Net cash used by operating activities …………

Cash flows from investing activities

Sale of equipment ……………………………………..

15,000

(2)

Investment in subsidiary …………………………...

(146,000)

(5)

Addition to buildings …………………………………

(125,000)

Extraordinary repairs to building………………..

(6)

Purchase of equipment ……………………………..

(117,400)

(2)

Purchase of patent…………………………………….

(1)

Net cash used by investing activities ………….

PROBLEM 23-5B (Continued)

Cash flows from financing activities

Redemption of bonds ………………………………..

(303,000)

(3)

Sale of bonds less expense of sale …………….

406,800

(4)

Payment of cash dividends ………………………..

Sale of stock ……………………………………………..

Net cash provided by financing activities ……

Decrease in cash ……………………………………………..

Cash, January 1, 2014 ………………………………………

Supplemental disclosures of cash flow information:

Cash paid during the year for:

Interest ……………………………………………………..

Income taxes …………………………………………….

PROBLEM 23-5B (Continued)

Comments on Numbered Items

(1) A patent was purchased for $31,000 cash. The account activity is

analyzed as follows:

Balance 12/31/13 ……………………………………………

Purchase ……………………………………………………….

Total ……………………………………………………………..

101,000

Balance 12/31/14 ……………………………………………

Amortization charged against income which

(2) Analysis of the Equipment account shows the following:

Balance 12/31/13 …………………………………………….

$290,000

Disposition of equipment …………………………..……

(26,400)

Total ………………………………………………………

263,600

Balance 12/31/14 …………………………………………….

Loss on sale:

Analysis of accumulated depreciation—

equipment:

Balance 12/31/13 of Accumulated

Depreciation …………………………………

Amount on asset sold ………………………

Balance …………………………………………..

Balance 12/31/14 ……………………………..

Depreciation charged against income