CHAPTER 8

SOLUTIONS TO B EXERCISES

E8-1B (15–20 minutes)

Items 6, 7, 8, 9, 11, 13, 14, 17, and 18 would be reported as inventory in the

financial statements.

The following items would not be reported as inventory:

1. Cost of goods sold in the income statement.

2. Short-term investments in the current asset section of the balance sheet.

3. Office supplies in the current assets section of the balance sheet.

E8-2B (10–15 minutes)

Inventory per physical count ………………………………………..

$200,000

Goods in transit to customer, f.o.b. destination ……………..

+ 25,000

The consigned goods of $20,000 are not owned by the company and were

properly excluded.

E8-3B (10–15 minutes)

1. Include. Merchandise passes to customer only when it is shipped.

2. Do not include. Title did not pass until January 3.

E8-4B (10–15 minutes)

1.

Raw Materials Inventory ………………………………………….

40,500

Accounts Payable …………………………………………..

40,500

2.

Raw Materials Inventory ………………………………………….

140,000

Accounts Payable …………………………………………..

140,000

3.

No adjustment necessary.

4.

Accounts Payable …………………………………………………..

38,000

Raw Materials Inventory ………………………………….

38,000

5.

Raw Materials Inventory ………………………………………….

95,000

Accounts Payable …………………………………………..

95,000

E8-5B (15–20 minutes)

(a)

Inventory December 31, 2014 (unadjusted) ……………..

$561,810

Transaction 2 ………………………………………………………..

–0–

Transaction 3 ………………………………………………………..

–0–

Transaction 4 ………………………………………………………..

–0–

Transaction 5 ………………………………………………………..

Transaction 6 ………………………………………………………..

Transaction 7 ………………………………………………………..

Transaction 8 ………………………………………………………..

600

(b)

Transaction 2

Accounts Payable ……………………………………

21,500

Purchases ………………………………………………………..

21,500

(To reverse purchase entry in 2014)

Transaction 3

Sales …………………………..………………………….

Accounts Receivable ………………………………………..

(To reverse sale entry in 2014)

Transaction 4

Purchases ………………………………………………

12,610

Accounts Payable ……………………………………………..

12,610

(To record purchase of

merchandise in 2014)

Transaction 8

Sales Returns and Allowances …………………

Accounts Receivable ………………………

E8-6B (10–20 minutes)

2013

2014

2015

Sales

$217,500

$270,000

$307,500

Sales returns

8,250

9,750

15,000

Net sales

209,250

260,250

292,500

Beginning inventory

Ending inventory

33,000

Purchases

181,500

195,000

223,500

Purchase returns and allowances

3,750

6,000

6,000

6,750

Cost of good sold

174,750

192,000

219,750

Gross profit

72,750

E8-7B (10–15 minutes)

(a)

May 10

Purchases ………………………………………………………………

19,600

Accounts Payable

($20,000 X .98) ……………………………………………..

19,600

May 11

Purchases ………………………………………………………………

18,018

Accounts Payable

($18,200 X .99) ……………………………………………..

May 19

Accounts Payable …………………………………………………..

Cash ………………………………………………………………

May 24

Purchases ………………………………………………………………

Accounts Payable

(b)

May 31

Purchase Discounts Lost ………………………………………..

182

Accounts Payable

($18,200 X .01) ……………………………………………..

182

(Discount lost on purchase

of May 11, $18,200, terms

1/15, n/30)

E8-8B (10 minutes)

