ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

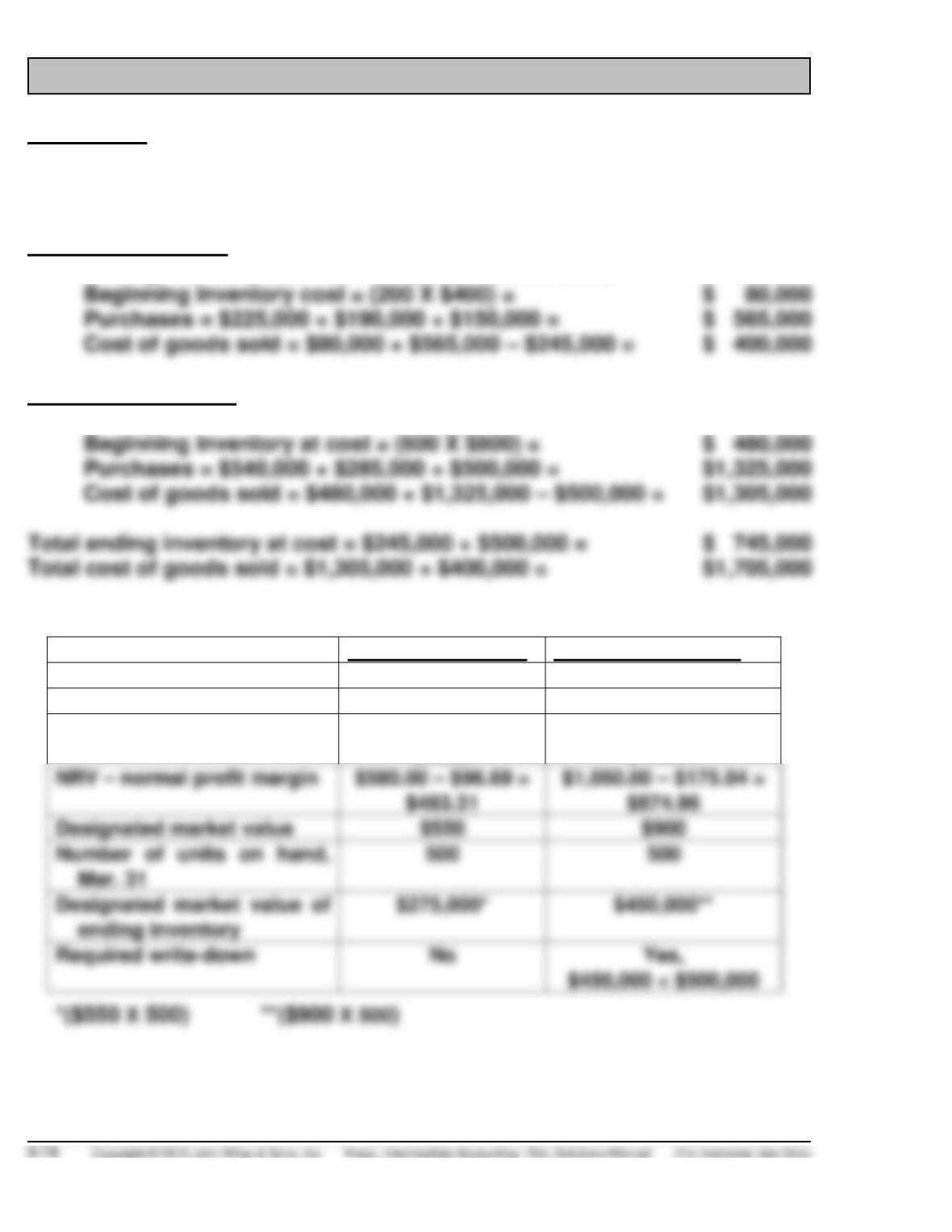

(a)

Residential pumps:

Ending inventory cost = (300 X $500) + (200 X $475) = $ 245,000

Commercial pumps:

Ending inventory at cost = (500 X $1,000) = $ 500,000

Lower-of-cost-or-market:

Residential pumps

Commercial pumps

NRV

$580

$1,050

Replacement cost

$550

$ 900

Normal profit margin

0.1667 X $580.00 =

$96.69

0.1667 X $1,050.00 =

$175.04

NRV – normal profit margin

$874.96

Designated market value

$550

Total amount of inventory reported on March 31 balance sheet = $695,000

($245,000 + $450,000).

