CHAPTER 12

Intangible Assets

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Intangible assets;

concepts, definitions;

items comprising

intangible assets.

1, 2, 3, 4, 5, 6,

7, 8, 9, 10, 11,

12, 13, 14

1, 2, 3,

5, 6

1, 2, 3, 4

1, 2, 3

5.

Research and

development costs

and similar costs.

19, 20, 21,

22, 23, 24

9, 10, 11, 12

4, 16, 17

1, 2, 3

4, 5

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1.

Describe the characteristics of

intangible assets.

1

1, 2, 3

1, 2, 3, 4

2.

initial valuation

of intangible assets.

10, 11

3.

Explain the procedure for

amortizing intangible assets.

3, 7, 8, 10,

15, 25

1, 2, 3, 4,

12, 13

4, 5, 6, 7,

9, 10, 11,

1, 2, 3, 6

2

Identify the costs to include in the

2, 24

1, 2, 3, 4

5, 7, 9,

1, 2, 3, 6

1, 2

13

4.

Describe the types of intangible

assets.

4, 11, 15

1, 2, 3

1

5.

Explain the accounting issues for

recording goodwill.

5, 12, 13,

14, 18

5

12, 13,

15

5, 6

6.

Explain the accounting issues

related to intangible-asset

impairments.

6, 7, 16,

17, 18

6, 7, 8

14, 15

5, 6

7.

Identify the conceptual issues

related to research and

development costs.

10, 19, 24

5, 9

3, 4

8.

Describe the accounting for

research and development and

similar costs.

9, 20, 21,

22, 23, 24

9, 10, 11,

4, 6, 8,

16, 17

4

3, 4

9.

Indicate the presentation of

intangible assets

and related items.

13

4, 6

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E12-1

Classification issues—intangibles.

Moderate

15–20

E12-2

Classification issues—intangibles.

Simple

10–15

E12-3

Classification issues—intangible asset.

Moderate

10–15

E12-4

Intangible amortization.

Moderate

15–20

E12-5

Correct intangible asset account.

Moderate

15–20

E12-6

Recording and amortization of intangibles.

Simple

15–20

E12-7

Accounting for trade name.

Simple

10–15

E12-8

Accounting for organization costs.

Simple

10–15

E12-9

Accounting for patents, franchises, and R&D.

Moderate

15–20

E12-10

Accounting for patents.

Moderate

20–25

E12-11

Accounting for patents.

Moderate

15–20

E12-12

Accounting for goodwill.

Moderate

20–25

E12-13

Accounting for goodwill.

Simple

10–15

E12-14

Copyright impairment.

Simple

15–20

E12-15

Goodwill impairment.

Simple

15–20

E12-16

Accounting for R&D costs.

Moderate

15–20

E12-17

Accounting for R&D costs.

10–15

P12-1

Correct intangible asset account.

Moderate

15–20

P12-2

Accounting for patents.

Moderate

20–30

P12-3

Accounting for franchise, patents, and trade name.

Moderate

20–30

P12-4

Accounting for R&D costs.

Moderate

15–20

P12-5

Goodwill, impairment.

25–30

P12-6

Comprehensive intangible assets.

Moderate

30–35

CA12-1

Accounting for pre-opening costs.

Moderate

20–25

CA12-2

Accounting for patents.

Moderate

25–30

CA12-3

Accounting for research and development costs.

Moderate

25–30

CA12-4

Accounting for research and development costs.

Moderate

20–25

SOLUTIONS TO CODIFICATION EXERCISES

CE12-1

According to the Master Glossary:

(a) Intangible assets are assets (not including financial assets) that lack physical substance. (The

term intangible assets is used to refer to intangible assets other than goodwill.)