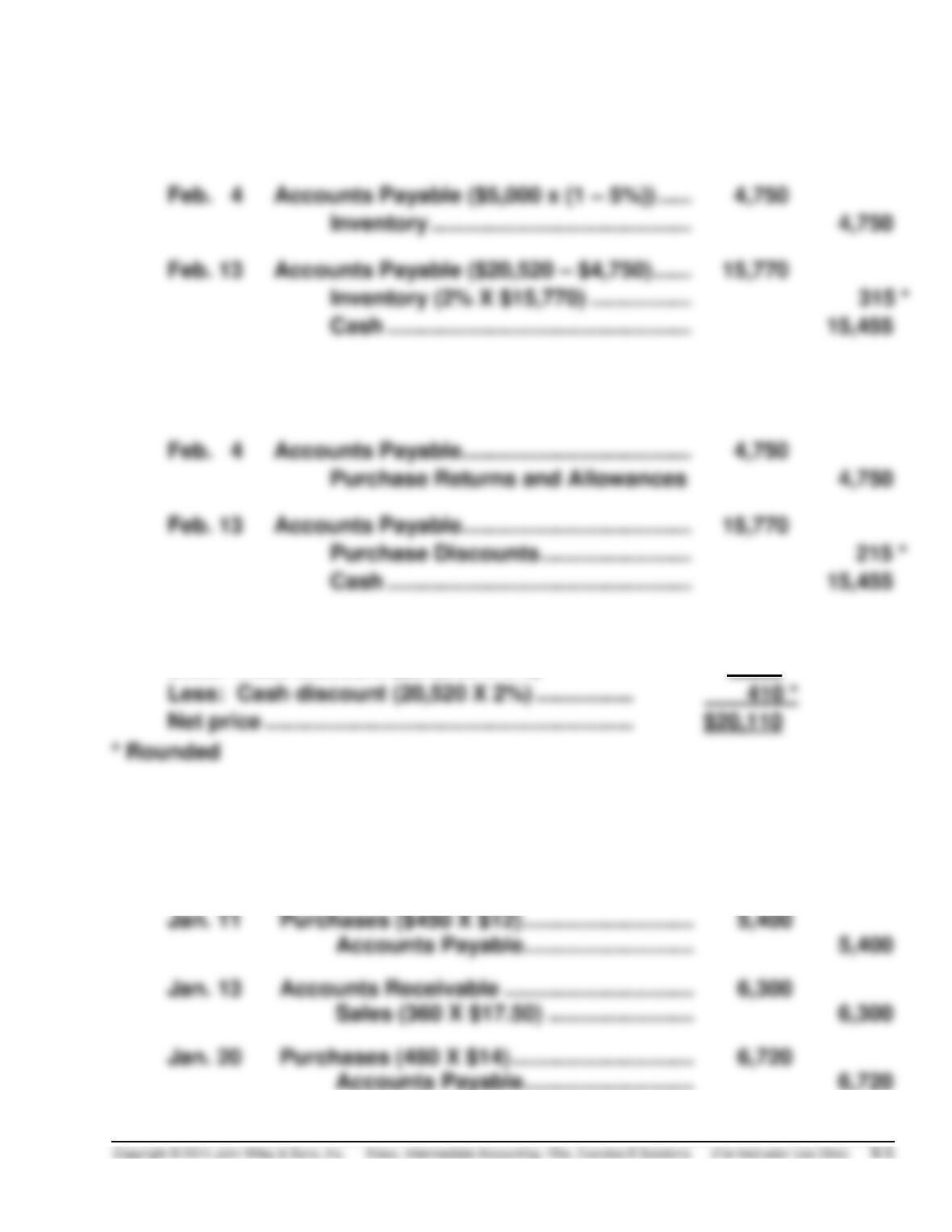

(a)

Feb. 1

Inventory ($21,600 x (1 – 5%)) …………………………………..

20,520

Accounts Payable …………………………………………..

20,520

Feb. 4

Accounts Payable ($5,000 x (1 – 5%)) ……………………….

Inventory ………………………………………………………..

Feb. 13

Accounts Payable ($20,520 – $4,750) ………………………..

15,770

Inventory (2% X $15,770) …………………………………

Cash ………………………………………………………………

15,455

(b)

Feb. 1

Purchases ………………………………………………………………

20,520

Accounts Payable …………………………………………..

20,520

Feb. 4

Accounts Payable……………………………………………………

Feb. 13

Accounts Payable……………………………………………………

15,770

Purchase Discounts ………………………….. $7,470)

Cash ………………………………………………………………

15,455

(c)

Purchase price (list) …………………………………..

$21,600

Less: Trade discount ($21,600 x 5%)

1,080

Less: Cash discount (20,520 X 2%) …………….

E8-9B (15–25 minutes)

(a)

Jan. 4

Accounts Receivable ………………………………………………

3,840

Sales (240 X $16) …………………………..………………..

3,840

Accounts Payable……………………………………………

5,400

Jan. 13

Accounts Receivable ………………………………………………

6,300

Jan. 20

Purchases (480 X $14) ……………………………………………..

6,720

Accounts Payable……………………………………………

6,720

E8-9B (Continued)

Jan. 27

Accounts Receivable ………………………………………………

5,400

Sales (300 X $18) …………………………………………….

5,400

Jan. 31

Inventory ($14 X 330) ………………………………………………

Cost of Goods Sold …………………………………………………

Purchases ($5,400 + $6,720) …………………………….

