E9-16B (15–20 minutes)

Furniture

Beds

Rugs

Inventory 1/1/14 (cost)

$ 76,000

$105,000

$211,000

Purchases to 9/9/14 (cost)

Cost of goods available

Deduct cost of goods sold*

Computation for cost of goods sold:*

Furniture:

$608,000

= $486,400

1.25

Beds:

$700,000

= $538,462

$656,000

*Alternative computation for cost of goods sold:

Markup on selling price: Cost of goods sold:

Furniture:

= 20% or 1/5

$608,000 X 80% = $486,400

Beds:

= 3/13

$700,000 X 10/13 = $538,462

Rugs:

= 1/3

$656,000 X 2/3 = $437,333

E9-17B (20–25 minutes)

Ending inventory:

(a)

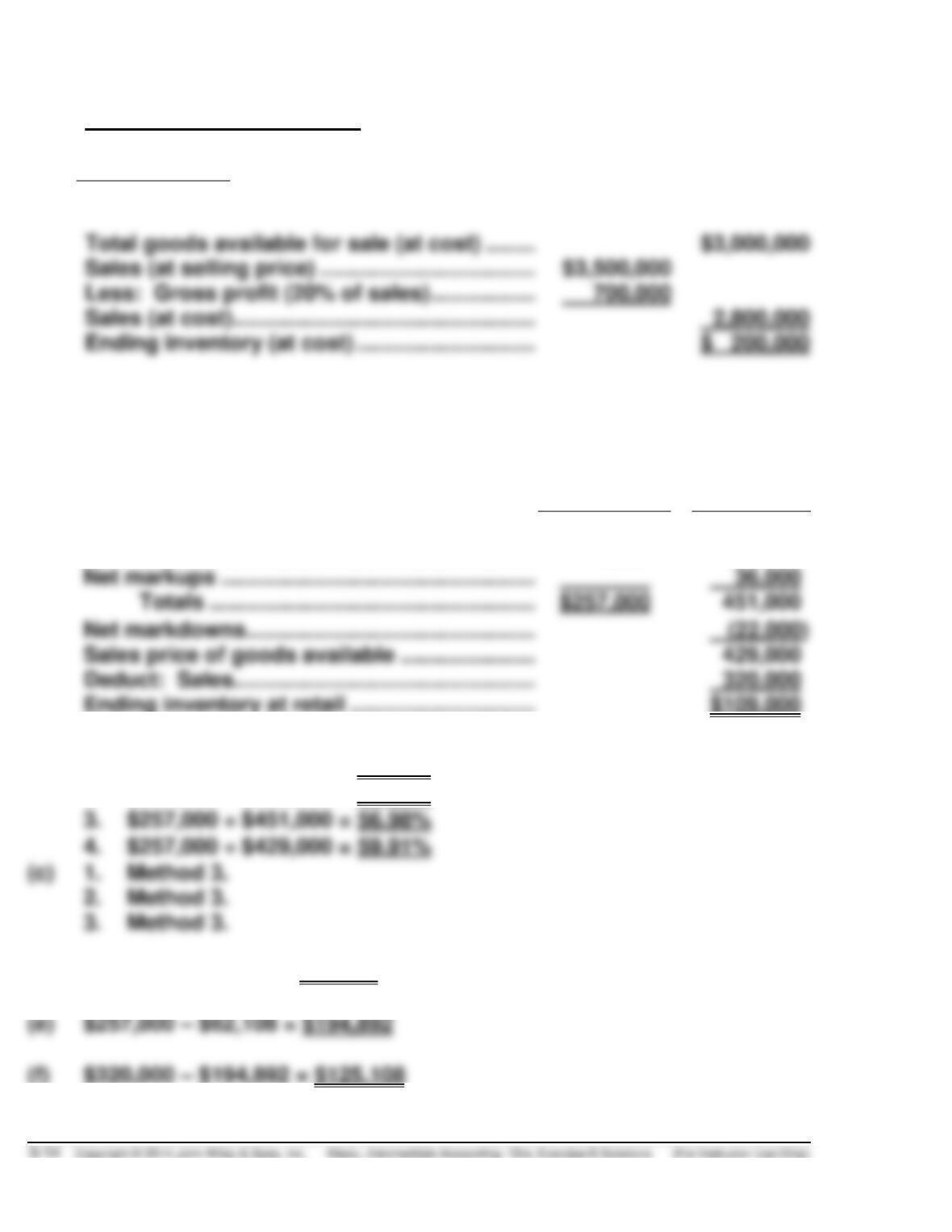

Gross profit is 25% of sales

Total goods available for sale (at cost) ………

$3,000,000

Sales (at selling price) ………………………………

Less: Gross profit (25% of sales) ……………..

(b)

Gross profit is 50% of cost

Total goods available for sale (at cost) ………

$3,000,000

Sales (at selling price) ………………………………

Less: Gross profit (33.33% of sales) …………

(c)

Gross profit is 40% of sales

Total goods available for sale (at cost) ………

$3,000,000

Sales (at selling price) ………………………………

Less: Gross profit (40% of sales) ……………..

E9-17B (Continued)

(d)

Gross profit is 25% of cost

25%

= 20% markup on selling price

100% + 25%

Total goods available for sale (at cost) ……..

$3,000,000

Sales (at selling price) ……………………………..

Less: Gross profit (20% of sales) ……………..

Sales (at cost) ………………………………………….

Ending inventory (at cost) ………………………..

$ 200,000

E9-18B (20–25 minutes)

(a)

Cost

Retail

Beginning inventory …………………………………

$ 81,000

$110,000

Purchases ……………………………………………….

176,000

305,000

Net markups ……………………………………………

Totals ……………………………………………..

451,000

Net markdowns ………………………………………..

(22,000)

Sales price of goods available ………………….

429,000

Deduct: Sales………………………………………….

Ending inventory at retail …………………………

(b)

1.

$257,000 ÷ $415,000 = 61.93%

2.

$257,000 ÷ $393,000 = 65.39%

3.

$257,000 ÷ $451,000 = 56.98%

4.

$257,000 ÷ $429,000 = 59.91%

(c)

Method 3.

Method 3.

Method 3.

(d)

56.98% X $109,000 = $62,108

(e)

