Time and Purposes of Concepts for Analysis (Continued)

CA 8-10 (Time 30–35 minutes)

Purpose—to provide the student with an opportunity to analyze the effect of changing from the FIFO

CA 8-11 (Time 20–25 minutes)

Purpose—to provide the student with an opportunity to analyze the ethical implications of purchasing

decisions under LIFO.

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 8-1

(a) Purchased merchandise in transit at the end of an accounting period to which legal title has

passed should be recorded as purchases within the accounting period. If goods are shipped f.o.b.

(b) Inventory ………………………………………………………………………………….. 35,300

Accounts Payable (Supplier) ……………………………………………………. 35,300

CA 8-2

(a) If the terms of the purchase are f.o.b. shipping point (manufacturer’s plant), Strider Enterprises

should include in its inventory goods purchased from its suppliers when the goods are shipped.

For accounting purposes, title is presumed to pass at that time.

(d) Products on consignment represent inventories owned by Strider Enterprises, which are physically

transferred to another enterprise. However, Strider Enterprises retains title to the goods until their

sale by the other company (Chavez Inc.).

CA 8-3

(a) According to FASB ASC 330-10–30–1:

“As applied to inventories, cost means in principle the sum of the applicable expenditures and

charges directly or indirectly incurred in bringing an article to its existing condition and

location.”

The discussion includes the following: “Selling expenses constitute no part of the inventory costs.”

To the extent that warehousing is a necessary function of importing merchandise before it can be

sold, certain elements of warehousing costs might be considered an appropriate cost of inventory

In theory, warehousing costs are considered a product cost because these costs are incurred to

maintain the product in a salable condition. However, in practice, warehousing costs are most fre-

quently treated as a period cost.

(b) It is correct to conclude that obsolete items are excludable from inventory. Cost attributable to

such items is “nonuseful” and “nonrecoverable” cost (except for possible scrap value) and should

(c) The primary use of the airplanes should determine their treatment on the balance sheet. Since the

airplanes are held primarily for sale, and chartering is only a temporary use, the airplanes should

be classified as current assets. Depreciation would not be appropriate if the planes are considered

inventory. FASB ASC Glossary entry for “Inventory” states in part that the term Inventory “excludes

long-term assets subject to depreciation accounting, or goods which, when put into use, will be so

classified.”

(d) The transaction is a product financing arrangement and should be reported by the company as

CA 8-4

(a) Cash discounts should not be accounted for as financial income when payments are made.

CA 8-4 (Continued)

(b) Cash discounts should not be accounted for as a reduction of cost of goods sold for the period

when payments are made. Cost of goods sold should be reduced when the earnings process is

(c) Cash discounts should be accounted for as a direct reduction of purchase cost because they

CA 8-5

(a) 1. Inventories are unexpired costs and represent future benefits to the owner. A balance sheet

2. Beginning and ending inventories are included in the computation of net income only for

the purpose of arriving at the cost of goods sold during the period of time covered by the

statement. Goods included in the beginning inventory which are no longer on hand are expired

costs to be matched against revenues earned during the period. Goods included in the ending

inventory are unexpired costs to be carried forward to a future period, rather than expensed.

(b) Financial accounting has as its goal the proper reporting of financial transactions and events in

accordance with generally accepted accounting principles. Income tax accounting has as its goal

the reporting of taxable transactions and events in conformity with income tax laws and regulations.

(c) FIFO and LIFO are inventory costing methods employed to measure the flow of costs. FIFO

CA 8-6

(a) Inventory profits occur when the inventory costs matched against sales are less than the replace–

ment cost of the inventory. The cost of goods sold therefore is understated and net income is con–

sidered overstated. By using LIFO (rather than some method such as FIFO), more recent costs

are matched against revenues and inventory profits are thereby reduced.

CA 8-6 (Continued)

(b) As long as the price level increases and inventory quantities do not decrease, a deferral of income

CA 8-7

(a) The average-cost method assumes that inventories are sold or issued evenly from the stock on

hand; the FIFO method assumes that goods are sold or used in the order in which they are

purchased (i.e., the first goods purchased are the first sold or used); and the LIFO method

matches the cost of the last goods purchased against revenue.

