CHAPTER 7

SOLUTIONS TO B EXERCISES

E7-1B (10–15 minutes)

(a) Cash includes the following:

1.

Commercial savings account—

First National Bank of Yojimbo ………………………..

$ 1,200,000

Money market fund—Nguyen Co. ………………………

(b) Other items classified as follows:

3. Travel advances (reimbursed by employee)* should be reported as

receivable—employee in the amount of $360,000.

4. Cash restricted in the amount of $3,000,000 for the retirement of

liability.**

8. Certificates of deposits of $1,000,000 each should be classified as

temporary investments.

9. Postdated check of $250,000 should be reported as an accounts

receivable.

10. The compensating balance requirement does not affect the balance

E7-2B (10–15 minutes)

1. Cash balance of $323,000 consisting of the checking account balance and

the savings account. Only the checking account balance should be

2. Cash balance is $116,300 computed as follows:

Overdraft …………………………………………………..

3. Cash balance of $205,000. Only the checking account balance should be

reported as cash.

The postdated check of $10,000 should be reported as a receivable.

reported as a receivable;

4. Cash balance is $336,000 computed as follows:

Checking account balance ………………………….

$ 61,000

E7-2B (Continued)

5. Cash balance is $171,900 computed as follows:

Checking account balance ………………………….

$171,000

Cash advance received from customer ……….

900

E7-3B (10–15 minutes)

Current assets

Accounts receivable

Customers

for a bank loan) …………………………..

Installment accounts due in 2015 ……

December 31, 2015* …………………….

Other** ($10,320 + $4,200) …………………

Investments

Advance to subsidiary company ………….

Accounts (of which accounts

in the amount of $40,000 have

E7-4B (10–15 minutes)

Computation of cost of goods sold:

Merchandise purchased ………………………………………..

Less: Ending inventory …………………………………………

Sales on account

$345,000

Less collections

203,000

Uncollected balance

Balance per ledger

87,000

E7-5B (15–20 minutes)

(a)

1.

June 3

Accounts Receivable—Pham Inc. …………………………...

1,500

Sales ……………………………………………………………..

1,500

June 12

Cash ………………………………………………………………………

1,470

Sales Discounts ($1,500 X 2%) …………………………………

Accounts Receivable—Pham …………………………..

1,500

June 3

Accounts Receivable—Pham …………………………………..

1,470

Sales ($1,500 X 98%) ……………………………………….

1,470

June 12

Cash ………………………………………………………………………

1,470

Accounts Receivable—Pham …………………………..

1,470

(b)

July 29

Cash ………………………………………………………………………

1,500

Accounts Receivable—Pham …………………………..

1,470

Sales Discounts Forfeited ……………………………….

30

not record this forfeiture until final cash settlement.)

E7-6B (5–10 minutes)

July 1

Accounts Receivable ………………………………………………

10,000

Sales …………………………..…………………………………

10,000

July 10

Cash ………………………………………………………………………

Sales Discounts ……………………………………………………..

Accounts Receivable …………………………..………….

July 17

Accounts Receivable ………………………………………………

Sales …………………………..…………………………………

July 30

Cash ………………………………………………………………………

Accounts Receivable …………………………..………….

E7-7B (10–15 minutes)

(a)

Bad Debt Expense …………………………………………………..

6,375

Allowance for Doubtful Accounts …………………….

6,375*

*.03 X ($225,000 – $12,500) = $6,375

(b)

Bad Debt Expense …………………………………………………..

1,500

Allowance for Doubtful Accounts …………………….

1,500**

E7-8B (15–20 minutes)

(a)

Allowance for Doubtful Accounts …………………………….

3,000

Accounts Receivable ………………………………………

3,000

(b)

Accounts Receivable ………………………………………………

Less: Allowance for Doubtful Accounts …………………..

Net realizable value …………………………………………

(c)

Accounts Receivable ………………………………………………

Less: Allowance for Doubtful Accounts …………………..

Net realizable value …………………………………………

E7-9B (8–10 minutes)

(a)

Bad Debt Expense …………………………………………………..

12,500

Allowance for Doubtful Accounts

[($180,000 X 5%) + $3,500] …………………………...