$257,000 – $62,108 = $194,892

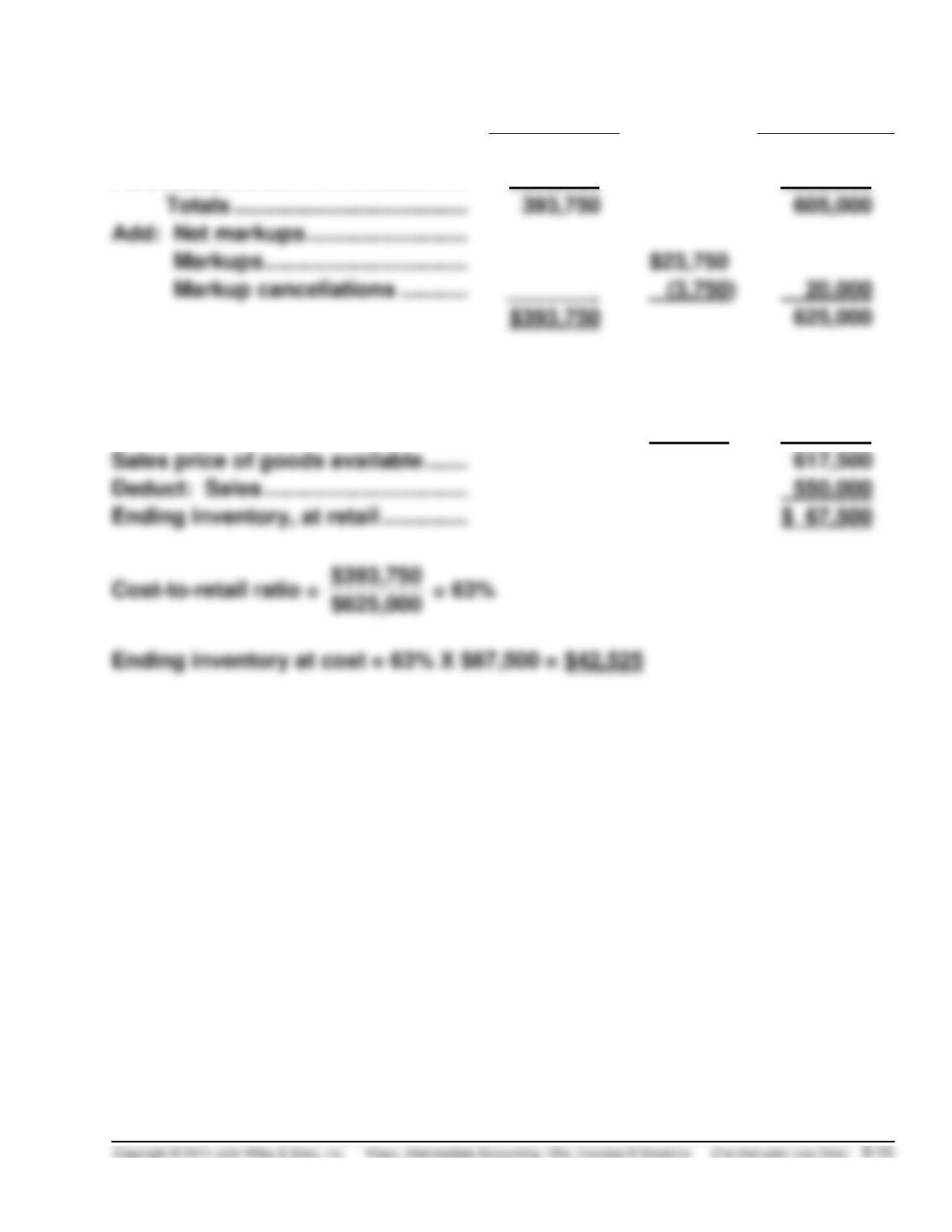

E9-19B (12–17 minutes)

Cost

Retail

Beginning inventory …………………..

$ 50,000

$ 70,000

Purchases …………………………………

343,750

535,000

Totals ………………………………..

393,750

605,000

Add: Net markups ……………………..

Markups …………………………...

$23,750

Markup cancellations ………..

(3,750)

20,000

Deduct: Net markdowns

Markdowns ………………………..

8,750

Markdowns cancellations …..

(1,250)

7,500

Sales price of goods available …….

617,500

Deduct: Sales …………………………...

550,000

E9-20B (20–25 minutes)

Cost

Retail

Beginning inventory ………………………..

$ 60,000

$ 93,000

Purchases ………………………………………

96,000

176,000

Purchase returns …………………………….

(4,000)

(6,000)

Freight on purchases ………………………

2,000

Totals …………………………………….

263,000

Add: Net markups…………………………...

Markups …………………………………

$20,000

Markup cancellations ………………

(3,000)

_______

17,000

Net markups ……………………………………

$154,000

280,000

Deduct: Net markdowns

Markdowns …………………………....

Markdowns cancellations ………..

(5,600)

Net markdowns ……………………………….

13,000

267,000

Deduct net sales ($204,000 – $4,000) ….

200,000

Cost-to-retail ratio =

$154,000

= 55%

$280,000

E9-21B (10–15 minutes)

(a) Inventory turnover:

(b) Average days to sell inventory:

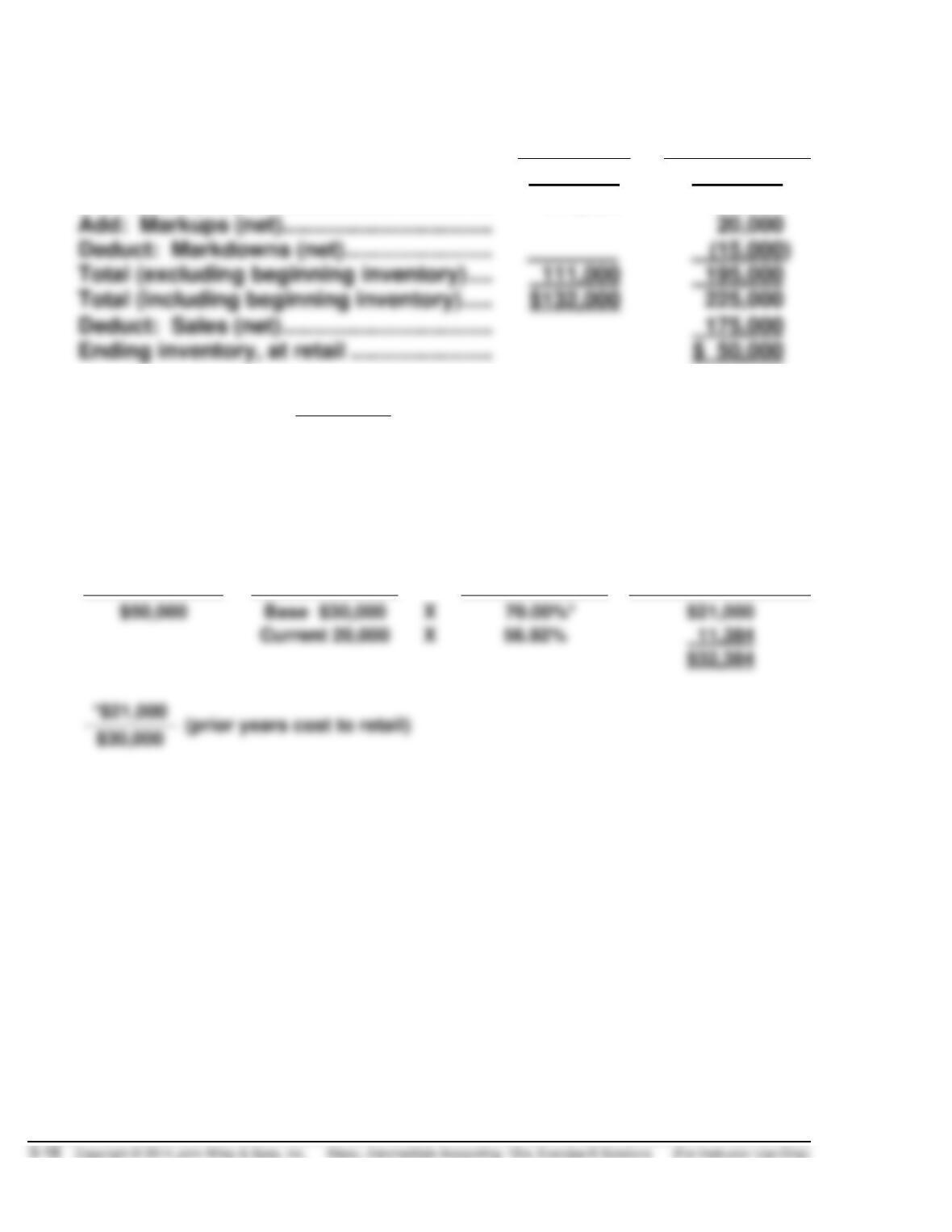

(a)

Conventional Retail Method

Cost

Retail

Inventory, January 1, 2014 ……………

$ 21,000

$ 30,000

Deduct: Markdowns (net) …………….

15,000

Ending inventory, at retail …………….

*E9-22B (Continued)

(b)

LIFO Retail Method

Cost

Retail

Inventory, January 1, 2014 …………………..

$ 21,000

$ 30,000

Purchases (net) ………………………………….

111,000

190,000

Total (excluding beginning inventory) ….

111,000

195,000

Deduct: Sales (net) …………………………....

175,000

Ending inventory, at retail …………………..