Inventory (300 X $10) ………………………………………

(c)

Jan. 4

Accounts Receivable ………………………………………………

3,840

Sales ………………………………………………………………..

3,840

Cost of Goods Sold …………………………………………………

2,400

Inventory (240 X $10) …………………………………………

2,400

Jan. 11

Inventory ………………………………………………………………..

5,400

Accounts Payable ……………………………………………..

5,400

Jan. 13

Accounts Receivable ………………………………………………

6,300

Sales ………………………………………………………………..

6,300

Cost of Goods Sold …………………………………………………

4,200

Inventory [(60 X $10) + (300 X $12)] ………………………..

4,200

Jan. 20

Inventory ………………………………………………………………..

6,720

Accounts Payable ……………………………………………..

6,720

Jan. 27

Accounts Receivable ………………………………………………

5,400

Sales ………………………………………………………………..

5,400

Cost of Goods Sold …………………………………………………

3,900

Inventory [(150 X $12) + (150 X $14)] ………………………

3,900

(d) Sales ………………………………………………………………… $15,540

Cost of goods sold

($2,400 + $4,200 + $3,900) ……………………………… 10,500

Gross profit ………………………………………………………. $ 5,040

E8-10B (10–15 minutes)

2014

2015

1.

Working capital

Understated

No effect

Current ratio

Understated

No effect

Retained earnings

No effect

Net income

2.

Working capital

Overstated

No effect

Current ratio

Overstated

No effect

Retained earnings

No effect

Net income

Overstated

3.

Working capital

No effect

No effect

Current ratio

Overstated

No effect

Retained earnings

No effect

Net income

No effect

No effect

E8-11B (10–15 minutes)

(a)

$638,000

=

1.66 to 1

$384,000

(c)

Event

Effect of Error

Adjust Income

Increase

(Decrease)

1.

Overstatement of purchases

Decreases net income

$10,000

and inventory (no effect on

Decreases net income

$11,000

E8-12B (15–20 minutes)

