PROBLEM 18-11B

(a) Installment Accounts Receivable …………………….. 600,000

Installment Sales Revenue ……………………….. 600,000

Cash ………………………………………………………………. 210,000

Installment Accounts Receivable ……………… 210,000

PROBLEM 18-12B

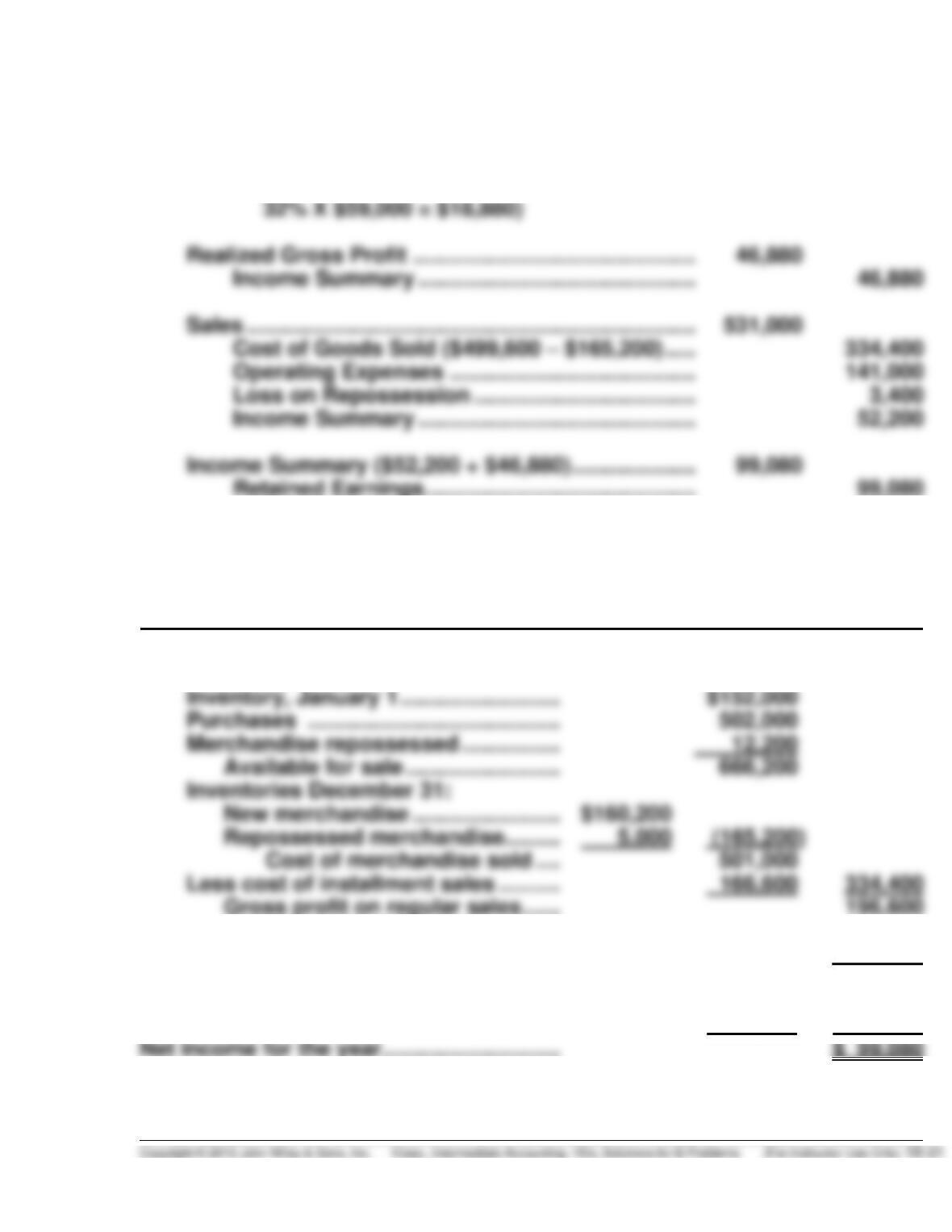

(a) Rate of gross profit—2014:

Deferred gross profit beginning of year

$70,000 + $8,400 = $78,400

Accounts receivable beginning of year

PROBLEM 18-12B (Continued)

Deferred Gross Profit (2014) ………………………………. 28,000

Deferred Gross Profit (2015) ………………………………. 18,880

Realized Gross Profit ………………………………….. 46,880

(35% X $80,000 = $28,000;

(b) STAR INC.