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

(b) Inventory at cost = $245,000 + $500,000 = $745,000

Designated market value = $275,000 + $450,000 = $725,000

$725,000 < $745,000, therefore write inventory down to $725,000

Analysis

In this problem, one product’s market value is above cost and the

other one is below. From a conservative perspective, the individual

product approach results in a write-down for any product whose

designated market value is below cost. So, potentially the individual

Principles

(a) If the designated market value is $1,050, the designated market value

of commercial pumps would be above cost. The written-down amount

PROFESSIONAL RESEARCH

(a) The codification provides guidance at: FASB ASC 330–10-05

(Codification String: Assets > 330 Inventory > 10 Overall > 05

(b) According to the FASB ASC 330-10-20, the Glossary indicates the

following.

Inventory is the aggregate of those items of tangible personal

property that have any of the following characteristics:

a. Held for sale in the ordinary course of business

The term inventory embraces goods awaiting sale (the merchandise

of a trading concern and the finished goods of a manufacturer),

goods in the course of production (work in process), and goods to be

consumed directly or indirectly in production (raw materials and

supplies). This definition of inventories excludes long-term assets

PROFESSIONAL RESEARCH (Continued)

(c) According to the FASB ASC 330–10-20, the Glossary indicates the

following for the term Market:

As used in the phrase lower-of-cost-or–market, the term market means

current replacement cost (by purchase or by reproduction, as the

(d) According to FASB ASC 330-10–35:

35–15 Only in exceptional cases may inventories properly be stated

above cost. For example, precious metals having a fixed

characteristic of unit interchangeability.

For: Goods Stated Above Cost

50-3 Where goods are stated above cost this fact shall be fully

disclosed.

35–16 It is generally recognized that income accrues only at the time

of sale, and that gains may not be anticipated by reflecting

assets at their current sales prices. However, exceptions for

reflecting assets at selling prices are permissible for both of

the following:

a. Inventories of gold and silver, when there is an effective

Where such inventories are stated at sales prices, they shall be

reduced by expenditures to be incurred in disposal.

PROFESSIONAL SIMULATION

Resources

Journal Entry

Cost of Goods Sold……………………………………………….

4,000

Allowance to Reduce Inventory to Market ………

4,000

Note: This entry assumes use of the cost–of–goods-sold method.

Explanation

Expected selling prices are important in the application of the lower-of–

cost-or-market rule because they are used in measuring losses of utility in

inventory that otherwise would not be recognized until the period during

IFRS CONCEPTS AND APPLICATION

IFRS9-1

Key similarities are (1) the guidelines on who owns the goods—goods in

transit, consigned goods, special sales agreements, and the costs to

include in inventory are essentially accounted for the same under IFRS and

Key differences are related to (1) the LIFO cost flow assumption—GAAP

permits the use of LIFO for inventory valuation. IFRS prohibits its use. FIFO

and average-cost are the only two acceptable cost flow assumptions

permitted under IFRS; (2) lower-of-cost-or–market test for inventory

valuation—IFRS defines market as net realizable value. GAAP on the other

hand defines market as replacement cost subject to the constraints of net

realizable value (the ceiling) and net realizable value less a normal markup

IFRS9-2

As shown in the analysis below, under IFRS, LaTour’s inventory turnover

ratio is computed as follows:

Difficulties in comparison to a company using GAAP could arise if the U.S.

company uses the LIFO cost flow assumption, which is prohibited under

numbers to FIFO and to permit an “apples to apples” comparison.

IFRS9-3

Reed must not be aware of the important convergence issue arising from

the use of the LIFO cost flow assumption; IFRS specifically prohibits its

use. Conversely, the LIFO cost flow assumption is widely used in the

United States because of its favorable tax advantages. In addition, many

argue that LIFO from a financial reporting point of view provides a better

IFRS9-4

(a) Biological assets are measured on initial recognition and at the end of

each reporting period at fair value less costs to sell (net realizable

IFRS9-5

(1) $12.80 ($14.80 – $1.50 – $.50).

IFRS9-6

Item

Net

Realizable

Value

Cost

LCNRV

D

$80*

$75

$75

E

62

80

62

F

60

80

60

G

35

80

35

H

70

50

50

40

36

36

IFRS9-7

(a)

