CHAPTER 24

FULL DISCLOSURE IN FINANCIAL REPORTING

IFRS questions are available at the end of this chapter.

TRUE-FALSE—Conceptual

Answer No. Description

MULTIPLE CHOICE—Conceptual

Answer No. Description

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 2

MULTIPLE CHOICE—Conceptual (cont.)

Answer N/o. Description

MULTIPLE CHOICE—Computational

Answer No. Description

Full Disclosure in Financial Reporting

24 – 3

MULTIPLE CHOICE—CPA Adapted

Answer No. Description

Item Description

BE24-84 Notes to financial statements.

BE24-85 Segment reporting.

EXERCISES

E24-86 Segment reporting.

E24-87 Interim reports.

E24-88 Inventory and cost of goods sold at interim dates.

E24-89 Forecasts.

*E24-90 Financial statement analysis.

*E24-91 Selected financial ratios.

*E24-92 Computation of selected ratios.

PROBLEMS

Item Description

P24-93 Segment Reporting.

P24-94 Interim Reports.

CHAPTER LEARNING OBJECTIVES

1. Review the full disclosure principle and describe implementation problems.

2. Explain the use of notes in financial statement preparation.

3. Discuss the disclosure requirements for related-party transactions, post-balance-sheet

events, and major business segments.

4. Describe the accounting problems associated with interim reporting.

5. Identify the major disclosures in the auditor’s report.

6. Understand management’s responsibilities for financials.

7. Identify issues related to financial forecasts and projections.

8. Describe the profession’s response to fraudulent financial reporting.

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 4

*9. Understand the approach to financial statement analysis.

*10. Identify major analytic ratios and describe their calculation.

*11. Explain the limitations of ratio analysis.

12. Describe techniques of comparative analysis.

13. Describe techniques of percentage analysis.

14. Compare the disclosure requirements under GAAP and IFRS

SUMMARY OF LEARNING OBJECTIVES BY QUESTIONS

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Item

Type

Learning Objective 1

1.

TF

2.

TF

21.

MC

22.

MC

23.

MC

S24.

MC

Learning Objective 2

3.

TF

5.

TF

S26.

MC

28.

MC

73.

MC

4.

TF

S25.

MC

P27.

MC

29.

MC

84.

E

Learning Objective 3

6.

TF

30.

MC

33.

MC

56.

MC

76.

MC

93.

P

7.

TF

31.

MC

34.

MC

74.

MC

85.

E

8.

TF

32.

MC

S35.

MC

75.

MC

86.

E

Learning Objective 4

9.

TF

S36.

MC

40.

MC

57.

MC

78.

MC

88.

E

10.

TF

P37.

MC

41.

MC

58.

MC

79.

MC

94.

P

11.

TF

38.

MC

42.

MC

59.

MC

80.

MC

12.

TF

39.

MC

43.

MC

77.

MC

87.

E

Learning Objective 5

13.

TF

14.

TF

15.

TF

16.

TF

S44.

MC

Learning Objective 6

P45.

MC

Learning Objective 7

17.

TF

18.

TF

S46.

MC

47.

MC

89.

E

Learning Objective 8

19.

TF

20.

TF

Learning Objective 10

48.

MC

52.

MC

61.

MC

65.

MC

69.

MC

81.

MC

91.

E

49.

MC

53.

MC

62.

MC

66.

MC

70.

MC

82.

MC

92.

E

50.

MC

54.

MC

63.

MC

67.

MC

71.

MC

83.

MC

51.

MC

60.

MC

64.

MC

68.

MC

72.

MC

90.

E

Learning Objective 11

55.

MC

Learning Objective 14 – IFRS

1.

TF

4.

TF

7.

MC

10.

MC

13.

MC

16.

SA

Full Disclosure in Financial Reporting

24 – 5

2.

TF

5.

TF

8.

MC

11.

MC

14.

MC

3.

TF

6.

MC

9.

MC

12.

MC

15.

MC

Note: TF = True-False P = Problem

MC = Multiple Choice BE = Brief Ex

E = Exercise

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 6

TRUE-FALSE—Conceptual

1. FASB standards directly affect financial statements, notes to the financial statements, and

management’s discussion and analysis.

2. The SEC requires that companies report to it certain substantive information that is not

found in their annual reports.

3. Accounting policies are the specific accounting principles and methods a company uses

and considers most appropriate to present fairly its financial statements.

4. In order to make adequate disclosure of related party transactions, companies should

report the legal form, rather than the economic substance, of these transactions.

5. If the loss on an account receivable results from a customer’s bankruptcy after the

balance sheet date, the company only discloses this information in the notes to the

financial statements.

6. FASB Statement 131 requires that general purpose financial statements include selected

information on a single basis of segmentation.

7. The FASB requires allocations of joint, common, or company-wide costs for external

reporting purposes.

8. If 10 percent or more of company revenue is derived from a single customer, the company

must disclose the total amount of revenue from each such customer by segment.

9. Companies should report accounting transactions as they occur, and expense recognition

should not change with the period of time covered under the integral approach.

10. Companies should generally use the same accounting principles for interim reports and

for annual reports.

11. Companies report extraordinary items in interim reports by prorating them over the four

quarters.

12. To compute the year–to-date tax, companies apply the estimated annual effective tax rate

to the year–to-date ordinary income at the end of each interim period.

13. In most situations, an auditor issues a qualified opinion or disclaims an opinion.

14. A qualified opinion is issued when the exception to the standard opinion is not of sufficient

magnitude to invalidate the statements as a whole.

15. Management’s discussion and analysis section covers three financial aspects of an

enterprise’s business-liquidity, profitability, and solvency.

16. The MD&A section must provide information about the effects of inflation and changing

prices, if they are material to financial statement trends.

