COMPARATIVE ANALYSIS CASE (Continued)

Pepsi

Inventory

In the first quarter of 2011, Quaker Foods North America (QFNA)

changed its method of accounting for certain U.S. inventories from

the last-in, first-out (LIFO) method to the average cost method. This

change is considered preferable by management as we believe that

the average cost method of accounting for all U.S. foods inventories

(d) Change in accounting policy (2009)

Coke

Recently Issued Accounting Guidance

Principles of Consolidation

The information presented above reflects the impact of the

Company’s adoption of accounting guidance issued by the Financial

COMPARATIVE ANALYSIS CASE (Continued)

Pepsi

Recent Accounting Pronouncements

In June 2009, the Financial Accounting Standards Board (FASB)

amended its accounting guidance on the consolidation of variable

interest entities (VIE). Among other things, the new guidance requires

FINANCIAL STATEMENT ANALYSIS CASE—WAL-MART

(a) (1) In the year of the change, Wal-Mart will reverse the revenue recog-

nized in prior periods for layaway sales that are not complete.

This will reduce income in the year of the change.

nition, not the overall amount recognized.

(b) By recognizing the revenue before delivery, Wal-Mart was recognizing

revenue before the earnings process was complete. In addition, if cus-

(c) Even if all retailers used the same policy, it still might be difficult to

compare the results for layaway transactions. For example what if

Note to instructor: The requirements for this case relate to Walmart

accounting policies for revenue recognition prior to implementation of the

new revenue standard. The new standard and its provisions are addressed

are addressed in more detail in Chapter 18.