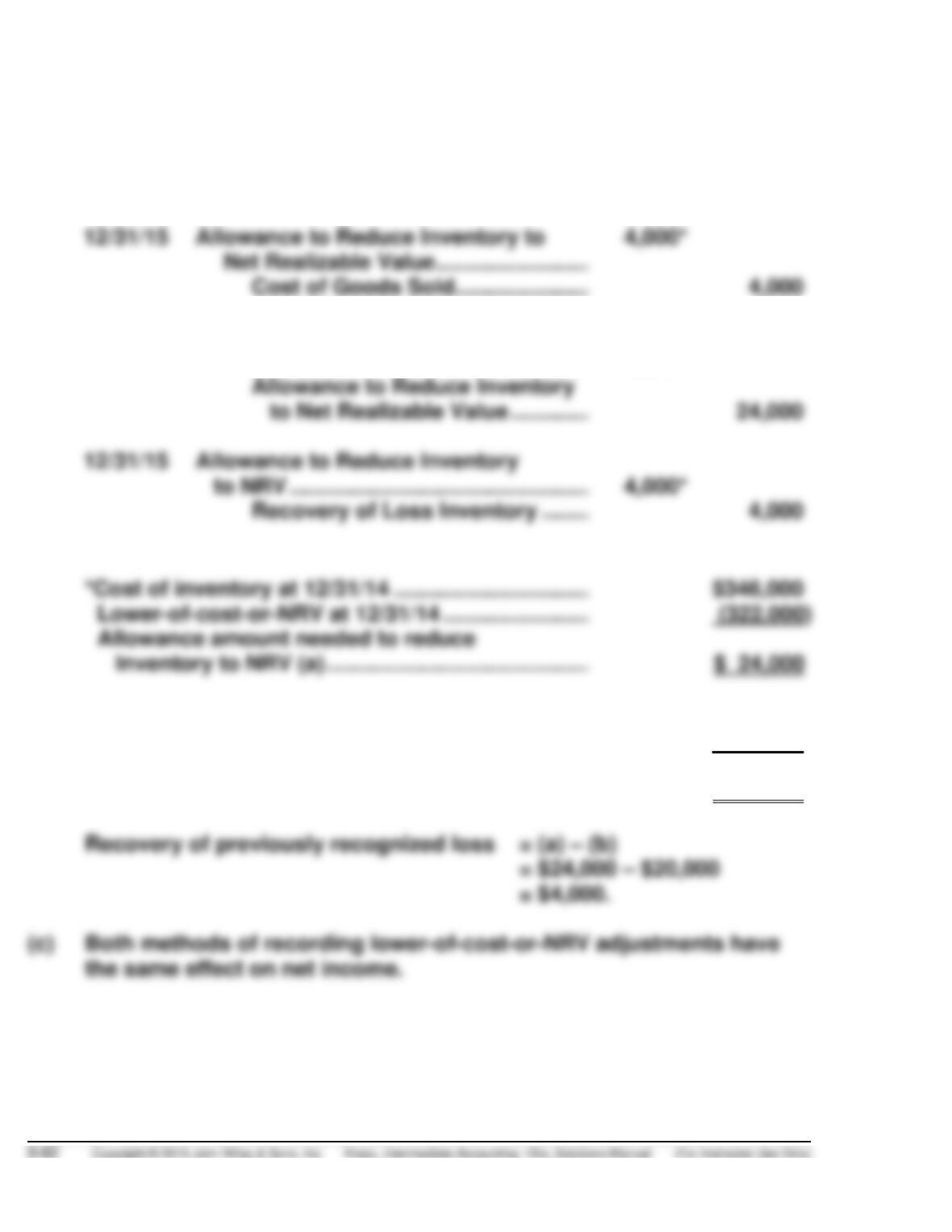

12/31/14

Cost of Goods Sold …………………………..

24,000

Allowance to Reduce Inventory

to Net Realizable Value …………………………..

24,000

Allowance to Reduce Inventory to

Cost of Goods Sold …………………………..

(b)

12/31/14

Loss Due to Decline of

Inventory to Net Realizable Value ………………………….

24,000

Allowance to Reduce Inventory

24,000

Allowance to Reduce Inventory

Recovery of Loss Inventory …………………………..

*Cost of inventory at 12/31/14 …………………………..

Lower-of-cost-or-NRV at 12/31/14 ……………………….

(322,000)

Inventory to NRV (a) ………………………………………..

$ 24,000

Cost of inventory at 12/31/15 …………………………..

$410,000

Lower-of-cost-or-NRV at 12/31/15 ……………………….

(390,000)

Allowance amount needed to reduce

Inventory to NRV (b) ………………………………………..

$ 20,000

Recovery of previously recognized loss

= (a) – (b)

= $24,000 – $20,000

= $4,000.