Cost-to-retail ratio =

$111,000

= 56.92% (rounded)

$195,000

Computation of ending inventory at LIFO cost, 2014:

Ending

Inventory at

Retail Prices

Layers at

Retail Prices

Cost to Retail

(Percentage)

Ending Inventory

at LIFO Cost

*E9-23B (15–20 minutes)

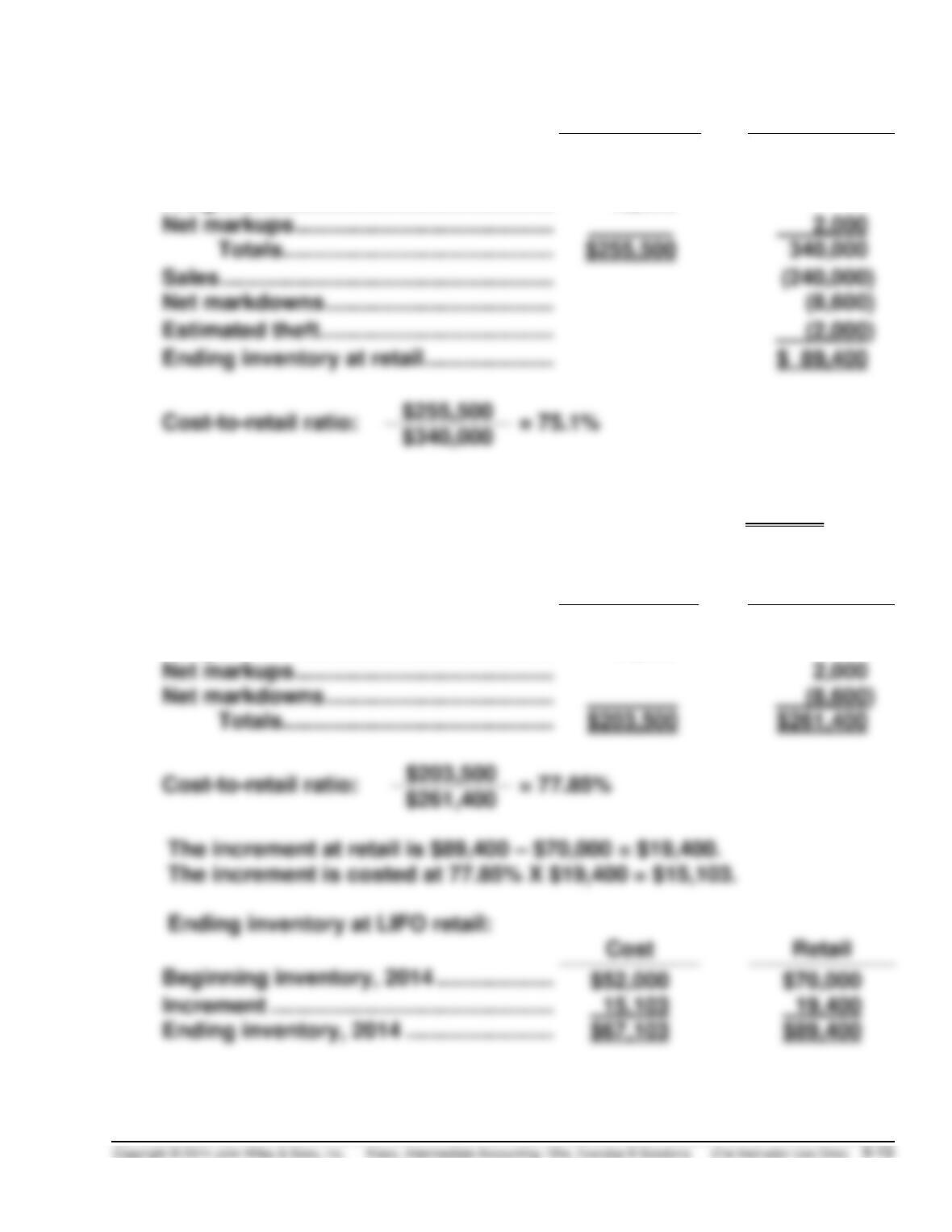

(a)

Cost

Retail

Inventory, January 1, 2014 ……………….

$ 52,000

$ 70,000

Net Purchases …………………………………

191,000

268,000

Freight-in ………………………………………..

12,500

Net markups ……………………………………

Totals ……………………………………..

