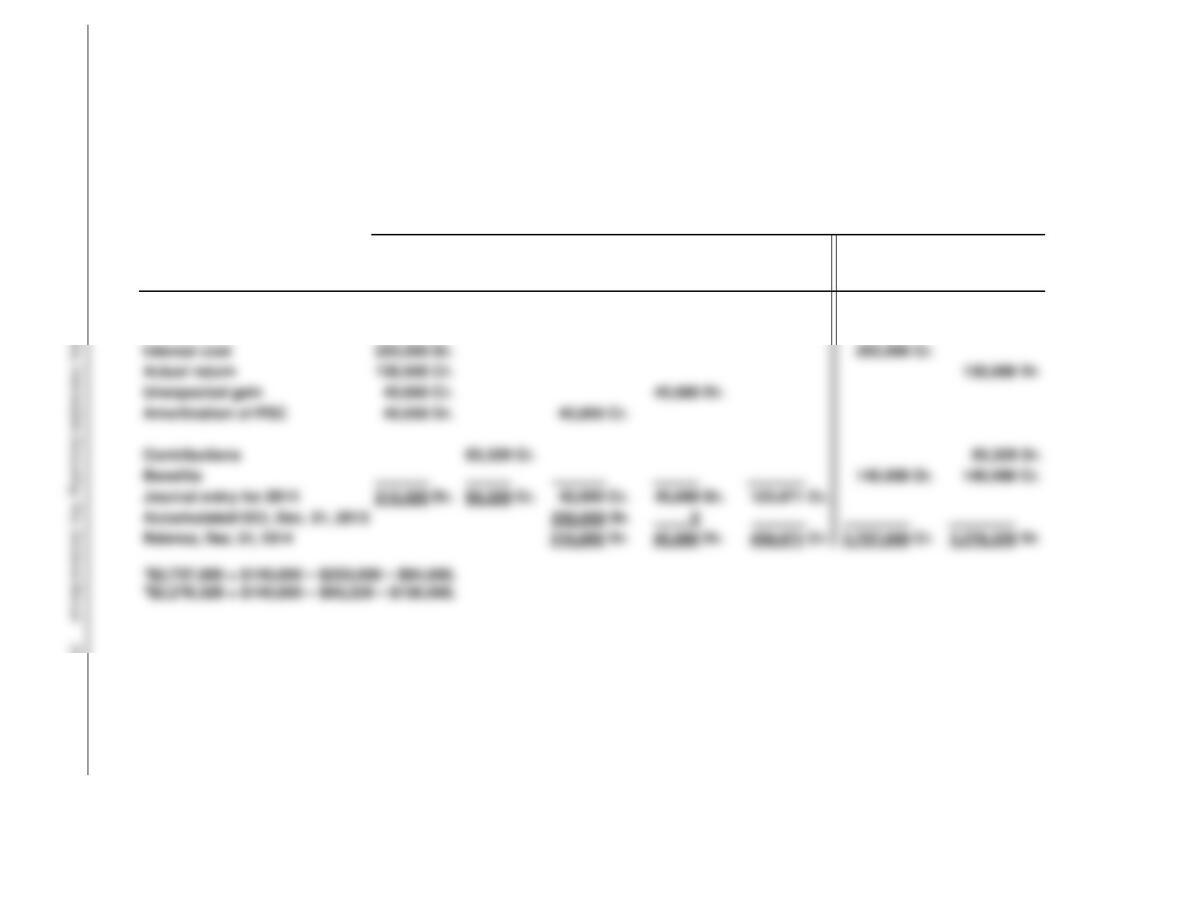

EXERCISE 20-9 (Continued)

(c) Accumulated OCI at December 31, 2014 is $255,680; this amount is

comprised of the following:

PSC

Gain/Loss

Balance Jan. 1, 2014*

$252,000 Dr.

$ 0

Amortization of PSC

Actuarial loss

Balance Dec. 31, 2014

$210,000 Dr.

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/

Liability

Projected

Benefit

Obligation

Plan Assets

Balance, Jan. 1, 2014

335,000 Cr.

2,530,000 Cr.1

2,195,000 Dr.2

Service cost

94,000 Dr.

94,000 Cr.

EXERCISE 20-9 (Continued)

20–22 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

Interest cost

253,000 Dr.

Actual return

130,000 Cr.

Unexpected gain

45,680 Cr.

Amortization of PSC

42,000 Dr.

Contributions

Journal entry for 2014

213,320 Dr.

Accumulated OCI, Dec. 31, 2013

252,000 Dr.

Balance, Dec. 31, 2014

210,000 Dr.

458,671 Cr.

EXERCISE 20-10 (20–25 minutes)

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 20–23

(a) WEBB CORP.

Pension Worksheet

General Journal Entries Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/

Liability

Projected

Benefit

Obligation

Plan Assets

Balance, Jan. 1, 2014

120,000 Cr.