Full Disclosure in Financial Reporting

24 – 7

17. A financial projection is a set of prospective financial statements that present a company’s

expected financial position and results of operations.

18. The difference between a financial forecast and a financial projection is that a forecast

provides information on what is expected to happen, while a projection provides

information on what might take place.

19. Fraudulent financial reporting is intentional or reckless conduct, whether act or omission,

that results in materially misleading financial statements.

20. Influences in a company’s internal environment may relate to industry conditions, poor

internal control systems, or legal and regulatory considerations.

True-False Answers—Conceptual

MULTIPLE CHOICE—Conceptual

21. Which of the following should be disclosed in a Summary of Significant Accounting

Policies?

a. Types of executory contracts

b. Amount for cumulative effect of change in accounting principle

c. Claims of equity holders

d. Depreciation method followed

22. An example of an inventory accounting policy that should be disclosed in a Summary of

Significant Accounting Policies is the

a. amount of income resulting from the involuntary liquidation of LIFO.

b. major backlogs of inventory orders.

c. method used for pricing inventory.

d. composition of inventory into raw materials, work-in-process, and finished goods.

23. Errors and irregularities are defined as intentional distortions of facts.

Errors Irregularities

a. Yes Yes

b. Yes No

c. No Yes

d. No No

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 8

S24. The full disclosure principle, as adopted by the accounting profession, is best described

by which of the following?

a. All information related to an entity’s business and operating objectives is required to

be disclosed in the financial statements.

b. Information about each account balance appearing in the financial statements is to be

included in the notes to the financial statements.

c. Enough information should be disclosed in the financial statements so a person

wishing to invest in the stock of the company can make a profitable decision.

d. Disclosure of any financial facts significant enough to influence the judgment of an

informed reader.

S25. The focus of APB Opinion No. 22 is on the disclosure of accounting policies. This

information is important to financial statement readers in determining

a. net income for the year.

b. whether accounting policies are consistently applied from year to year.

c. the value of obsolete items included in ending inventory.

d. whether the working capital position is adequate for future operations.

S26. If a business entity entered into certain related party transactions, it would be required to

disclose all of the following information except the

a. nature of the relationship between the parties to the transactions.

b. nature of any future transactions planned between the parties and the terms involved.

c. dollar amount of the transactions for each of the periods for which an income state-

ment is presented.

d. amounts due from or to related parties as of the date of each balance sheet presented.

P27. Events that occur after the December 31, 2015 balance sheet date (but before the

balance sheet is issued) and provide additional evidence about conditions that existed at

the balance sheet date and affect the realizability of accounts receivable should be

a. discussed only in the MD&A (Management’s Discussion and Analysis) section of the

annual report.

b. disclosed only in the Notes to the Financial Statements.

c. used to record an adjustment to Bad Debt Expense for the year ending December 31,

2015

d. used to record an adjustment directly to the Retained Earnings account

28. Which of the following post-balance-sheet events would generally require disclosure, but

no adjustment of the financial statements?

a. Retirement of the company president

b. Settlement of litigation when the event that gave rise to the litigation occurred prior to

the balance sheet date.

c. Employee strikes

d. Issue of a large amount of capital stock

29. Which of the following subsequent events (post-balance-sheet events) would require

adjustment of the accounts before issuance of the financial statements?

a. Loss of plant as a result of fire

b. Changes in the quoted market prices of securities held as an investment

c. Loss on an uncollectible account receivable resulting from a customer’s major flood

loss

d. Loss on a lawsuit, the outcome of which was deemed uncertain at year end.

Full Disclosure in Financial Reporting

24 – 9

30. Revenue of a segment includes

a. only sales to unaffiliated customers.

b. sales to unaffiliated customers and intersegment sales.

c. sales to unaffiliated customers and interest revenue.

d. sales to unaffiliated customers and other revenue and gains.

31. An operating segment is a reportable segment if

a. its operating profit is 10% or more of the combined operating profit of profitable

segments.

b. its operating loss is 10% or more of the combined operating losses of segments that

incurred an operating loss.

c. the absolute amount of its operating profit or loss is 10% or more of the company’s

combined operating profit or loss.

d. None of these answers are correct.

32. A segment of a business enterprise is to be reported separately when the revenues of the

segment exceed 10 percent of the

a. total combined revenues of all segments reporting profits.

b. total revenues of all the enterprise’s industry segments.

c. total export and foreign sales.

d. combined net income of all segments reporting profits.

33. All of the following information about each operating segment must be reported except

a. unusual items.

b. interest revenue.

c. cost of goods sold.

d. depreciation and amortization expense.

34. The profession requires disaggregated information in the following ways:

a. products or services.

b. geographic areas.

c. major customers.

d. All of these answers are correct.

S35. In presenting segment information, which of the following items must be reconciled to the

entity’s consolidated financial statements?

Operating Identifiable

Revenues Profit (Loss) Assets

a. Yes Yes Yes

b. No Yes Yes

c. Yes No Yes

d. Yes Yes No

S36. APB Opinion No. 28 indicates that

a. all companies that issue an annual report should issue interim financial reports.

b. the discrete view is the most appropriate approach to take in preparing interim

financial reports.

c. the three basic financial statements should be presented each time an interim period

is reported upon.

d. the same accounting principles used for the annual report should be employed for

interim reports.

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 10

P37. Rondelli Manufacturing Company employs a standard cost system. A planned volume

variance in the first quarter of 2015, which is expected to be absorbed by the end of the

fiscal year, ordinarily should

a. be deferred at the end of the first quarter, regardless of whether it is favorable or

unfavorable.

b. never be deferred beyond the quarter in which it occurs.

c. be deferred at the end of the first quarter if it is favorable; unfavorable variances are to

be recognized in the period incurred.

d. be deferred at the end of the first quarter if it is unfavorable; favorable variances are to

be recognized in the period incurred.