(b)

Bad Debt Expense …………………………………………………..

10,000

Allowance for Doubtful Accounts

($1,000,000 X 1%) ………………………………………..

E7-10B (10–12 minutes)

(a) The direct write-off approach is not theoretically justifiable even though

required for income tax purposes. The direct write–off method does not

(b) Bad Debt Expense – 1% of Sales = $76,000 ($7,600,000 X 1%)

E7-11B (8–10 minutes)

Balance 1/1 ($1,400 – $310)

$1,090

Over one year

E7-12B (15–20 minutes)

8/1

Accounts Receivable—Sharper Co. ………………………….

20,790

Sales ($21,000 X 99%) ……………………………………..

20,790

8/5

Cash [$57,000 X (1 – 5%)] …………………………………………

54,150

Loss on Sale of Receivables …………………………………….

Accounts Receivable ($57,000 X 99%) ………………

Sales Discounts Forfeited ………………………………..

8/9

Accounts Receivable ………………………………………………

300

Sales Discounts Forfeited

($30,000 X 1%) …………………………..………………..

300

Cash ………………………………………………………………………

Finance Charge ($20,000 X 6%) ………………………………..

Notes Payable ………………………………………………..

20,000

E7-12B (Continued)

8/11

Accounts Receivable—Sharper Co. ………………………….

210

Sales Discounts Forfeited

($21,000 X 1%) ………………………………………………

9/29

Allowance for Doubtful Accounts ……………………………..

16,800

Accounts Receivable—Sharper Co.

$21,000 – (20% X $21,000) = $16,800] ……………..

E7-13B (10–15 minutes)

(a)

Cash ………………………………………………………………………

94,000

Finance Charge ………………………………………………………

6,000

**

Notes Payable…………………………………………………

**3% X $200,000 = $6,000

(b)

Cash ………………………………………………………………………

175,000

Accounts Receivable ………………………………………

175,000

(c)

Notes Payable …………………………………………………………

100,000

Interest Expense …………………………………………………….

Cash ………………………………………………………………

*8% X $100,000 X 3/12 = $2,000

E7-14B (15–18 minutes)

1.

Cash ……………………………………………………………………….

46,000

Loss on Sale of Receivables

($50,000 X 8%) ………………………………………………………

Accounts Receivable ……………………………………….

50,000

2.

Cash ………………………………………………………………………

18,800

Finance Charge ($20,000 X 6%) ………………………………..

1,200

Notes Payable …………………………………………………

20,000

Bad Debt Expense …………………………………………………..

6,880

Allowance for Doubtful Accounts

[($122,000 X 4%) + $2,000]……………………………..

Bad Debt Expense …………………………………………………..

Allowance for Doubtful Accounts

($810,000 X 2%) …………………………………………….

E7-15B (15–20 minutes)

(a)

To be recorded as a sale, all of the following conditions would be met:

1.

The transferred asset has been isolated from the transferor (put

beyond reach of the transferor and its creditors).

either the transferred assets or beneficial interests in the transferred

E7-15B (Continued)

(b)

Computation of net proceeds:

Cash received ($262,500 X 92%) ……………

$241,500

Due from factor ($262,500 X 5%) …………..

13,125

Less: Recourse obligation …………………..

Computation of gain or loss:

Carrying value ……………………………………..

Net proceeds ……………………………………….

The following journal entry would be made:

Cash……………………………………………………………….

$241,500

Due from Factor ………………………………………………

Loss on Sale of Receivables …………………………….

Recourse Liability …………………………………….

Accounts Receivable ………………………………..

E7-16B (15–20 minutes)

(a)

To be recorded as a sale, all of the following conditions would be met:

1.

The transferred asset has been isolated from the transferor (put

beyond reach of the transferor and its creditors).

either the transferred assets or beneficial interests in the transferred

assets.

before their maturity.

E7-16B (Continued)

(b)

Computation of net proceeds:

Cash received ($200,000 X 92%) ……………..

$184,000

Due from factor ($200,000 X 6%) ……………..

12,000

$196,000

Less: Recourse obligation……………………..

4,500

Net proceeds …………………………………………

$191,500

Computation of gain or loss:

Carrying value ……………………………………..

$200,000

Net proceeds ……………………………………….

Loss on sale of receivables ………………….

$ 8,500

The following journal entry would be made:

Cash ………………………………………………………………

$184,000

Due from Factor ……………………………………………..

Loss on Sale of Receivables …………………………...

Recourse Liability ……………………………………

Accounts Receivable ……………………………….

E7-17B (10–15 minutes)

(a)

July 1

Cash ………………………………………………………………………

93,000

Due from Factor ………………………………………………………

5,000

Loss on Sale of Receivables ……………………………………

2,000

Accounts Receivable ………………………………………

($5,000 = 5% X $100,000)

($2,000 = 2% X $100,000)

(b)

July 1

Accounts Receivable …………………………..………………….

Due to KTT Corp. …………………………………………….

5,000

Cash ………………………………………………………………

E7-18B (10–15 minutes)

1.

July 1

Notes Receivable ……………………………………………………

732,053.70

Discount on Notes Receivable …………………………

232,053.70

Land ……………………………………………………….……..

375,000.00

Gain on Sale of Land ………………………………………

125,000.00

Face value of note

Present value of 1 for 4 periods at 10%

Present value of note

Face value of note

2.

July 1

Notes Receivable ……………………………………………………

400,000.00

Discount on Notes Receivable …………………………

128,037.12

Service Revenue …………………………………………….

271,962.88

Computation of the present value of

the note:

Maturity value …………………………………………………

Present value of $400,000 due

in 8 years at 10%—$400,000

X .46651 ………………………………………………………

Present value of $16,000

payable annually for 8 years

at 10% annually—$16,000

X 5.33493 …………………………………………………….

Present value of the note and

and interest ………………………………………………….

E7-19B (20–25 minutes)

(a)

Notes Receivable …………………………………………………….

100,000.00

Discount on Notes Receivable ………………………….

24,386.00

Consulting Revenue ………………………………………..

75,614.00*

$100,000 X .75614 = $75,614

(b)

Discount on Notes Receivable ………………………………….

11,342.10

Interest Revenue ……………………………………………..

11,342.10*

*$75,614 X 15%

(c)

Discount on Notes Receivable ………………………………….

Interest Revenue ……………………………………………..

Rounded by $0.48.

Cash ……………………………………………………………………….

Notes Receivable …………………………………………….

E7-20B (10–15 minutes)

(a)

Accounts Receivable ………………………………………………

685,000

Sales ……………………………………………………………..

685,000

Cash ……………………………………………………….……………..

650,000

Accounts Receivable ………………………………………

650,000

E7-20B (Continued)

(c) Monaco Company’s turnover ratio has increased. That is, it is turning

E7-21B (10–15 minutes)

(a)

Cash [$50,000 X (1 – 10%)] ……………………………………….

45,000

Due from Factor ………………………………………………………

3,000

Loss on Sale of Receivables …………………………………….

4,000

Accounts Receivable ………………………………………

Recourse Obligation ……………………………………….

Computation of cash received

Accounts receivable ………………………………………..

$50,000

Less: Due from factor (6% X $50,000) ………………

Finance charge (4% X $50,000) ………………

2,000

Cash received …………………………………………..

$45,000

Computation of net proceeds (cash and other

assets received, less any liabilities incurred)

Cash received …………………………………………………

$45,000

Due from factor ……………………………………………….

3,000

$48,000

Less: Recourse liability …………………………………..

2,000

Net proceeds …………………………………………….

$46,000

Computation of loss

Carrying (Book) value ……………………………………..

$50,000

Less: Net proceeds ………………………………………..

Loss on sale of receivables ……………………….

$ 4,000

Repair Expense ………………………………………………………..

Postage Expense ($40.00 – $12.90) …………………………...

Office Supplies ………………………………………………………..

Cash Over and Short ………………………………………………..

Cash ($200.00 – $46.50) …………………………………..

E7-21B (continued)

(b) Accounts Receivable Turnover =

Net Sales

Average Trade Receivables (net)

Net Sales

=

14.1

With the factoring transaction, Monaco Company’s turnover ratio increases by

even more than in the earlier exercise. By factoring the receivables, Monaco is

able to convert them to cash. The cost of this approach to converting

receivables to cash is captured in the Loss on Sale of Receivables account

*E7-22B (5–10 minutes)

1.

April 1

Petty Cash ………………………………………………………………

1,000

Cash ………………………………………………………………

1,000

2.

April 10

Cash Over and Short ……………………………………………….

Transportation-In (or Inventory) ……………………………….

Supplies Expense ……………………………………………………

Postage Expense …………………………………………………….

Miscellaneous Expense …………………………………………..

Cash ($1,000 – $135) ……………………………………….

3.

April 20

Petty Cash ………………………………………………………………

Cash ………………………………………………………………

*E7-23B (10–15 minutes)

Accounts Receivable—Employees

($25.00 + $12.00) ……………………………………………………

37.00

*E7-24B (15–20 minutes)

(a) WANG COMPANY

Bank Reconciliation

July 31

Balance per bank statement, July 31 ………………………..

$17,300

Add: Deposits in transit ………………………………………….

4,700a

Deduct: Outstanding checks …………………………………..

(2,200)b

Correct cash balance, July 31 ………………………………….

$19,800

Balance per books, July 31 ………………………………………

Add: Collection of note ………………………………………….

Less: Bank service charge ……………………………………..

NSF check ……………………………………………………

Corrected cash balance, July 31 ………………………………

$19,800

aComputation of deposits in transit

Deposits per books ……………………………………………

$11,620

Deposits per bank in July …………………………………..

Less: Deposits in transit (June) ………………………….

July ………………………………………………………………..

(6,920)

bComputation of outstanding checks

Checks written per books …………………………………..

$6,200

Checks cleared by bank in July …………………………..

(June)* …………………………………………………….

July ………………………………………………………………..

Outstanding checks, July 31 ……………………………………

(b)

Cash ………………………………………………………………………

1,300

Office Expenses—Bank Service Charge ……………………

30

Accounts Receivable ………………………………………………

670

Notes Receivable …………………………………………….

2,000

*E7-25B (15–20 minutes)

(a) ELFEN COMPANY

Bank Reconciliation, October 31, 2014

Tri National Bank

Balance per bank statement, October 31, 2014 …………..

$16,090

Add: Cash on hand ………………………………………………….

$ 250

Deposits in transit …………………………………………..

4,800

5,050

Deduct: Outstanding checks …………………………………….

1,550

Correct cash balance ………………………………………………..

$19,590

Balance per books, October 31, 2014

($17,801 + $45,000 – $45,271) ………………………………….

Add: Overstated check for supplies ………………………….

Note ($2,000) and interest ($40) collected …………

2,040

Deduct: Bank service charges ………………………………….

Correct cash balance

$19,590

(b)

Cash ……………………………………………………….……………..

2,040

Notes Receivable ……………………………………………

2,000

Interest Revenue …………………………..………………..

40

(To record collection of note and interest)

Office Expense—Bank Charges …………………………..…..

Cash ………………………………………………………………

(To record August bank charges)

Cash

Supplies Expense …………………………………………..

supplies)

(c) The corrected cash balance of $19,590 would be reported in the October

31, 2014, balance sheet.

*E7-26B (15-25 minutes)

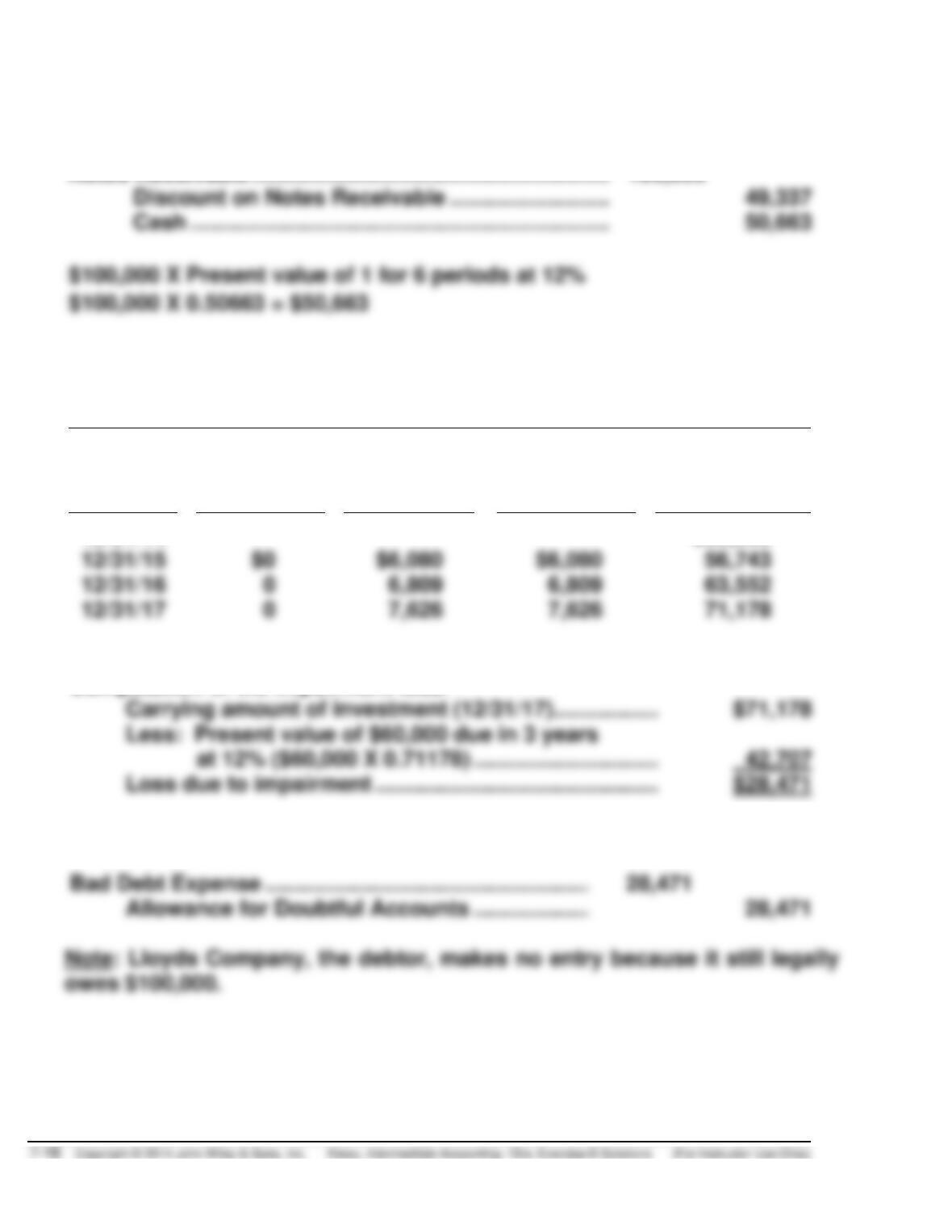

(a) Journal entry to record issuance of loan by London Bank:

December 31, 2014

Notes Receivable ……………………………………………………..

100,000

Discount on Notes Receivable …………………………

(b) Note Amortization Schedule

(Before Impairment)

Date

Cash

Received

(0%)

Interest

Revenue

(12%)

Increase in

Carrying

Amount

Carrying

Amount of

Note

12/31/14

$50,663

12/31/15

Computation of the impairment loss:

at 12% ($60,000 X 0.71178) …………………………

The entry to record the loss by London Bank is as follows:

Bad Debt Expense …………………………………………………..

Allowance for Doubtful Accounts …………………….

*E7-27B (15-25 minutes)

(a) Cash received by State Construction Company on December 31, 2014:

Present value of principal ($1,000,000 X 0.49718) ….

$497,180

Present value of interest ($100,000 X 3.35216) ………

Cash received …………………………………………………….

$832,396

(b) Note Amortization Schedule

(Before Impairment)

Date

Cash

Received

(10%)

Interest

Revenue

(15%)

Increase in

Carrying

Amount

Carrying

Amount of

Note

$24,859

100,000

(c) Loss due to impairment:

Carrying amount of loan (12/31/16) …………………..

$885,843

3 years ($700,000 X 0.65752) ………………….

for 3 years ($100,000 X 2.28323) ……………………

Loss due to impairment …………………………………..

$197,256