600,000 Cr.

480,000 Dr.

Service cost

90,000 Dr.

90,000 Cr.

Interest cost*

54,000 Dr.

54,000 Cr.

Actual return

55,000 Cr.

55,000 Dr.

Unexpected gain**

Amortization of PSC

19,000 Dr.

Liability increase

76,000 Cr.

Contributions

Benefits

85,000 Dr.

85,000 Cr.

Journal entry for 2014

Accumulated OCI, Dec. 31, 2013

100,000 Dr

Balance, December 31, 2014

186,000 Cr.

735,000 Cr.

549,000 Dr.

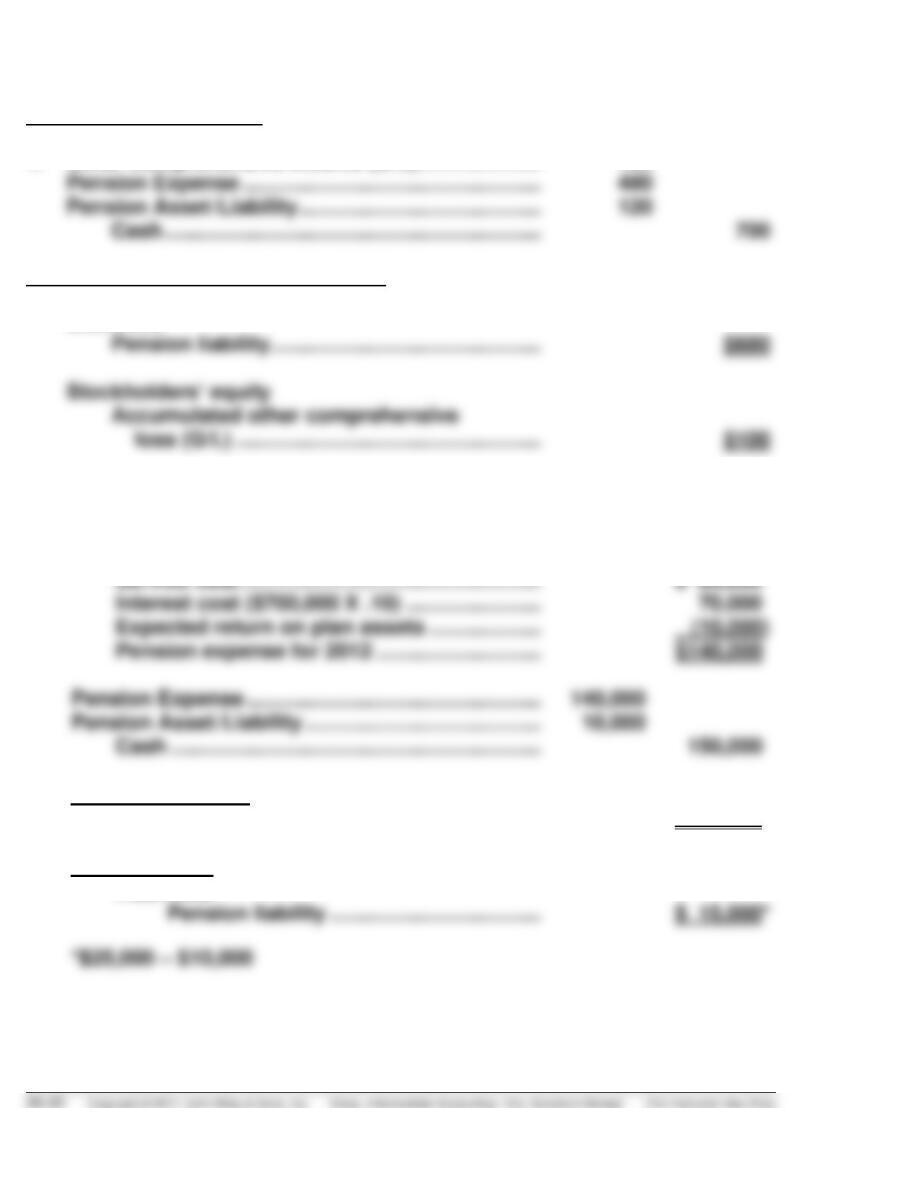

EXERCISE 20-11 (20–30 minutes)