(b) The weighted-average-cost method combines the cost of all the purchases in the period with the

CA 8-8

(a) 1. The LIFO method (periodic) allocates costs on the assumption that the last goods purchased

2. The dollar-value method of LIFO inventory valuation is a procedure using dollars instead of

units to measure increments or reductions in inventory. The method presumes that goods in

the inventory can be classified into pools or homogenous groups. After the grouping into pools

the ending inventory is priced at the end-of-year prices and a price index number is applied to

CA 8-8 (Continued)

(b) The advantages of the dollar-value method over the traditional LIFO method are as follows:

1. The application of the LIFO method is simplified because, under the pooling procedure, it is not

necessary to assign costs to opening and closing quantities of individual items. As a result,

LIFO liquidation is less possible.

The disadvantages of the dollar-value method as compared to the traditional LIFO method are

as follows:

1. Due to technological innovations and improvements over time, material changes in the com–

position of inventory may occur. Items found in the ending inventory may not have existed

during the base year. Thus, conversion of the ending inventory to base-year prices may be

(c) The basic advantages of LIFO are:

1. Matching—In LIFO, the more recent costs are matched against current revenues to provide a

better measure of current earnings.

2. Tax benefits—As long as the price level increases and inventory quantities do not decrease, a

deferral of income taxes occurs.

The major disadvantages of LIFO are:

1. Reduced earnings—Because current costs are matched against current revenues, net income

is lower than it is under other inventory methods when price levels are increasing.

2. Inventory understated—The inventory valuation on the balance sheet is ordinarily outdated

because the oldest costs remain in inventory.