(b) An asset representing the future economic benefits arising from other assets acquired in a

(c) Research and Development:

Research is planned search or critical investigation aimed at discovery of new knowledge with the

hope that such knowledge will be useful in developing a new product or service (referred to as

(d) A development stage entity is an entity devoting substantially all of its efforts to establishing a new

business and for which either of the following conditions exists:

1. Planned principal operations have not commenced.

CE12-2

See FASB ASC 350-30–35. In the discussions related to “Determining the Useful Life of an Intangible

Asset”

35-1 The accounting for a recognized intangible asset is based on its useful life to the reporting

35-2 The useful life of an intangible asset to an entity is the period over which the asset is expected

to contribute directly or indirectly to the future cash flows of that entity. The useful life is not the

CE12-2 (Continued)

35-3 The estimate of the useful life of an intangible asset to an entity shall be based on an analysis of

all pertinent factors, in particular, all of the following factors with no one factor being more

presumptive than the other:

a. The expected use of the asset by the entity.

b. The expected useful life of another asset or a group of assets to which the useful life of the

intangible asset may relate.

c. Any legal, regulatory, or contractual provisions that may limit the useful life. The cash flows

and useful lives of intangible assets that are based on legal rights are constrained by the

Further, if an income approach is used to measure the fair value of an intangible asset, in

determining the useful life of the intangible asset for amortization purposes, an entity shall

consider the period of expected cash flows used to measure the fair value of the intangible

asset adjusted as appropriate for the entity-specific factors in this paragraph.

35-4 If no legal, regulatory, contractual, competitive, economic, or other factors limit the useful life of

an intangible asset to the reporting entity, the useful life of the asset shall be considered to be

CE12-3

According the FASB ASC 730-10-50:

50-1 Disclosure shall be made in the financial statements of the total research and development

CE12-4

According the FASB ASC 926-720-25,

General

Overall Deals

25-1 An entity may enter into an overall deal arrangement. An entity shall charge the costs of overall

ANSWERS TO QUESTIONS

1. The two main characteristics of intangible assets are:

(a) they lack physical substance.

(b) they are not a financial instrument.

3. Limited-life intangibles should be amortized by systematic charges to expense over their useful

life. An intangible asset with an indefinite life is not amortized.

4. When intangibles are created internally, it is often difficult to determine the validity of any future

service potential. To permit deferral of these types of costs would lead to a great deal of subject-

5. Companies cannot capitalize self-developed, self-maintained, or self-created goodwill. These expen-

ditures would most likely be reported as selling expenses.

6. Factors to be considered in determining useful life are:

(a) The expected use of the asset by the entity.

7. The amount of amortization expensed for a limited-life intangible asset should reflect the pattern in

8. This trademark is an indefinite life intangible and, therefore, should not be amortized.

9. The $190,000 should be expensed as research and development expense in 2014. The $91,000 is

10. Amortization Expense ………………………………………………………….. 35,000

Patents (or Accumulated Patent Amortization) ……………………. 35,000

Straight-line amortization is used because the pattern of use cannot be reliably determined.

11. Artistic-related intangible assets involve ownership rights to plays, pictures, photographs, and

video and audiovisual material. These ownership rights are protected by copyrights. Contract-related

Questions Chapter 12 (Continued)

12. Varying approaches are used to define goodwill. They are

(a) Goodwill should be measured initially as the excess of the fair value of the acquisition cost

over the fair value of the net assets acquired. This definition is a measurement definition but

does not conceptually define goodwill.

13. Goodwill is recorded only when it is acquired by purchase. Goodwill acquired in a business

combination is considered to have an indefinite life and therefore should not be amortized, but

should be tested for impairment on at least an annual basis.

14. Many analysts believe that the value of goodwill is so subjective that it should not be given the

same status as other types of assets such as cash, receivables, inventory, etc. The analysts are

15. Accounting standards require that if events or changes in circumstances indicate that the carrying

amount of such assets may not be recoverable, then the carrying amount of the asset should be

assessed. The assessment or review takes the form of a recoverability test that compares the sum

16. Under U.S. GAAP, impairment losses on assets held for use may not be restored.

17. Impairment losses are reported as part of income from continuing operations, generally in the

“Other expenses and losses” section. Impairment losses (and recovery of losses for assets to be

18. The amount of goodwill impaired is $40,000, computed as follows:

Questions Chapter 12 (Continued)

19. Research and development costs are incurred to develop new products or processes, to improve

present products, or to discover new knowledge. R&D expenditures present problems of

(1) identifying the costs associated with particular activities, projects, or achievements, and

(2) determining the magnitude of the future benefits and the length of time over which such

benefits may be realized. R&D activities may incur costs classified as follows:

20. (a) Personnel (labor) type costs incurred in R&D activities should be expensed as incurred.

