Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–41

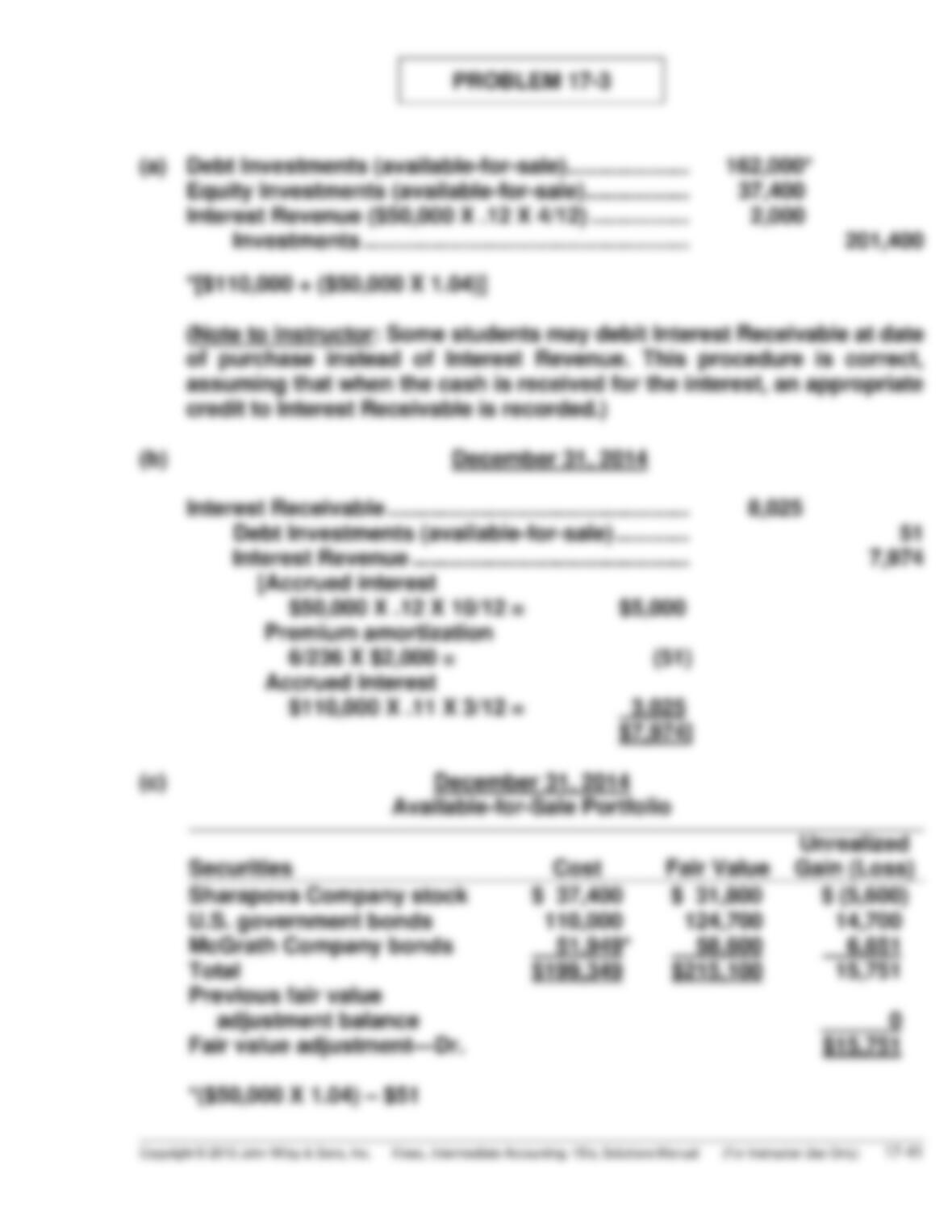

PROBLEM 17-3

(a) Debt Investments (available-for-sale)……………….. 162,000*

Equity Investments (available-for-sale) …………….. 37,400

Interest Revenue ($50,000 X .12 X 4/12) ……………. 2,000

Investments …………………………………………….. 201,400

17–42 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 17-3 (Continued)

