CHAPTER 20

SOLUTIONS TO B EXERCISES

E20-1B (5–10 minutes)

(a)

Computation of pension expense:

Service cost …………………………………………………

$250,000

Interest cost ($2,600,000 X 0.08) ……………………

208,000

Actual (expected) return on plan assets ………..

Prior service cost amortization ……………………..

40,000

(b) Pension Expense ………………………………………………

433,000

Cash …………………………..……………………………….

E20-2B (10–15 minutes)

Computation of pension expense:

Service cost …………………………………………………

$210,000

Actual (and expected) return on plan assets ….

Prior service cost amortization ……………………..

35,000

Pension expense for 2014 …………………………….

$284,000

E20-3B (15–25 minutes)

McCaw Company

Pension Worksheet—2014

General Journal Entries

Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service Cost

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan Assets

Balance, January 1, 2014

360,000 Cr.

1,800,000 Cr.

1,440,000 Dr.

(a) Service cost

210,000 Dr.

210,000 Cr.

20-2 Copyright © 2014 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 14/e, Exercise B Solutions (For Instructor Use Only)

(b) Interest cost

162,000 Dr.

162,000 Cr.

(c) Actual return

123,000 Cr.

(d) Amortization of PSC

(e) Contributions

263,000 Cr.

220,000 Dr.

Journal entry*

263,000 Cr.

Accumulated OCI, Dec. 31, 2013

325,000 Dr.

Balance, Dec. 31, 2014

290,000 Dr.

1,952,000 Cr.

1,606,000 Dr.

E20-4B (10–15 minutes)

I-PASS CORPORATION

Pension Worksheet—2014

General Journal Entries

Memo Record

Items

Annual

Pension

Expense

Cash

Pension

Asset /

Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, January 1, 2014

950,000 Cr.

950,000 Dr.

(a) Service cost

75,000 Dr.

75,000 Cr.

Copyright © 2014 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 14/e, Exercise B Solutions (For Instructor Use Only) 20-3

(b) Interest cost

57,000 Dr.

57,000 Cr.

(c) Actual return

40,600 Cr.

(d) Contributions

(e) Benefits

91,400 Dr.

81,400 Cr.

81,400 Cr.

958,400 Dr.

E20-5B (15–25 minutes)

Computation of Service-Years

Year

Jane

John

Jimmy

Jenny

Jerry

Total

2014

1

1

1

1

1

5

2015

1

1

1

1

4

2017

1

1

1

3

2018

1

1

2

2019

1

1

6

1

3

6

4

Cost per service-year: $210,000 ÷ 20 = $10,500

Computation of Annual Prior Service Cost Amortization

Year

Total

Service-Years

Cost Per

Service-Years

Annual

Amortization

2014

5

$10,500

$ 52,500

2015

4

2017

3

2018

2

$210,000

E20-6B (10–15 minutes)