(b) Materials and equipment costs should be expensed immediately unless the items have

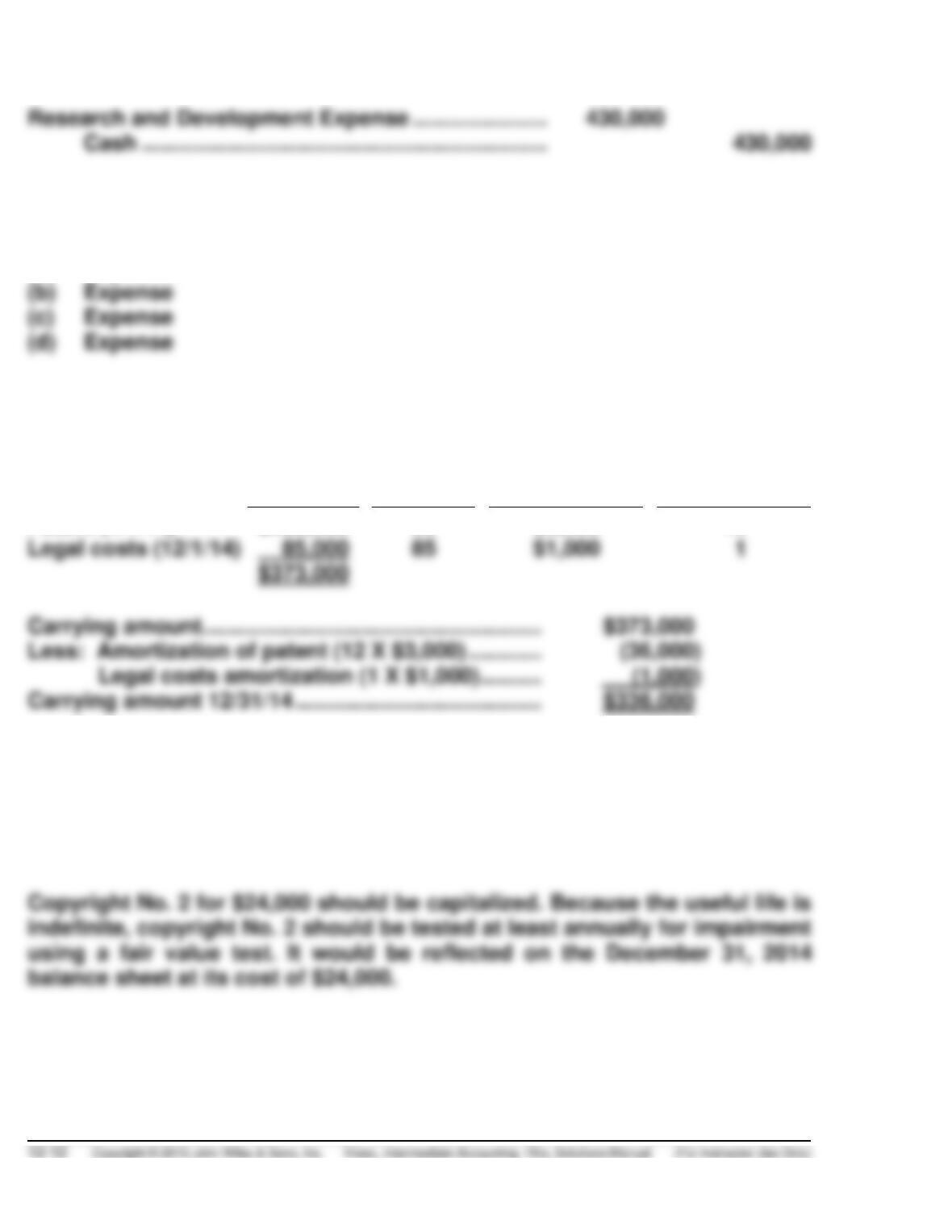

21. (a) Expense as R&D.

(b) Expense as R&D.