Income Statement

For the Year Ended December 31, 2015

Sales ………………………………………………….. $531,000

Cost of goods sold:

Gross profit realized on

installment sales …………………. 46,880

Total gross profit realized …. 243,480

Operating expenses ……………………………. 141,000

Loss on repossession ………………………… 3,400 144,400

-1-

November 1, 2014

-2-

-3-

December 31, 2014

Cost of Installment Sales ………………………………………………. 728

-4-

-5-

May, 2015

PROBLEM 18-13B (Continued)

Balance at repossession ………….. $500*

PROBLEM 18-14B

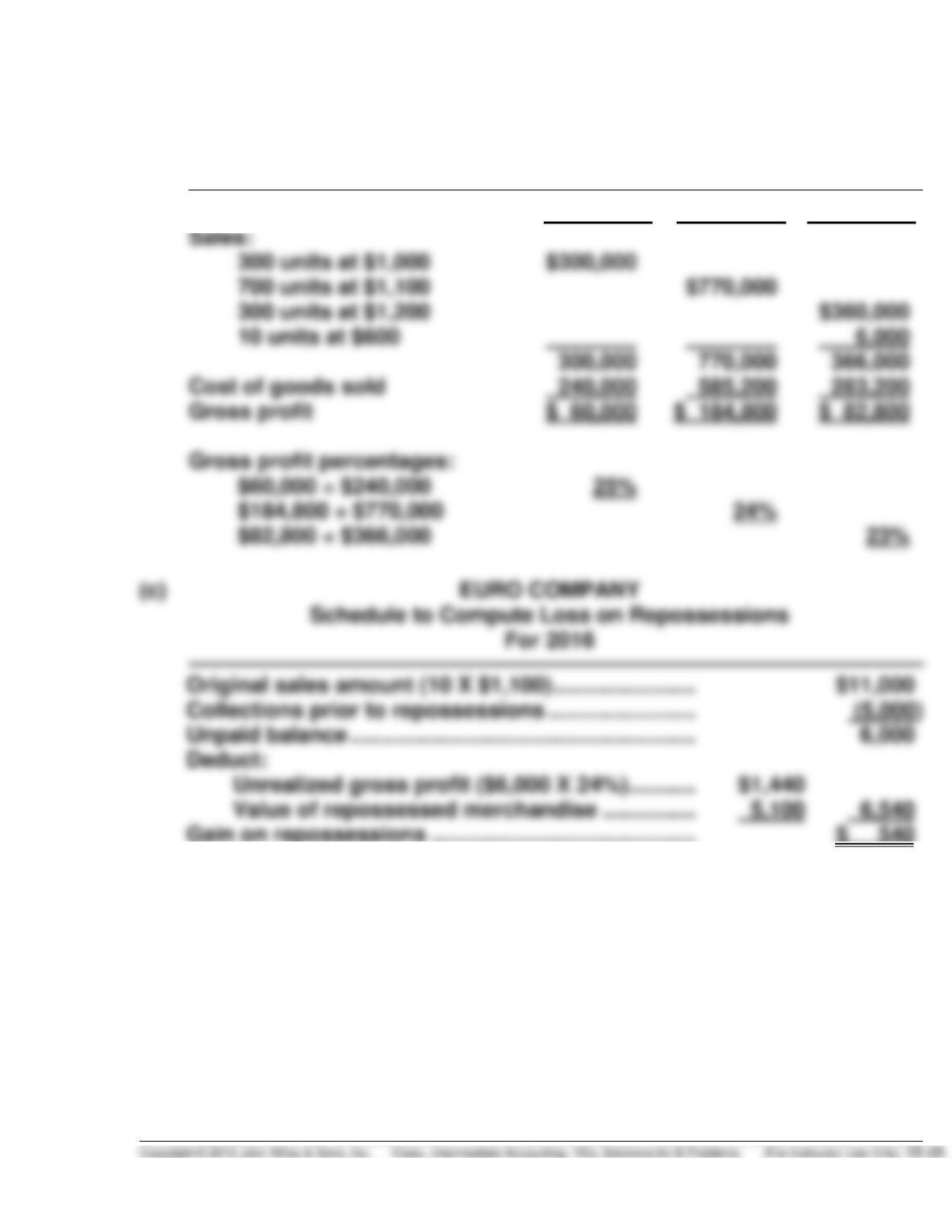

(a) 1. EURO COMPANY

Schedule to Compute Cost

of Goods Sold on Installments

2. EURO COMPANY

Schedule to Compute Average Unit Cost

of Goods Sold on Installments

PROBLEM 18-14B (Continued)

(b) EURO COMPANY

Schedule to Compute Gross Profit Percentages

For 2014, 2015, and 2016

2014

2015

2016

Sales:

Cost of goods sold

Gross profit percentages:

$82,800 ÷ $366,000

PROBLEM 18-14B (Continued)

(d) EURO COMPANY

Schedule to Compute Net Income

From Installment Sales

PROBLEM 18-15B

(a) DOLPHIN CONSTRUCTION COMPANY, INC.

Computation of Costs on Uncompleted Contract

In Excess of Related Billings

December 31, 2014

PROBLEM 18-15B (Continued)

DOLPHIN CONSTRUCTION COMPANY, INC.

Computation of Costs Relating to Substantially

Completed Contract in Excess of Billings

December 31, 2016

Balance, December 31, 2016 …………………………………….. $ 200,000

(b) DOLPHIN CONSTRUCTION COMPANY, INC.

Computation of Profit or Loss to be Recognized

On Uncompleted Contract

Year Ended December 31, 2014

PROBLEM 18-15 (Continued)

DOLPHIN CONSTRUCTION COMPANY, INC.

Computation of Loss to be Recognized

On Uncompleted Contract

Year Ended December 31, 2015

PROBLEM 18-16B

Dear Kim:

This letter regards the revenue recognition matter which we discussed earlier.

By using a recognition method called percentage-of-completion, you will

show a profit in every year of the construction project, assuming, of course,

contract will be completed.)

The most frequently used measure of this degree of completion is the cost–

to-cost method, which determines the percentage of a project’s completion

as the ratio of costs that have already been incurred to the total estimated

costs required in order to finish the project. This percentage is then applied

PROBLEM 18-16B (Continued)