Sales ………………………………………………

(240,000)

Net markdowns …………………………..…..

Estimated theft ………………………………..

Ending inventory at retail …………………

Ending inventory at lower-of–average-cost-or-market =

$89,400 X 75.1% = $67,139

(b)

Cost

Retail

Purchases ………………………………………

$191,000

$268,000

Freight-in ………………………………………..

12,500

Net markups ……………………………………

Net markdowns ……………………………….

Totals ……………………………………..

Cost

Retail

Beginning inventory, 2014 ……………….

Increment ……………………………………….

Ending inventory, 2014 ……………………

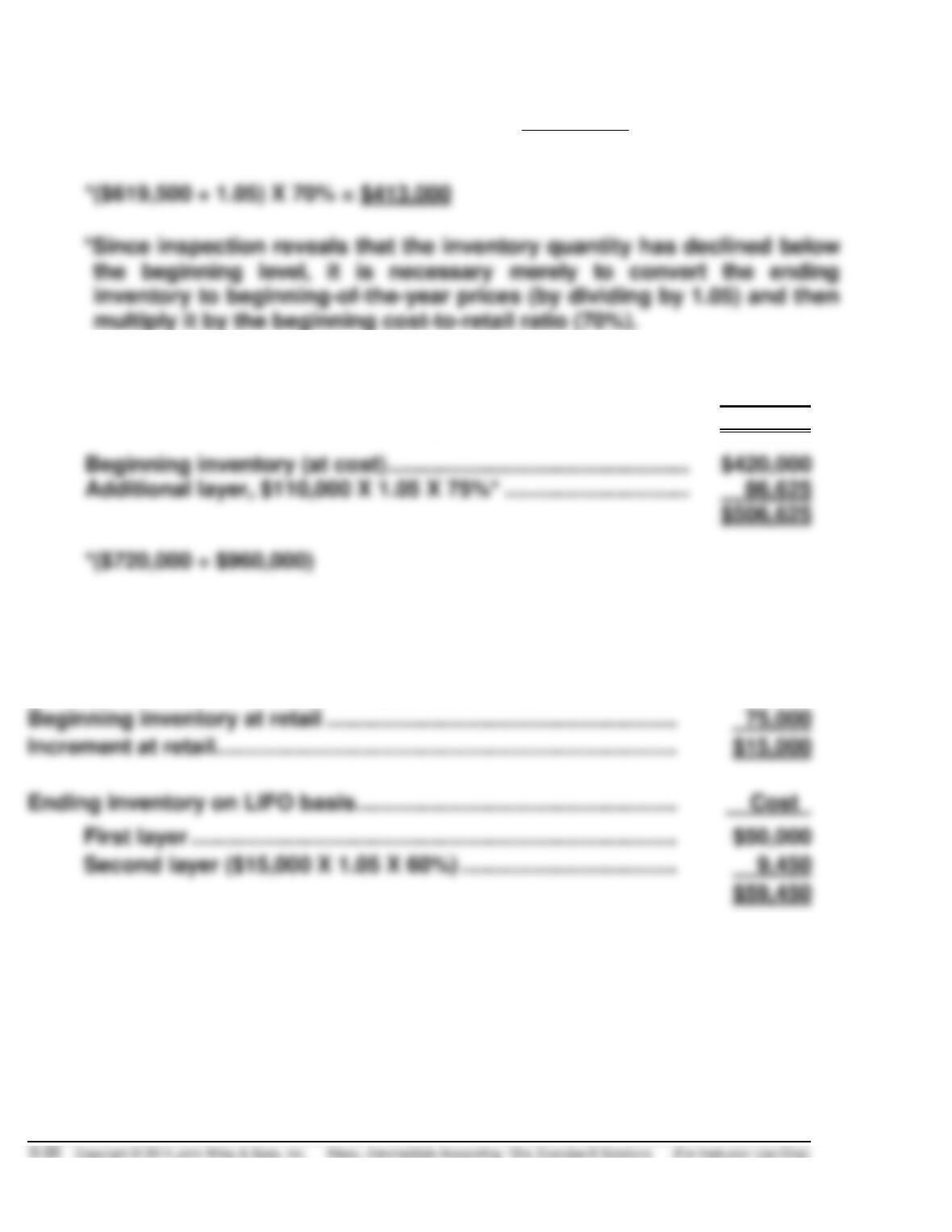

*E9-24B (10–15 minutes)

