E18–17B (15–25 minutes)

(a) Computation of gross profit to be recognized under completed-contract

method:

No computation necessary. No gross profit to be recognized prior to

completion of contract.

E18–18B (15–25 minutes)

BEARING CONSTRUCTION COMPANY

Income Statement (partial)

Year Ended December 31, 2014

_________________________________________________________________

E18-19B (15–20 minutes)

(a) Computation of gross profit recognized:

2014

2015

$70,000 X 15%*

$10,500

$201,000 X 15%*

$30,150

$10,500

$56,070

E18–20B (15–20 minutes)

(a) Deferred Gross Profit—2012 ……………………… 34,700*

Deferred Gross Profit—2013 ……………………… 49,400**

Deferred Gross Profit—2014 ……………………… 30,000***

Realized Gross Profit …………………………. 114,100

E18–21B (15–20 minutes)

Gross profit ratio—2014: ($600,000 – $480,000) ÷ $600,000 = 20%

Gross profit ratio—2015: ($530,000 – $442,800) ÷ $530,000 = 18%

(a) Balance, December 31, 2014:

Deferred Gross Profit Account—2014 Installment Sales

E18–224B (10–15 minutes)

UPPER WORLD CORPORATION

Income before Income Taxes on Installment-Sale Contract

For the Year Ended December 31, 2014

E18–23B (10–15 minutes)

(a) Realized gross profit recognized in 2015 under the installment method of

16.67% respectively.

2015

2015

E18–23B (Continued)

2. as a deferred credit between liabilities and stockholders’ equity. This

treatment is criticized because there is no obligation to outsiders; or

3. as an adjustment or offset to the related Installment Accounts

Receivable. This is because the deferred gross profit is a part of

revenue from installment sales not yet realized. The related receivable

will be overstated unless the deferred gross profit is deducted. On the

E18–24B (15–20 minutes)

(a) Computation of gross profit realized—cost recovery method:

Cash

Original

Cost

Balance of

Unrecovered

Gross

Profit

E18–25B (10–15 minutes)

1. Repossessed Merchandise ………………………………….. 475

Deferred Gross Profit …………………………………………… 720*

Loss on Repossession ………………………………………… 605

2. Repossessed Merchandise …………………………………… 850

Deferred Gross Profit …………………………………………… 676*

Installment Accounts Receivable ……………………. 1,280**

E18–26B (15–20 minutes)

Cash ……………………………………………………………………………. 700

Installment Accounts Receivable ……………………………. 700

(To record the collection of cash on installment

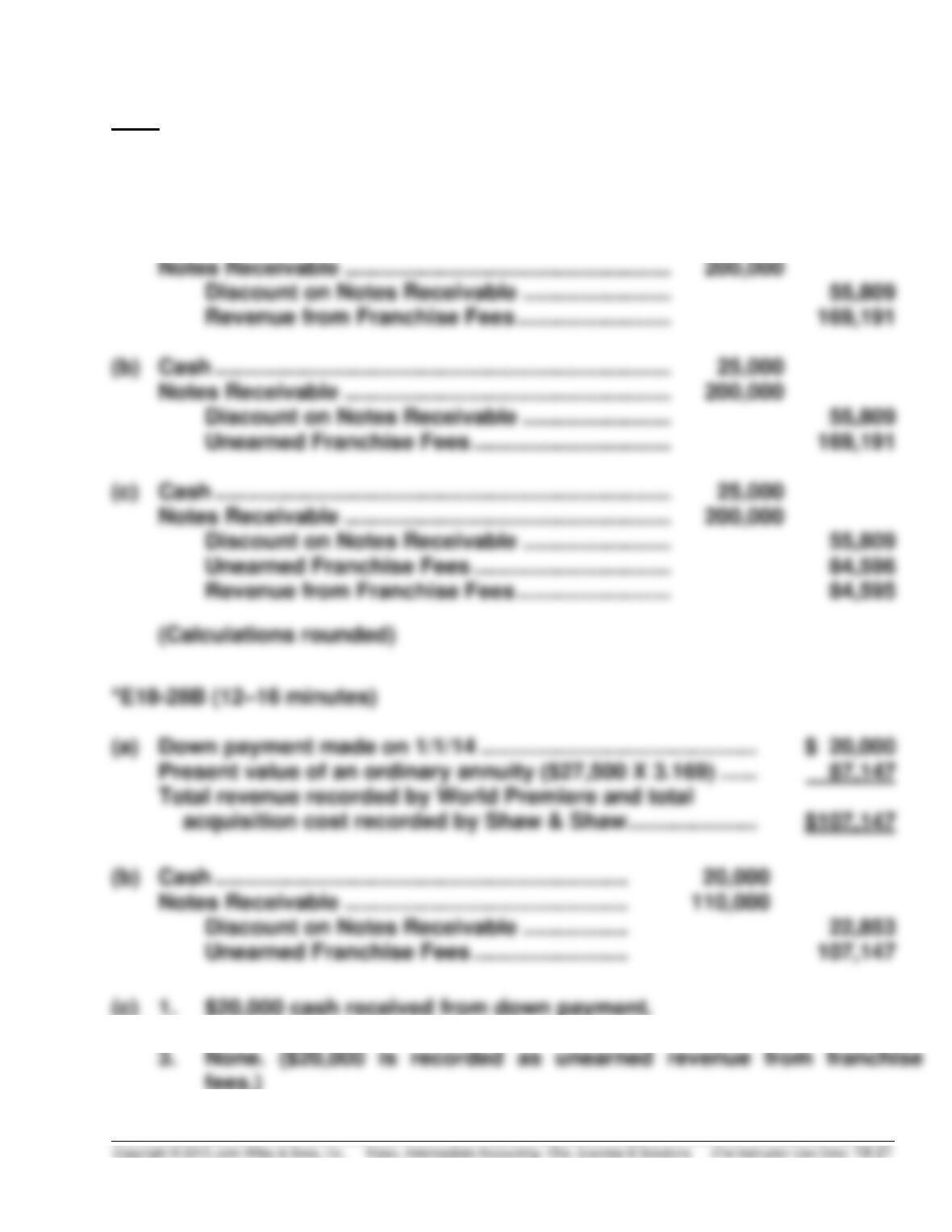

*E18-27B (14–18 minutes)

Note: For each part below, the present value of the notes receivable is

$141,191, calculated as follows:

$40,000 X 3.60478 (ordinary and 5 payments, 12%)

(a) Cash ……………………………………………………………….. 25,000

2. $20,000 cash received from down payment.