(c) Capitalize as patent and/or license and amortize.

Also, see Illustration 12-14 (page 22).

24. These costs are referred to as start-up costs, or more specifically organizational costs in this case.

The accounting for start-up costs is straightforward—expense these costs as incurred. The

profession recognizes that these costs are incurred with the expectation that future revenues will

occur or increased efficiencies will result. However, to determine the amount and timing of future

benefits is so difficult that a conservative approach—expensing these costs as incurred—is

required.

25. The total life, per revised facts, is 40 years (10 + 30). There are 30 (40 – 10) remaining years for

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 12-1

Patents …………………………………………………………………..

54,000

Amortization Expense ……………………………………………..

BRIEF EXERCISE 12-2

Patents …………………………………………………………………..

24,000

Amortization Expense ……………………………………………..

BRIEF EXERCISE 12-3

Trade Names …………………………………………………………..

68,000

Amortization Expense ……………………………………………..

BRIEF EXERCISE 12-4

Franchises ……………………………………………………………..

120,000

Amortization Expense ……………………………………………..

BRIEF EXERCISE 12-5

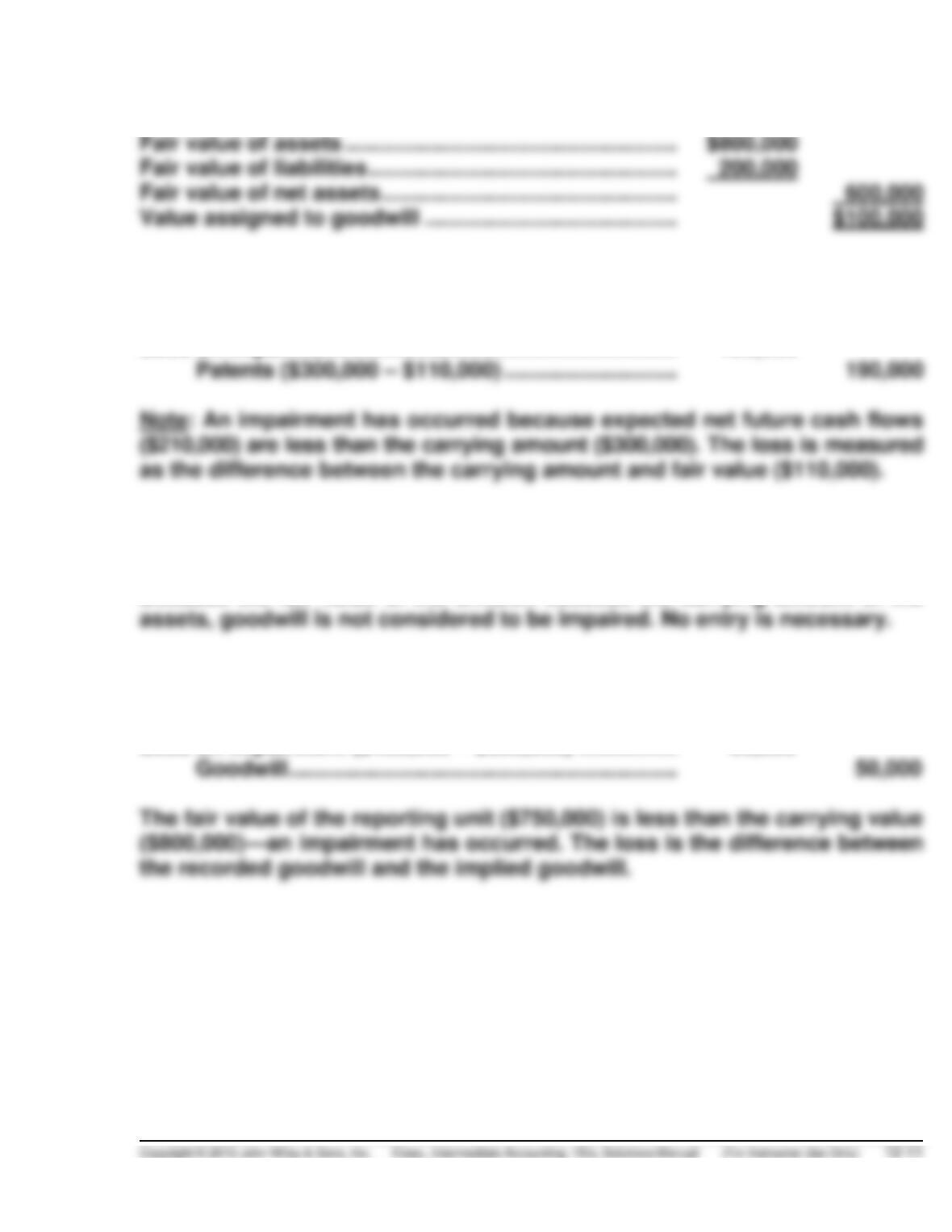

Purchase price …………………………………………………….

$700,000

Fair value of assets ………………………………………………

Fair value of liabilities …………………………………………..

Fair value of net assets …………………………………………

BRIEF EXERCISE 12-6

Loss on Impairment ………………………………………………..

190,000

Patents ($300,000 – $110,000) ………………………….

BRIEF EXERCISE 12-7

Because the fair value of the division exceeds the carrying amount of the

BRIEF EXERCISE 12-8

Loss on Impairment ($400,000 – $350,000) ……………….

50,000

Goodwill ……………………………………………………….

BRIEF EXERCISE 12-9

Organization Expense ……………………………………………..

60,000

Cash …………………………..………………………………….

60,000

BRIEF EXERCISE 12-10

BRIEF EXERCISE 12-11

(a) Capitalize

BRIEF EXERCISE 12-12

Carrying

Amount

Life in

Months

Amortization

Per Month

Months

Amortization

Patent (1/1/14)

$288,000

96

$3,000

12

BRIEF EXERCISE 12-13

Copyright No. 1 for $9,900 should be expensed and therefore not reported

on the balance sheet.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 12–13