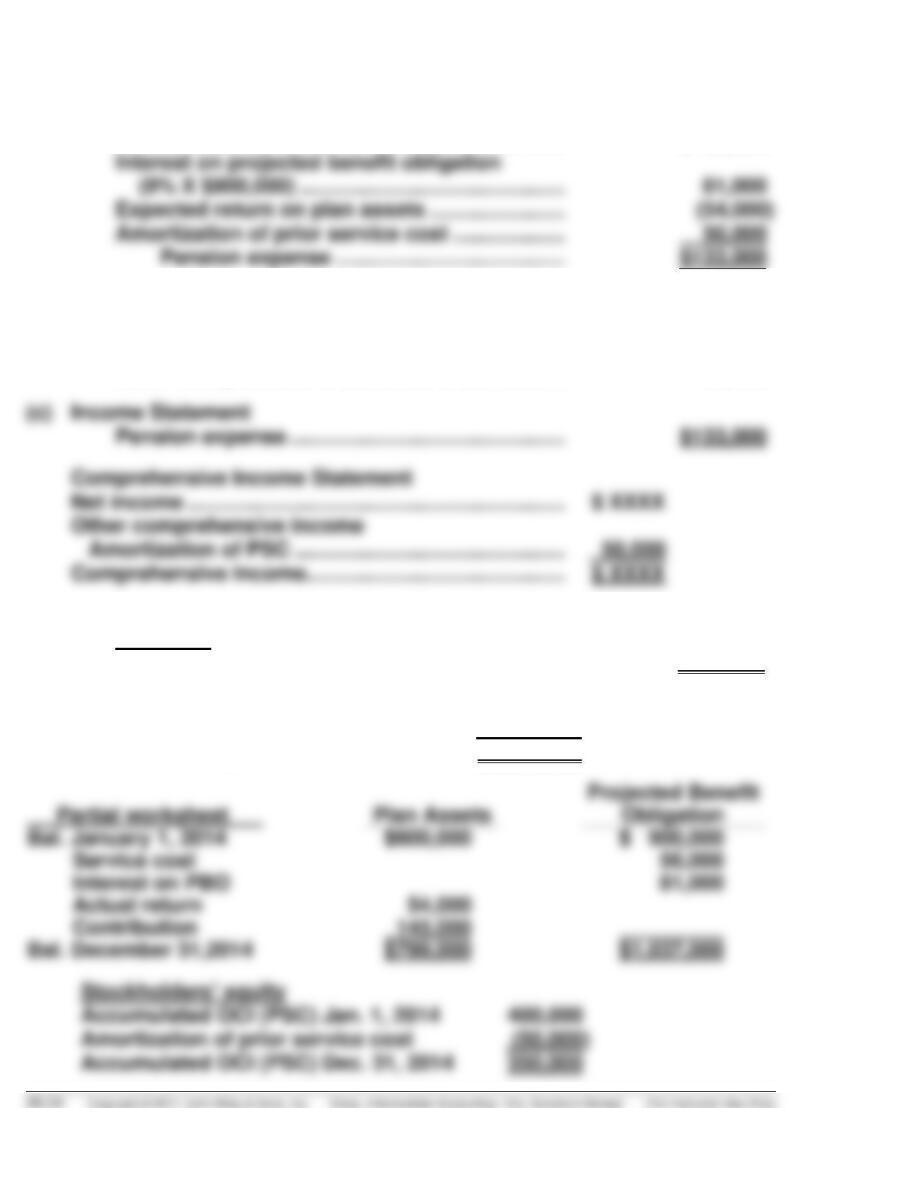

(a) Pension expense for 2014 composed of the following:

Service cost ………………………………………………. $ 56,000

(b) Pension Expense ……………………………………………… 133,000

Pension Asset /Liability …………………………………….. 62,000

Cash …………………………………………………………. 145,000

Other Comprehensive Income (PSC) …………… 50,000

Balance Sheet

Liabilities

Pension liability …………………………………………. $238,000*

*Projected benefit obligation $1,037,000

Plan assets (799,000)

Pension liability $ 238,000

EXERCISE 20-12 (20–30 minutes)

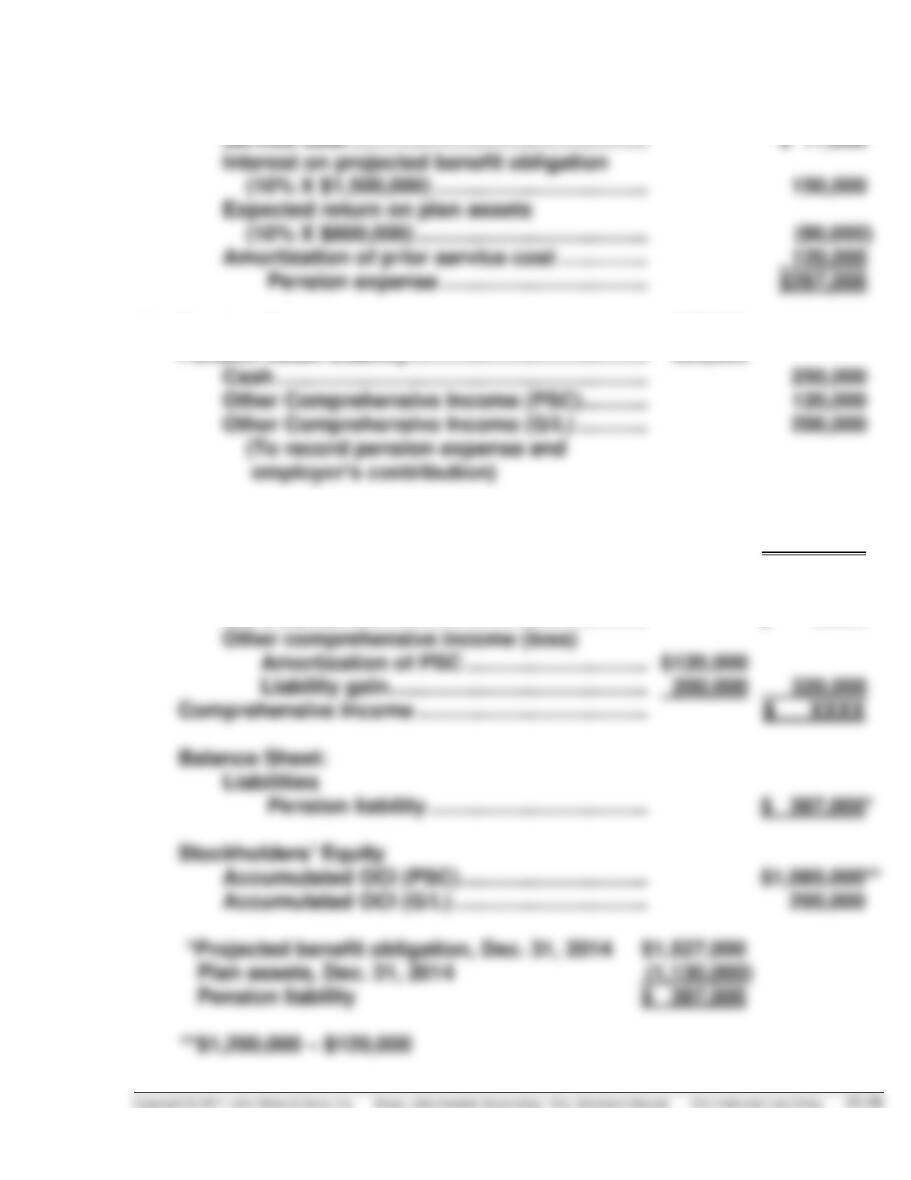

(a) Pension expense for 2014 composed of the following:

(b) Pension Expense ………………………………………….. 267,000

Pension Asset /Liability …………………………………. 303,000

(c) Income Statement:

Pension expense ……………………………………. $ 267,000

Comprehensive Income Statement

Net income …………………………………………….. $ XXXX

EXERCISE 20-12 (Continued)

20–26 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

Note to instructor: To prove the amounts reported, a worksheet might be prepared as follows:

General Journal Entries Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan Assets

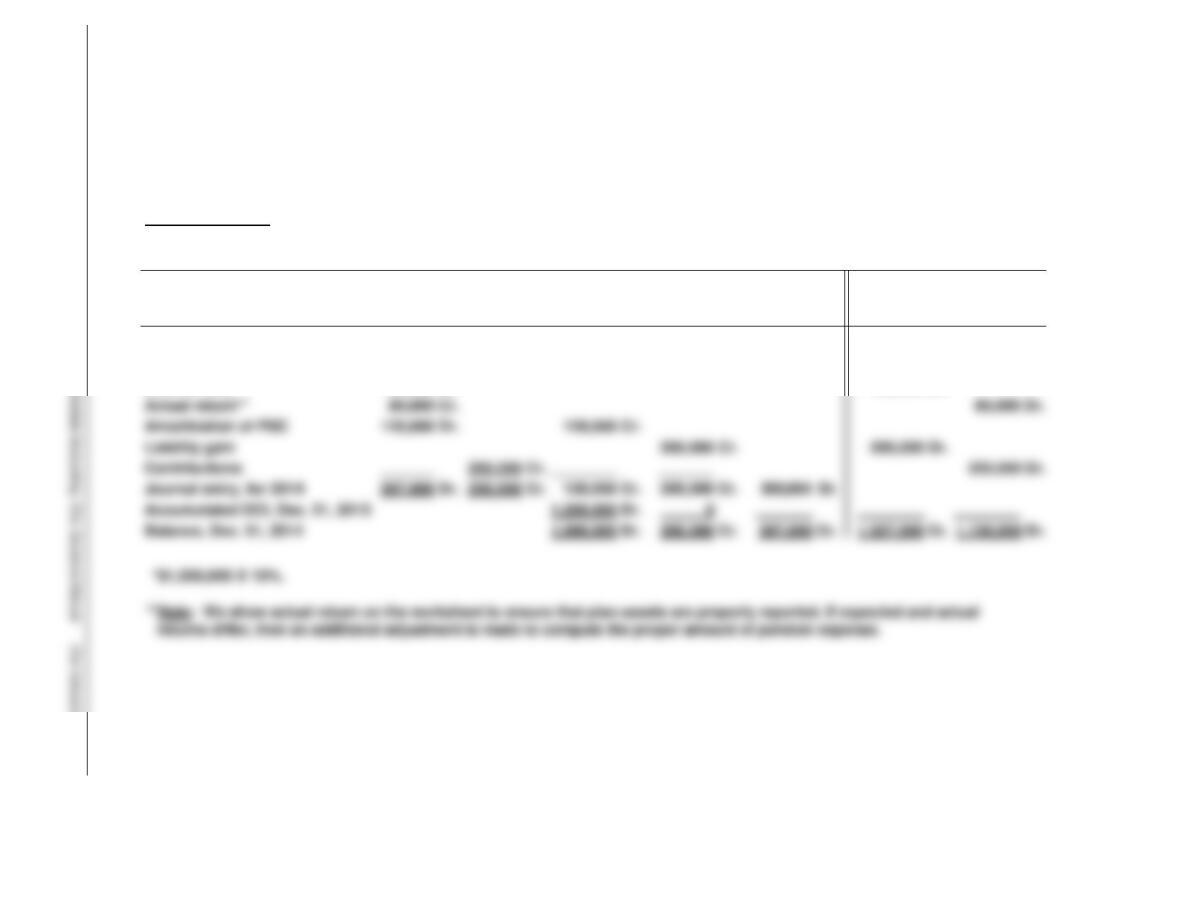

Balance, Jan. 1, 2014

700,000 Cr.

*1,500,000 Cr.

800,000 Dr.

Service cost

77,000 Dr.

77,000 Cr.

Interest cost*

150,000 Dr.

150,000 Cr.

Actual return**

80,000 Cr.

Amortization of PSC

120,000 Dr.

Liability gain

200,000 Dr.

Contributions

250,000 Dr.

Journal entry, for 2014

267,000 Dr.

Accumulated OCI, Dec. 31, 2013

1,200,000 Dr.

Balance, Dec. 31, 2014

1,080,000 Dr.

EXERCISE 20-13 (35–45 minutes)

(a) Actual Return = (Ending – Beginning fair value of assets) –

(Contributions – Benefits)

Fair value of plan assets,

(b) Computation of pension liability gains and losses and pension asset gains

and losses.

1. Difference between 12/31/14 actuarially computed PBO and 12/31/14

recorded projected benefit obligation (PBO):

2. Difference between actual fair value of

plan assets and expected fair value:

12/31/14 actual fair value

of plan assets ……………………….. 2,620

EXERCISE 20-13 (Continued)

Beginning-of-the-Year

Year

PBO

Plan

Assets (FV)

10%

Corridor

Accumulated

OCI (G/L)

Loss

Amortization

2014

$2,500

$1,700

$250

$240

–0–

(d) Pension expense for 2014:

Service cost ……………………………………………………….. $ 400

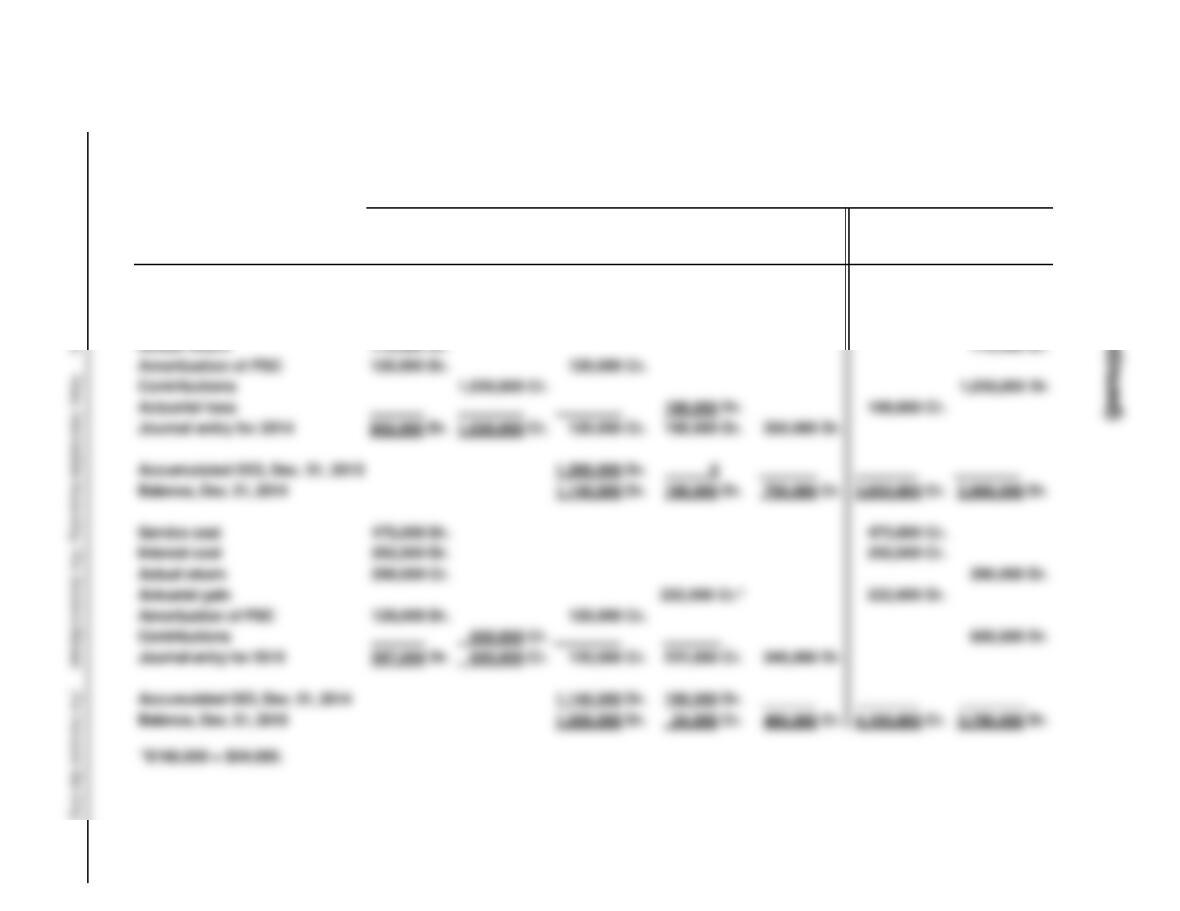

EXERCISE 20-14 (40–50 minutes)

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 20–29

ERICKSON COMPANY

Pension Worksheet—2014

General Journal Entries

Memo Record Entries

Items

Annual Pension

Expense

Cash

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

800 Cr.

2,500 Cr.

1,700 Dr.

Service cost

400 Dr.

400 Cr.

Interest cost(a)

250 Dr.

250 Cr.

Actual return(b)

420 Cr.

Unexpected gain(c)

250 Dr.

Contributions

700 Cr.

Benefits

200 Dr.

Liability increase(d)

350 Cr.

Journal entry for 2014

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

3,300 Cr.

EXERCISE 20-14 (Continued)

Journal entries 12/31/14

1. Other Comprehensive Income (G/L) ………………… 100

Balance Sheet at December 31, 2014

Liabilities

EXERCISE 20-15 (15–20 minutes)

(a) Computation of pension expense:

(b) Income Statement:

Pension expense …………………………..……….. $140,000

Balance Sheet:

Liabilities

General Journal Entries

Memo Record Entries

Annual Pension

Expense

Cash

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

25,000 Cr.

700,000 Cr.

675,000 Dr.*

Service cost

80,000 Dr.

80,000 Cr.

Interest cost

70,000 Dr.

70,000 Cr.

EXERCISE 20-15 (Continued)

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 20–31

Actual return

10,000 Cr.

Contributions

150,000 Dr.

Benefits

35,000 Dr.

Journal entry for 2014

Balance, Dec. 31, 2014

815,000 Cr.

800,000 Dr.

EXERCISE 20-16 (25–35 minutes)

The excess of the cumulative net gain or loss over the corridor amount is

amortized by dividing the excess by the average remaining service period of

employees. The average remaining service period is computed as follows:

Average remaining service life per employee =

5,600

400

= 14.

Amortization of Net (Gain) or Loss

(Gain) or Loss For the Year

Ended December 31,

Amount

2014

(300,000

2015

(480,000

2016

2017

Year

Projected

Benefit

Obligation (a)

Plan

Assets (a)

Corridor (b)

Accumulated

OCI (G/L) (a)

Minimum

Amortization

of (Gain) Loss

2014

$4,000,000

$2,400,000

$400,000

$ 0

$ 0

2015

4,520,000

2,200,000

452,000

300,000

0

2017

4,240,000

3,040,000

424,000

EXERCISE 20-17 (30–40 minutes)

(a)

Prior Service Cost

(b) The excess of the accumulated OCI (G/L) over the corridor amount is

amortized by dividing the excess by the average remaining service life

per employee. The average service life is 10.5 years.

Amortization of Net (Gain) or Loss

Year

Projected

Benefit

Obligation (a)

Plan

Assets(a)

10%

Corridor(b)

Accumulated

OCI (G/L)(a)

Minimum

Amortization

of (Gain) Loss

2014

$2,800,000

$1,700,000

$280,000

($ 0

$ –0–

2015

3,650,000

2,900,000

365,000

198,000

–0–(c)

(a) As of the beginning of the year.

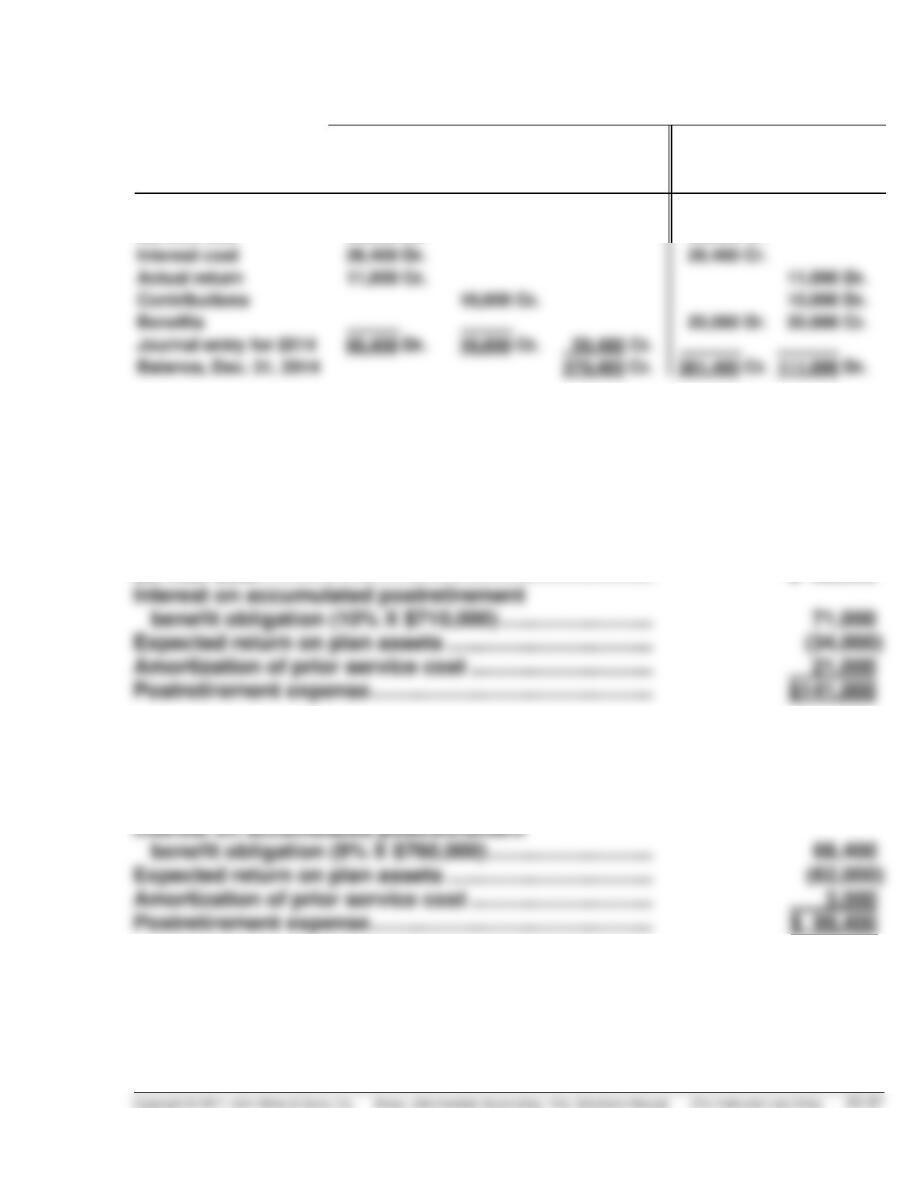

(c) Pension expense for 2014 is composed of the following:

Service cost ……………………………………………………….. $ 400,000

EXERCISE 20-17 (Continued)

Pension expense for 2015 is composed of the following:

Service cost ……………………………………………………….….. $475,000

Interest on projected benefit obligation

General Journal Entries Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—

Gain/Loss

Pension

Asset/

Liability

Projected

Benefit

Obligation

Plan Assets

Balance, Jan. 1, 2014

1,100,000 Cr.

2,800,000 Cr.

1,700,000 Dr.

Service cost

400,000 Dr.

400,000 Cr.

Interest cost

252,000 Dr.

252,000 Cr.

EXERCISE 20-17 (Continued)

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 20–35

Actual return

170,000 Cr.

Amortization of PSC

120,000 Dr.

Contributions

Actuarial loss

198,000 Cr.

Journal entry for 2014

602,000 Dr.

Accumulated OCI, Dec. 31, 2013

1,260,000 Dr.

Balance, Dec. 31, 2014

1,140,000 Dr.

Service cost

475,000 Dr.

475,000 Cr.

Interest cost

292,000 Dr.

292,000 Cr.

Actual return

290,000 Cr.

Actuarial gain

222,000 Dr.

Amortization of PSC

120,000 Dr.

Contributions

Journal entry for 2015

597,000 Dr.

Accumulated OCI, Dec. 31, 2014

1,140,000 Dr.

Balance, Dec. 31, 2015

1,020,000 Dr.

EXERCISE 20-18 (20–25 minutes)

(a) Below is the completed worksheet, indicating debit and credit entries.

General Journal Entries

Memo Record

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—Gain/

Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

1,100 Cr.

2,800 Cr.

1,700 Dr.

Service cost

500 Dr.

500 Cr.

Interest cost

280 Dr.

280 Cr.

Actual return

220 Cr.

Unexpected gain

150 Dr.

Amortization of PSC

55 Cr.

Contributions

Benefits

200 Dr.

Liability increase

365 Cr.

Accumulated OCI, Dec. 31, 2013

1,100 Dr.

0

Balance, Dec. 31, 2014

1,045 Dr.

1,225 Cr.

3,745 Cr.

2,520 Dr.

(b) Pension Expense …………………………..……… 765

Other Comprehensive Income (G/L) ………. 215

Pension Asset/Liability ……………………… 125

Cash ………………………………………………… 800

Other Comprehensive Income (PSC) ….. 55

(c) Usher records no amortization of gain or loss in 2014, because there were

*EXERCISE 20-19 (5–10 minutes)

Postretirement benefit expense is comprised of the following:

EXERCISE 20-20 (25–30 minutes)

General Journal Entries

Memo Record

Annual

Postretirement

Expense

Cash

Postretirement

Asset/Liability

APBO

Plan Assets

Balance, Jan. 1, 2014

220,000 Cr.

330,000 Cr.

110,000 Dr.

Service cost

45,000 Dr.

45,000 Cr.

Interest cost

26,400 Dr.

26,400 Cr.

Actual return

11,000 Cr.

11,000 Dr.

Contributions

10,000 Cr.

10,000 Dr.

Benefits

20,000 Dr.

20,000 Cr.

Journal entry for 2014

60,400 Dr.

10,000 Cr.

Postretirement Expense …………………………………. 60,400

Postretirement Asset/Liability ………………….. 50,400

Cash ………………………………………………………. 10,000

*EXERCISE 20-21 (10–12 minutes)

Service cost …………………………………………………………. $ 83,000

*EXERCISE 20-22 (10–12 minutes)

Service cost …………………………………………………………. $ 90,000

*EXERCISE 20-23 (15–20 minutes)

See worksheet on next page.

*EXERCISE 20-23 (15–20 minutes)

20–38 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

ENGLEHART CO.

Postretirement Benefit Worksheet—2014

General Journal Entries

Memo Record

Items

Annual

Postretirement

Expense

Cash

OCI—Prior

Service Cost

Postretirement

Asset/Liability

APBO

Plan

Assets

Balance, Jan. 1, 2014

50,000 Cr.

760,000 Cr.

710,000 Dr.

Service cost

90,000 Dr.

90,000 Cr.

Interest cost

68,400 Cr.

Actual return

62,000 Cr.

Contributions

56,000 Cr.

Benefits

40,000 Dr.

Amortization of PSC

3,000 Cr.

Journal entry for 2014

99,400 Dr.

56,000 Cr.

40,400 Cr.

Accumulated OCI, Dec. 31, 2013

100,000 Dr.

Balance, Dec. 31, 2014

90,400 Cr.

878,400 Cr.

788,000 Dr.

*EXERCISE 20-24 (25–30 minutes)

(a) Below is the completed worksheet, indicating debit and credit entries.

General Journal Entries

Memo Record Entries

Annual

Expense

Cash

Other

Comprehensive

Income—PSC

Postretirement

Asset/Liability

APBO

Plan

Assets

Balance, Jan. 1, 2014

290,000 Cr.

410,000 Cr.

120,000 Dr.

Service cost

56,000 Dr.

56,000 Cr.

Interest cost

36,900 Cr.

Actual/Expected return

Contributions

66,000 Dr.

Benefits

Amortization of PSC

Accumulated OCI, Dec. 31, 2013

30,000 Dr.

Balance, Dec. 31, 2014

27,000 Dr.

314,900 Cr.

497,900 Cr.

183,000 Dr.

TIME AND PURPOSE OF PROBLEMS

Problem 20-1 (Time 40–50 minutes)

Purpose—to provide a problem that requires preparation of a pension worksheet for two separate

years’ pension transactions. Included in the problem are an unexpected loss and prior service cost

amortization.

Problem 20-2 (Time 45–55 minutes)

Problem 20-3 (Time 40–50 minutes)

Problem 20-4 (Time 30–40 minutes)

Problem 20-5 (Time 45–55 minutes)

Problem 20-6 (Time 45–60 minutes)

Purpose—to provide a problem that requires computation and amortization of prior service cost,

computation of pension expense, and preparation of pension journal entries.

Problem 20-8 (Time 45–60 minutes)

Problem 20-9 (Time 40–45 minutes)

Purpose—to provide a problem that requires preparation of a worksheet for two years, journal entries,

and indicates financial statement presentation.

Problem 20-10 (Time 25–30 minutes)

Purpose—to provide a problem to understand elements of a pension worksheet.

Problem 20-11 (Time 35–45 minutes)