Fair Value Adjustment (available-for-sale) ………. 15,751

Unrealized Holding Gain or Loss—Equity … 15,751

(d) July 1, 2015

Cash ($119,200 + $3,025) ……………………………….. 122,225

Debt Investments (available-for-sale) ………. 110,000

Interest Revenue ($110,000 X .11 X 3/12) ….. 3,025

Gain on Sale of Investments …………………… 9,200

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–43

PROBLEM 17-4

(a) The bonds were purchased at a discount. That is, they were purchased

at less than their face value because the bonds’ amortized cost

increased from $491,150 to $550,000.

(b) December 31, 2014

Fair Value Adjustment (available-for-sale) …………… 4,850

Unrealized Holding Gain or Loss—Equity …….. 4,850

Available-for-Sale Portfolio

Amortized

Cost

Fair

Value

Unrealized

Gain (Loss)

Debt Investment

$491,150

$497,000

$5,850

Previous fair value adjustment—Dr.

1,000

Fair value adjustment—Dr.

$4,850

Debt Investment

$519,442

$509,000

$(10,442)

Previous fair value adjustment—Dr.

5,850

Fair value adjustment—Cr. needed

to bring balance to $10,442 Cr.

($16,292)

17–44 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

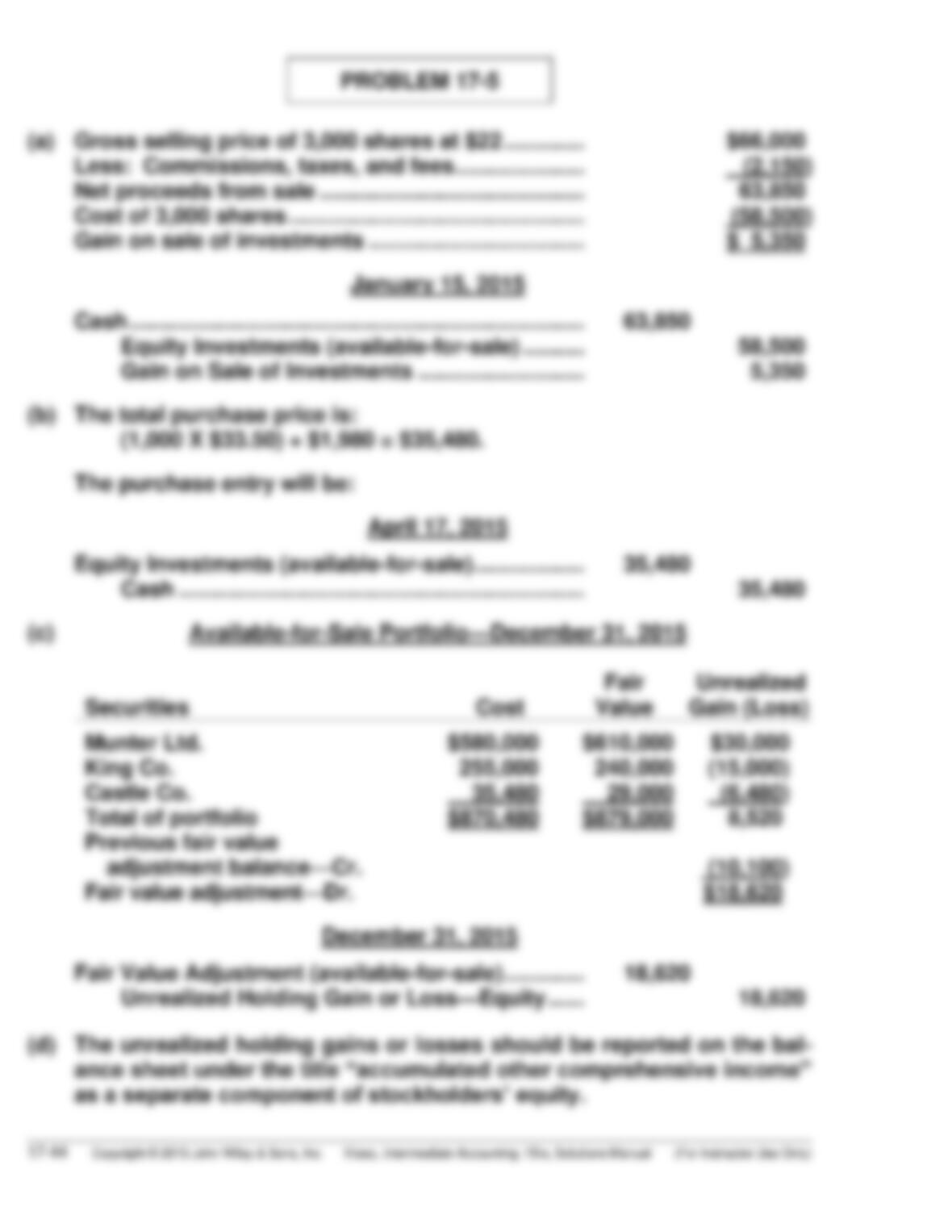

PROBLEM 17-5

(a) Gross selling price of 3,000 shares at $22 …………. $66,000

Less: Commissions, taxes, and fees ………………… (2,150)

Net proceeds from sale ……………………………………. 63,850

Cost of 3,000 shares ………………………………………… (58,500)

Gain on sale of investments …………………………….. $ 5,350

Equity Investments (available-for-sale) ………. 58,500

Munter Ltd.

King Co.

255,000

240,000

(15,000)

Castle Co.

35,480

29,000

(6,480)

Total of portfolio

$870,480

$879,000

( 8,520

Previous fair value

adjustment balance—Cr.

(10,100)

Fair value adjustment—Dr.

$18,620

Unrealized Holding Gain or Loss—Equity …… 18,620

(d) The unrealized holding gains or losses should be reported on the bal–

ance sheet under the title “accumulated other comprehensive income”

as a separate component of stockholders’ equity.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–45