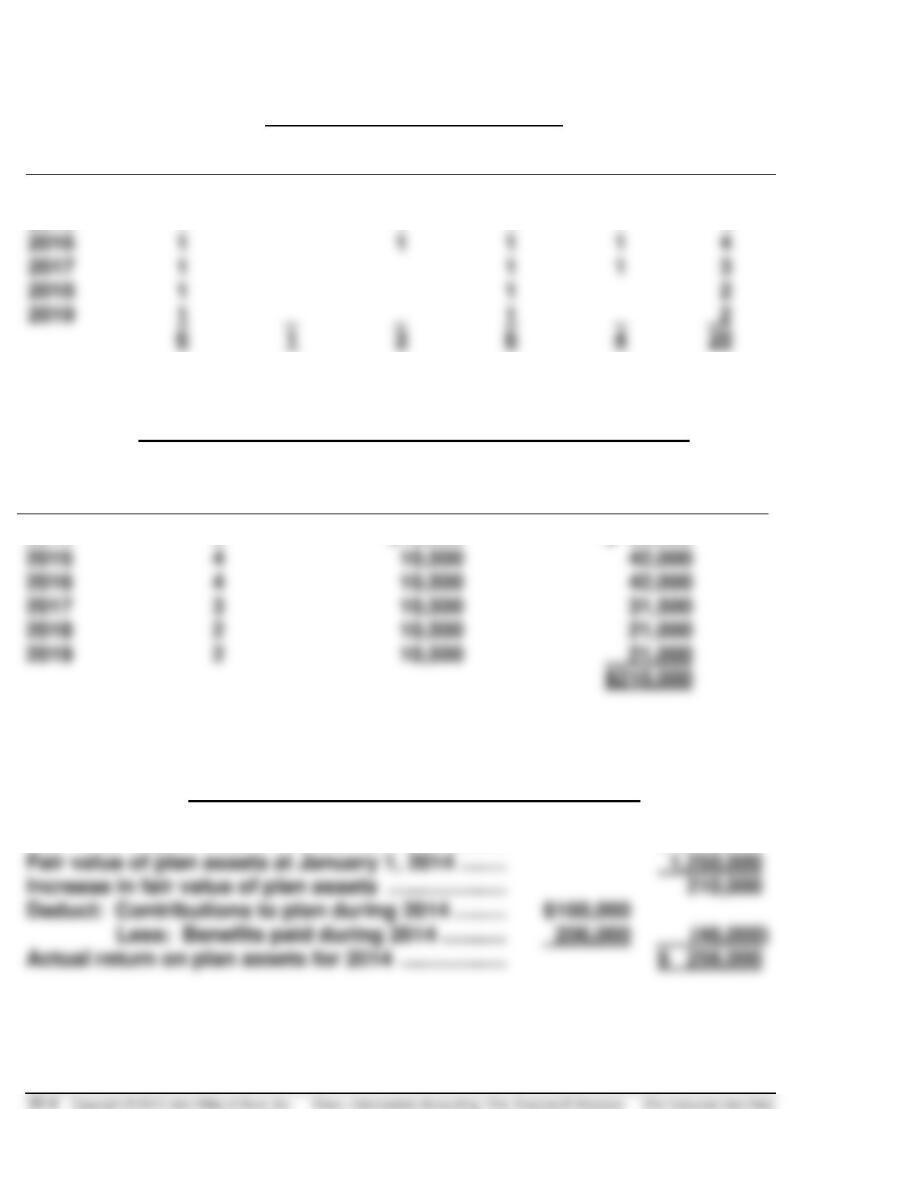

Computation of Actual Return on Plan Assets

Fair value of plan assets at December 31, 2014 … $1,460,000

E20-7B (15–25 minutes)

EAGLE HOMES CORPORATION

Pension Worksheet—2014

General Journal Entries

Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

Pension

Asset/

Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, January 1, 2014

59,400 Cr.

1,255,000 Cr.

1,195,600 Dr.

(a) Prior service cost

200,000 Dr.

200,000 Cr.

New Balance, January 1, 2014

200,000 Dr.

1,455,000 Cr.

1,195,600 Dr.

Copyright © 2014 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 14/e, Exercise B Solutions (For Instructor Use Only) 20-5

(b) Service cost

(c) Interest cost

(d) Actual return

(e) Amortization of PSC

(f) Contributions

85,000 Cr.

(g) Benefits

Journal entry, December 31

85,000 Cr.

175,000 Dr.

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

175,000 Dr.

1,559,300 Cr.

1,272,210 Dr.

E20-8B (20–25 minutes)

Corridor and Minimum Loss Amortization

Projected

Benefit

Plan Asset

10%

Accumulated

Minimum

Amortization

Year

Obligation (a)

Value (a)

Corridor

OCI (G/L)

of Loss

2014

$1,000,000

$ 900,000

$100,000

$ 0

$ 0

2,000,000

E20-9B (25–35 minutes)

(a) Note to financial statements disclosing components of 2014 pension

expense:

(b) Comprehensive income items, 2014

Amortization of prior service cost …………………… $ (36,800)

Unexpected asset loss …………………………………… 26,800

E20-9B (Continued)

(c) Accumulated OCI at December 31, 2014 is $394,800; the amount is

comprised of the following:

E20-10B (20–25 minutes)