Errors in Inventories

Year

Net

Income

Per Books

Add

Overstate-

ment Jan. 1

Deduct

Understate-

ment Jan. 1

Deduct

Overstate-

ment Dec. 31

Add

Understate-

ment Dec. 31

Corrected

Net Income

2010

$ 50,000

$8,000

$ 58,000

2013

65,000

59,000

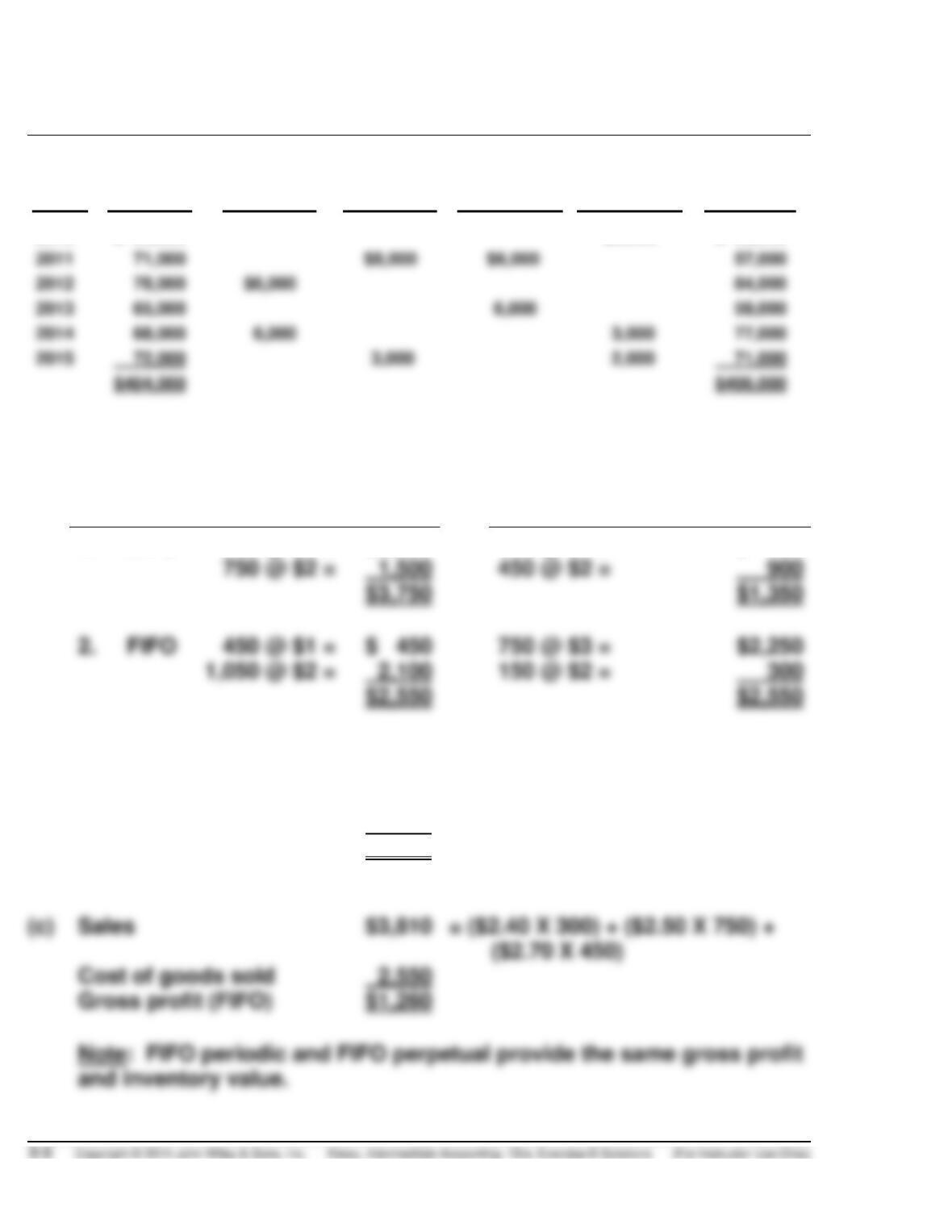

E8-13B (15–20 minutes)

(a)

Cost of Goods Sold

Ending Inventory

1.

LIFO

750 @ $3 =

$2,250

450 @ $1 =

$ 450

750 @ $2 =

450 @ $2 =

900

$3,750

FIFO

450 @ $1 =

$ 450

750 @ $3 =

1,050 @ $2 =

150 @ $2 =

300

$2,550

(b)

LIFO

150 @ $1 =

$ 150

450 @ $2 =

900

300 @ $3 =

900

$1,950

($2.70 X 450)

Cost of goods sold

Gross profit (FIFO)

$1,260

and inventory value.

E8-13B (Continued)

(d) FIFO inventory is based on current costs. Therefore, older costs are

E8-14B (20–25 minutes)

(a)

1.

LIFO

1,200 @ $10.00 =

$12,000

$12,000

2.

Average cost

1,200 @ $10.43 = $12,516

3,330

$67,805

(b)

1.

FIFO

300 @ $11.10 =

$ 3,330

900 @ $11.00 =

9,900

$13,230

2.

LIFO

400 @ $10.00 =

$ 4,000

$12,800

(c)

Total merchandise available for sale

Less inventory (FIFO)

(d)

FIFO.

E8-15B (15–20 minutes)

(a) SAWYER COMPANY

Computation of Inventory For Product

BAP Under FIFO Inventory Method

March 31, 2014

Units

Unit Cost

Total Cost

March 26, 2014

1,200

$6.00

$ 7,200

February 16, 2014

January 25, 2014 (portion)

400

2,000

March 31, 2014, inventory

(b) SAWYER COMPANY

Computation of Inventory For Product

BAP Under LIFO Inventory Method

March 31, 2014

Units

Unit Cost

Total Cost

Beginning inventory

1,200

$4.00

$ 4,800

January 5, 2014 (portion)

March 31, 2014, inventory

(c) SAWYER COMPANY

Computation of Inventory For Product

BAP Under Weighted-Average Inventory Method

March 31, 2014

Units

Unit Cost

Total Cost

Beginning inventory

1,200

$4.00

$ 4,800

January 5, 2014

January 25, 2014

2,600

February 16, 2014

March 26, 2014

Weighted-average cost

($44,600 ÷ 9,000)

$4.96*

March 31, 2014, inventory

$4.96

E8-16B (15–20 minutes)

(a)

1.

3,100 units available for sale – 2,500 units sold = 600 units in the

ending inventory.

300 @ $9.05 =

$2,715

200 @ 9.10 =

sale = $8.79 weighted-average unit cost.

cost.

(b)

1.

cost the ending inventory.

LIFO will yield the lowest gross profit because this method will yield

the highest cost of goods sold figure in the situation presented.

2.

are the lower costs.

LIFO will yield the lowest ending inventory because LIFO uses the

E8-17B (10–15 minutes)

(a)

1.

600 @ $15 =

$ 9,000

240 @ $12 =

2,880

$11,880

600 @ $10 =

240 @ $12 =

E8-17B (Continued)

(b)

1.

FIFO

$11,800 [same as (a)]

2.

LIFO

150 @ $10 =

$ 1,500

600 @ $15 =

9,000

E8-18B (15–20 minutes)

First-in, first-out

Last-in, first-out

Sales

$472,500

$472,500

Cost of goods sold:

Inventory, Jan. 1

$ 45,000

$ 45,000

Purchases

Cost of goods available

Inventory, Dec. 31

Cost of goods sold

Gross profit

Operating expenses

*Purchases

3,000 @ $17 =

$ 51,000

5,000 @ $20 =

100,000

3,500 @ $25 =

87,500

$238,500

First-in, first-out:

3,500 units @ $25 =

500 units @ $20 =

***Last-in, first-out:

3,000 units @ $15 =

1,000 units @ $17 =

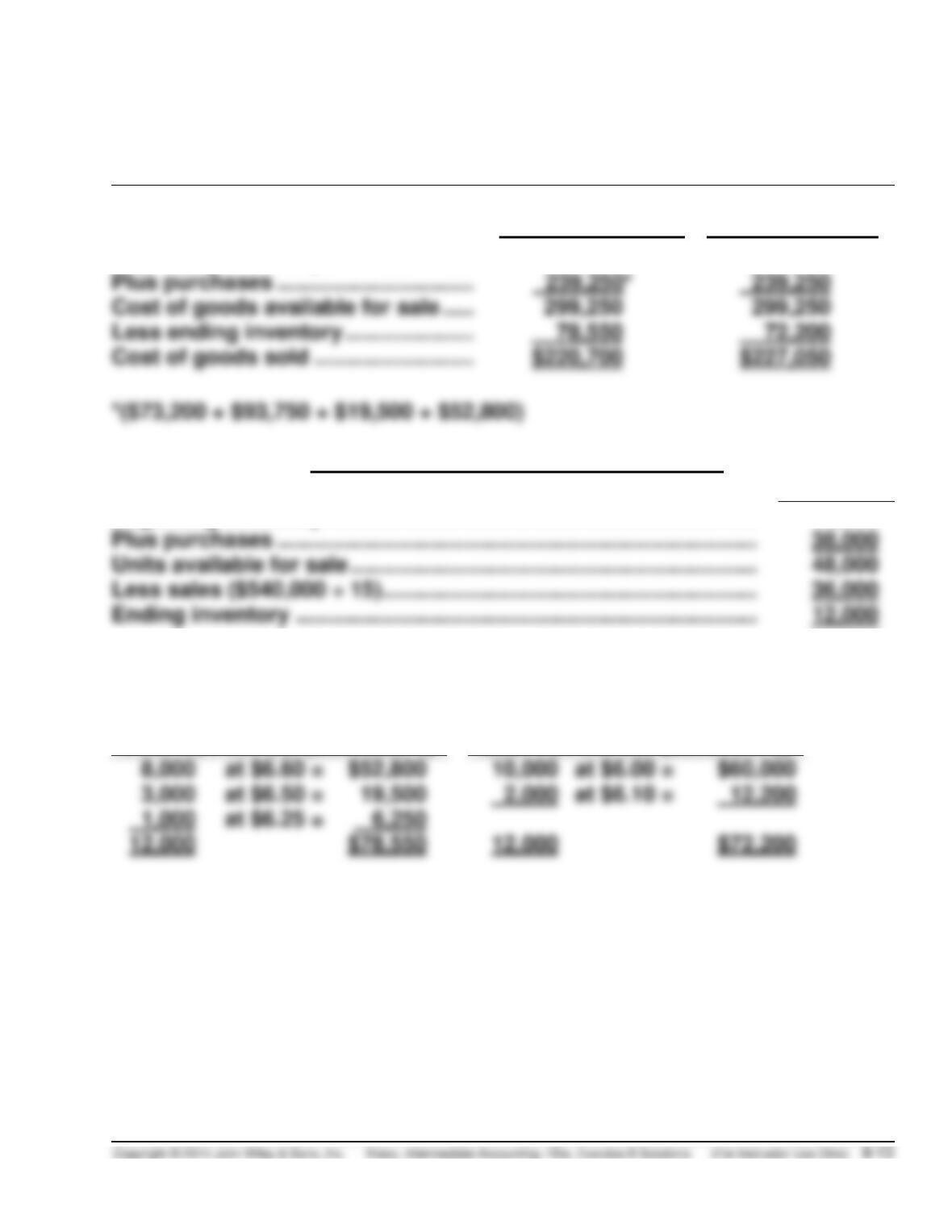

E8-19B (20–25 minutes)