(c)

Both methods of recording lower-of-cost-or-NRV adjustments have

IFRS9-8

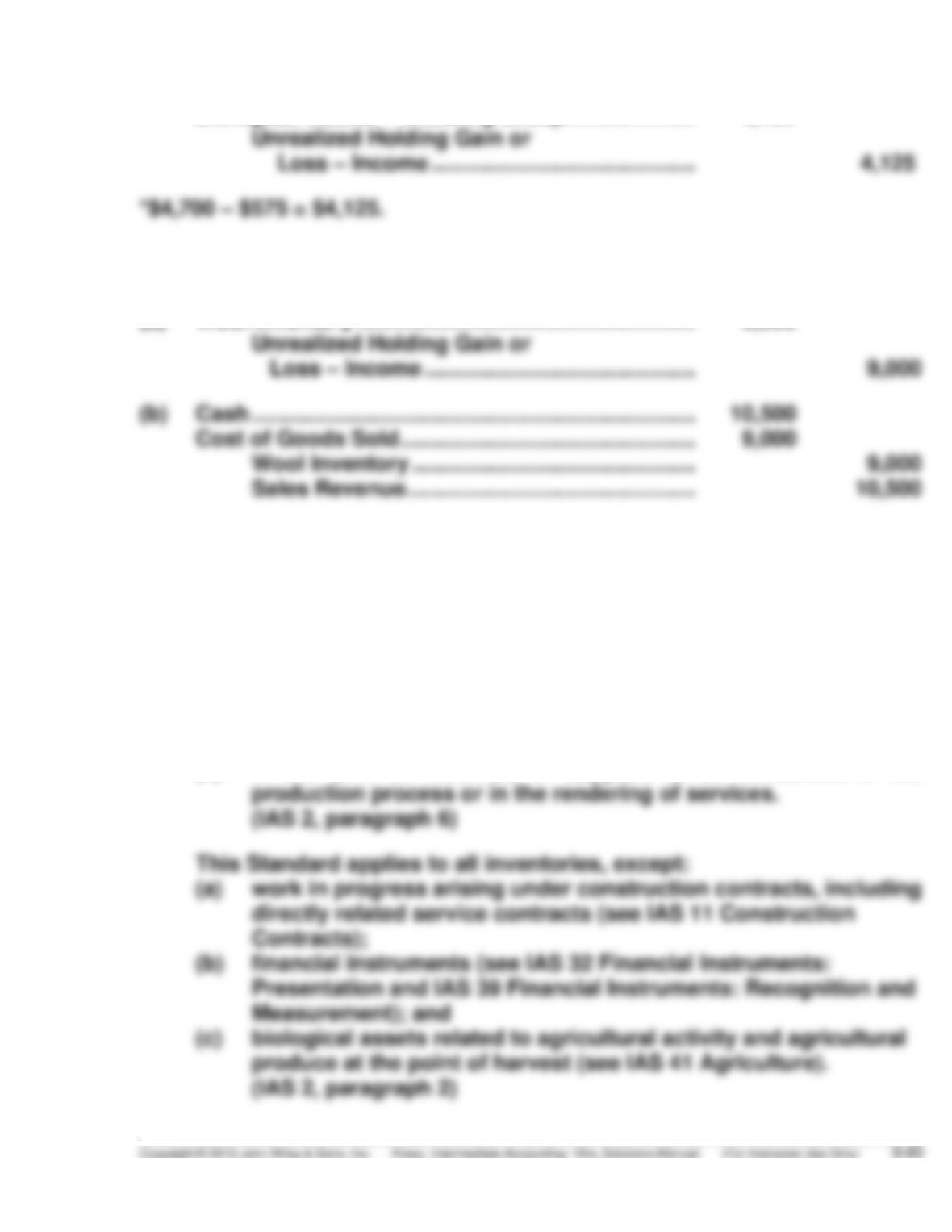

Biological Assets – Shearing Sheep …………………

4,125*

IFRS9-9

(a)

Wool Inventory ……………………………………………….

9,000

(b)

Cash ………………………………………………………………

Wool Inventory ……………………………………….

Sales Revenue ………………………………………..

IFRS9-10

(a) The IFRS requirements related to accounting and reporting for

inventories is found in IAS 2 (Inventories), IAS 18 (Revenue) and IAS

41 (Agriculture).

Inventories are assets:

(a) held for sale in the ordinary course of business;

(b) in the process of production for such sale; or

(c) in the form of materials or supplies to be consumed in the

IFRS9-10 (Continued)

(c) Net realisable value refers to the net amount that an entity expects to

realise from the sale of inventory in the ordinary course of business.

(d) This Standard does not apply to the measurement of inventories held by:

(a) producers of agricultural and forest products, agricultural produce

after harvest, and minerals and mineral products, to the extent

that they are measured at net realisable value in accordance

(IAS 2, paragraph 3).

IFRS9-11

(a) Inventories are valued at the lower-of-cost-or-net realisable value

using the retail method, which is computed on the basis of selling

IFRS9-11 (Continued)

(d)

Inventory turnover =

Cost of Sales

=

£6,179.1

Average Inventory

£681.9 + £685.3

2

Its gross profit percentages for 2012 and 2011 are as follows: