CHAPTER 23

SOLUTIONS TO B EXERCISES

E23-1B (10–15 minutes)

(a) (3) Investing activity.

(b) (4) Financing activity.

(c) (3) Investing activity.

E23-2B (20–30 minutes)

(a)

Shown in the financing activities section of a statement of cash flows

E23-2B (Continued)

(c)

Plant assets (cost) …………………………………………………..

$70,000)

Accumulated depreciation [($60,000 ÷ 6) X 2] ……………

20,000)

Book value at date of sale ……………………………………….

50,000)

Sale proceeds …………………………………………………………

(25,000)

(d) The goodwill impairment is reported in the operating activities section of

the statement of cash flows. It is added to net income in arriving at net

cash provided by operating activities.

(e) The warranty payments affect the accrued warranty expense liability.

(f) The sale of the U.S. Treasury bill is not reported in the statement of cash

flows. This instrument is considered a cash equivalent and therefore

cash and cash equivalents have not changed as a result of this

transaction.

Noncash investing and financing activities

Purchase of land by issuance

of bonds ………………………………………………………

E23-2B (Continued)

(h) The net income of $176,000 should be reported in the operating activities

section of the statement of cash flows. Depreciation of $69,000 is

reported in the operating activities section of the statement of cash flows.

The loss on sale of the equity investment also appears in the operating

E23-3B (15–25 minutes)

GUESSER COMPANY

Statement of Cash Flows (partial)

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income ………………………………………………………

$ 71,000

Adjustments to reconcile net income

Depreciation expense ………………………………..

Decrease in accounts receivable ………………..

Increase in inventory …………………………………

Increase in prepaid expenses …………………….

Increase in accounts payable …………………….

E23-4B (20–30 minutes)

GUESSER COMPANY

Statement of Cash Flows (partial)

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers ………….

$818,000

(a)