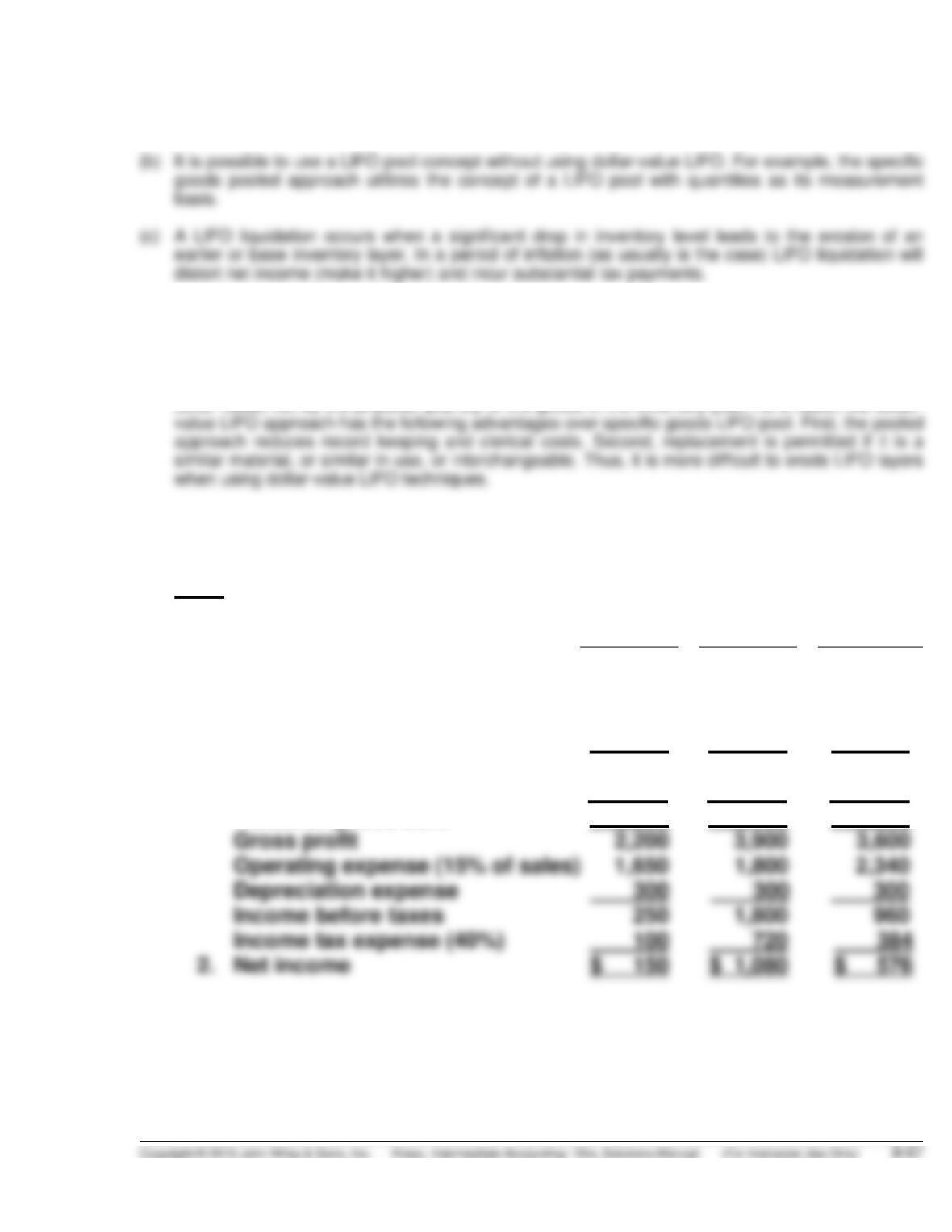

CA 8-9

(a) A LIFO pool is a group of similar items which are combined and accounted for together under the

LIFO inventory method.

(d) Price indexes are used in the dollar-value LIFO method to: (1) convert the ending inventory at

current year-end cost to base-year cost, and (2) determine the current-year cost for each inventory

layer other than the base-year layer.

(e) The dollar-value LIFO method measures the increases and decreases in a pool in terms of total

dollar value, not by the physical quantity of the goods in the inventory pool. As a result, the dollar–

CA 8-10

(a) FIFO (Amounts in thousands, except earnings per share)

2014

2015

2016

Sales revenue

$11,000

$12,000

$15,600

Cost of goods sold

Beginning inventory

8,000

7,200

9,000

Purchases

8,000

9,900

12,000

Cost of goods available for sale

16,000

17,100

21,000

1. Ending inventory*

(7,200)

(9,000)

(9,000)

Cost of goods sold

8,800

8,100

12,000

Gross profit

2,200

3,900

3,600

Operating expense (15% of sales)

Depreciation expense

300

Income before taxes

250

1,800

Income tax expense (40%)