PROBLEM 17-6

(a) (1) October 10, 2014

Cash (5,000 X $54) ……………………………………. 270,000

Gain on Sale of Investments ………………. 55,000

Equity Investments (trading) ……………………. 163,500

17–46 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 17-6 (Continued)

At December 31, 2014, McElroy had the following fair value

adjustment:

Trading Securities Portfolio—December 31, 2014

Securities

Cost

Fair

Value

Unrealized

Gain (Loss)

Monty, Inc. preferred

$133,000

$106,000

($(27,000)

Oakwood Corp. common

180,000

193,000

13,000)

Patriot common

163,500

132,000

( (31,500)

Total of portfolio

$476,500

$431,000

(45,500)

Previous fair value adjustment

balance—Cr.

(9,000)

Fair value adjustment—Cr.

($(36,500)

used would be associated with available-for-sale securities. In addition,

the Unrealized Holding Gain or Loss—Equity account is used instead of

Unrealized Holding Gain or Loss—Income. The Unrealized Holding

Loss—Equity is included in other comprehensive income and then

would be reported on the balance sheet in Accumulated comprehensive

income.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–47

PROBLEM 17-7

(a) February 1

Debt Investments (available-for-sale)………………… 300,000

Interest Revenue (4/12 X .10 X $300,000) …………… 10,000

Cash ………………………………………………………… 310,000

April 1

Cash ……………………………………………………………….. 15,000

Interest Revenue ($300,000 X .10 X 6/12) …….. 15,000

July 1

Debt Investments (available-for-sale)………………… 200,000

Interest Revenue (1/12 X .09 X $200,000) …………… 1,500

Cash ………………………………………………………… 201,500

September 1

Cash [($60,000 X 99%) + ($60,000 X .10 X 5/12)] …. 61,900

Loss on Sale of Investments …………………………... 600

Debt Investments (available-for-sale) …………. 60,000

Interest Revenue

(5/12 X .10 X $60,000 = $2,500) ……………….. 2,500

December 1

Cash ($200,000 X 9% X 6/12) …………………………….. 9,000

Interest Revenue ………………………………………. 9,000

17–48 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 17-7 (Continued)

December 31

Interest Receivable …………………………………………. 7,500

Interest Revenue ……………………………………… 7,500

(3/12 X $240,000 X .10 = $6,000)

(1/12 X $200,000 X .09 = $1,500)

($6,000 + $1,500 = $7,500)

Gibbons Co.

$240,000

$228,000*

$(12,000)

Sampson, Inc.

200,000

186,000**

(14,000)

Total

$440,000

$414,000

$(26,000)

*$240,000 X 95%

**$200,000 X 93%

Investments (held-to–maturity) would be used instead of Debt

Investments (available-for-sale). In addition, held–to-maturity securities

would be carried at amortized cost and not valued at fair value at year–

end, so the last entry would not be made.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–49

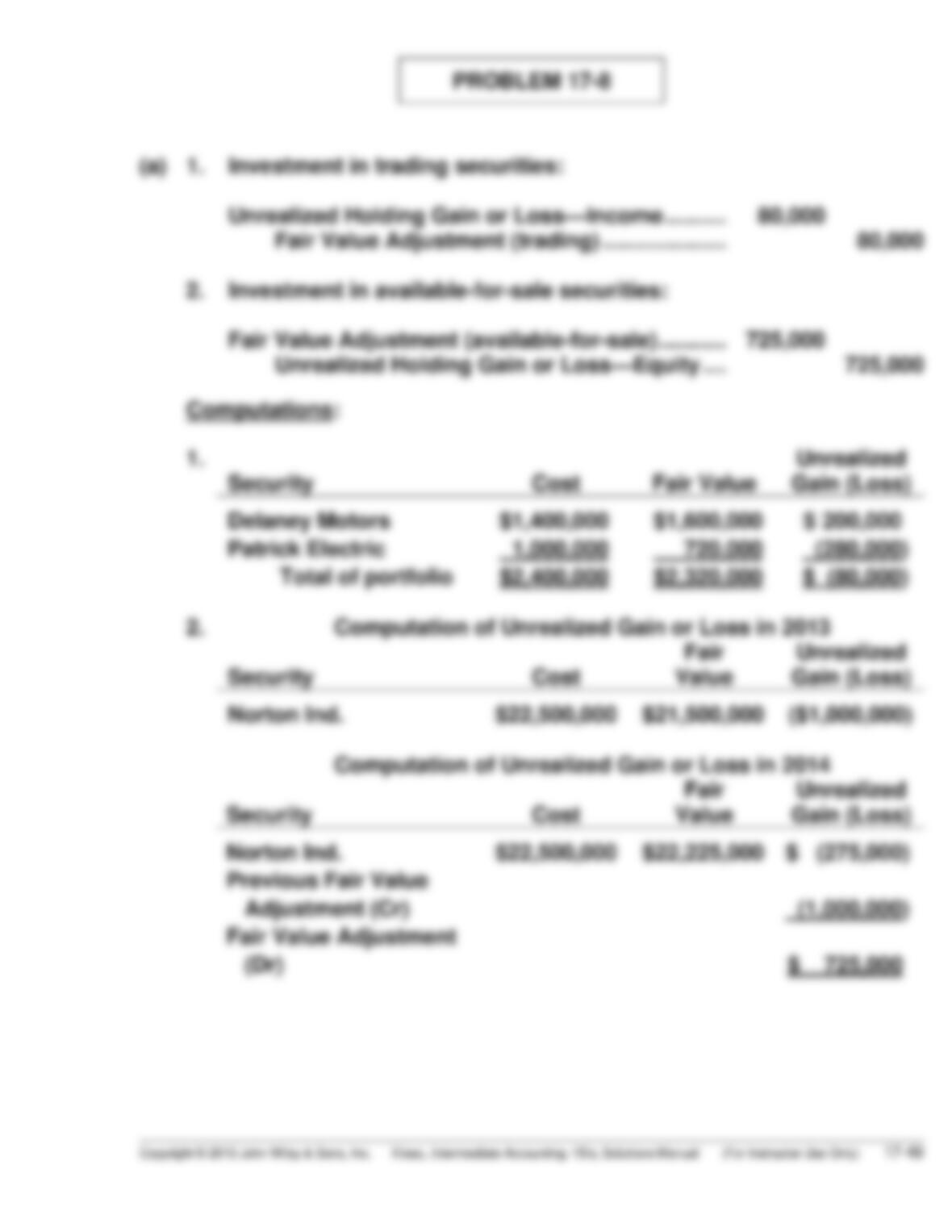

PROBLEM 17-8

(a) 1. Investment in trading securities:

Unrealized Holding Gain or Loss—Income ………. 80,000

Fair Value Adjustment (trading) ……………….. 80,000

2. Investment in available-for-sale securities:

Fair Value Adjustment (available-for-sale) ……….. 725,000

Unrealized Holding Gain or Loss—Equity …. 725,000

Patrick Electric

1,000,000

720,000

( (280,000)

Total of portfolio

$2,400,000

$2,320,000

($ (80,000)

Norton Ind.

$22,500,000

$21,500,000

(($1,000,000)

Norton Ind.

$22,500,000

$22,225,000

Previous Fair Value

Adjustment (Cr)

(1,000,000)

Fair Value Adjustment

(Dr)

$ 725,000

Delaney Motors

$1,400,000

$1,600,000

17–50 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 17-8 (Continued)

(b) The unrealized holding loss on the valuation of Brooks’ trading securities

is reported on the income statement. The loss would appear in the “Other

expenses and losses” section of the income statement. The Fair Value

Adjustment is a valuation account and it will be used to show the

reduction in the fair value of the trading securities. The trading

securities portfolio is disclosed in the balance sheet as a current asset

and reported at its fair value.

account is used to report the increase in fair value of the available-for–

sale securities. The fair value of the securities is reported in the

Investments section of the balance sheet. It should be noted that a

combined statement of income and comprehensive income, a statement

of comprehensive income, or a statement of stockholders’ equity would

report the components of comprehensive income.

realized holding losses. Any change in the net unrealized holding gain

or loss account should also be disclosed. The disclosure for trading

securities includes the change in net unrealized holding gains or losses

which was included in earnings.

Cash ($100,000 X 25%) ………………………………………. 25,000

Equity Investments (Norton Industries) ………….. 25,000

With 25% ownership, Brooks has significant influence and should apply

the equity method. No fair value adjustments are recorded under the

equity method.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–51

PROBLEM 17-9

(a) Available-for-Sale Portfolio

Securities

Cost

Fair

Value

Unrealized

Gain (Loss)

Frank, Inc.

$ 22,000

$ 32,000

($(10,000)

Ellis Corp.

115,000

95,000

(20,000)

Mendota Company

124,000

96,000

( (28,000)

Total of portfolio

$261,000

$223,000

($(38,000)

Equity Investments (available-for-sale) ………. $261,000

Less: Fair value adjustment ……………………… 38,000

Equity Investments (available-for-sale),

at fair value ……………………………………………. $223,000

Paid-in capital in excess of par—

common stock ……………………………………….. xx

Retained earnings …………………………………….. xx

Accumulated other comprehensive loss …….. (38,000)

Total stockholders’ equity ………………….. $ xx

Fair

Value

Unrealized

Ellis Corp.

$115,000

$140,000

Mendota Company

Total of portfolio

$289,000

$278,000

($(11,000)

Previous fair value

adjustment balance—Cr.

( (38,000)

Fair Value Adjustment—Dr.

($27,000

*(4,000 X $31) + (2,000 X $25)

**[(4,000 + 2,000) X $23]

17–52 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 17-9 (Continued)

Balance Sheet—December 31, 2015

Long-term investments:

Equity investments (available-for-sale),

at cost ………………………………………………. $289,000

Less: Fair value adjustment …………………. 11,000

Equity investments (available-for-sale),

at fair value ……………………………………….. $278,000

Paid-in capital in excess of par—

common stock …………………………………… xx

Retained earnings ………………………………… xx

Accumulated other comprehensive loss … (11,000)

Total stockholders’ equity ……………… $ xx

value, which is the new cost basis of the security. The unrealized

holding loss of $6,000 [($11 – $8) X 2,000] is recognized in earnings at

the date of the transfer.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–53

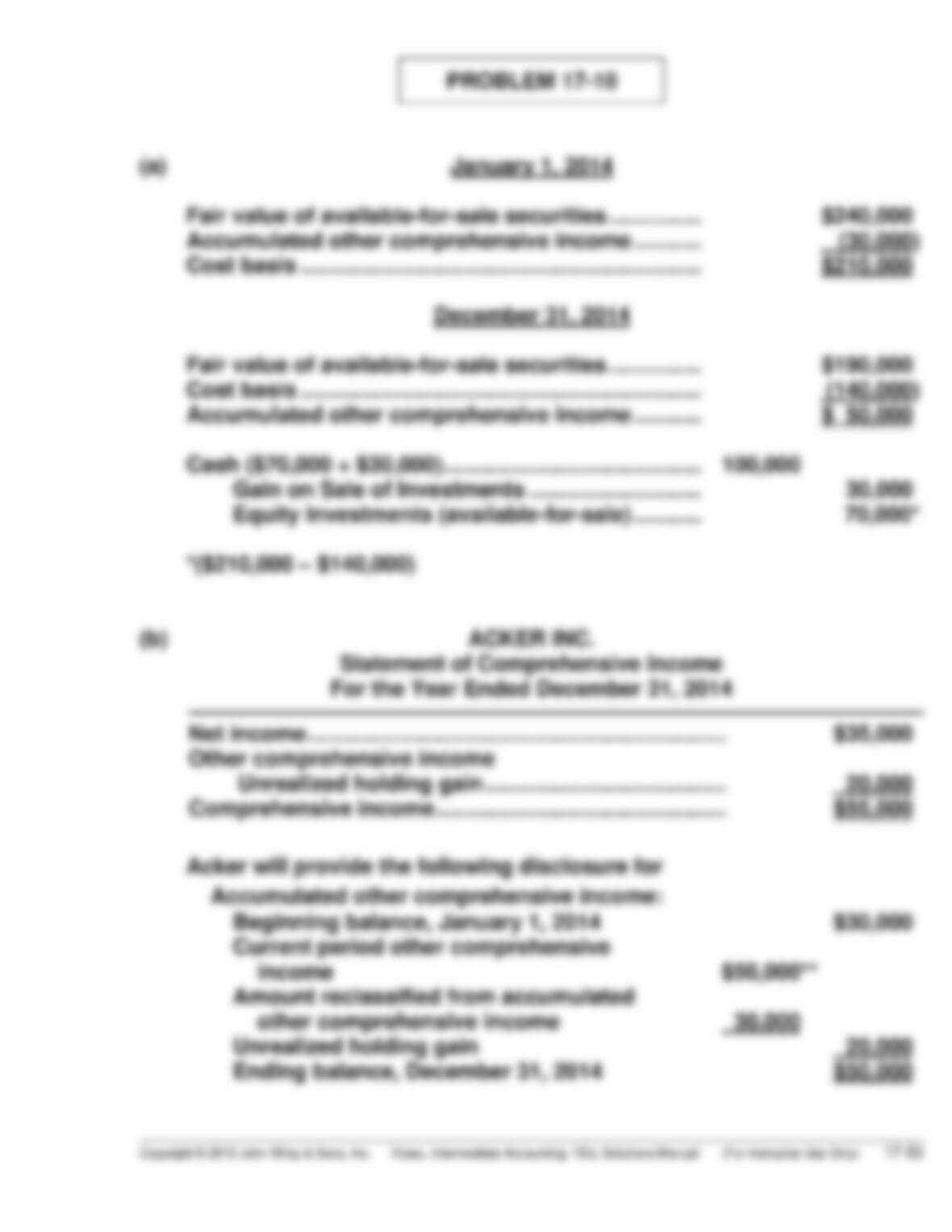

PROBLEM 17-10

(a) January 1, 2014

Fair value of available-for-sale securities …………… $240,000

Accumulated other comprehensive income ……….. (30,000)

Cost basis ……………………………………………………….. $210,000

December 31, 2014

Fair value of available-for-sale securities …………… $190,000

Cost basis ……………………………………………………….. (140,000)

Accumulated other comprehensive income ……….. $ 50,000

Cash ($70,000 + $30,000) …………………………………… 100,000

Gain on Sale of Investments ………………………. 30,000

Equity Investments (available-for-sale) ……….. 70,000*

*($210,000 – $140,000)

Accumulated other comprehensive income:

Beginning balance, January 1, 2014 $30,000

Current period other comprehensive

income $50,000**

Amount reclassified from accumulated

other comprehensive income 30,000

Unrealized holding gain 20,000

Ending balance, December 31, 2014 $50,000

17–54 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 17-10 (Continued)

**Accumulated other comprehensive

income 12/31/14 ………………………………………………. $50,000

Accumulated other comprehensive

