Continuing Case Solution

Chapter 10

Memorandum

To: Eric Conner and Phil Martin, CM2

From: L. Harbach

Re: Equipment Replacement

Date: January 16, 2013

I have analyzed the four options you presented for handling the old equipment,

Option 1: Self-construction of new equipment

Journal Entries

DR CR

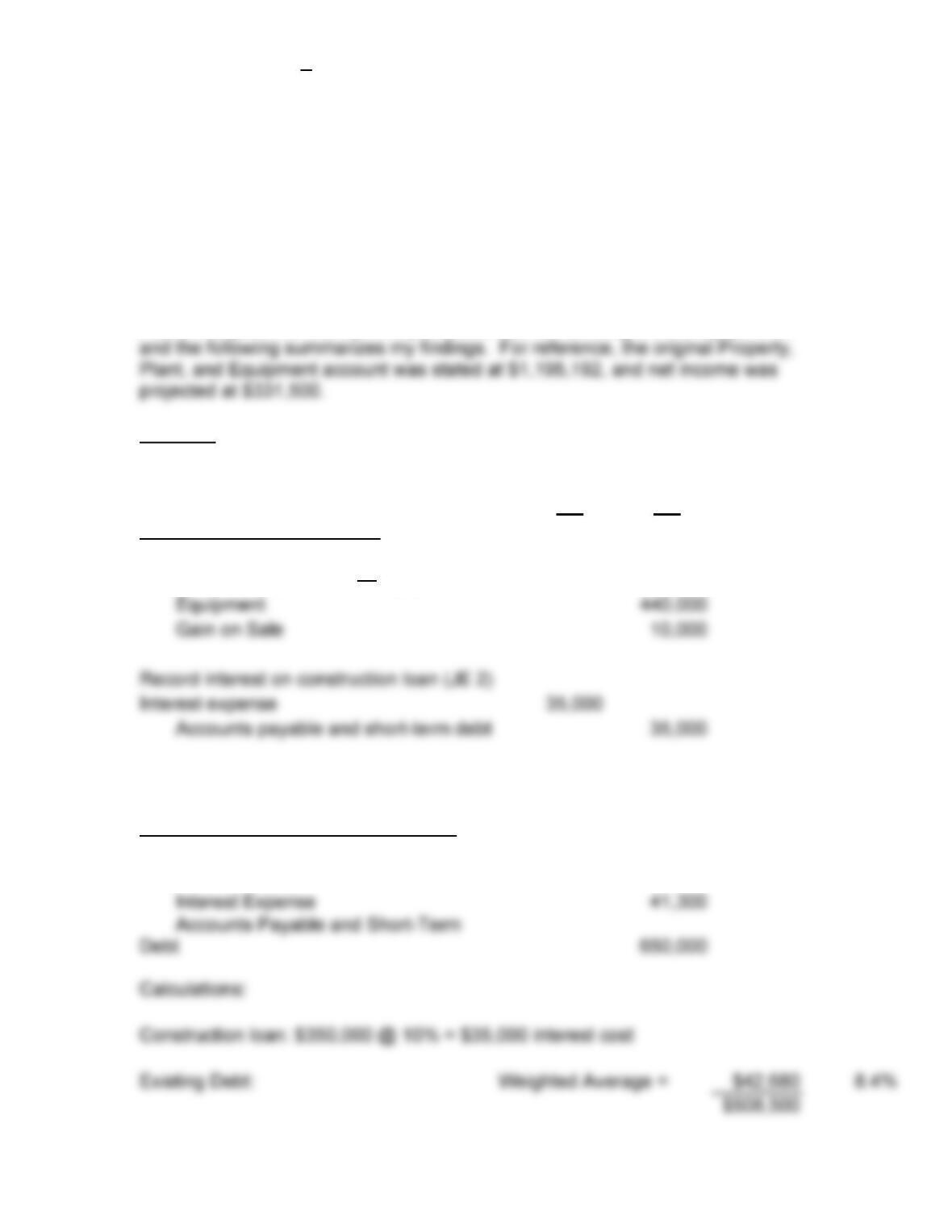

Sale of old equipment (JE 1):