100

720

2. Net income

$ 150

$ 1,080

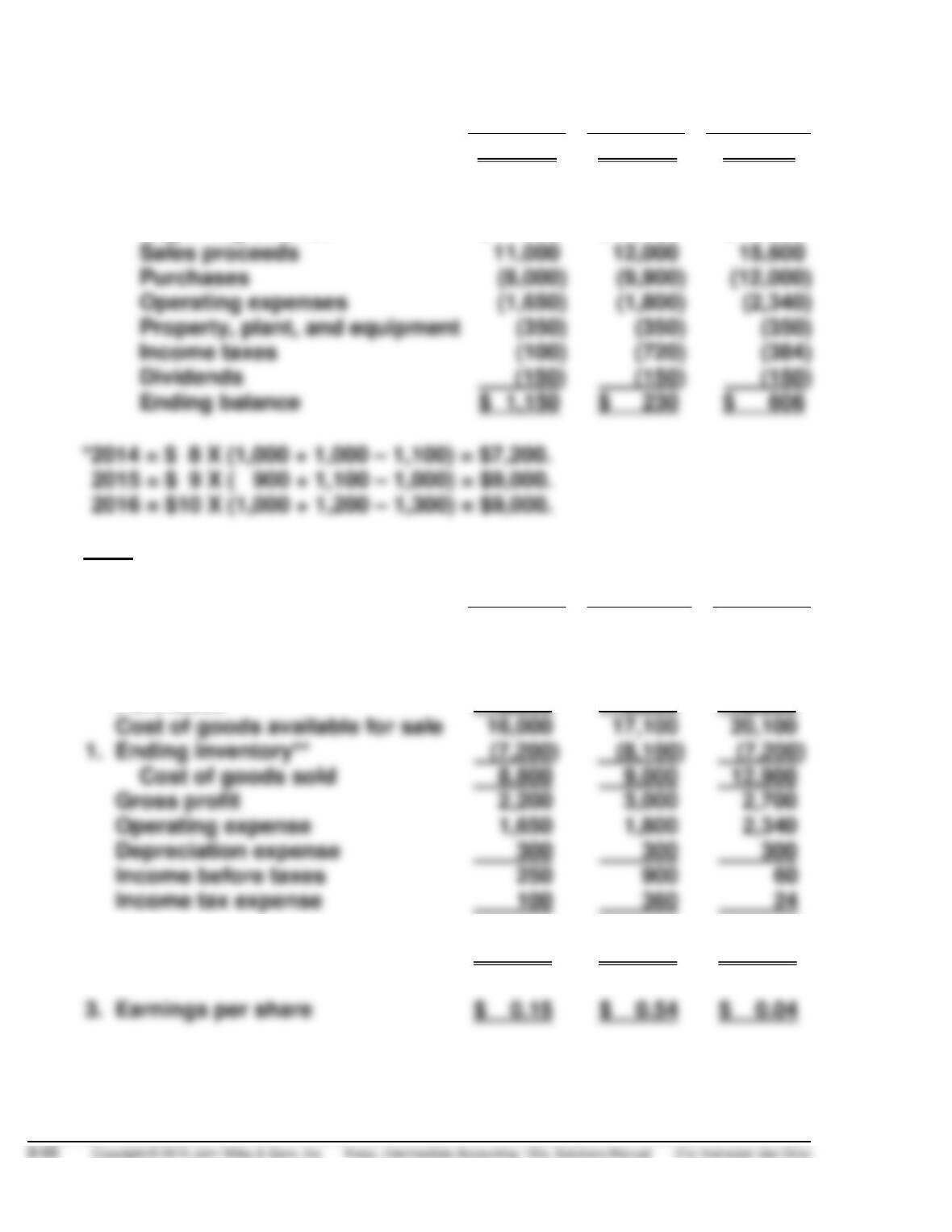

CA 8-10 (Continued)

2014

2015

2016

3. Earnings per share

$ 0.15

$ 1.08

$ 0.58

4. Cash balance

Beginning balance

$ 400

$ 1,150

$ 230

Sales proceeds

Purchases

Operating expenses

Property, plant, and equipment

Income taxes

(100)

(720)

Dividends

(150)

Ending balance

LIFO (Amounts in thousands, except earnings per share)

2014

2015

2016

Sales revenue

$11,000

$12,000

$15,600

Cost of goods sold

Beginning inventory

8,000

7,200

8,100

Purchases

8,000

9,900

12,000

Cost of goods available for sale

16,000

20,100

1. Ending inventory**

(7,200)

Cost of goods sold

8,800

9,000

12,900

Gross profit

2,200

3,000

2,700

Operating expense

Depreciation expense

300

300

300

Income before taxes

900

2. Net income

$ 150

$ 540

$ 36

3. Earnings per share

$ 0.15

$ 0.54

$ 0.04

CA 8-10 (Continued)

2014

2015

2016

4. Cash balance

Beginning balance

$ 400

$ 1,150

$ 590

Sales proceeds

11,000

12,000

15,600

Operating expenses

Dividends

(b) According to the computation in (a), Harrisburg Company can achieve

the goal of income tax savings by switching to the LIFO method. As

shown in the schedules, under the LIFO method, Harrisburg will have

CA 8-11

(a) Major stakeholders are investors, creditors, Wilkens’ management

(including the president and plant accountant), and other employees

of Wilkens Company. The inventory purchase in this instance reduces

net income substantially and lowers Wilkens Company’s tax liability.