CONSTANCE CORPORATION

Schedules of Cost of Goods Sold

For the First Quarter Ended July 31, 2014

Schedule 1

First-in, First-out

Schedule 2

Last-in, First-out

Beginning inventory ……………………

$ 60,000

$ 60,000

Cost of goods available for sale …..

Schedules Computing Ending Inventory

Units

Beginning inventory …………………………………………………………….

10,000

Plus purchases ……………………………………………………………………

38,000

Units available for sale …………………………………………………………

Less sales ($540,000 ÷ 15) …………………………………………………….

36,000

The unit computation is the same for both assumptions, but the cost assigned

to the units of ending inventory are different.

First-in, First-out (Schedule 1)

Last-in, First-out (Schedule 2)

at $6.60 =

at $6.00 =

at $6.50 =

at $6.10 =

at $6.25 =

E8-20B (10–15 minutes)

(a)

FIFO Ending Inventory – December 31, 2014

105 @ $9.80* =

$1,029.00

20 @ $11.88** =

(b)

LIFO Cost of Goods Sold—2014

105 @ $9.80 =

$1,029.00

180 @ $11.88 =

40 @ $12.87* =

35 @ $10.78** =

377.30

(c) FIFO matches older costs with revenue. When prices are increasing then

E8-21B (10–15 minutes)

(a) The difference between the inventory used for internal reporting pur–

poses and LIFO is referred to as the Allowance to Reduce Inventory to

E8-21B (Continued)

(c) Cash flow was computed as follows:

Revenue …………………………...

$6,500,000

Cost of goods sold …………….

Operating expenses …………..

Income taxes ……………………..