Cash

60,000

Accumulated Depreciation Equipment

390,000

440,000

term debt

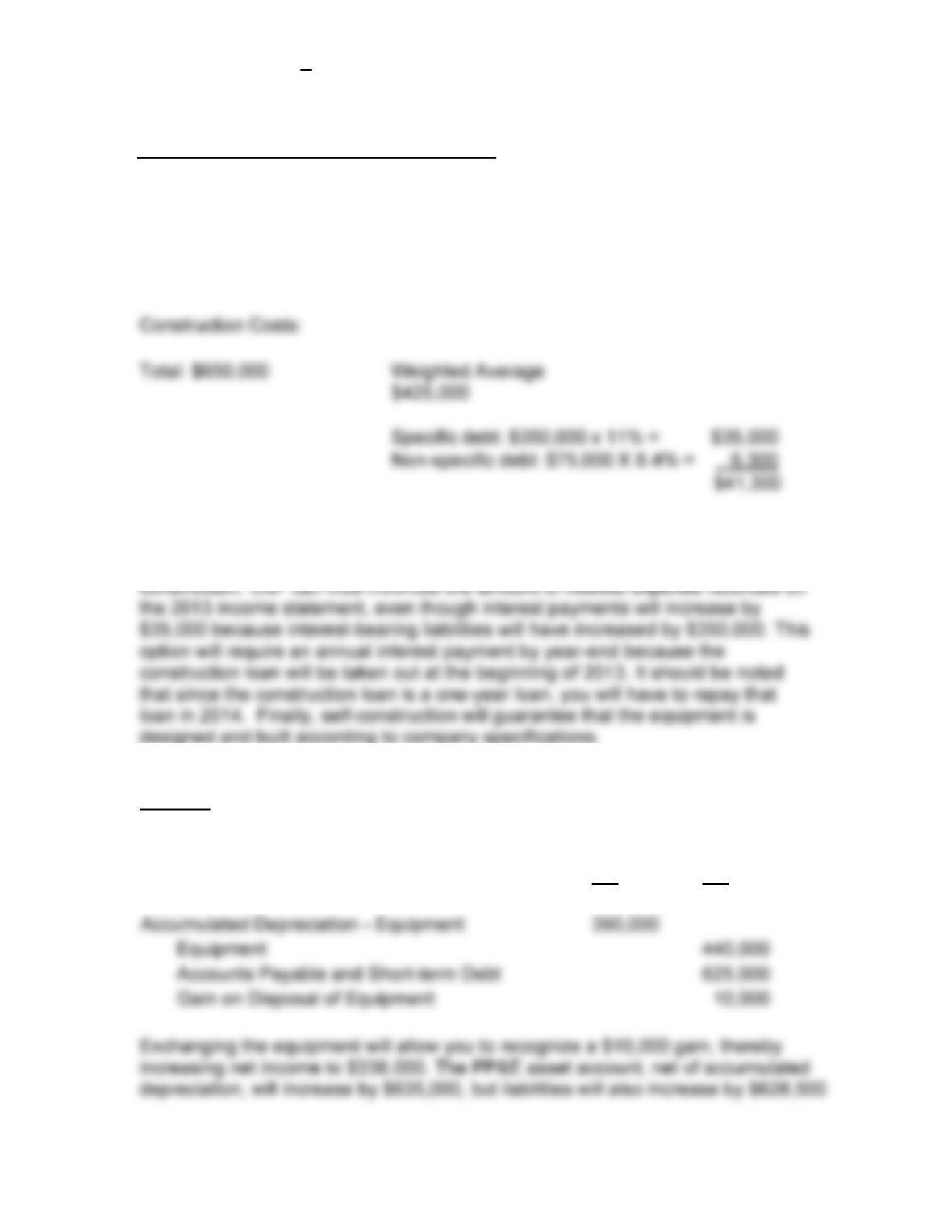

Construction of new equipment (JE 3):

Equipment (new) 691,300 ($650,000 + $41,300)

$42,680

Continuing Case Solution

$200,000 @ 9% =

$18,000

$308,500 @ 8% =

$24,680

$508,500

$42,680

Actual interest costs = $35,000 + $18,000 + $24,680 = $77,680

Interest expense after considering capitalized interest: = $77,680 –

$41,300 = $36,380

Self-constructing the equipment will allow you to increase the Property, Plant,

and Equipment account, net of accumulated depreciation by $691,300. This

method will also allow you to capitalize the interest costs associated with

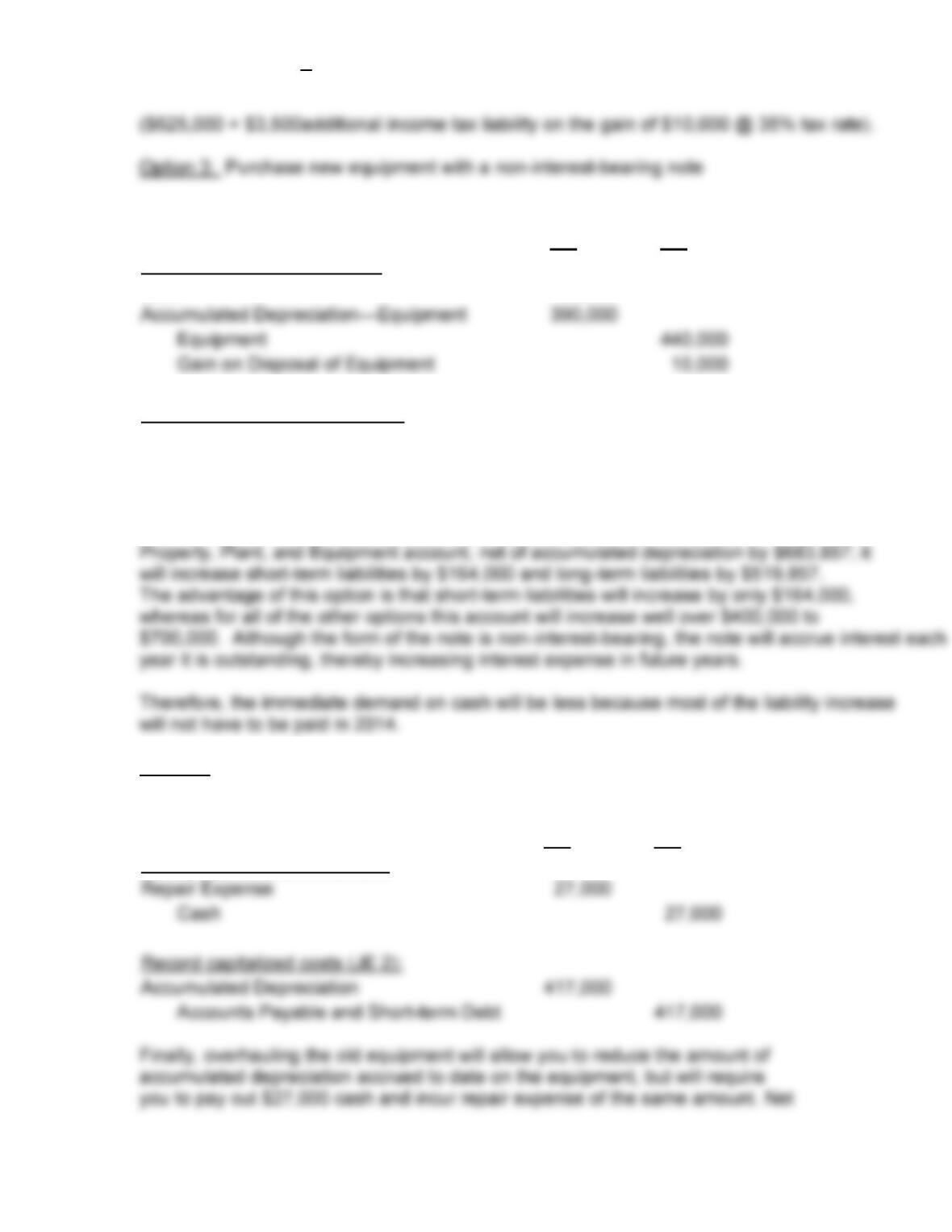

Option 2: Exchange the old equipment for new equipment

Journal Entries

DR CR

Equipment

685,000

Continuing Case Solution

Journal Entries

DR CR

Sale of old equipment (JE 1):

Cash

60,000

440,000

Acquisition of equipment (JE 2):

Equipment 683,857

Accounts Payable and Short–

Term Debt

164,000

Long-term Liabilities 519,857

Purchasing new equipment with a non-interest-bearing note will increase the

Option 4: Overhauling the old equipment

Journal Entries

DR CR

Record repair expense (JE 1):

Continuing Case Solution

income will be $313,950. Total liabilities will increase by $417,000, but this

amount is considerably less than the liability increase reflected in the other options. This is an

Qualitative Considerations

It is also important to take into consideration the non-financial elements of

replacing the equipment. New equipment and technology may allow CM2 to

operate more efficiently, but a consequence may be layoffs of skilled labor.