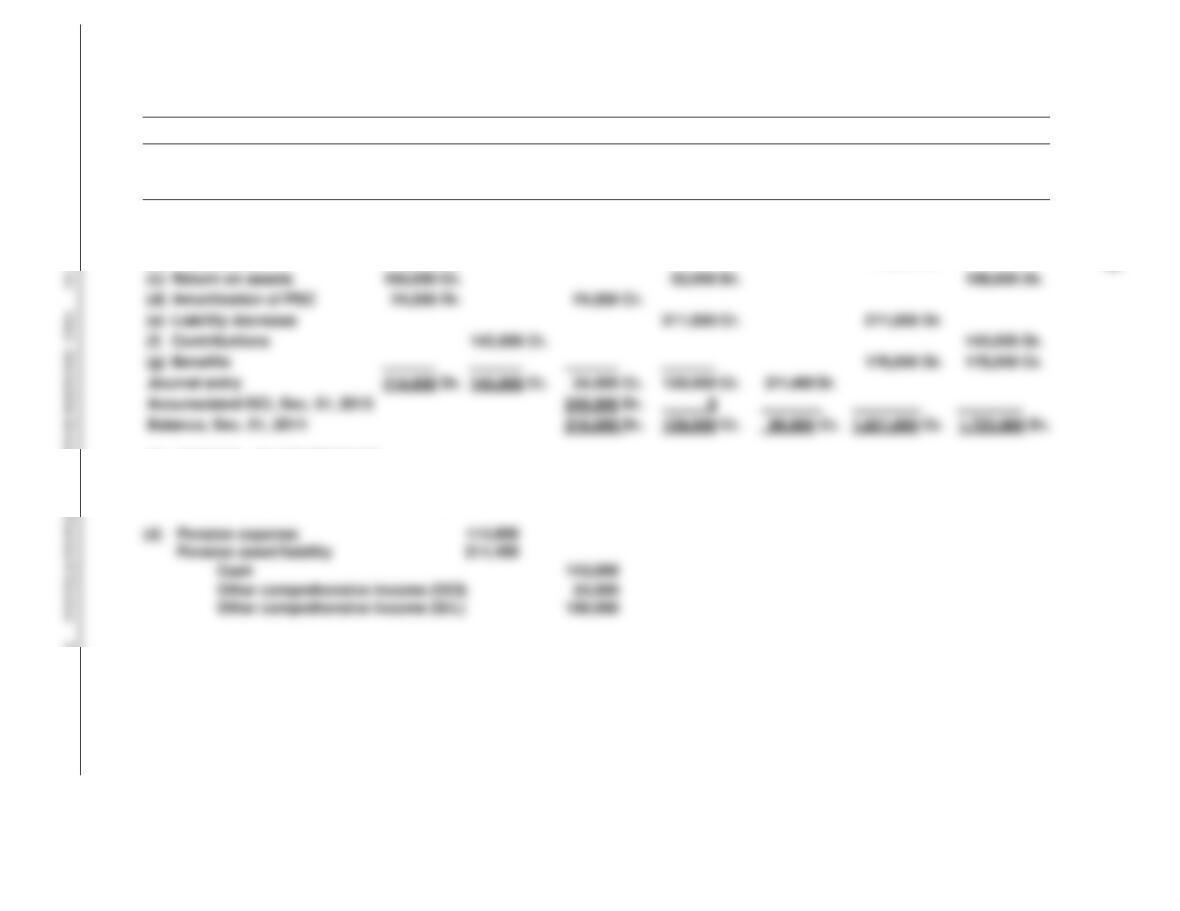

(a) DADE SHUTTERS INC.

Pension Worksheet—2014

General Journal Entries Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service Cost

OCI—Net

Gain or Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan assets

Balance, January 1, 2014

310,000 Cr.

1,960,000 Cr.

1,650,000 Dr.

(a) Service cost

133,000 Dr.

133,000 Cr.

(b) Interest cost

117,600 Dr.

117,600 Cr.

(b) $117,600 = $1,960,000 X 0.06

(c) Expected return = $160,000

Unexpected loss = Actual return – Expected return; $52,000 = $108,000 – $160,000

20-8 Copyright © 2014 John Wiley & Sons Inc Kieso Intermediate Accounting 14/e Exercise B Solutions (For Instructor Use Only)

(c) Return on assets

160,000 Cr.

(d) Amortization of PSC

(e) Liability decrease

211,000 Dr.

(f) Contributions

(g) Benefits

178,000 Dr.

114,600 Dr.

1,821,600 Cr.

1,723,000 Dr.

E20-11B (20–30 minutes)

(a) Pension expense for 2014 composed of the following:

Service cost ……………………………………………………… $186,000

(b) Pension Expense ……………………………………….. 333,000

Pension Asset/Liability ………………………….. 193,000

E20-12B (20–30 minutes)

(a) Pension expense for 2014 was composed of the following:

Service cost ……………………………………………………… $225,000

E20-12B (Continued)

(b) Pension Asset/Liability …………………………... 75,000

Pension Expense ……………………………………. 681,000

Cash …………………………..…………………….. 156,000

(c) Income Statement:

Pension expense ……………………………………………….. $ 681,000

Note: To prove the amounts reported, a worksheet might be prepared as follows:

General Journal Entries Memo Record

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service

Cost

OCI—Net

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Jan. 1, 2014

3,200,000 Cr.

5,000,000 Cr.

1,800,000 Dr.

(a) Service cost

225,000 Dr.

225,000 Cr.

400,000 Dr.

400,000 Cr.

(c) Actual return

144,000 Cr.

200,000 Dr.

(e) Contributions

156,000 Cr.

400,000 Dr.

Journal entry Dec. 31

681,000 Dr.

156,000 Cr.

Accumulated OCI, Dec. 31, 2013

3,200,000 Dr. .

Copyright © 2014 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 14/e, Exercise B Solutions (For Instructor Use Only) 20–11

E20-13B (35–45 minutes)

(a) Actual Return = (Ending – Beginning) – (Contributions – Benefits)

Fair value of plan assets,

December 31, 2014 …………………………..…… $740

(b) Computation of pension liability gains and losses and pension asset gains

and losses.

1. Difference between 12/31/14 actuarially computed PBO and 12/31/14

recorded projected benefit obligation (PBO):

Liability loss ………………………….. $0

2. Difference between actual fair value of plan assets and expected fair

value:

12/31/14 actual fair value

(c) Because no net gain or loss existed at the beginning of the period, no

amortization occurs. Therefore, the corridor calculation is not needed. An