(d) The company has extra cash because its taxes are less. The reason

taxes are lower is because cost of goods sold (in a period of inflation) is

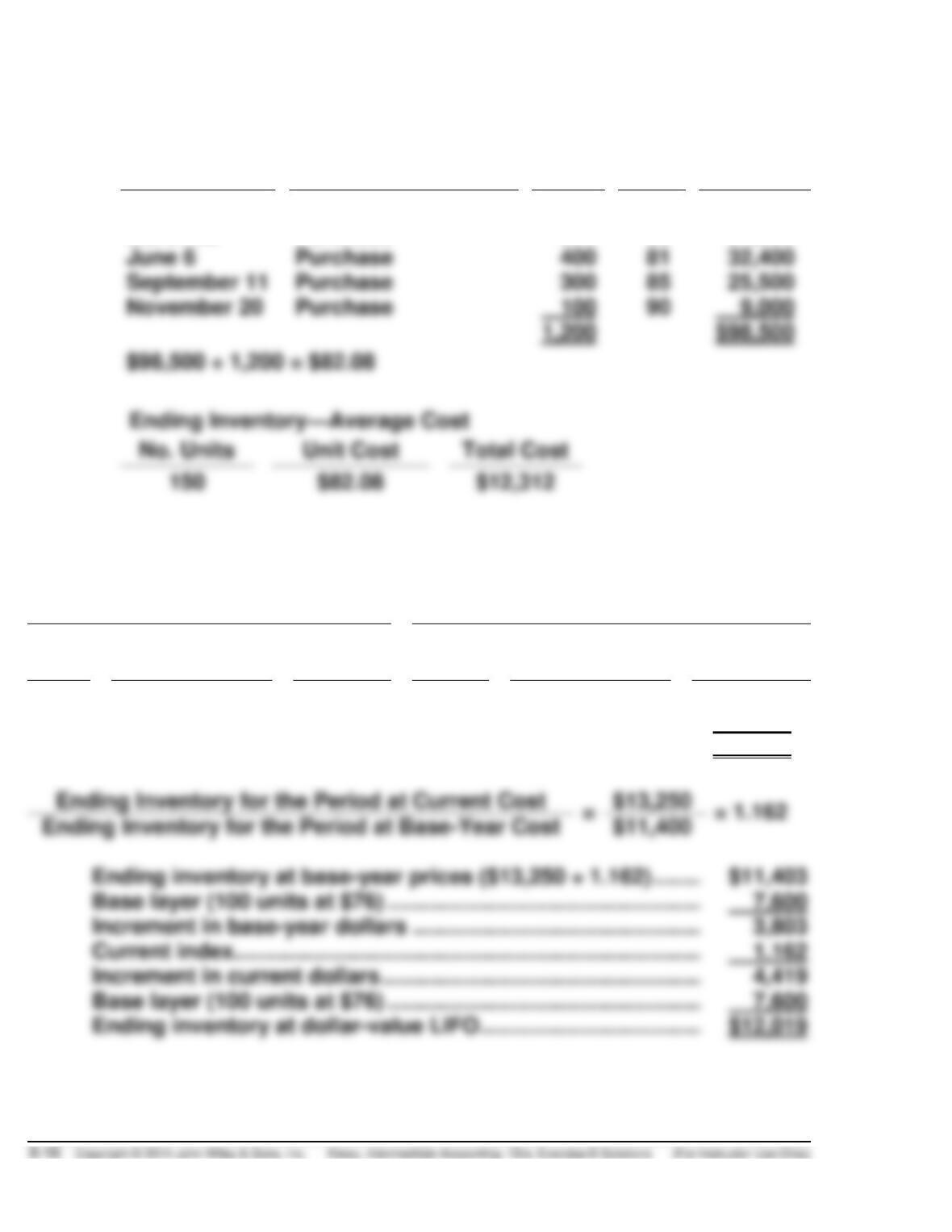

E8-22B (25–30 minutes)

(a)

1.

Ending inventory—Specific Identification

Date

No. Units

Unit Cost

Total Cost

November 20

June 6

2.

Ending inventory—FIFO

Date

No. Units

Unit Cost

Total Cost

November 20

September 11

3.

Ending inventory—LIFO

Date

No. Units

Unit Cost

Total Cost

March 20

E8-22B (Continued)

4.

Ending inventory—Average Cost

Date

Explanation

No.

Units

Unit

Cost

Total

Cost

January 1

Beginning inventory

100

$76

$ 7,600

March 20

Purchase

300

80

24,000

November 20

Purchase

100

90

9,000

(b) Double Extension Method

Base-Year Costs

Current Costs

Units

Base-Year

Cost Per Unit

Total

Units

Current-Year

Cost Per Unit

Total

150

$76

$11,400

100

$90

$9,000

50

$85

4,250

$13,250

Ending Inventory for the Period at Current Cost

Ending inventory at base-year prices ($13,250 ÷ 1.162) ………..

Current index…………………………………………………………………….

Ending inventory at dollar-value LIFO …………………………………

E8-23B (5–10 minutes)

$24,250 – $23,000 = $1,250 increase at base prices.

E8-24B (15–20 minutes)

(a)

12/31/14 inventory at 1/1/14 prices, $530,000 ÷ 1.06 ……………..

$500,000

Inventory 1/1/14 ………………………………………………………………..

510,000

Inventory at 1/1/14 prices …………………………………………………..

$510,000

Less decrease at 1/1/14 prices …………………………………………..

10,000

(b)

12/31/15 inventory at base prices, $588,600 ÷ 1.09 ………………

$540,000

12/31/14 inventory at base prices ……………………………………….

500,000

$40,000 X 1.09 ………………………………………………………………..

43,600

E8-25B (20–25 minutes)

Ending Inventory—Dollar-value LIFO:

2013

$180,000

2014

$180,000 @ 1.00 =

$180,000

30,000 @ 1.05 =

31,500

$211,500

2015

$180,000 @ 1.00 =

$180,000

10,000 @ 1.05 =

10,500

$190,500

2016

$180,000 @ 1.00 =

$180,000

10,000 @ 1.05 =

10,500

4,000 @ 1.25 =

5,000

$195,500

2017

$180,000 @ 1.00 =

$180,000

10,000 @ 1.05 =

10,500

5,000

2018

$180,000 @ 1.00 =

$180,000

10,000 @ 1.05 =

10,500

4,000 @ 1.25 =

5,000

12,000 @ 1.40 =

16,800

E8-26B (15–20 minutes)

