PROBLEM 18-1B

(a) 1. The point of sale method recognizes revenue when the earnings

2. The completion–of–production method recognizes revenue only when

the project is complete and the contract is completed. This is used

primarily with short-term contracts, or with long–term contracts when

3. The percentage–of-completion method of revenue recognition is

used on long-term projects, usually construction. To apply it, the

following conditions must exist:

(i) A firm contract price with a high probability of collection.

PROBLEM 18-1B (Continued)

recognized to that date. That total less the income that was recog-

4. The installment-sales method may be applicable when the sales

price is received over an extended period of time. The installment–

sales method recognizes revenue as the cash is collected and is used

when the collection of the sales price is not reasonably assured.

This method is commonly used for tax purposes, but it is not in

PROBLEM 18-1 (Continued)

Oracle Books Division

Sales—fiscal 2014 …………………………………………………. $15,000,000

Less: Sales returns and allowances (25%) ……………… 3,250,000

Net sales—revenue to be recognized in fiscal 2014 …. $11,750,000

PROBLEM 18-2B

(a)

2014

2015

2016

Contract price

$3,000,000

$3,000,000

$3,000,000

Less estimated cost:

Costs to date

800,000

2,000,000

2,580,000

Estimated cost to complete

—

Estimated total cost

Estimated total gross profit

$ 420,000

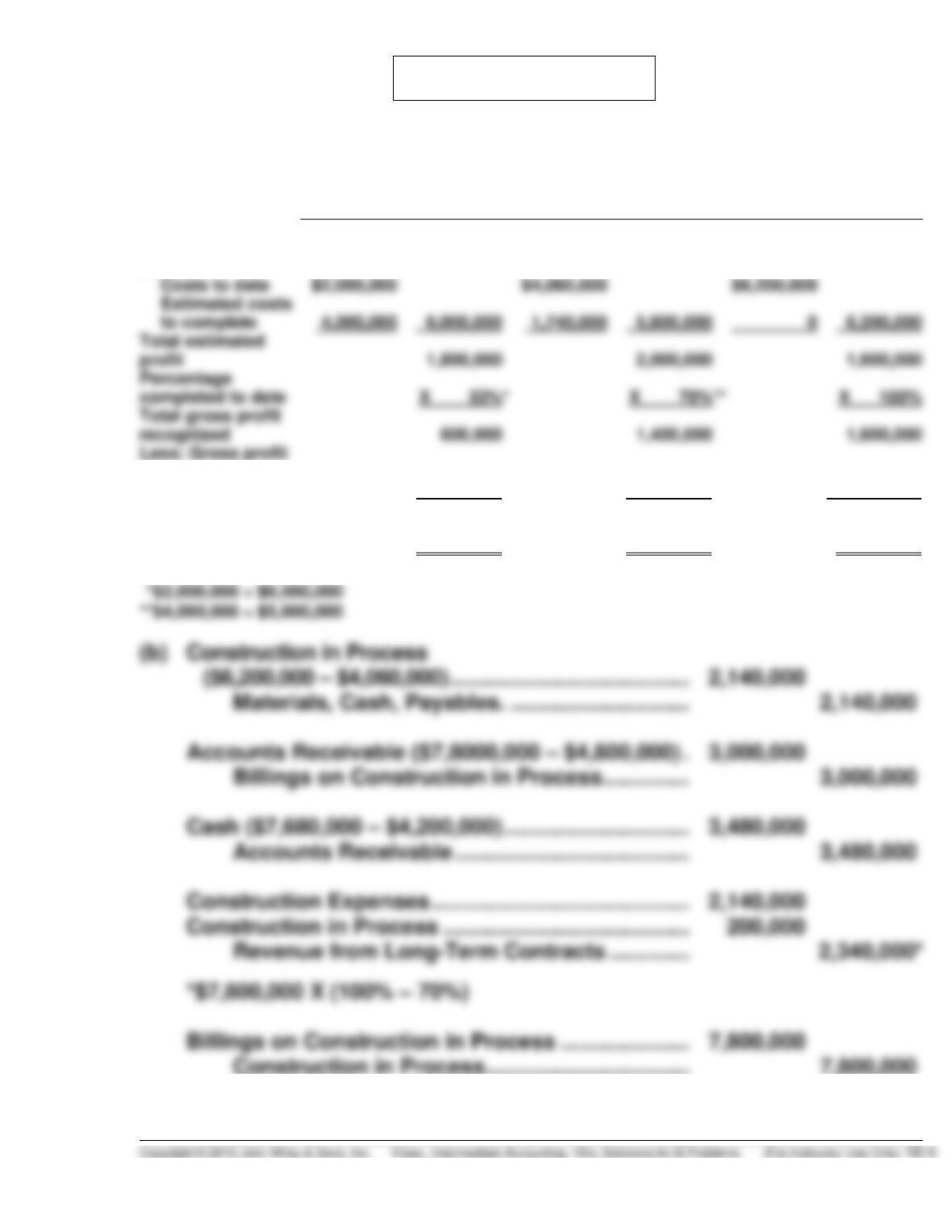

PROBLEM 18-3B

(a) Gross profit recognized in:

2014

2015

2016

Contract price

$7,800,000

$7,800,000

$7,800,000

Costs:

$2,000,000

$4,060,000

$6,200,000

0

Total estimated

profit

Total gross profit

recognized

Less: Gross profit

recognized in

previous years

0

600,000

1,400,000

Gross profit

recognized in

current year

$ 600,000

$ 800,000

$ 200,000

PROBLEM 18-3B (Continued)

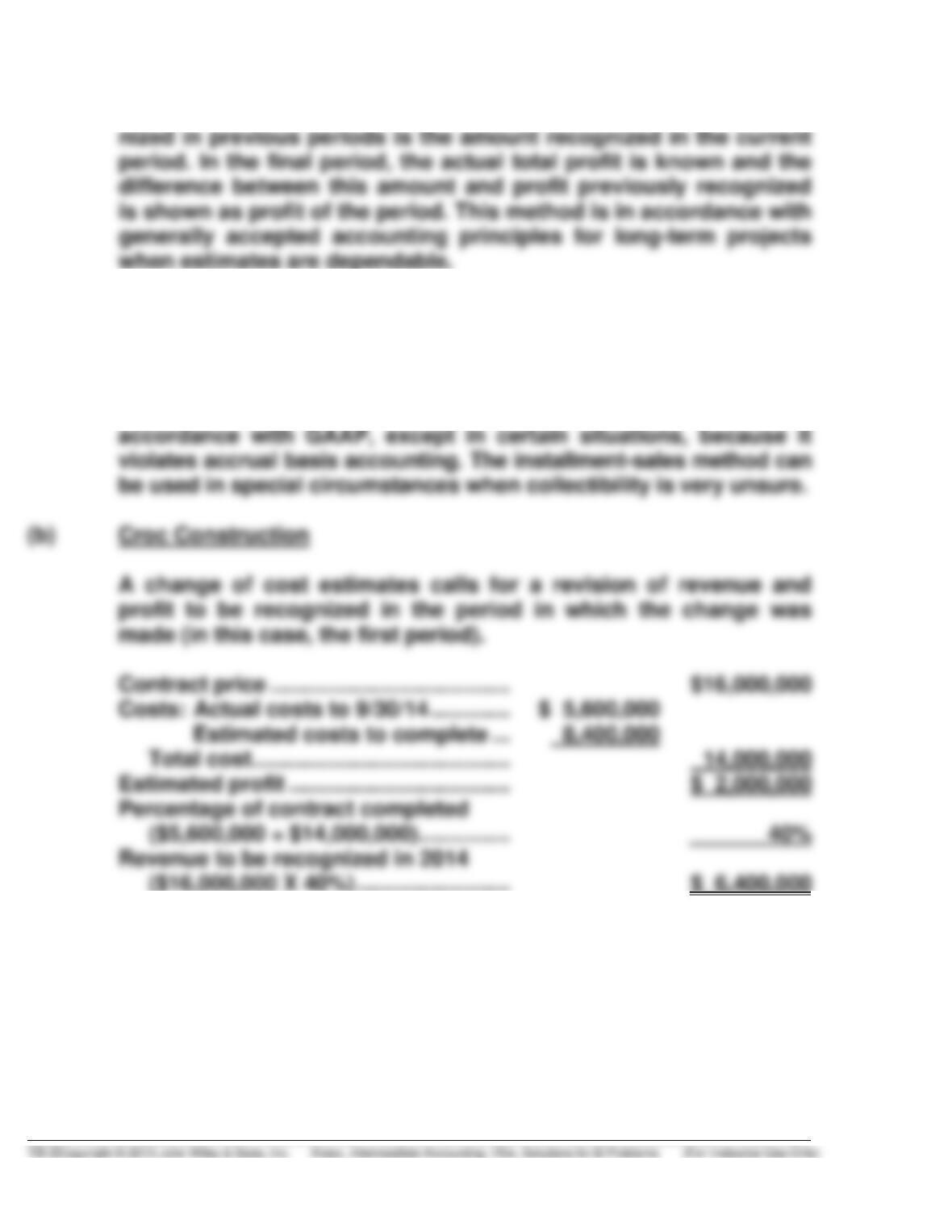

(c) JIAQIAN COMPANY

Balance Sheet (Partial)