income 1/1/14 ………………………………………………….. 30,000

Increase in unrealized holding gain…………………….. 20,000

Realized holding gain ………………………………………… 30,000

Total holding gains arising during period ……………. $50,000

Equity investments

(available-for-sale)

190,000

Retained earnings

Accumulated other

35,000

comprehensive income

50,000

Total assets

$345,000

Total equity

$345,000

*Beginning balance ……………………………………………………….. $ 50,000

Dividend revenue …………………………………………………………. 5,000

Cash proceeds on sale …………………………………………………. 100,000

$155,000

Assets

Cash

$155,000*

Common stock

$260,000

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–55

PROBLEM 17-11

(a)

1. 3/1/14 Cash ……………………………………………… 1,800

Dividend Revenue (900 X $2) ….. 1,800

2. 4/30/14 Cash ……………………………………………… 3,300

Gain on Sale of Investments ……… 600*

Equity Investments

(available-for-sale) …………………. 2,700

*(300 X ($11 – $9))

3. 5/15/14 Equity Investments (available-

for-sale) ………………………………………. 1,600

Cash (100 X $16) ………………………. 1,600

4. 12/31/14 Fair Value Adjustment (available-

for-sale) ………………………………………. 8,500

Unrealized Holding Gain

or Loss—Equity …………………….. 8,500

Chance Comp. ($4,500 – $2,700)

1,800

1,600(3)

(200)

Total of portfolio

$36,400

$37,400

$ 1,000

Previous fair value

adjustment bal.—Cr.

(7,500)

Fair value adjustment—Dr.

$ 8,500

[200 X ($8 – $9)] ……………………………… 200

Equity Investments

(available-for-sale) …………………. 1,800

6. 3/1/15 Cash ……………………………………………… 1,800

Dividend Revenue ……………………. 1,800

Security

Evers Comp. ($15,000 + $1,600)

$16,600

$ 2,100

Rogers Comp.

17–56 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 17-11 (Continued)

7. 12/21/15 Dividend Receivable ……………………… 3,300

Dividend Revenue (1,100 X $3) …. 3,300

8. 12/31/15 Fair Value Adjustment

(available-for-sale) ……………………… 4,200

Unrealized Holding Gain or

Loss—Equity ……………………….. 4,200

Security

Cost

Fair Value

Unrealized

Gain (Loss)

Evers Comp.