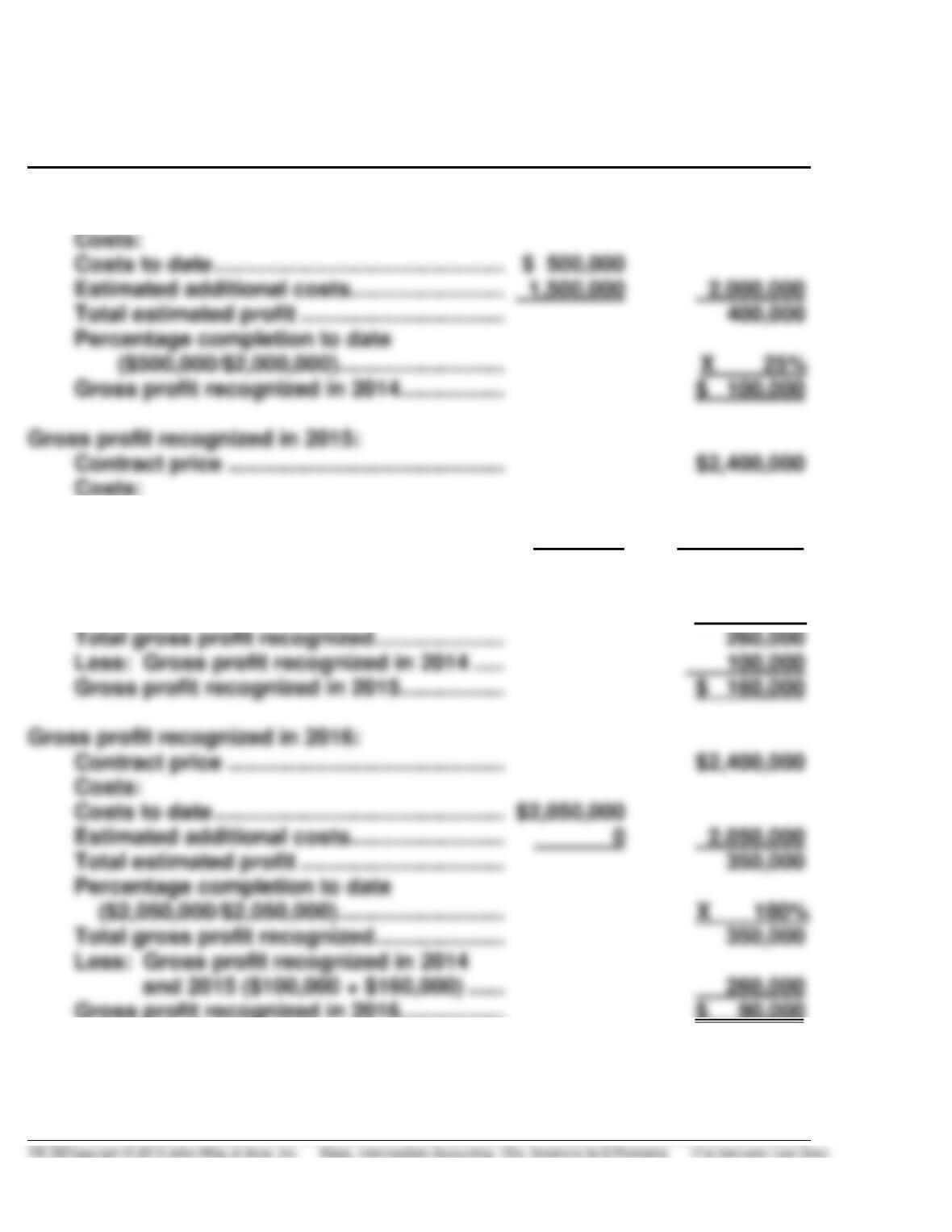

2014 and 2015 actually allow you to show a profit before the project has been

PROBLEM 18-16B (Continued)

Percentage-of–Completion Method

Three-Year Schedule of Gross Profit Recognition

Gross profit recognized in 2014:

Contract price ……………………………………… $2,400,000

Costs to date …………………………..…………… $1,300,000

Estimated additional costs ……………………. 700,000 2,000,000

Total estimated profit …………………………... 400,000

Percentage completion to date

($1,300,000/$2,000,000) ……………………… X 65%

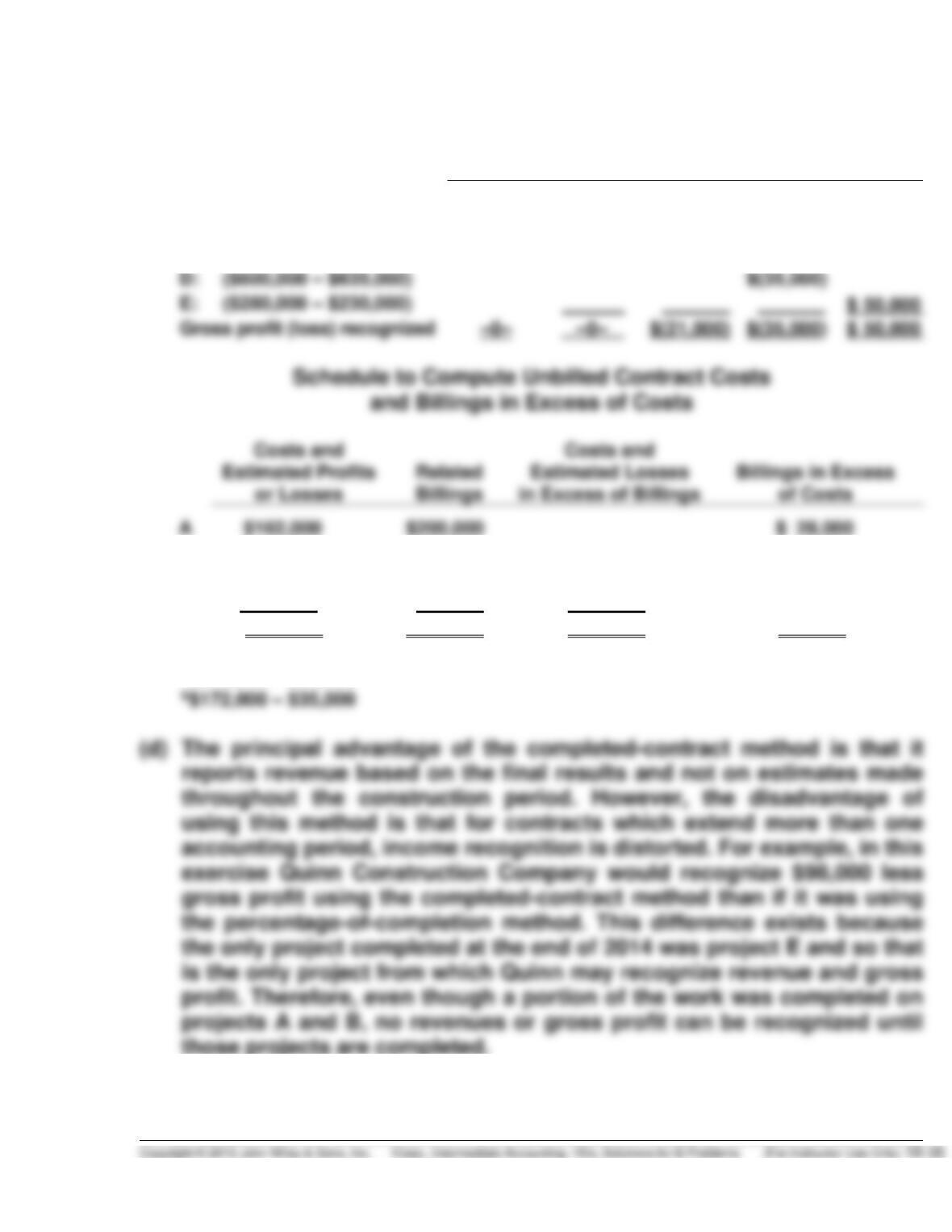

PROBLEM 18-17B

(a) Schedule to Compute Gross Profit for 2014

A

B

C

D

E

Estimated profit (loss):

A: ($200,000 – $180,000)

$20,000

B: ($500,000 – $400000)

$100,000

C: ($360,000 – $381,000)

$(21,000)

D: ($600,000 – $635,000)

$(35,000)

A: ($162,000 ÷ $180,000)

B: ($320,000 ÷ $400,000)

C: (not applicable)

D: (not applicable)

Gross profit (loss) recognized

$18,000

$(21,000)

$(35,000)

C

D

37,000

PROBLEM 18-17B (Continued)

(b) Partial Income Statement

Revenue from long-term contracts …………………………………. $1,305,985*

Costs of construction

($162,000 + $320,000 + $304,465 + $197,520 + $230,000) .. 1,213,985

($1,110,000 – $815,000) ……………………….. $ 295,000

Inventories

Construction in process …………………………. $816,000***

Less: Billings ………………………………………… 630,000***

Costs and recognized profits

PROBLEM 18-17B (Continued)

(c) Schedule to Compute Gross Profit for 2014

A

B

C

D

E

A: Not completed

–0–

B: Not completed

–0–

C: ($360,000 – $381,000)

$(21,000)

D: ($600,000 – $635,000)

Gross profit (loss) recognized

$(21,000)

B

320,000

280,000

$40,000

C

279,000 a

250,000

29,000

D

137,000 b

100,000

37,000

$898,800

$830,000

$106,000

$28,000

a$300,000 – $21,000

PROBLEM 18-17B (Continued)

On the other hand, the percentage-of-completion method does recog-

nize revenue and gross profit before the completion of a project. If

Quinn can determine reliable estimates of its progress and meets the