SOLUTIONS TO EXERCISES

EXERCISE 12-1 (15–20 minutes)

(a) 10, 13, 15, 16, 17, 19, 23

(b) 1. Long-term investments in the balance sheet.

2. Property, plant, and equipment in the balance sheet.

3. Research and development expense in the income statement.

4. Current asset (prepaid rent) in the balance sheet.

12. Research and development expense in the income statement.

14. Research and development expense in the income statement.

18. Research and development expense in the income statement.

EXERCISE 12-2 (10–15 minutes)

The following items would be classified as an intangible asset:

Cable television franchises Film contract rights

Music copyrights Customer lists

EXERCISE 12-2 (Continued)

Investments in affiliated companies would be classified as part of the

investments section of the balance sheet.

EXERCISE 12-3 (10–15 minutes)

(a)

Trademarks

$15,000

Excess of cost over fair value of net identifiable

assets of acquired subsidiary (goodwill)

(b) Organization costs, $24,000, should be expensed. Discount on bonds

payable, $35,000, should be reported as a contra account to bonds

payable in the long-term liabilities section.

EXERCISE 12-4 (15–20 minutes)

1. Alatorre should report the patent at $600,000 (net of $400,000

accumulated amortization) on the balance sheet. The computation of

Amortization for 2012 and 2013 ($1,000,000/10) X 2

2014 amortization: ($1,000,000 – $200,000) ÷ (6 – 2)

2. Alatorre should amortize the franchise over its estimated useful life.

Because it is uncertain that Alatorre will be able to retain the franchise

3. These costs should be expensed as incurred. Therefore $275,000 of

organization expense is reported in income for 2014.

4. Because the license can be easily renewed (at nominal cost), it has an

EXERCISE 12-5 (15–20 minutes)

Research and Development Expense ………………………..

940,000

Patents ……………………………………………………………………

75,000

Rent Expense [(5 ÷ 7) X $91,000] ……………………………….

65,000

Prepaid Rent [(2 ÷ 7) X $91,000] …………………………..……

Advertising Expense ………………………………………………..

Income Summary …………………………………………………….

Discount on Bonds Payable ……………………………………..

Interest Expense ……………………………………………………..

Paid in Capital in Excess of Par on Common Stock …..