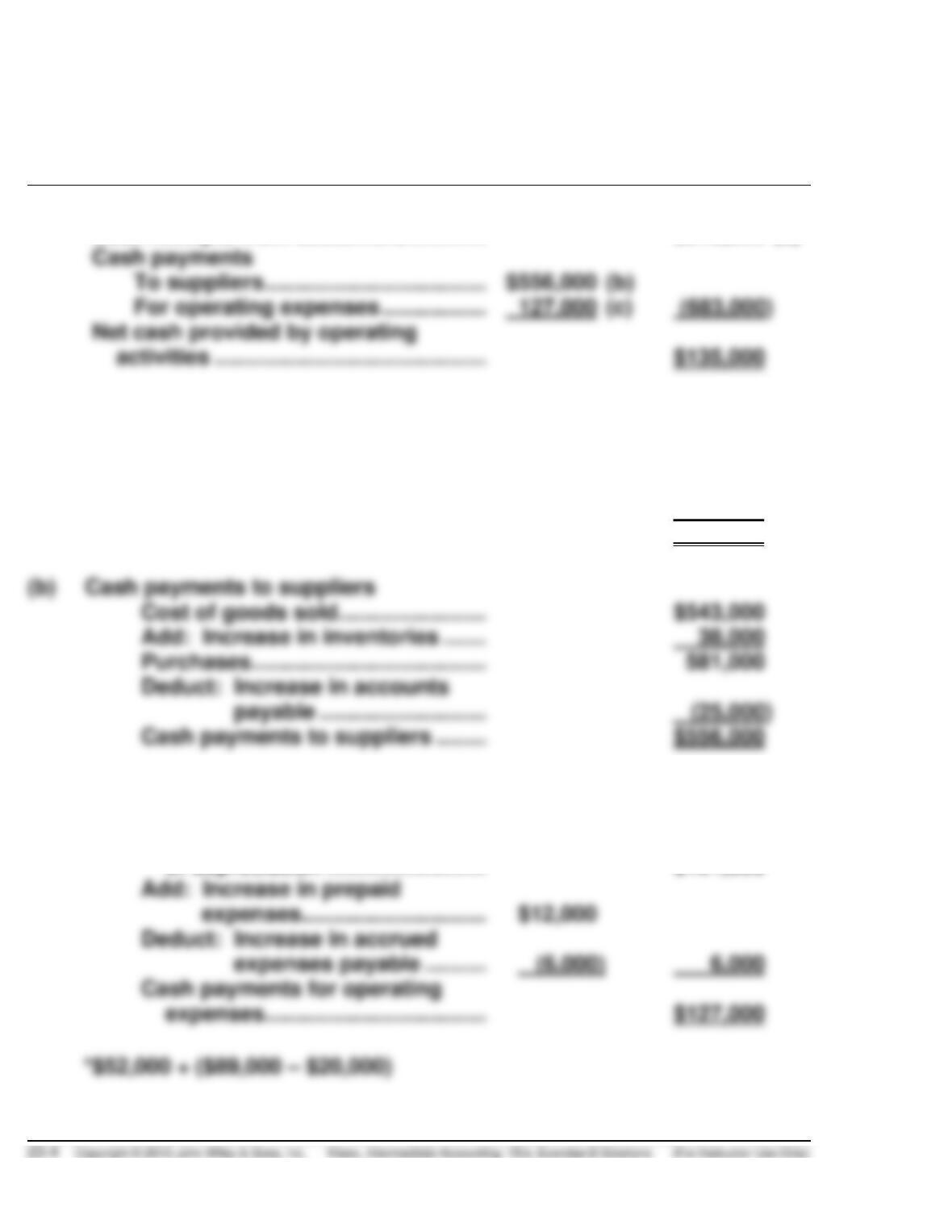

Cash payments

To suppliers ………………………………

(b)

For operating expenses ……………..

(c)

(683,000)

Net cash provided by operating

activities ……………………………………..

$135,000

Computations:

(a)

Cash receipts from customers

Sales ……………………………………….

$755,000

Add: Decrease in accounts

receivable ……………………….

63,000

Cash receipts from customers …..

$818,000

(b)

Cash payments to suppliers

Cost of goods sold ……………………

$543,000

Add: Increase in inventories …….

38,000

Purchases ………………………………..

Deduct: Increase in accounts

payable ………………………

(25,000)

Cash payments to suppliers ……..

$556,000

(c)

Cash payments for operating

expenses

Operating expenses, exclusive

of depreciation ……………………..

$121,000*

Add: Increase in prepaid

expenses …………………………

Deduct: Increase in accrued

expenses payable ……….

6,000

Cash payments for operating

expenses………………………………

$127,000

E23-5B (20–30 minutes)

KRAYON COMPANY

Statement of Cash Flows (partial)

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers ……..

$1,554,000

(a)

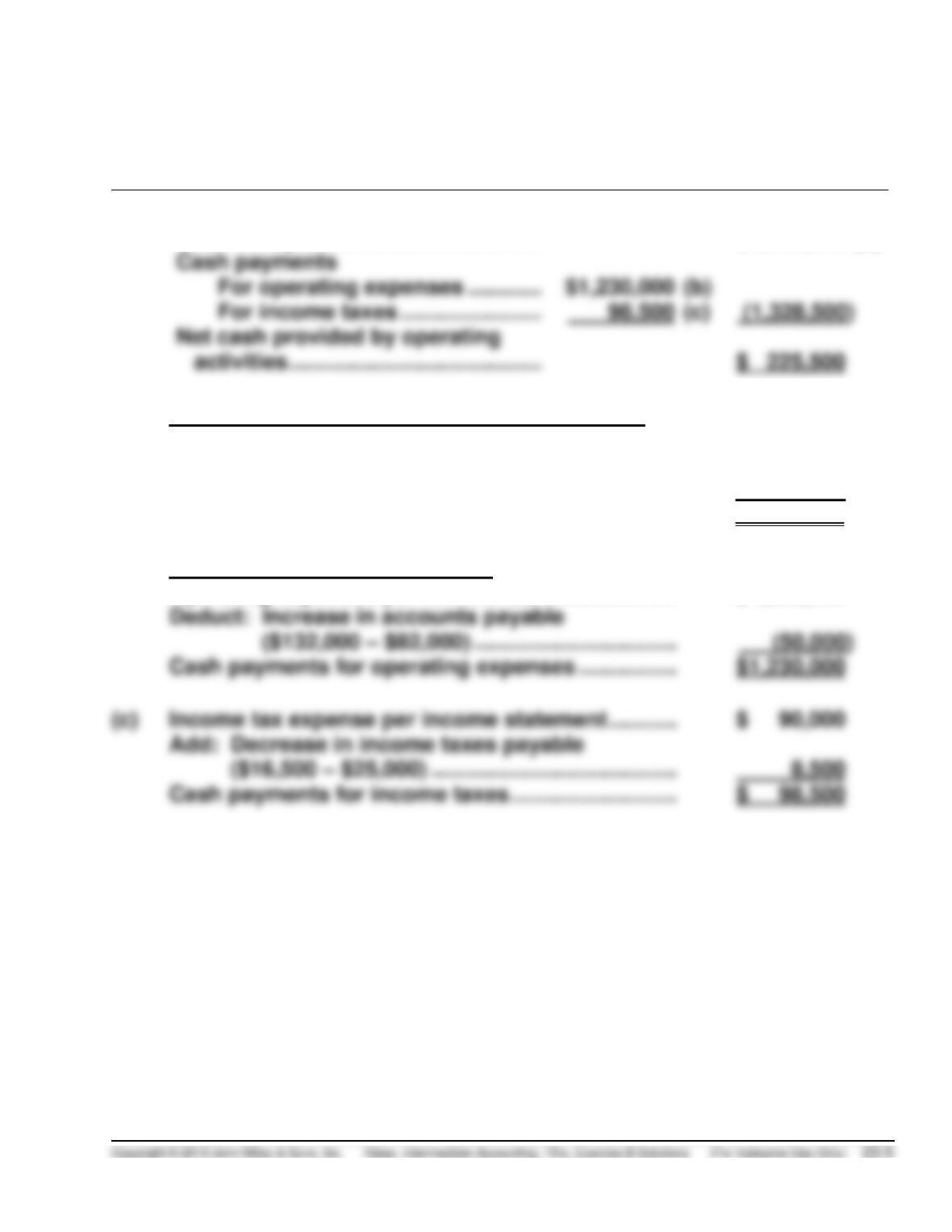

Cash payments

For operating expenses …………

(b)

For income taxes …………………..

(c)

Net cash provided by operating

activities …………………………………..

$ 225,500

(a)

Computation of cash receipts from customers:

Revenue from fees

$1,604,000

Deduct: Increase in accounts receivable

Add: ($169,000 – $119,000) …………………………..

(50,000)

Cash receipts from customers ………………………….

$1,554,000

(b)

Computation of cash payments:

Operating expenses per income statement ………..

$1,280,000

Deduct: Increase in accounts payable

Cash payments for operating expenses …………….

$1,230,000

(c)

Income tax expense per income statement ………..

$ 90,000

Add: Decrease in income taxes payable

Add ($16,500 – $25,000) ………………………………….

8,500

Cash payments for income taxes ………………………

$ 98,500

E23-6B (15–20 minutes)

KRAYON COMPANY

Statement of Cash Flows (partial)

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income …………………………………………………….

$130,000

Adjustment to reconcile net income

to net cash provided by operating activities:

Depreciation expense ……………………………….

Gain on sale of equipment …………………………

Increase in accounts receivable …………………

Increase in accounts payable …………………….

Decrease in income taxes payable ……………..

95,500

E23-7B (15–20 minutes)

Situation A:

Cash flows from operating activities

($1,950,000 – $321,000) ……………………………..

Cash receipts from customers

Situation B:

(a)

Computation of cash payments to suppliers

Cost of goods sold ………………………………..

$940,000

Deduct: Decrease in inventory ………………

(96,900)

Increase in accounts payable…………

(64,900)

Operating expenses ………………………………

$523,000

Deduct: Decrease in prepaid expenses ….

(12,000)

Increase in accrued expenses

payable …………………………..………..

(25,000)

E23-8B (20–30 minutes)

Cash flows from operating activities

Net income ………………………………………………….

$540,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Increase in warranty accrual ………………….

Other comments:

No. 1 is shown as a cash outflow in the financing section.

No. 3 is shown as a cash inflow in the financing section.

E23-9B (20–30 minutes)

(a)

Sales (revenues) ………………………………………………..

$2,105,800

Add: Net decrease in accounts receivable

($270,000 – $9,600) – ($298,000 – $8,100) …….

29,500

Cash collected from customers…………………………..

$2,135,300

(b)

Cost of goods sold …………………………………………….

$1,205,000

Add: Increase in inventory ($187,000 – $171,000) …

16,000

Purchases ………………………………………………………...

E23-9B (Continued)

(c)

Interest expense

$ 8,500

Add: Decrease in unamortized bond

premium ($5,000 – $4,500) ……………………

500

Cash paid for interest ………………………………….

$ 9,000

(d)

Income tax expense …………………………………….

$170,300

Deduct: Increase in income taxes payable

Deduct: Increase in deferred tax liability

(8,600)

Cash paid for income taxes ………………………….

$149,300

(e)

General and administrative expenses …………..

$285,000

Deduct: Depreciation expense

Deduct: Bad debts expense …………………………

Cash paid for general and admin. expenses ….

$267,250

E23-10B (25–35 minutes)

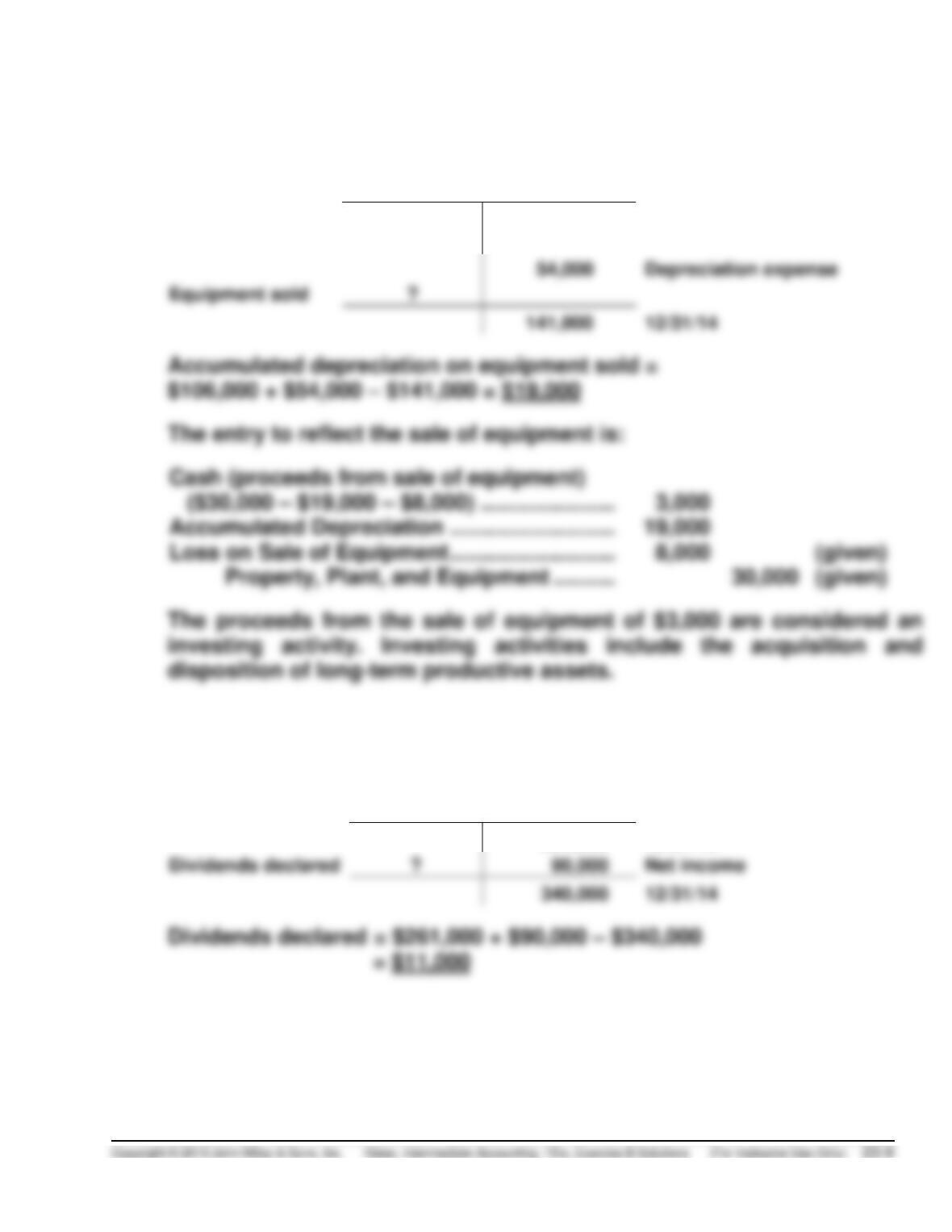

(a) The solutions approach is to prepare a T-account for property, plant, and

equipment.

E23-10B (Continued)

(b) The solutions approach is to set up a T-account for accumulated

depreciation.

Accumulated Depreciation

106,000

12/31/13

Depreciation expense

Equipment sold

141,000

12/31/14

(c) The cash dividends paid can be determined by analyzing T-accounts for

retained earnings and dividends payable.

Retained Earnings

261,000

12/31/13

Dividends declared

Net income

340,000

12/31/14

E23-10B (Continued)

Dividends payable

10,000

12/31/13

11,000

Dividends declared

Cash dividends paid

?

0

12/31/14

(d) The redemption of bonds payable amount is determined by setting up a

T-account.

Bonds Payable

100,000

12/31/13

Bond conversion

12/31/14

E23-11B (30–35 minutes)

FULTON CORP.

Statement of Cash Flows

For the Year Ended December 31, 2014

(Indirect Method)

Cash flows from operating activities

Net income …………………………………………………………….

$2,145

Adjustments to reconcile by operating activities:

Depreciation expenses ($600 – $455) ………………..

$145

Loss on sale of investments …………………………….

Increase in receivables ……………………………………

Increase in inventory ……………………………………….

Decrease in accounts payable………………………….

Decrease in accrued liabilities………………………….

Net cash provided by operating activities ………………..

Cash flows from investing activities

Sale of investments

[$200 – $50] ……………………………………………………….

150

Net cash used by investing activities ………………………

Cash flows from financing activities

Retirement of bonds payable ………………………………….

Payment of cash dividends …………………………………….

Net cash used by financing activities ……………………..

(800)

Net increase in cash ………………………………………………………

Cash, January 1, 2014 ……………………………………………………

Noncash investing and financing activities

Issuance of common stock for land ………………………..

$100