38. In considering interim financial reporting, how does the profession conclude that such

reporting should be viewed?

a. As a “special” type of reporting that need not follow generally accepted accounting

principles.

b. As useful only if activity is evenly spread throughout the year so that estimates are

unnecessary.

c. As reporting for a basic accounting period.

d. As reporting for an integral part of an annual period.

39. Accounting principles are modified for the following at interim dates.

Revenue Losses

a. Yes Yes

b. Yes No

c. No Yes

d. No No

40. The following methods of estimating inventory can be used at interim dates for inventory

pricing. May they also be used at year end?

Gross Profit Method Retail Inventory Method

a. No No

b. No Yes

c. Yes No

d. Yes Yes

41. A company that uses the last-in, first-out (LIFO) method of inventory pricing finds at an

interim reporting date that there has been a partial liquidation of the base period inventory

level. The decline is considered temporary and the partial liquidation is expected to be

replaced prior to year end. The amount shown as inventory at the interim reporting date

should

a. be shown at the actual level, and cost of sales for the interim reporting period should

include the expected cost of replacement of the liquidated LIFO base.

b. be shown at the actual level, and cost of sales for the interim reporting period should

reflect the historical cost of the liquidated LIFO base.

c. not give effect to the LIFO liquidation, and cost of sales for the interim reporting period

should reflect the historical cost of the liquidated LIFO base.

d. be shown at the actual level, and the decrease in inventory level should not be

reflected in the cost of sales for the interim reporting period.

Full Disclosure in Financial Reporting

24 – 11

42. Companies should disclose all of the following in interim reports except

a. basic and diluted earnings per share.

b. changes in accounting principles.

c. post-balance-sheet events.

d. seasonal revenue, cost, or expenses.

43. The required approach for handling extraordinary items in interim reports is to

a. prorate them over all four quarters.

b. prorate them over the current and remaining quarters.

c. charge or credit the loss or gain in the quarter that it occurs.

d. disclose them only in the notes.

S44. If the financial statements examined by an auditor lead the auditor to issue an opinion that

contains an exception that is not of sufficient magnitude to invalidate the statement as a

whole, the opinion is said to be

a. unqualified.

b. qualified.

c. adverse.

d. exceptional.

P45. The MD&A section of a company’s annual report is to cover the following three items:

a. income statement, balance sheet, and statement of owners’ equity.

b. income statement, balance sheet, and statement of cash flows.

c. liquidity, capital resources, and results of operations.

d. changes in the stock price, mergers, and acquisitions.

S46. Which of the following best characterizes the difference between a financial forecast and a

financial projection?

a. Forecasts include a complete set of financial statements, while projections include

only summary financial data.

b. A forecast is normally for a full year or more and a projection presents data for less

than a year.

c. A forecast attempts to provide information on what is expected to happen, whereas a

projection may provide information on what is not necessarily expected to happen.

d. A forecast includes data which can be verified about future expectations, while the

data in a projection is not susceptible to verification.

47. A financial forecast per professional pronouncements presents to the best of the

responsible party’s knowledge and belief,

a. an entity’s expected financial position, results of operations, and cash flows.

b. an assessment of the company’s ability to be successful in the future.

c. given one or more hypothetical assumptions, an entity’s expected financial position,

results of operations, and cash flows.

d. an assessment of the company’s ability to be successful in the future under a number

of different assumptions.

*48. Cash, short-term investments, and net receivables are the numerator for

Acid-Test Ratio Current Ratio

a. Yes No

b. Yes Yes

c. No No

d No Yes

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 12

*49. Theoretically, in computing the accounts receivable turnover, the numerator should

include

a. net sales.

b. net credit sales.

c. total sales.

d. total credit sales.

*50. The return on common stock equity is calculated by dividing

a. net income by average common stockholders’ equity.

b. net income less preferred dividends by average common stockholders’ equity.

c. net income by ending common stockholders’ equity.

d. net income less preferred dividends by ending common stockholders’ equity.

*51. The payout ratio is calculated by dividing

a. dividends per share by earnings per share.

b. cash dividends by net income plus preferred dividends.

c. cash dividends by market price per share.

d. cash dividends by net income less preferred dividends.

*52. Which of the following ratios measures long-term solvency?

a. Acid-test ratio

b. Accounts receivable turnover

c. Debt to assets

d. Current ratio

*53. The calculation of the times interest earned involves dividing

a. net income by annual interest expense.

b. net income plus income taxes by annual interest expense.

c. net income plus income taxes and interest expense by annual interest expense.

d. None of these answers are correct.

*54. When should an average amount be used for the numerator or denominator?

a. When the numerator is a balance sheet item or items

b. When the denominator is a balance sheet item or items

c. When a ratio consists of an income statement item and a balance sheet item

d. When the numerator is an income statement item or items

*55. The basic limitations associated with ratio analysis include

a. the lack of comparability among firms in a given industry.

b. the use of estimated items in accounting.

c. the use of historical costs in accounting.

d. All of these answers are correct.

Full Disclosure in Financial Reporting

24 – 13

Multiple Choice Answers—Conceptual

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

MULTIPLE CHOICE—Computational

56. Presented below are four segments that have been identified by Haley Productions:

Total Revenue Operating

Segments (Unaffiliated) Profit (Loss) Identifiable Assets

A $255,000 $30,000 $900,000

B 600,000 (55,000) 800,000

C 225,000 6,000 450,000

D 90,000 4,000 225,000

For which of the segments would information have to be disclosed in accordance with

professional pronouncements?

a. Segments A, B, C, and D

b. Segments A, B, and C

c. Segments A and B

d. Segments A and D

57. In January 2015, Post, Inc. estimated that its year-end bonus to executives would be

$840,000 for 2015. The actual amount paid for the year-end bonus for 2014 was

$770,000. The estimate for 2015 is subject to year-end adjustment. What amount, if any,

of expense should be reflected in Post’s quarterly income statement for the three months

ended March 31, 2015?

a. $ -0-.

b. $192,500.

c. $210,000.

d. $840,000.