Intangible Assets …………………………..…………………..

Amortization Expense [($75,000 ÷ 10) X 1/2] ……………..

EXERCISE 12-6 (15–20 minutes)

Patents …………………………………………………………………..

350,000

Goodwill …………………………………………………………………

360,000

Franchise ……………………………………………………….

450,000

Copyright ……………………………………………………….

156,000

Research and Development Expense ……………………….

215,000

Intangible Assets …………………………………………….

1,531,000

Amortization Expense ……………………………………………..

Patents ($350,000/8) ………………………………………..

Franchise ($450,000/10 X 6/12) …………………………

Copyright ($156,000/5 X 5/12) …………………………..

EXERCISE 12-7 (10–15 minutes)

(a) 2013 amortization: $16,000 ÷ 10 = $1,600.

12/31/13 book value: $16,000 – $1,600 = $14,400.

(c) Carrying amount ($19,733) > future cash flows ($16,000); thus the

trade name fails the recoverability test. The new carrying value is

$15,000—the trade name’s fair value.

EXERCISE 12-8 (10–15 minutes)

(a)

Attorney’s fees in connection with organization

of the company

$15,000

Costs of meetings of incorporators to discuss

organizational activities

State filing fees to incorporate

1,000

(b)

Organization Expense …………………………………………….

23,000

Cash (Payables) ……………………………………………..

EXERCISE 12-9 (15–20 minutes)

(a) JIMMY CARTER COMPANY

Intangibles Section of Balance Sheet

December 31, 2014

Patent from Ford Company, net of accumulated

Schedule 1 Computation of Patent from Ford Company

Cost of patent at date of purchase

$2,000,000

Amortization of patent for 2013 ($2,000,000 ÷ 10 years)

Amortization of patent for 2014 ($1,800,000 ÷ 5 years)

Schedule 2 Computation of Franchise from Reagan Company

Cost of franchise at date of purchase

$ 480,000

Amortization of franchise for 2014 ($480,000 ÷ 10)

EXERCISE 12-9 (Continued)

(b) JIMMY CARTER COMPANY

Income Statement Effect

For the year ended December 31, 2014

Patent from Ford Company:

Amortization of patent for 2014

($1,800,000 ÷ 5 years)

$360,000

Franchise from Reagan Company:

Amortization of franchise for 2014

($480,000 ÷ 10)

Payment to Reagan Company

($2,500,000 X 5%)

Research and development costs

EXERCISE 12-10 (15–20 minutes)

(a)

2010

Research and Development Expense ……………………….

170,000

Cash ……………………………………………………….

170,000

Patents ……………………………………………………….

Cash ……………………………………………………….

Amortization Expense …………………………..

Patents [($18,000 ÷ 10) X 3/12] ………………………….

2011

Amortization Expense …………………………..

Patents ($18,000 ÷ 10) …………………………..

EXERCISE 12-10 (Continued)

(b)

2012

Patents ……………………………………………………….

9,480

Cash ……………………………………………………….

9,480

Amortization Expense ……………………………………………..

1,940

Patents ($750 + $1,190) …………………………..

1,940

[Jan. 1–June 1: ($18,000 ÷ 10) X

5/12 = $750

June 1–Dec. 31: ($18,000 – $450 –

$1,800 – $750 + $9,480) = $24,480;

($24,480 ÷ 12) X 7/12 = $1,190]

2013

Amortization Expense ……………………………………………..

Patents ($24,480 ÷ 12) …………………………..

2,040

(c)

2014 and 2015

Amortization Expense ……………………………………………..

10,625

Patents ($21,250 ÷ 2) …………………………..