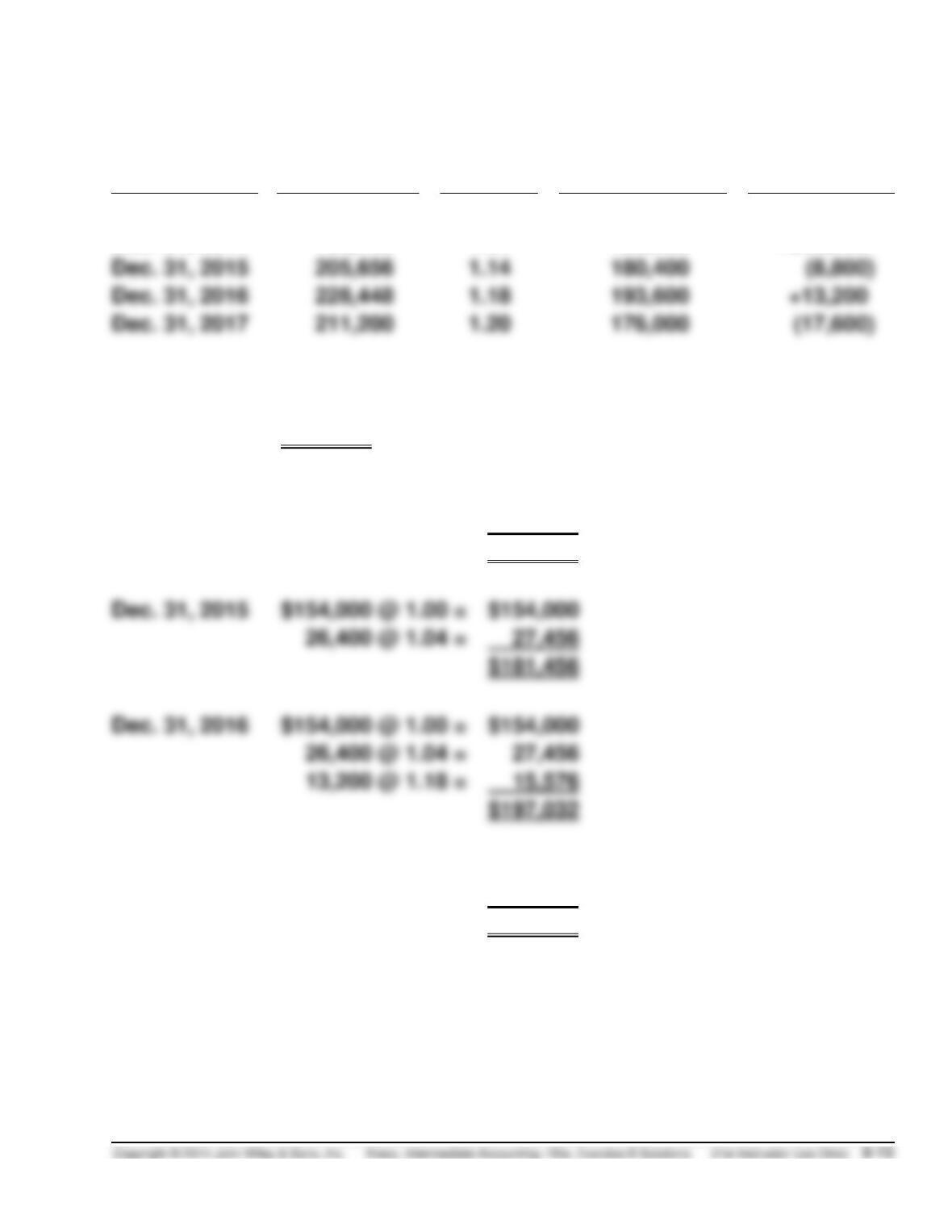

Date

Current $

Price

Index

Base-Year $

Change

from

Prior Year

Dec. 31, 2013

$154,000

1.00

$154,000

—

Dec. 31, 2014

196,768

1.04

189,200

+$35,200

Dec. 31, 2015

205,656

1.14

180,400

Dec. 31, 2016

228,448

1.18

193,600

Dec. 31, 2017

211,200

1.20

176,000

Ending Inventory—Dollar-value LIFO:

Dec. 31, 2013

$154,000

Dec. 31, 2014

$154,000 @ 1.00 =

$154,000

35,200 @ 1.04 =

36,608

$190,608

Dec. 31, 2015

$154,000 @ 1.00 =

$154,000

$181,456

Dec. 31, 2016

$154,000 @ 1.00 =

$154,000

26,400 @ 1.04 =

13,200 @ 1.18 =

15,576

Dec. 31, 2017

$154,000 @ 1.00 =

$154,000

22,000 @ 1.04 =

22,880

$176,880