58. On January 15, 2015, Vancey Company paid property taxes on its factory building for the

calendar year 2015 in the amount of $960,000. In the first week of April 2015, Vancey

made unanticipated major repairs to its plant equipment at a cost of $2,400,000. These

repairs will benefit operations for the remainder of the calendar year. How should these

expenses be reflected in Vancey’s quarterly income statements?

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 14

Three Months Ended

3/31/15 6/30/15 9/30/15 12/31/15

a. $240,000 $1,040,000 $1,040,000 $1,040,000

b. $240,000 $2,640,000 $240,000 $240,000

c. $960,000 $1,600,000 $ -0- $ -0-

d. $840,000 $840,000 $840,000 $840,000

59. An inventory loss from market decline of $1,200,000 occurred in May 2015, after its March 31,

2015 quarterly report was issued. None of this loss was recovered by the end of the year.

How should this loss be reflected in the company’s quarterly income statements?

Three Months Ended

3/31/15 6/30/15 9/30/15 12/31/15

a. $ -0- $ -0- $ -0- $1,200,000

b. $ -0- $400,000 $400,000 $400,000

c. $ -0- $1,200,000 $ -0- $ -0-

d. $300,000 $300,000 $300,000 $300,000

Use the following information for questions 60 through 63.

Information for Ramirez Corp. is given below:

Ramirez Corp.

Balance Sheet

December 31, 2015

Assets Equities

Cash $ 200,000 Accounts payable $ 420,000

Accounts receivable (net) 1,300,000 Income taxes payable 126,000

Inventories 1,626,000 Miscellaneous accrued payables 150,000

Plant and equipment, Bonds payable (10%, due 2017) 1,250,000

net of depreciation 1,322,000 Preferred stock ($100 par, 6%

Patents 174,000 cumulative nonparticipating) 500,000

Other intangible assets 50,000 Common stock (no par, 30,000

Total Assets $4,672,000 shares authorized, issued

and outstanding) 750,000

Retained earnings 1,626,000

Treasury stock—1,000 shares

of preferred (150,000)

Total Equities $4,672,000

Ramirez Corp.

Income Statement

Year Ended December 31, 2015

Net sales $6,000,000

Cost of goods sold 4,000,000

Gross profit 2,000,000

Operating expenses (including bond interest expense) 1,000,000

Income before income taxes 1,000,000

Income tax 300,000

Net income $ 700,000

Full Disclosure in Financial Reporting

24 – 15

Additional information:

There are no preferred dividends in arrears, the balances in the Accounts Receivable and

Inventory accounts are unchanged from January 1, 2015, and there were no changes in the

Bonds Payable, Preferred Stock, or Common Stock accounts during 2015. Assume that preferred

dividends for the current year have not been declared.

*60. At December 31, 2015, the current ratio was

a. 1,500 ÷ 420.

b. 4,450 ÷ 546.

c. 3,126 ÷ 546.

d. 3,126 ÷ 696.

*61. The number of times interest was earned during 2015 was

a. 700 ÷ 125.

b. 1,000 ÷ 125.

c. 1,124 ÷ 125.

d. 874 ÷ 125.

*62. At December 31, 2015, the book value per share of common stock was

a. $74.21.

b. $77.55.

c. $79.20.

d. $78.20.

*63. The rate of return for 2015 based on the year-end common stockholders’ equity was

a. 700 ÷ 2,346.

b. 700 ÷ 2,376.

c. 670 ÷ 2,346..

d. 670 ÷ 2,376.

Use the following information for questions 64 through 69.

The following data are provided:

December 31

2015 2014

Cash $ 750,000 $ 500,000

Accounts receivable (net) 800,000 600,000

Inventories 1,300,000 1,100,000

Plant assets (net) 3,500,000 3,250,000

Accounts payable 550,000 400,000

Income taxes payable 100,000 50,000

Bonds payable 700,000 700,000

10% Preferred stock, $50 par 1,000,000 1,000,000

Common stock, $10 par 1,200,000 900,000

Paid-in capital in excess of par 800,000 650,000

Retained earnings 2,000,000 1,750,000

Net credit sales 6,400,000

Cost of goods sold 4,200,000

Operating expenses 1,450,000

Net income 750,000

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 16

Additional information:

Depreciation included in cost of goods sold and operating expenses is $610,000. On May 1,

2015, 30,000 shares of common stock were issued. The preferred stock is cumulative. The

preferred dividends were not declared during 2015.

*64. The accounts receivable turnover for 2015 is

a. 6,400 ÷ 800.

b. 4,200 ÷ 800.

c. 6,400 ÷ 700.

d. 4,200 ÷ 700.

*65. The inventory turnover for 2015 is

a. 6,400 ÷ 1,300.

b. 4,200 ÷ 1,300.

c. 6,400 ÷ 1,200.

d. 4,200 ÷ 1,200.

*66. The profit margin on sales for 2015 is

a. 2,200 ÷ 6,400.

b. 750 ÷ 6,400.

c. 2,200 ÷ 4,200.

d. 750 ÷ 4,200.

*67. The return on common stock equity for 2015 is

a. 750 ÷ 3,600.

b. 750 ÷ 4,000.

c. 650 ÷ 3,600.

d. 650 ÷ 4,000.