(a)

Cost-to-retail ratio—beginning inventory:

$420,000

= 70%

$600,000

(b)

Ending inventory at retail prices deflated $745,500 ÷ 1.05 …

$710,000

Beginning inventory at beginning-of-year prices ……………..

600,000

Inventory increase in terms of beginning–of-year dollars ….

$110,000

Beginning inventory (at cost) ………………………………………….

$420,000

Additional layer, $110,000 X 1.05 X 75%* …………………………

*($720,000 ÷ $960,000)

*E9-25B (5–10 minutes)

Ending inventory at retail (deflated) $94,500 ÷ 1.05 …………………

$90,000

Beginning inventory at retail …………………………..…………………….

Increment at retail…………………………………………………………………

$15,000

First layer …………………………………………………………………….

$50,000

Second layer ($15,000 X 1.05 X 60%) ……………………………..

9,450

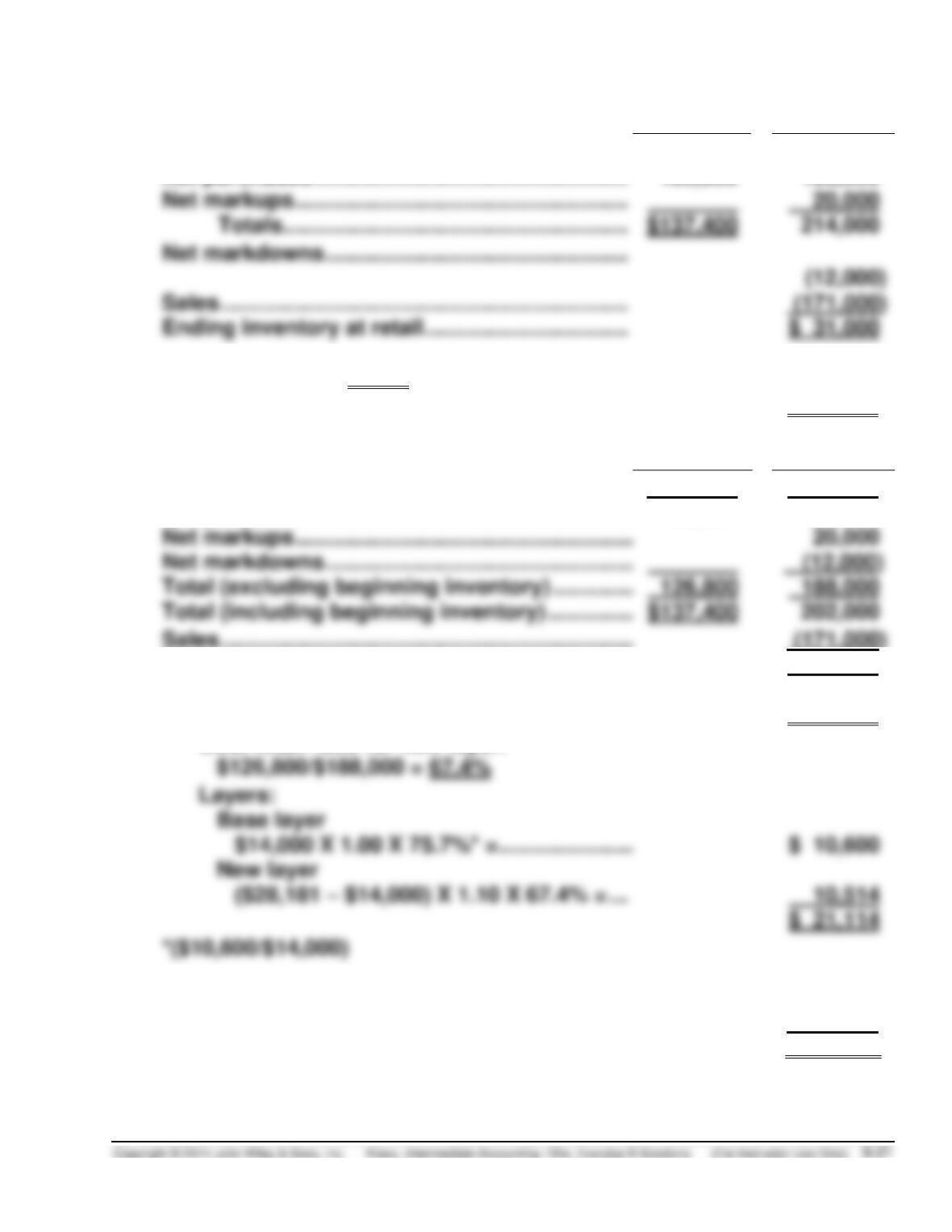

*E9-26B (20–25 minutes)

(a)

Cost

Retail

Beginning inventory …………………………..………

$ 10,600

$ 14,000

Net purchases ……………………………………………

126,800

180,000

Net markups ………………………………………………

20,000

Totals ………………………………………………..

Sales …………………………………………………………

(171,000)

Ending inventory at retail …………………………...

$ 31,000

Cost-retail ratio = 64.2% ($137,400/$214,000)

Ending inventory at cost ($31,000 X 64.2%) …

$ 19,902

(b)

Cost

Retail

Beginning inventory …………………………..………………

$ 10,600

$ 14,000

Net purchases ……………………………………………………

126,800

180,000

Net markups ………………………………………………………

20,000

Net markdowns …………………………..……………………..

Total (excluding beginning inventory) …………………

126,800

188,000

Total (including beginning inventory) ………………….

Ending inventory at retail (current) ……………………..