December 31, 2015

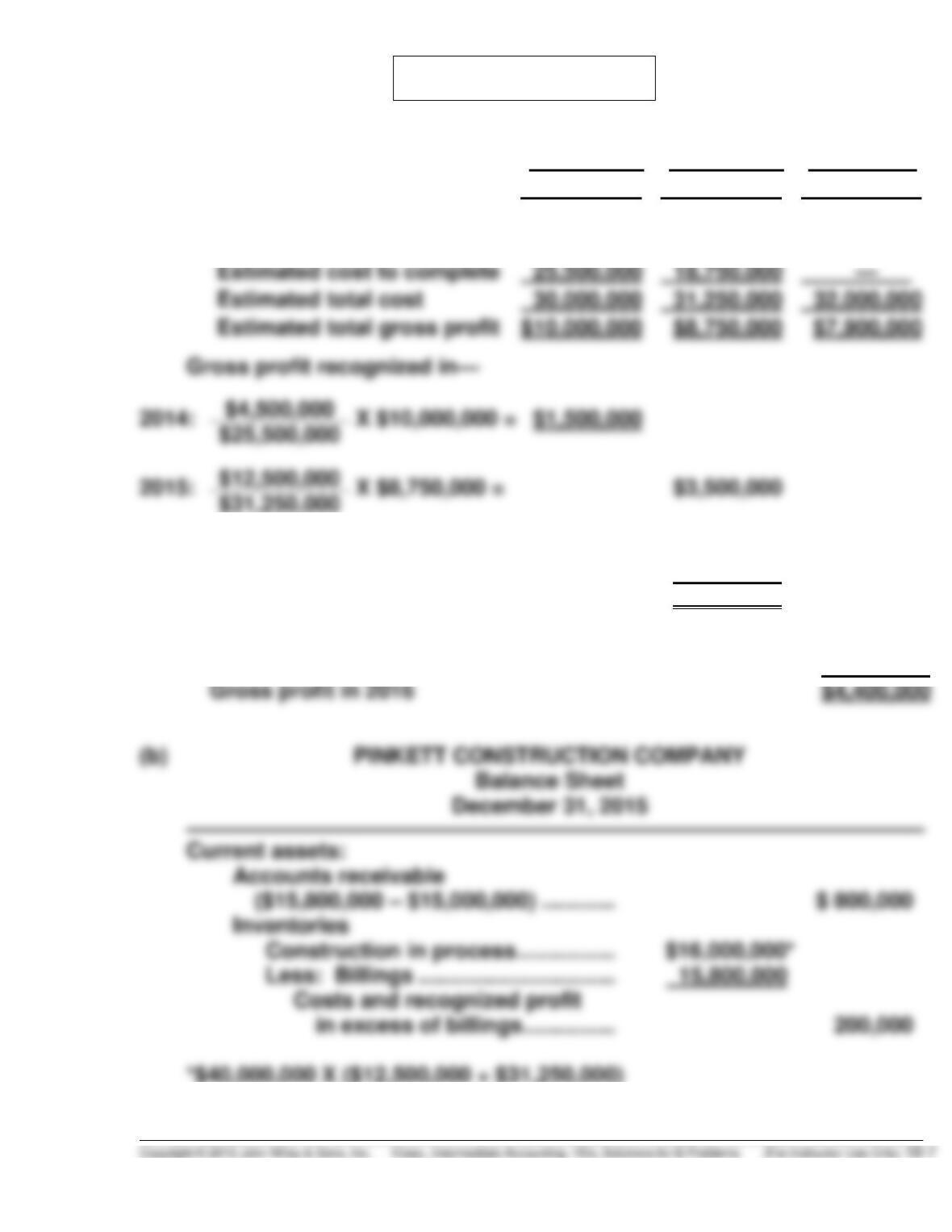

PROBLEM 18-4B

(a)

2014

2015

2016

Contract price

$40,000,000

$40,000,000

$39,900,000

Less estimated cost:

Costs to date

4,500,000

12,500,000

32,000,000

Estimated cost to complete

Estimated total cost

Estimated total gross profit

$10,000,000

Less 2014 recognized

gross profit

1,500,000

Gross profit in 2015

$2,000,000

2016:

Less 2014–2015 recognized

gross profit

3,500,000

Gross profit in 2016

PROBLEM 18-5B

(a) The completed-contract method of revenue recognition recognizes income

only upon completion of a project or shipment of a product. All associ–

ated costs are expensed at the point of sale, and there are no interim

1. Assuming that all costs are incurred, all billings to customers are

made, and all collections from customers are received within 30

days of billing, the Limerock’s revenue, cost of sales, and gross

(1)

(2)

(3)

(4)

(5)

(6)

2014

$12,000

$3,000

$10,000*

$2,000

30%

2015

72%

2016

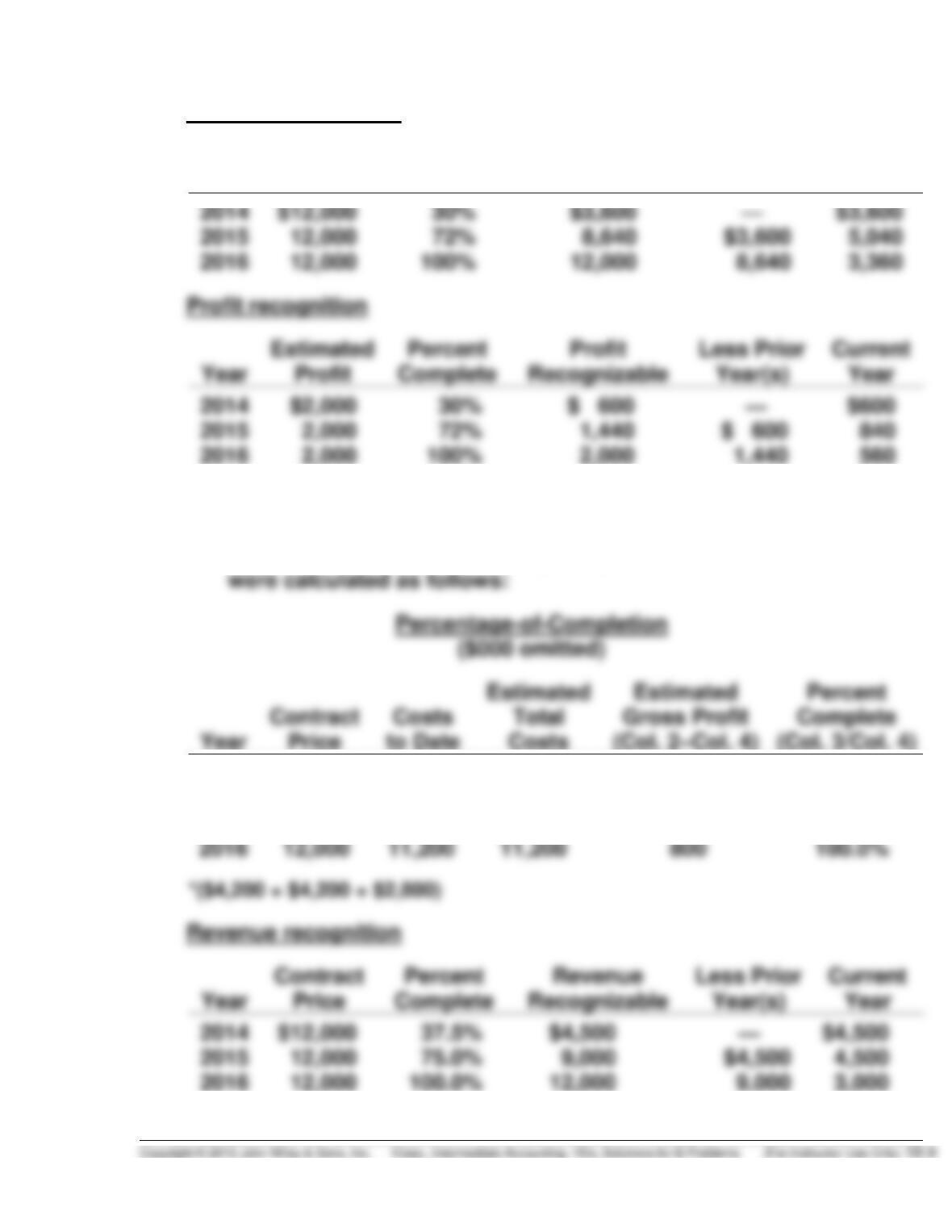

PROBLEM 18-5B (Continued)

Revenue recognition

Year

Contract

Price

Percent

Complete

Revenue

Recognizable

Less Prior

Year(s)

Current

Year

3,360

2. Assuming the same facts as in Instruction (b)1., but that cost

overruns of $1,200,000 were experienced in 2014, Limerock’s

revenue, costs of sales, and gross profit for 2014, 2015, and 2016

(1)

(2)

(3)

(4)

(5)

(6)

2014

$12,000

$4,200

$11,200*

$800

37.5%

2015

12,000

8,400

11,200

800

75.0%

Contract

Percent

Revenue

$4,500

PROBLEM 18-B5 (Continued)

Profit recognition

3. Assuming the same facts as in Instructions (b)1. and (b)2., but that

additional cost overruns of $900,000 are experienced in 2015,

Limerock’s revenue, cost of sales, and gross profit for 2014, 2015,

(1)

(2)

(3)

(4)

(5)

(6)

2014

$12,000

$4,200

$11,200

$800

37.5%

2015

12,000

9,300*

12,100

(100)

76.9%

2016

12,000

12,100

12,100

(100)

100.0%

$3,000

9,228

$3,000

PROBLEM 18-6B

(a) Computation of Recognizable Profit/Loss

Percentage-of–Completion Method

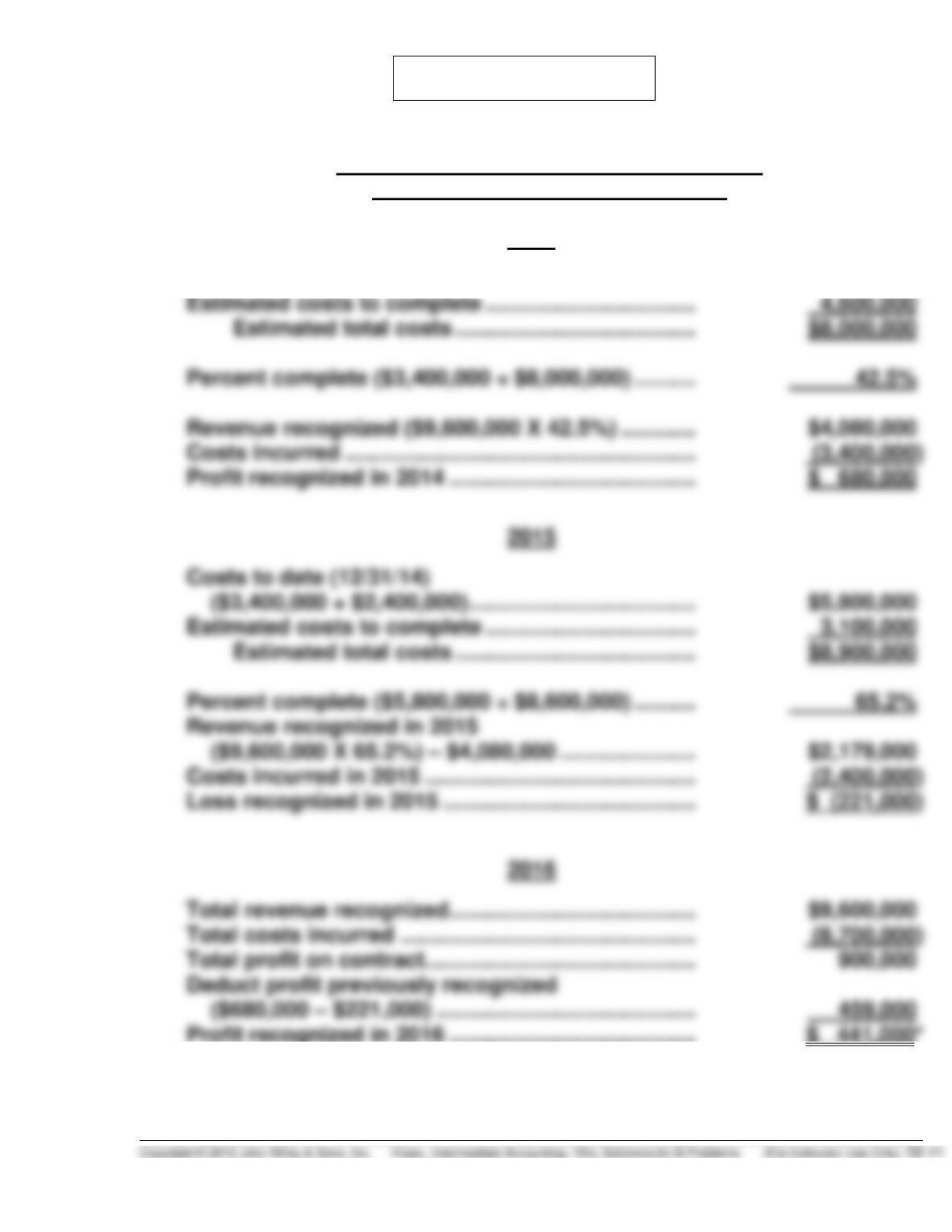

2014

Costs to date (12/31/14) ……………………………………. $3,400,000

PROBLEM 18-6B (Continued)

*Alternative

Revenue recognized in 2016

($9,600,000 X 34.8%) …………………………………….. $3,341,000

PROBLEM 18-7B

(a) Computation of Recognizable Profit/Loss

Percentage-of–Completion Method

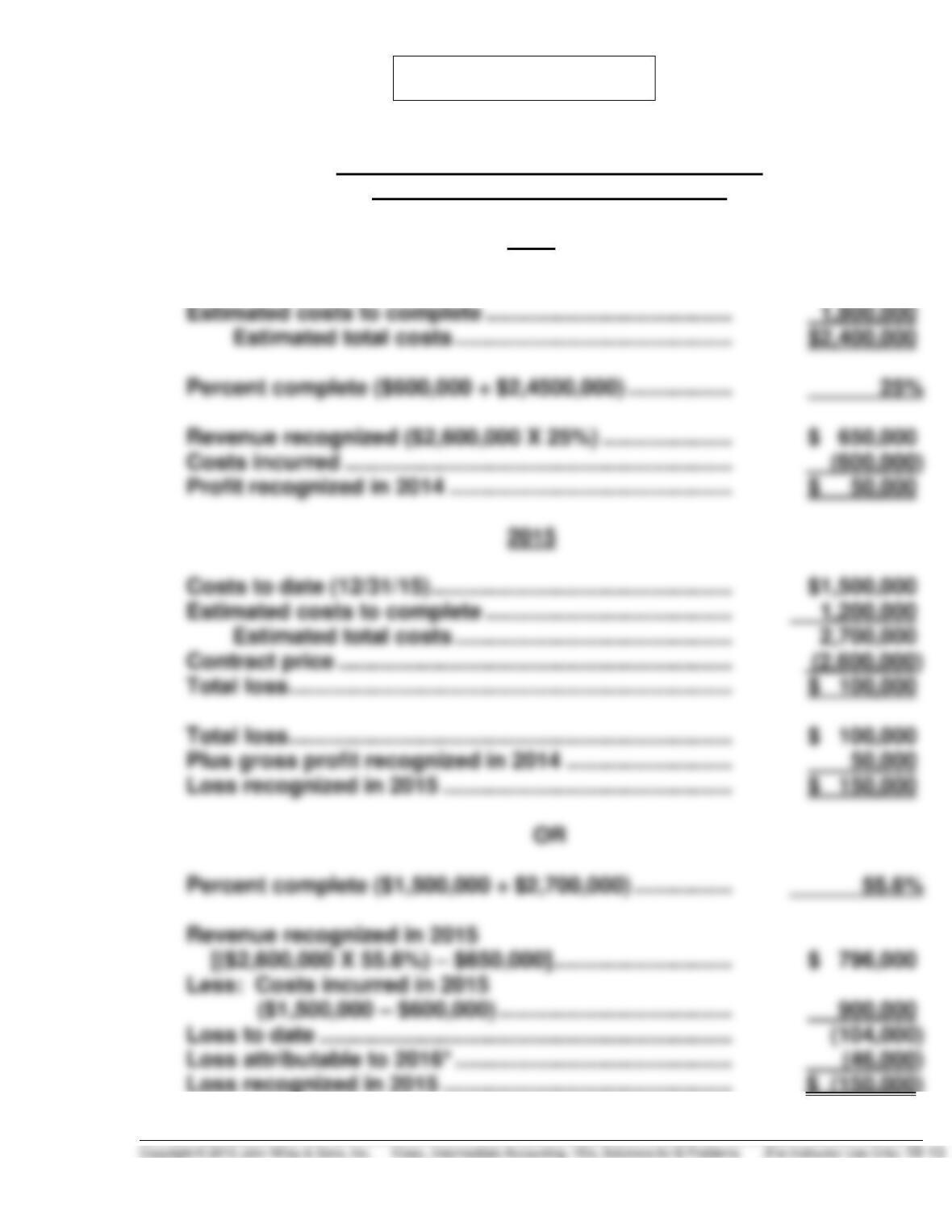

2014

Costs to date (12/31/14) …………………………………………. $ 600,000

PROBLEM 18-7 (Continued)

*2016 revenue

($2,600,000 – $650,000 – $796,000) ……………… $ 1,154,000

Less: 2016 estimated costs …………………………... 1,200,000

2016 loss …………………………………………….. $ (46,000)

(b) Computation of Recognizable Profit/Loss

Completed-Contract Method

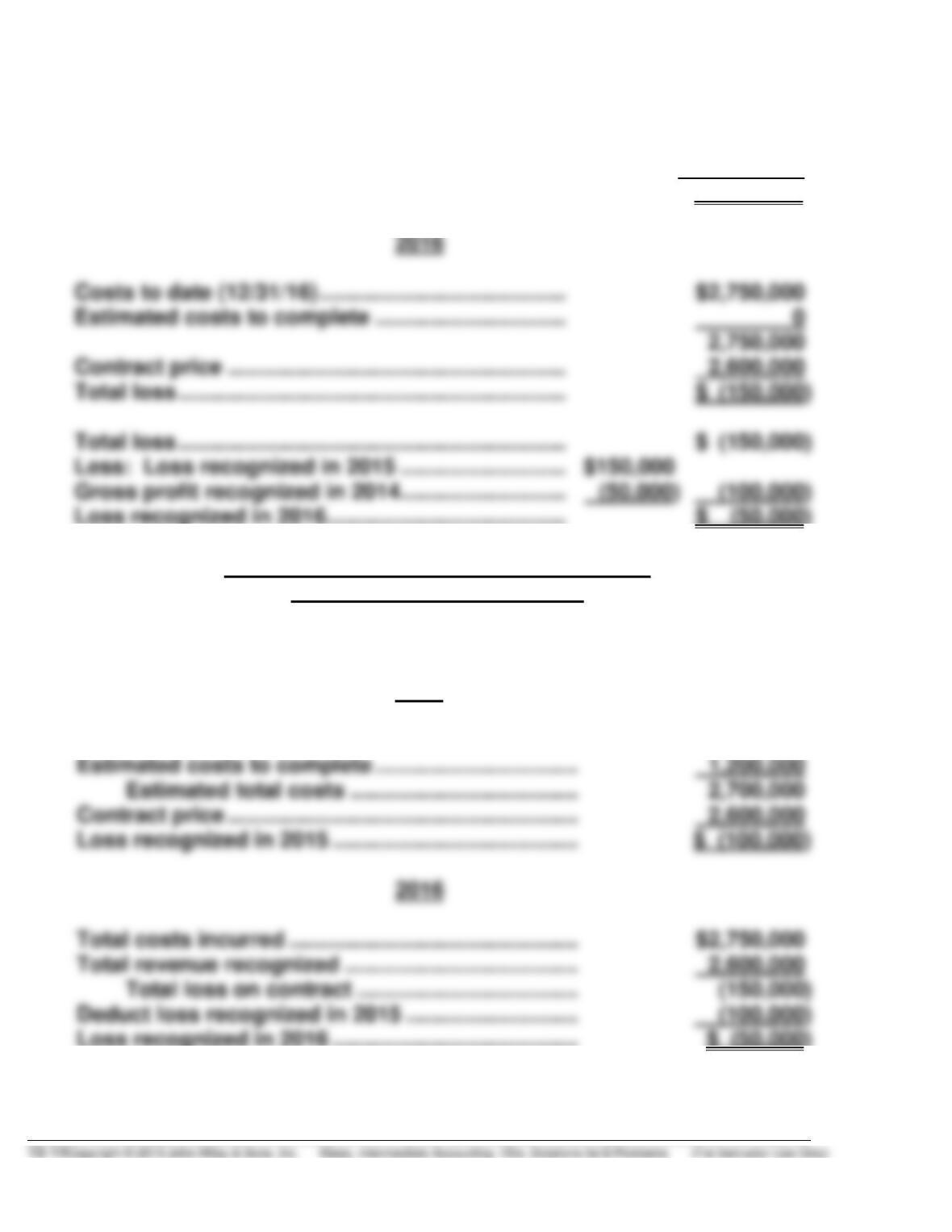

2014—NONE

2015

Costs to date (12/31/15)…………………………………… $1,500,000

PROBLEM 18-8B

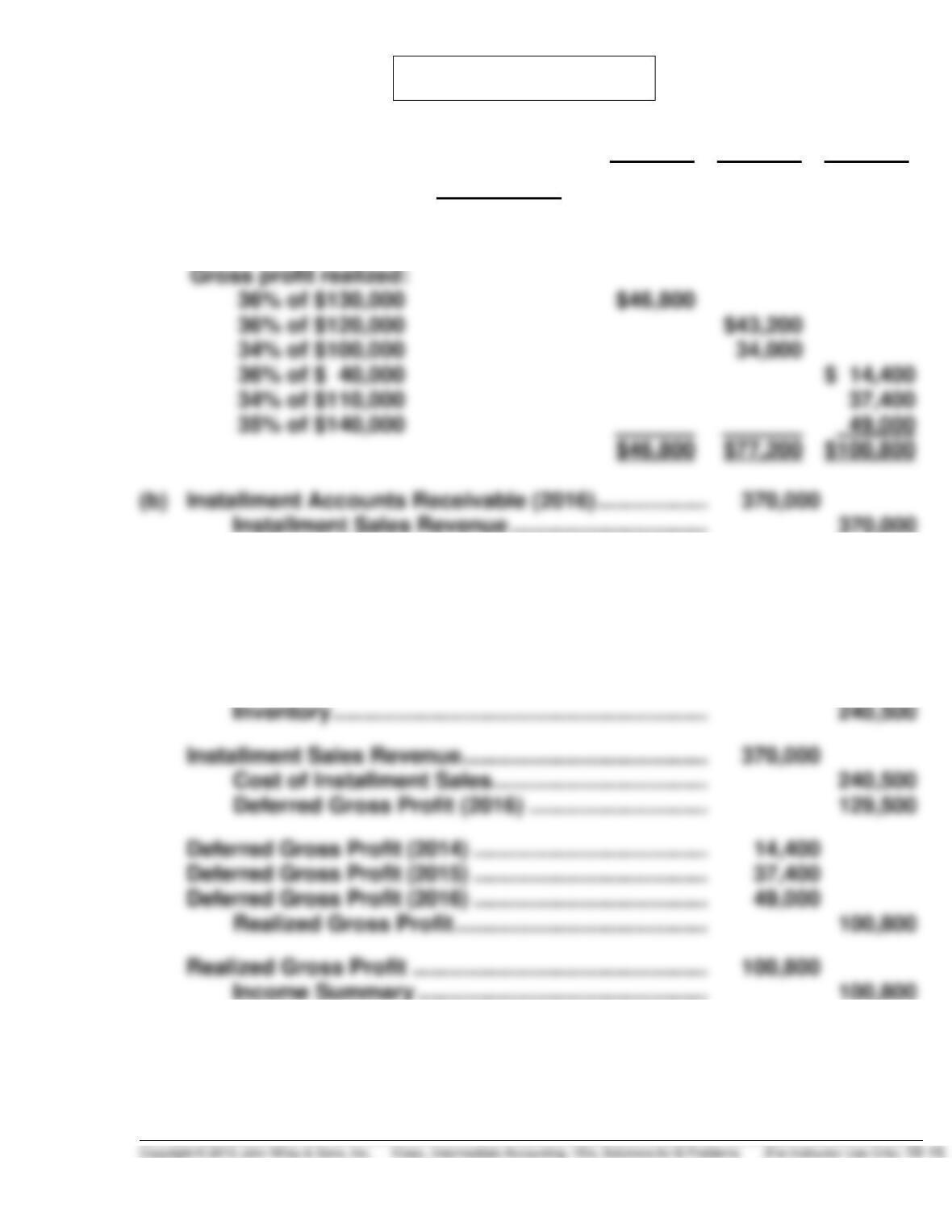

(a)

Rate of gross profit

(

Gross profit

Sales

)

2014

2015

2016

36%

34%

35%

Gross profit realized:

35% of $140,000

Cash ……………………………………………………….………… 290,000

Installment Accounts Receivable (2014) ………. 40,000

Installment Accounts Receivable (2015) ………. 110,000

Installment Accounts Receivable (2016) ………. 140,000

Cost of Installment Sales …………………………..………. 240,500

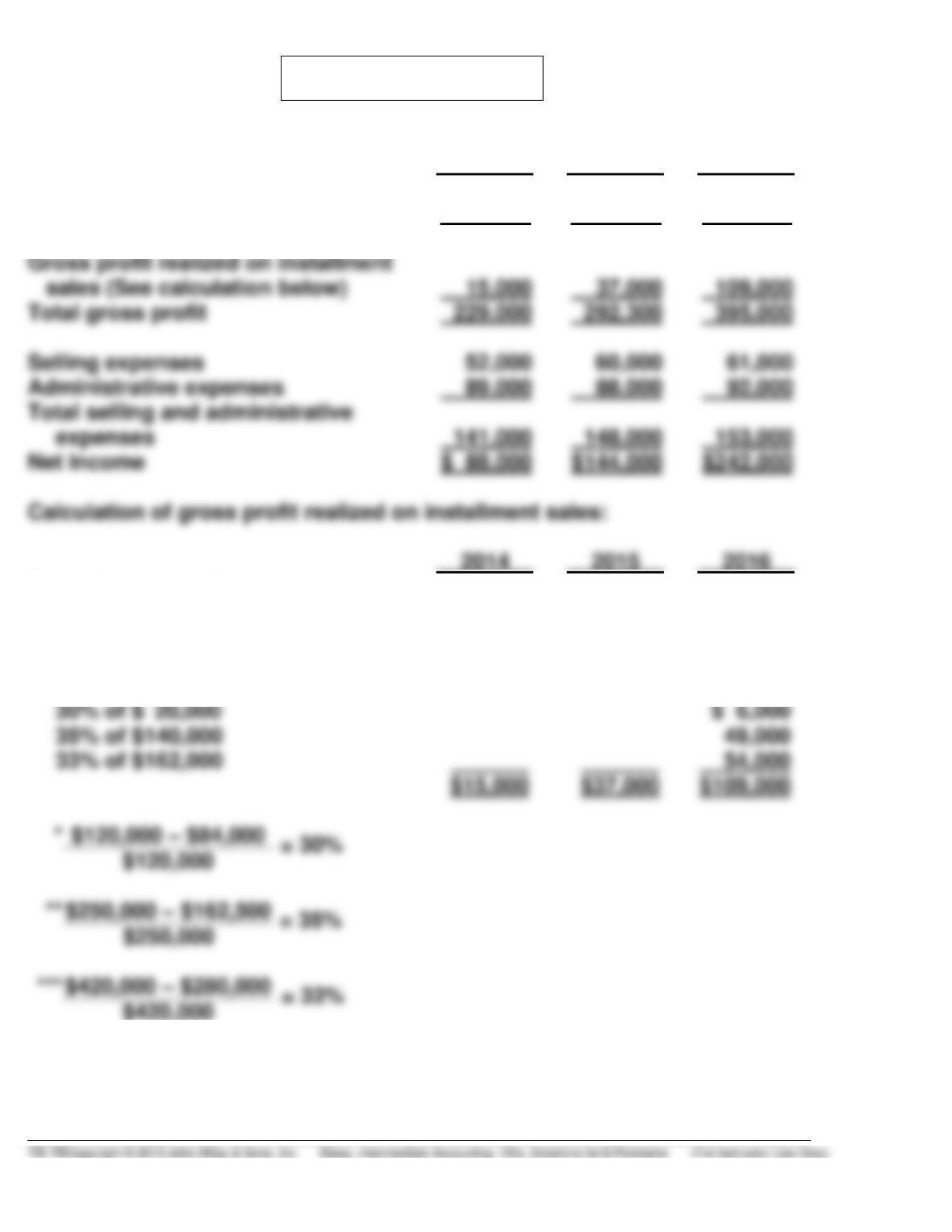

PROBLEM 18-9B

2014

2015

2016

Sales

$705,000

$780,000

$835,000

Cost of sales

491,000

525,000

549,000

Gross profit

214,000

255,000

286,000

Total gross profit

229,000

292,300

395,000

Selling expenses

Administrative expenses

Net income

Calculation of gross profit realized on installment sales:

Rate of gross profit

* 33%*

** 36%**

40%***

Gross profit realized:

30% of $ 50,000

$15,000

30% of $ 30,000

$ 9,000

35% of $ 80,000

28,000

30% of $ 20,000

35% of $140,000

33% of $162,000

$15,000

PROBLEM 18-10B

(a) Rate of gross profit on 2014 installment sales:

Deferred gross profit on repossessions

$14,000 – $2,600 – $6,500 = $4,900

$4,900 ÷ $14,000 = 35%

(b) Installment Sales Revenue …………………………..….. 180,000

Cost of Installment Sales ………………………….. 126,000

Deferred Gross Profit (2015) …………………….. 54,000

Deferred Gross Profit (2014) ……………………………. 36,400

Deferred Gross Profit (2015) ……………………………. 3,600

PROBLEM 18-10B (Continued)

(c) MATEY STORES

Income Statement