*68. The book value per share of common stock at 12/31/15 is

a. 3,900 ÷ 120.

b. 3,880 ÷ 120.

c. 3,900 ÷ 110.

d. 4,000 ÷ 110.

*69. At December 31, 2015, the acid-test ratio was

a. 1,550 ÷ 650.

b. 1,550 ÷ 1,080.

c. 2,100 ÷ 800.

d. 2,850 ÷ 650.

*70. Presented below is information related to Tolbert Company.

Current Assets

Cash $ 4,000

Short-term investments 75,000

Accounts receivable 61,000

Inventories 110,000

Prepaid expenses 30,000

Total current assets $280,000

Full Disclosure in Financial Reporting

24 – 17

Total current liabilities are $100,000. What is the acid-test ratio?

a. 2.8 to 1.

b. 2.5 to 1.

c. 1.4 to 1.

d. 0.8 to 1.

*71. Perez Company’s net accounts receivable were $800,000 at December 31, 2014 and

$880,000 at December 31, 2015. Net cash sales for 2015 were $520,000. The accounts

receivable turnover for 2015 was 8.0. What were Perez’s total net sales for 2015?

a. $4,160,000.

b. $6,720,000.

c. $7,240,000.

d. $6,200,000.

*72. During 2015, Quirk, Incorporated purchased $3,500,000 of inventory. The cost of goods

sold for 2015 was $3,600,000 and the ending inventory at December 31, 2015, was

$400,000. What was the inventory turnover for 2015?

a. 7.0.

b. 7.2.

c. 8.0.

d. 9.0.

Multiple Choice Answers—Computational

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

MULTIPLE CHOICE—CPA Adapted

73. Which of the following facts concerning plant assets should be included in the summary of

significant accounting policies?

Depreciation Method Composition

a. No Yes

b. Yes Yes

c. Yes No

d. No No

74. Farr, Inc. is a multidivisional corporation which has both intersegment sales and sales to

unaffiliated customers. Farr should report segment financial information for each division

meeting which of the following criteria?

a. Segment profit or loss is 10% or more of consolidated profit or loss.

b. Segment profit or loss is 10% or more of combined profit or loss of all company

segments.

c. Segment revenue is 10% or more of combined revenue of all the company segments.

d. Segment revenue is 10% or more of consolidated revenue.

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 18

75. Unruh Corp. and its divisions are engaged solely in manufacturing operations. The

following data (consistent with prior years’ data) pertain to the industries in which

operations were conducted for the year ended December 31, 2015.

Assets

Industry Revenue Profit 12/31/15

A $ 8,000,000 $1,320,000 $16,000,000

B 6,400,000 1,120,000 14,000,000

C 4,800,000 960,000 10,000,000

D 2,400,000 440,000 5,200,000

E 3,400,000 540,000 5,600,000

F 1,200,000 180,000 2,400,000

$26,200,000 $4,560,000 $53,200,000

In its segment information for 2015, how many reportable segments does Unruh have?

a. Three

b. Four

c. Five

d. Six

76. The following information pertains to Nixon Corp. and its divisions for the year ended

December 31, 2015.

Sales to unaffiliated customers $3,000,000

Intersegment sales of products similar to those sold to

unaffiliated customers 900,000

Interest earned on loans to other operating segments 60,000

Nixon and all of its divisions are engaged solely in manufacturing operations. Nixon has a

reportable segment if that segment’s revenue exceeds

a. $396,000.

b. $390,000.

c. $306,000.

d. $300,000.

77. Advertising costs may be accrued or deferred to provide an appropriate expense in each

period for

Interim Year-end

Financial Reporting Financial Reporting

a. Yes No

b. Yes Yes

c. No No

d. No Yes

78. Mayo Corp. has estimated that total depreciation expense for the year ending December 31,

2015 will amount to $450,000, and that 2015 year-end bonuses to employees will total

$900,000. In Mayo’s interim income statement for the six months ended June 30, 2015,

what is the total amount of expense relating to these two items that should be reported?

a. $0.

b. $225,000.

c. $675,000.

d. $1,350,000.

Full Disclosure in Financial Reporting

24 – 19

79. Fina Corp. had the following transactions during the quarter ended March 31, 2015:

Loss from hurricane damage $420,000

Payment of fire insurance premium for calendar year 2015 700,000

What amount should be included in Fina’s income statement for the quarter ended

March 31, 2015?

Extraordinary Loss Insurance Expense

a. $420,000 $700,000

b. $420,000 $175,000

c. $105,000 $175,000

d. $0 $700,000

80. For interim financial reporting, an extraordinary gain occurring in the second quarter

should be

a. recognized ratably over the last three quarters.

b. recognized ratably over all four quarters with the first quarter being restated.

c. recognized in the second quarter.

d. disclosed by note only in the second quarter.

*81. How is the average inventory used in the calculation of each of the following?

Acid-Test (Quick) Ratio Inventory Turnover

a. Numerator Numerator

b. Numerator Denominator

c. Not Used Denominator

d. Not Used Numerator

*82. Which of the following ratios is(are) useful in assessing a company’s ability to meet

current maturing or short-term obligations?

Acid-Test Ratio Debt to Assets Ratio

a. No No

b. No Yes

c. Yes Yes

d. Yes No

*83. Which of the following ratios should be used in evaluating the effectiveness with which the

company uses its assets?

Accounts receivable Turnover Payout Ratio

a. Yes Yes

b. No No

c. Yes No

d. No Yes

Multiple Choice Answers—CPA Adapted

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Item

Ans.

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 20

DERIVATIONS — Computational

No. Answer Derivation

Full Disclosure in Financial Reporting

24 – 21

DERIVATIONS — Computational (cont.)

No. Answer Derivation

DERIVATIONS — CPA Adapted

No. Answer Derivation

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 22

BRIEF EXERCISES

BE. 24-84—Notes to financial statements.