31,000

Ending inventory at retail (base year)

($31,000 ÷ 1.10) ……………………………………………….

$ 28,181

Cost-retail ratio for new layer:

$126,800/$188,000 = 67.4%

Layers:

Base layer

$14,000 X 1.00 X 75.7%* = …………………………

$ 10,600

New layer

($28,181 – $14,000) X 1.10 X 67.4% = …

10,514

$ 21,114

*($10,600/$14,000)

(c)

Cost of goods available for sale ………………………….

$137,400

Ending inventory at cost, from (b) ……………………….

(21,114)

Cost of goods sold …………………………………………….

$ 116,286

*E9-27B (20–25 minutes)

2013

Restate to base-year retail ($271, 000 ÷ 1.05) ……….

$ 258,095

Layers: 1. $250,000 X 1.00 X 58.4%* = ………………

2. $ 8,095 X 1.05 X 58.0% = ………………

Ending inventory ……………………………………………….

$ 150,930

2014

Restate to base-year retail ($291,500 ÷ 1.08) ………..

$ 269,907

Layers: 1. $250,000 X 1.00 X 58.4% = ………………..

$ 146,000

2. $ 8,095 X 1.05 X 58.0% = ……………….

3. $ 11,812 X 1.08 X 60.0% = ……………….

Ending inventory

$ 158,584

2015

Restate to base-year retail ($280,000 ÷ 1.10) ………..

$ 254,545

Layers: 1. $250,000 X 1.00 X 58.4% = ………………..

2. $ 4,545 X 1.05 X 58.0% = ……………….

2,768

Ending inventory

$ 148,768

2016

Restate to base-year retail ($311,000 ÷ 1.20) ………..

$ 259,167

Layers: 1. $250,000 X 1.00 X 58.4% = ………………..

$ 146,000

2. $ 4,545 X 1.05 X 58.0% = ……………….

3. $ 4,622 X 1.20 X 59.0% = ……………….

Ending inventory ……………………………………………….

$ 152,040

*E9-28B (5–10 minutes)

Inventory (beginning) ………………………………………………

1,400

Adjustment to Record Inventory at Cost*

($100,000 – $98,600) ……………………………………..