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

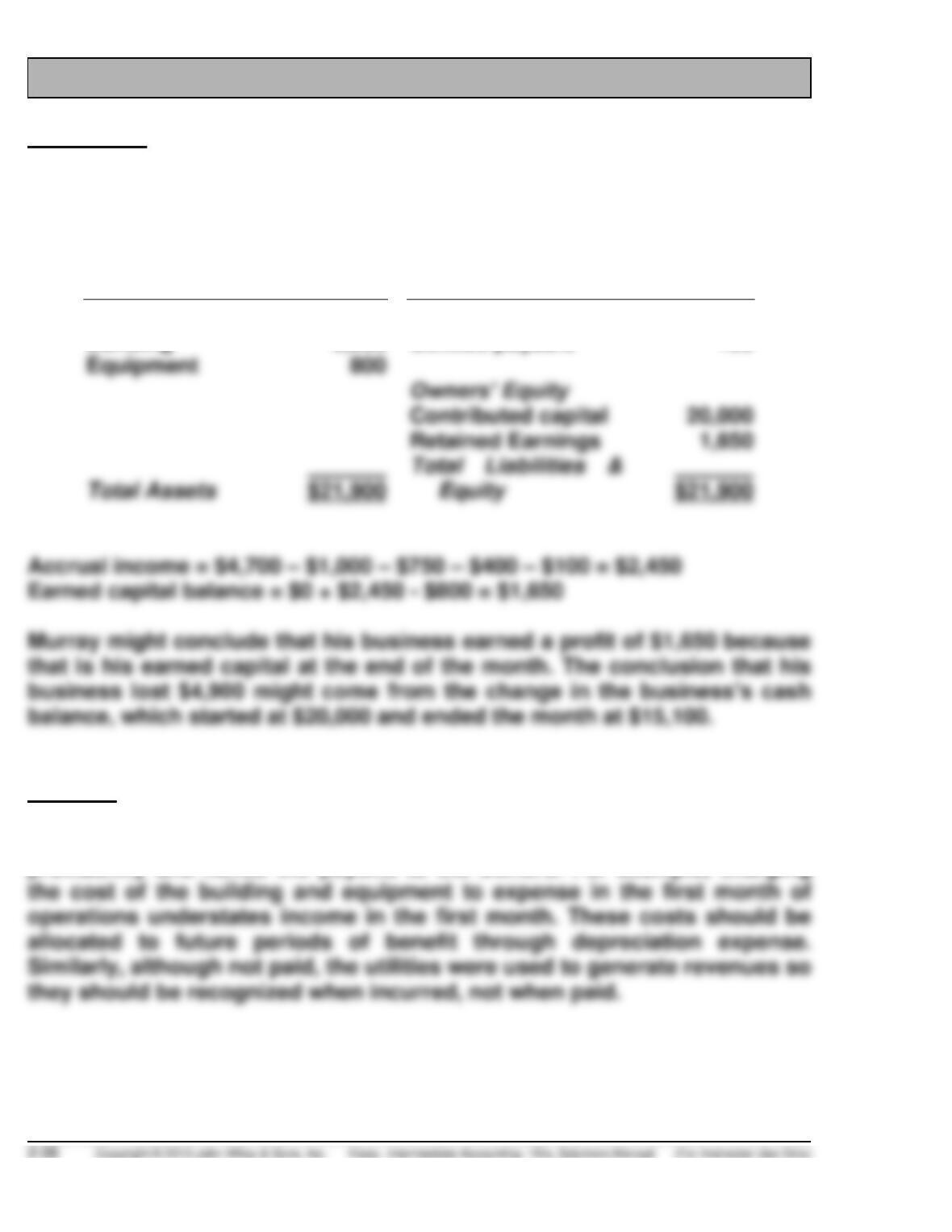

Caddie Shack Company

Statement of Financial Position

May 31, 2014

Assets

Liabilities

Cash

$15,100

Advertising payable

$ 150

Building

6,000

Utilities payable

100

Equipment

800

Contributed capital

Retained Earnings

1,650

Analysis

The income measure of $2,450 is most relevant for assessing the future

profitability and hence the payoffs to the owners. For example, charging

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Principles

GAAP income is the accrual income computed above as $2,450. The key

concept illustrated in the difference between the loss of $4,900 and profit of

PROFESSIONAL RESEARCH

Search Strings: concept statement, “materiality”, “articulation”

(a) According to Concepts Statement 2 (CON 2): Qualitative Characteristics

of Accounting Information, “Glossary”:

(b) CON 2, Appendix C—See Table 1—refers to several SEC cases which

apply materiality. Students might also research SEC literature (e.g. Staff

Accounting Bulletin No. 99), although SEC literature is not in the FARS

database.

“ a. An accounting change in circumstances that puts an enterprise

in danger of being in breach of covenant regarding its financial

condition may justify a lower materiality threshold than if its

position were stronger.

b. A failure to disclose separately a nonrecurrent item of revenue

PROFESSIONAL RESEARCH (Continued)

However, according to CON 2, Pars. 129, 131 the FASB notes that

more than magnitude must be considered in evaluating materiality:

Almost always, the relative rather than the absolute size of a

SFAC No. 2, Par. 131. Some hold the view that the Board should

promulgate a set of quantitative materiality guides or criteria covering

a wide variety of situations that preparers could look to for authoritative

(c) SFAC No. 3, Par. 15. The two classes of elements are related in such

a way that (a) assets, liabilities, and equity are changed by elements

of the other class and at any time are their cumulative result and (b)

PROFESSIONAL SIMULATION

Explanation

1. Most accounting methods are based on the assumption that the business

enterprise will have a long life. Acceptance of this assumption

provides credibility to the historical cost principle, which would be of

2. The company is too conservative in its accounting for this transaction.

The expense recognition principle indicates that expenses should be

allocated to the appropriate periods involved. In this case, there appears

to be a high uncertainty that the company will have to pay. FASB

3. This entry violates the economic entity assumption. This assumption

in accounting indicates that economic activity can be identified with a

particular unit of accountability. In this situation, the company erred by

charging this cost to the wrong economic entity.

Research

According to Concepts Statement 8 (CON 8) par. QCII:

Information is material if omitting it or misstating it could influence decisions

that users make on the basis of the financial information of a specific

IFRS CONCEPTS AND APPLICATION

IFRS2-1

The IASB framework makes two assumptions. One assumption is that

financial statements are prepared on an accrual basis; the other is that the

IFRS2-2

While there is some agreement that the role of financial reporting is to assist

IFRS2-3

The FASB differentiates gains and losses from revenue and expenses where

IFRS2-4

As indicated, the measurement project relates to both initial measurement

and subsequent measurement. Thus, the continuing controversy related to

historical cost and fair value accounting suggests that this issue will be

IFRS2-5

The IASB and FASB frameworks are strikingly similar. This is not surprising,

given that the IASB framework was adopted after the FASB developed its

framework (the IASB framework was approved in April 1989). In addition, the

IASC, the predecessor to the IASB, was formed to facilitate harmonization of

accounting standards across countries. This objective could be aided by

adopting a similar conceptual framework.

Note to Instructors—These differences may be resolved as the FASB and

IASB work on their performance reporting projects.

IFRS2-6

Search Strings: “materiality”, “completeness”

(a) According to the Framework (para. 30): Information is defined to be

(b) (1) According to the Framework, (para. 29–30):

29 The relevance of information is affected by its nature and materiality.

In some cases, the nature of information alone is sufficient to determine

IFRS2-6 (Continued)

(2) With respect to Completeness (para. 30):

To be reliable, the information in financial statements must be

complete within the bounds of materiality and cost. An omission

(c) According to the Framework (para. 22):

Accrual basis

In order to meet their objectives, financial statements are prepared on

the accrual basis of accounting. Under this basis, the effects of

IFRS2-7

Marks and Spencer plc

(a) Revenue Recognition

Revenue

Revenue comprises sales of goods to customers outside the Group

(b) Historical Cost

-Property, plant, and equipment

A. Goodwill

Goodwill arising on consolidation represents the excess of the

consideration transferred and the amount of any non-controlling

interest in the acquiree over the fair value of the identifiable assets

IFRS2-7 (Continued)

(c) New Accounting Pronoucements and Policies