($24,480 – $1,190 – $2,040) = $21,250

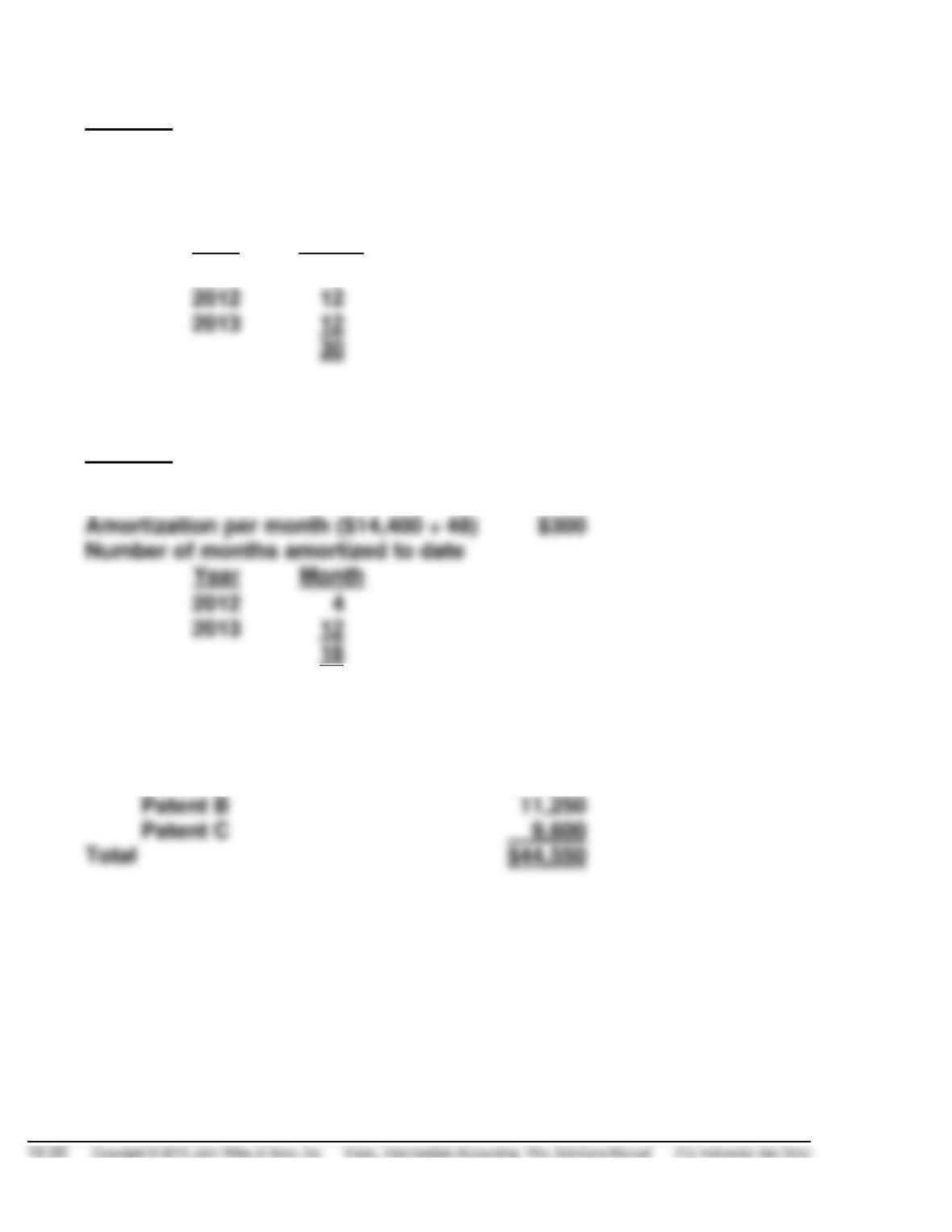

EXERCISE 12-11

(a)

Patent A

Life in years

17

Life in months (12 X 17)

204

Amortization per month ($30,600 ÷ 204)

$150

Number of months amortized to date

Year

Month

2010

10

2013

12

EXERCISE 12-11 (Continued)

Patent B

Life in years

10

Life in months (12 X 10)

120

Amortization per month ($15,000 ÷ 120)

$125

Number of months amortized to date

Year

Month

2011

6

2012

12

Book value 12/31/13 $11,250: ($15,000 – [$125 X 30])

Patent C

Life in years

4

Life in months (12 X 4)

48

Amortization per month ($14,400 ÷ 48)

Number of months amortized to date

Year

Book value 12/31/13 $9,600: ($14,400 – [$300 X 16])

At December 31, 2013

Patent A

$23,700

Patent B

Patent C