An article in Dun’s Review made the following comments:

“Every other year, say, companies should print the notes in big type

and the base figures in smaller ones.”

Instructions

(a) Are notes considered as part of the financial statements and what basic purpose do they

serve?

(b) What are the general types of notes?

Solution 24-84

BE. 24-85—Segment reporting.

The Financial Accounting Standards Board requires the reporting of disaggregated financial data

about the different types of business activities in which an enterprise engages.

Instructions

Identify 4 of the 6 items of disaggregated information the FASB requires that an enterprise report.

Solution 24-85

Full Disclosure in Financial Reporting

24 – 23

EXERCISES

Ex. 24-86—Segment reporting.

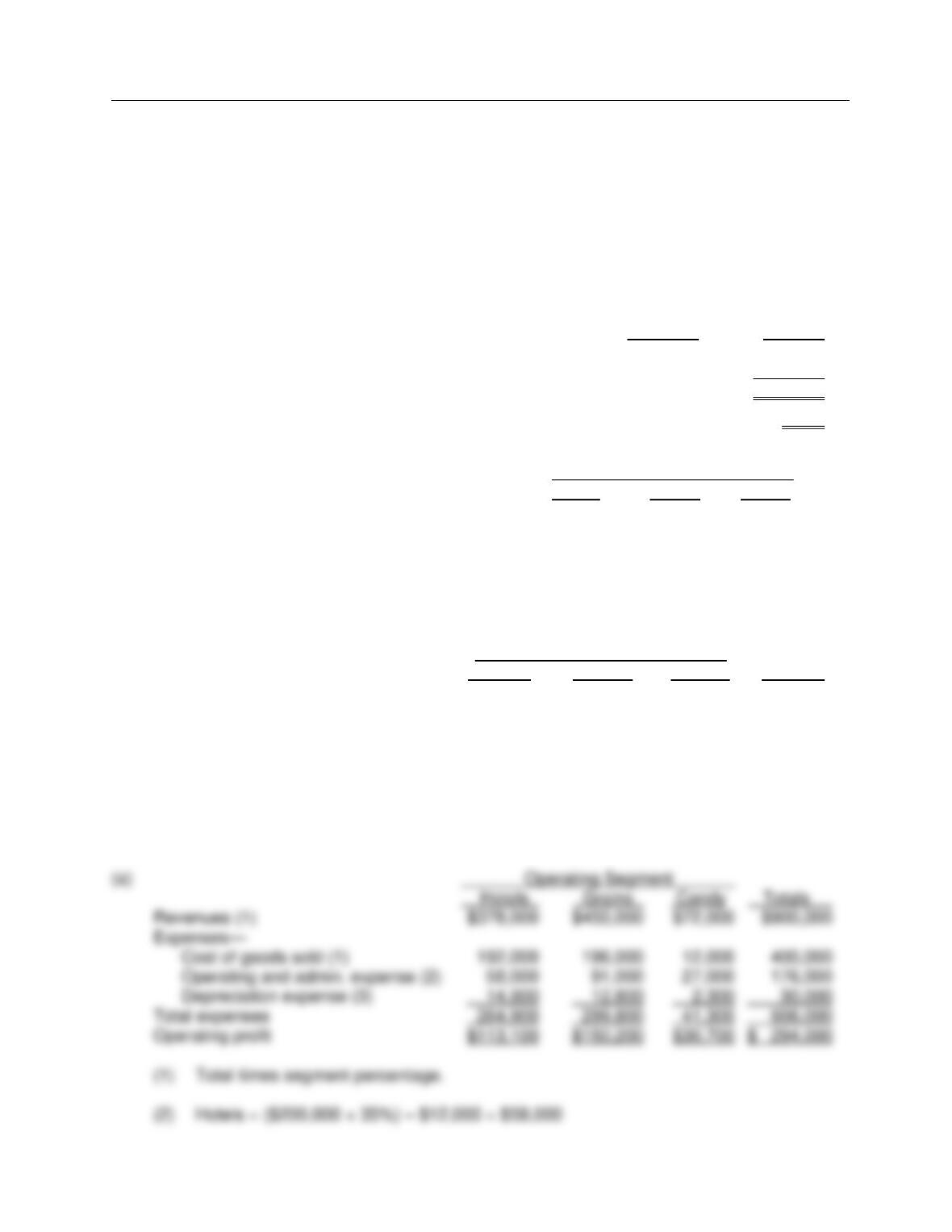

Finney Company’s condensed income statement is presented below:

Revenues $900,000

Expenses

Cost of goods sold $400,000

Operating and administrative expenses 200,000

Depreciation expense 40,000 640,000

Income before taxes 260,000

Income tax expenses 78,000

Net income $182,000

Earnings per share (100,000 shares) $1.82

The following data is compiled relative to Finney’s operating segments:

Percent Identified with Segment

Hotels Grains Candy

Revenues 42% 50% 8%

Cost of goods sold 48 49 3

Operating and administrative expense 35 50 15

Depreciation expense 46 42 12

Included in the amounts allocated to each segment on the above percentages are the following

expenses which relate to general corporate activities:

Operating Segment

Hotels Grains Candy Totals

Operating and administrative expense $12,000 $9,000 $3,000 $24,000

Depreciation expense 3,500 4,000 2,500 10,000

Instructions

(a) Prepare a schedule showing the amounts distributed to each segment.

(b) Based only on the above information, which segments must be reported and why?

Solution 24-86

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 24

Ex. 24-87—Interim reports.

A few years ago, a publishing company in the fourth quarter had a net profit figure that exceeded

sales for that quarter. Such a situation as this suggests that some difficult accounting issues are

involved in interim reporting.