$16,600

$20,900(1)

$4,300

Rogers Comp.

18,000

18,900(2)

900

Total of portfolio

$34,600

$39,800

$5,200

Previous fair value

adjustment bal.—Dr.

1,000

Fair value adjustment—Dr.

$4,200

(1)(1,100 X $19) (2)(900 X $21)

Investments

Equity investments (available-

for-sale), at fair value

37,400

39,800

Stockholders’ equity

Accumulated other

comprehensive income

1,000

5,200

(b)

Partial Balance Sheet as of

Current Assets

Dividend receivable

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–57

PROBLEM 17-12

(a) Balance Sheet

Equity Investments (available-for-sale), at fair value ……… $123,000

(Reported as current or noncurrent based on intent)

Unrealized Holding Loss (available-for-sale) …………………. $ 4,000

($127,000 – $123,000) (reported as a separate

component of stockholders’ equity as a

deduction and identified as accumulated

other comprehensive loss)

Unrealized Holding Loss (available-for-sale) …………………. $42,000

($136,000 – $94,000) (reported as a separate

component of stockholders’ equity as a

deduction and identified as accumulated

other comprehensive loss)

Other Expenses and Losses

Loss on Sale of Investments ……………… $1,800*

*The entry made to recognize the loss on sale is as follows:

Cash …………………………………………………………… 38,200

Loss on Sale of Investments ………………………… 1,800

Equity Investments (available-for-sale) …. 40,000

17–58 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

PROBLEM 17-12 (Continued)

(c) Balance Sheet

Equity investments (available-for-sale), at fair value ………. $88,000

(Reported as current or noncurrent based on intent)

Unrealized holding gain (available-for-sale) …………………… $ 8,000

($88,000 – $80,000) (reported as a separate

component of stockholders’ equity as an

addition and identified as accumulated

other comprehensive gain)

The entry made to record the sale of Lindsay Jones’ stock was:

Cash ……………………………………………………….…….. 39,900

Loss on Sale of Investments …………………………... 8,100

Equity Investments (available-for-sale)

($15,000 + $33,000) ………………………………. 48,000

(2) Statement of Comprehensive Income

Unrealized holding loss ………………………….. $38,000*

*($42,000 – $4,000)

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 17–59

*PROBLEM 17-13

(a) July 7, 2014

Call Option …………………………………………………….. 240

Cash ………………………………………………………... 240

(b) September 30, 2014

Call Option …………………………………………………….. 1,400

Unrealized Holding Gain or Loss—Income

($7 X 200) ………………………………………………. 1,400

Unrealized Holding Gain or Loss—Income ……….. 60

Call Option ($240–$180) …………………………….. 60

(c) December 31, 2014

Unrealized Holding Gain or Loss—Income ……….. 400

Call Option ($2 X 200) ……………………………….. 400

Unrealized Holding Gain or Loss—Income ……….. 115

Call Option ($180 – $65) …………………………….. 115

Cash (200 X $6) ………………………………………………. 1,200

Loss on Settlement of Call Option …………………… 30

Call Option* ……………………………………………… 1,230

*Value of Call Option at Settlement:

Call Option

240

1,400

60

200

400

115

35

1,230

17–60 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

*PROBLEM 17-14

(a) July 7, 2014

Put Option ………………………………………………………. 240

Cash …………………………………………………………. 240

(b) September 30, 2014

Unrealized Holding Gain or Loss—Income ………… 115

Put Option ($240 – $125) …………………………….. 115

(c) December 31, 2014

Unrealized Holding Gain or Loss—Income ………… 75

Put Option ($125 – $50) ………………………………. 75

(d) January 31, 2015

Loss on Settlement of Put Option …………………….. 50

Put Option ($50 – $0) …………………………………. 50