(b) No, the president would not recommend a year-end inventory pur–

chase because under FIFO there would be no effect on net income.

FINANCIAL STATEMENT ANALYSIS CASE 1

(a)

Sales ………………………………………………………………

$618,876,000

Cost of goods sold* …………………………………………

474,206,000

Gross profit …………………………………………………….

144,670,000

Selling and administrative expense …………………..

Income from operations …………………………………..

Other expense …………………………………………………

Income before income tax ………………………………..

$ 17,846,000

$475,476,000

(b) $17,846,000 income before taxes X 46.6% tax = $8,316,236 tax;

(c) No, the use of different costing methods does not necessarily mean

that there is a difference in the physical flow of goods. As explained

the physical flow of the goods.

FINANCIAL STATEMENT ANALYSIS CASE 2

(a) The most likely physical flow of goods for a pharmaceutical manufac-

turer would be FIFO; that is, the first goods manufactured would be the

(b) Noven should consider first whether the inventory costing method

will make a difference. If the prices in the economy, especially if the

(c) This amount is likely not shown in a separate inventory account

because it is immaterial; that is, it is not large enough to make a differ-

ence with investors. Another possible reason is that no goods have yet

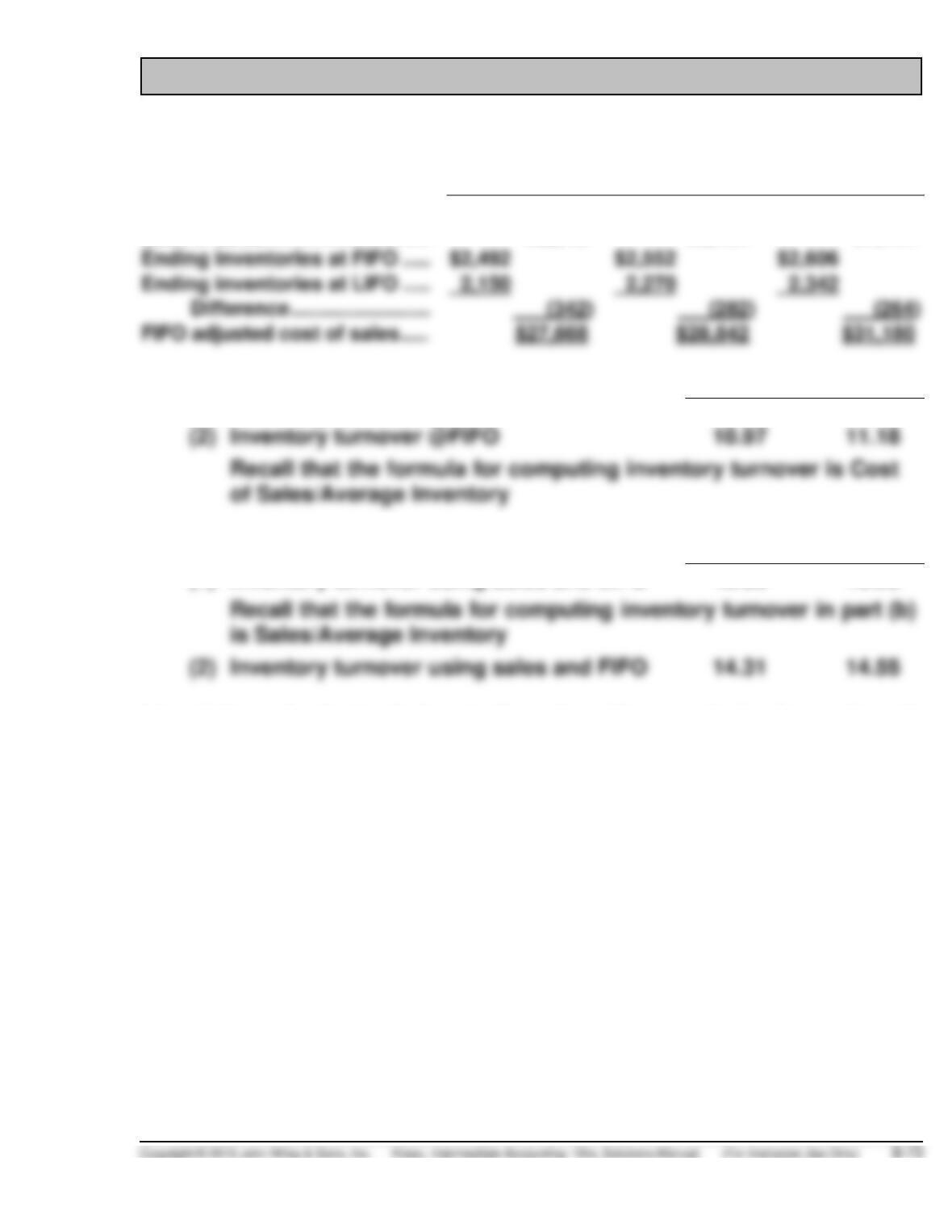

FINANCIAL STATEMENT ANALYSIS CASE 3

Feb. 25

Feb. 26

Feb. 27

2012

2011

2010

Revenues …………………………..…

$36,100

$37,534

$40,597

Cost of sales …………………………

28,010

29,124

31,444

(264)

FIFO adjusted cost of sales …….

(a)

2012

2011

(1)

Inventory turnover @LIFO

12.67

12.63

(2)

Inventory turnover @FIFO

11.18

(b)

2012

2011

(1)

Inventory turnover using sales and LIFO

16.33

16.28

(2)

Inventory turnover using sales and FIFO

14.55

(c) Using sales instead of cost of goods sold accounts for the mark-up in

the inventory. By using cost of goods sold, there is a better matching

of the costs associated to inventory, and should result in more useful

information.