Instructions

(a) What are the major accounting problems related to interim reports?

(b) What problem exists with income taxes in interim reports and how does GAAP recommend

that taxes be reported? What does GAAP require?

(c) Many academicians have attempted to predict the year’s net income after the first quarter’s

income is reported. These attempts are generally unsuccessful, no matter how sophisticated

the prediction model. What might be the reason for this inability to predict?

Solution 24-87

Full Disclosure in Financial Reporting

24 – 25

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 26

Ex. 24-88—Inventory and cost of goods sold at interim dates.

Discuss how inventory and cost of goods sold may be afforded special accounting treatment at

interim dates.

Solution 24-88

Ex. 24-89—Forecasts.

Recent proposals by investors and others have suggested that corporations include financial

forecasts in their annual reports. It further has been suggested that the CPA attest to those

forecasts.

Instructions

(a) What arguments are advanced to support the publication of such forecasts?

(b) What arguments are advanced that oppose the publication of such forecasts?

Solution 24-89

Full Disclosure in Financial Reporting

24 – 27

Solution 24-89 (cont.)

*Ex. 24-90—Financial statement analysis.

The condensed financial statements of Marks Company for the years 2014-2015 are presented

below: Marks Company

Comparative Balance Sheets

As of December 31, 2014 and 2015

2015 2014

Cash $ 420,000 $ 120,000

Accounts receivable (net) 360,000 300,000

Inventories 380,000 340,000

Plant and equipment 1,800,000 1,112,000

Accumulated depreciation (260,000) (192,000)

$2,700,000 $1,680,000

Accounts payable $ 340,000 $ 160,000

Dividends payable -0- 40,000

Bonds payable 400,000 -0-

Common stock ($10 par) 1,520,000 1,200,000

Retained earnings 440,000 280,000

$2,700,000 $1,680,000

Additional data:

Market value of stock at 12/31/15 is $80 per share.

Marks sold 32,000 shares of common stock at par on July 1, 2015.

Marks Company

Condensed Income Statement

For the Year Ended December 31, 2015

Sales revenue $2,400,000

Cost of goods sold 1,650,000

Gross profit 750,000

Administrative and selling expenses 500,000

Net income $ 250,000

Instructions

Compute the following financial ratios by placing the proper amounts in the parentheses provided

for numerators and denominators.

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 28

*Ex. 24-90 (cont.)

a. Current ratio at 12/31/15 ( )

( )

b. Acid test ratio at 12/31/15 ( )

( )

c. Accounts receivable turnover in 2015 ( )

( )

d. Inventory turnover in 2015 ( )

( )

e. Profit margin on sales in 2015 ( )

( )

f. Earnings per share in 2015 ( )

( )

g. Return on common stock equity in 2015 ( )

( )

h. Price earnings ratio at 12/31/15 ( )

( )

i. Debt to assets at 12/31/15 ( )

( )

j. Book value per share at 12/31/15 ( )

( )

*Solution 24-90

Full Disclosure in Financial Reporting

24 – 29

*Ex. 24-91—Selected financial ratios.

The following information pertains to Wamser Company:

Cash $ 20,000

Accounts receivable 125,000

Inventory 75,000

Plant assets (net) 380,000

Total assets $600,000

Accounts payable $ 75,000

Accrued taxes and expenses payable 25,000

Long-term debt 50,000

Common stock ($10 par) 160,000

Paid-in capital in excess of par 90,000

Retained earnings 200,000

Total equities $600,000

Net sales (all on credit) $800,000

Cost of goods sold 600,000

Net income 81,000

Instructions

Compute the following: (It is not necessary to use averages for any balance sheet figures

involved.)

(a) Current ratio

(b) Inventory turnover

(c) Accounts receivable turnover

(d) Book value per share

(e) Earnings per share

(f) Debt to assets

(g) Profit margin on sales

(h) Return on common stock equity

*Solution 24-91

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 30

*Ex. 24-92—Computation of selected ratios.

The following data is given:

December 31,

2015 2014

Cash $ 66,000 $ 50,000

Accounts receivable (net) 90,000 60,000

Inventories 90,000 110,000

Plant assets (net) 383,000 325,000

Accounts payable 55,000 40,000

Salaries and wages payable 10,000 5,000

Bonds payable 70,000 70,000

8% Preferred stock, $40 par 100,000 100,000

Common stock, $10 par 120,000 90,000

Paid-in capital in excess of par 80,000 65,000

Retained earnings 194,000 175,000

Net credit sales 900,000

Cost of goods sold 700,000

Net income 81,000

Instructions

Compute the following ratios:

(a) Acid-test ratio at 12/31/15

(b) Accounts receivable turnover in 2015

(c) Inventory turnover in 2015

(d) Profit margin on sales in 2015

(e) Return on common stock equity in 2015

(f) Book value per share of common stock at 12/31/15

*Solution 24-92

Full Disclosure in Financial Reporting

24 – 31

PROBLEMS

Pr. 24-93—Segment reporting.

A central issue in reporting on operating segments of a business enterprise is the determination

of which segments are reportable.

Instructions

1. What are the tests to determine whether or not an operating segment is reportable?

2. What is the test to determine if enough operating segments have been separately reported

upon, and what is the guideline on the maximum number of operating segments to be shown?

Solution 24-93

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 32

Pr. 24-94—Interim reporting.

Interim financial reporting has become an important topic in accounting. There has been

considerable discussion as to the proper method of reflecting results of operations at interim

dates. Accordingly, the Accounting Principles Board issued an opinion clarifying some aspects of

interim financial reporting.

Instructions

(a) Discuss generally how revenue should be recognized at interim dates and specifically how

revenue should be recognized for industries subject to large seasonal fluctuations in

revenue and for long-term contracts using the percentage-of-completion method at annual

reporting dates.

(b) Discuss generally how product and period costs should be recognized at interim dates. Also

discuss how inventory and cost of goods sold may be afforded special accounting treatment

at interim dates.

(c) Discuss how the provision for income taxes is computed and reflected in interim financial

statements.

Solution 24-94

Full Disclosure in Financial Reporting

24 – 33

Solution 24-94 (cont.)

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 34

IFRS QUESTIONS

True/False

1. Due to the broader range of options available under U.S. GAAP compared to IFRS, note

disclosures are generally more expansive under U.S. GAAP than under IFRS.

2. IFRS requires companies to prepare interim reports on a quarterly basis.

3. IFRS requires segment reporting, and uses the management approach to identify reportable

segments.

4. IFRS requires companies to disclose transactions with related parties, including the name of

the related party and any doubtful amounts related to outstanding balances for the related

party.

5. Neither U.S. GAAP nor IFRS requires interim reports.

Multiple Choice

6. If Benjamin Company and Iris, Inc. are similar companies in every regard, except

Benjamin Company uses IFRS while Iris, Inc. uses U.S. GAAP, which of the following is

true?

a. Iris, Inc. is required to issue interim statements every 6 months.

b. Benjamin Company need not recognize post-balance sheet events.

c. Benjamin Company is not required by IFRS to issue interim statements.

d. All of the above are true.

7. Benjamin Company uses IFRS, while Iris, Inc. uses U.S. GAAP, for their external

financial reporting. On January 16, 2015, both companies settled lawsuits relating to

industrial accidents that occurred in 2013. Benjamin Company paid $550,000 and Iris, Inc.

paid $230,000. Assuming that no accrual had been previously made, what amount of loss

should be reported on the income statement for the year ended December 31, 2014 for

each company?

Benjamin Company Iris, Inc.

a. $-0- $-0-

b. $550,000 $230,000

c. $-0- $230,000

d. $550,000 $-0-

Full Disclosure in Financial Reporting

24 – 35

8. IFRS requires which of the following disclosures regarding related parties?

I. The name of the related party.

II. The amount and terms of the outstanding balance.

III. Doubtful amounts related to the outstanding balance.

a. I, II, and III.

b. I and II.

c. I and III.

d. II and III.

9. Nicole, Inc. uses IFRS for its external financial reporting. During 2013, an employee of

the company was injured in the factory. Discussions with corporate attorneys resulted in a

determination that the company would be required to pay between $1,500,000 and

$3,000,000 to settle the injury claim. Nicole, Inc. accrued a contingent liability on

December 31, 2013 for $1,500,000. On February 4, 2014, Nicole, Inc. settled the lawsuit

for $3,300,000. What amount of loss should be reported on the income statement for the

year ended December 31, 2014 for Nicole, Inc. related to this lawsuit?

a. $3,300,000

b. $1,800,000

c. $1,500,000

d. $300,000.

10. Identifiable assets for the 4 industry segments of Brittle Company are as follows:

Candy $120,000

Stix $240,000

Chips $980,000

Gum $ 45,000

Brittle Company uses IFRS for its external financial reporting. Using only the identifiable

assets test, which of the segments are reportable?

a. Under IFRS, all four segments must be reported.

b. Candy, Stix, and Chips only.

c. Chips only.

d. Stix and Chips only.

11. Operating profits and losses for the 4 industry segments of Brittle Company are as

follows: Candy ($590,000)

Stix $ 20,000

Chips $ 85,000

Gum $ 9,000

Brittle Company uses IFRS for its external financial reporting. Using only the operating

profits (loss) test, which of the segments are reportable?

a. Under IFRS, all four segments must be reported.

b. Stix, Chips, and Gum only.

c. Candy and Chips only.

d. Candy only.

Test Bank for Intermediate Accounting, Fifteenth Edition

24 – 36

12. Which of the following is true regarding IFRS and GAAP?

a. Due to the broader range of options available under U.S. GAAP compared to IFRS,

note disclosures are generally more expansive under U.S. GAAP than under IFRS.

b. IFRS requires companies to prepare interim reports on a quarterly basis.

c. IFRS requires segment reporting, and uses the management approach to identify

reportable segments.

d. U.S. GAAP requires companies to disclose transactions with related parties, including

the name of the related party and any doubtful amounts related to outstanding

balances for the related party.

*13. IFRS is important for U.S. investors for all of the following reasons except

a. the SEC requires that foreign companies that list on U.S. stock exchanges provide a

reconciliation between IFRS and U.S. GAAP.

b. many U.S. companies, such as McDonald’s, generate 50% of their sales outside the

U.S.

c. mergers frequently take place between companies from different countries.

d. financial markets are among the most significant international markets.

*14. Challenges to convergence of IFRS with U.S. GAAP include all of the following

except

a. cultural differences exist between countries.

b. the litigious environment in the U.S. is best suited to very detailed standards.

c. legal barriers to change include the difficulty associated with changing loan covenants.

d. political issues result in politicians setting the final accounting standards.

*15. High-quality standards in an international environment include which of the following?

a. They permit a wide variety of alternative practices.

b. They are stated in ambiguous terms to allow practitioners the opportunity to interpret

and implement.

c. They are comprehensive, covering major transactions facing companies.

d. All of the above are necessary for high-quality international standards.

Answers to Multiple Choice:

Short Answer

16. Bill Novak is working on an audit of an IFRS client. In his review of the client’s interim reports, he

notes that the reports are prepared on a discrete basis. That is, each interim report is viewed as a

distinct period. Is this acceptable under IFRS? If so, explain how that treatment could affect

comparisons to U.S. GAAP company?

Full Disclosure in Financial Reporting

24 – 37