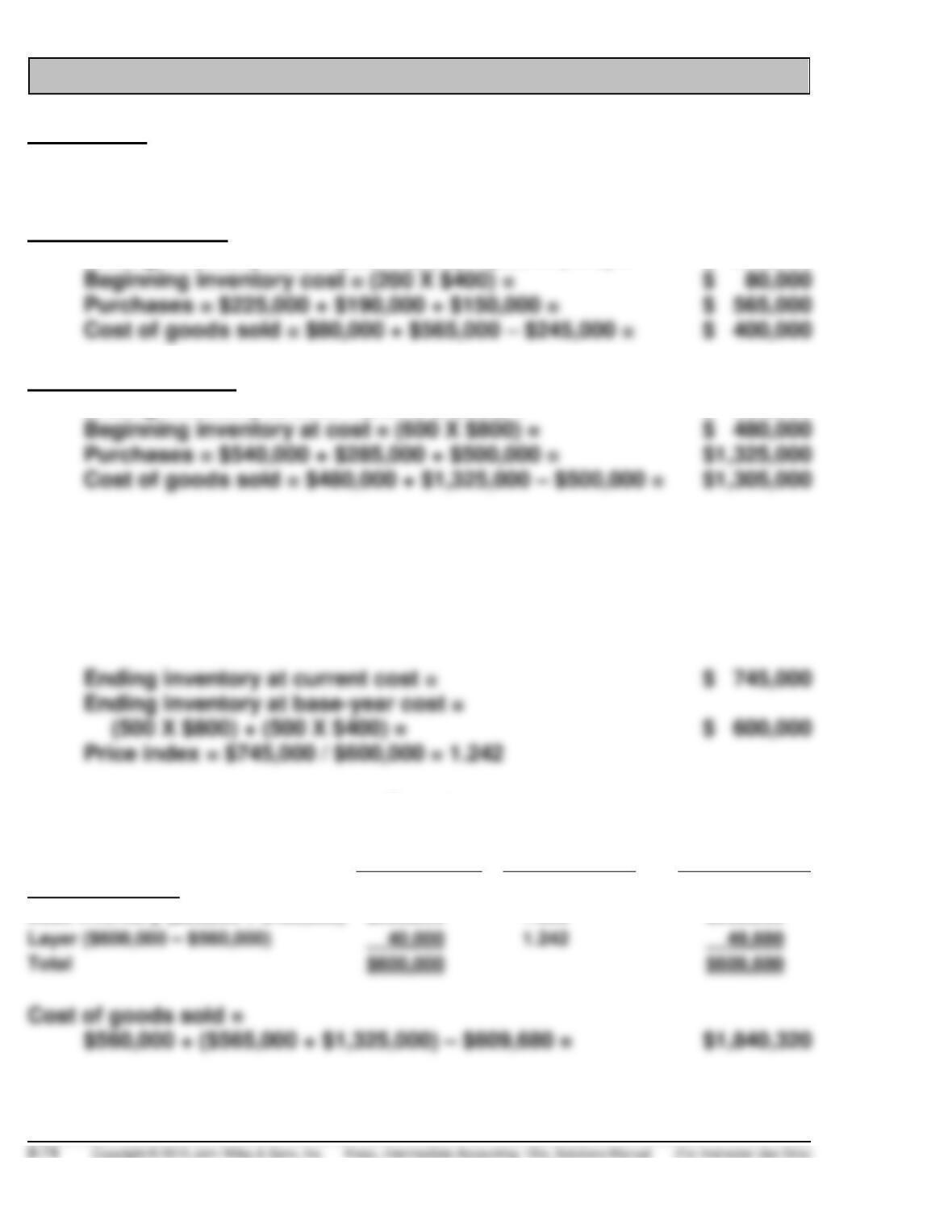

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

(a) FIFO

Residential pumps:

Ending inventory cost = (300 X $500) + (200 X $475) = $ 245,000

Commercial pumps:

Ending inventory at cost = (500 X $1,000) = $ 500,000

Total ending inventory at cost = $245,000 + $500,000 = $ 745,000

Total cost of goods sold = $1,305,000 + $400,000 = $1,705,000

(b) Dollar-value LIFO (one pool)

Current

Inventory at

base cost

Conversion

price index

Inventory at

LIFO cost

Ending inventory

Base inventory ($80,000 + $480,000)

$560,000

1.000

$560,000

Layer ($600,000 – $560,000)

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Analysis

(a) The purpose of a current ratio is to provide some indication of the

resources the company has available to meet short term obligations,

lower values.

(b) The U.S. Securities and Exchange Commission requires companies

using LIFO to disclose the current cost of their inventories. Many

Principles

Companies can change from one inventory accounting method to

another, but not back and forth. Changes in accounting method (when

not mandated by a regulatory body such as the FASB) should be to

PROFESSIONAL RESEARCH

(a) According to FASB ASC 605-15-15:

15-2 The guidance in this Subtopic applies to the following

transactions:

a. Sales in which a product may be returned, whether as a

matter of contract or as a matter of existing practice, either

by the ultimate customer or by a party who resells the

b. Sales by a manufacturer who repurchases the product subject

to an operating lease with the buyer.

(b) The guidance in this subtopic (FASB ASC 605-15-15) does not apply to

the following transactions:

c. Sales transactions in which a customer may return defective goods,

such as under warranty provisions. (See Topic 460 regarding war–

PROFESSIONAL RESEARCH (Continued)

> Right of Return (FASB ASC 605-15)

05-3 It is the practice in some industries for customers to be given the

right to return a product to the seller under certain circumstances.

(c) Yes, different industries should be allowed to make different types of

policies. (FASB ASC 605-15-05).

05-4 Sometimes, the returns occur very soon after a sale is made, as

(d) According to FASB ASC 605-15-25:

25-3 The ability to make a reasonable estimate of the amount of future

returns depends on many factors and circumstances that will vary

from one case to the next. However, any of the following factors

may impair the ability to make a reasonable estimate:

PROFESSIONAL RESEARCH (Continued)

25-4 The existence of one or more of the factors in the preceding

PROFESSIONAL SIMULATION

Explanation

To: Norwel Management

From: Student

Re: Advantages of LIFO

The major advantages of the LIFO inventory method include better matching

of costs with revenues, deferral of income taxes, improved cash flow, and

minimization of the impact of future price declines on future earnings.