CHAPTER 9

Inventories: Additional Valuation Issues

SOLUTIONS TO B PROBLEMS

PROBLEM 9-1

Item

Cost

Replacement

Cost

Ceiling*

Floor**

Designated

Market

Lower-of–

Cost-or–

Market

A

$470

$ 460

$ 450

$350

$ 450

$450

B

450

430

480

372

430

430

C

830

610

820

640

640

640

D

960

1,000

1,070

830

1,000

960

PROBLEM 9-2

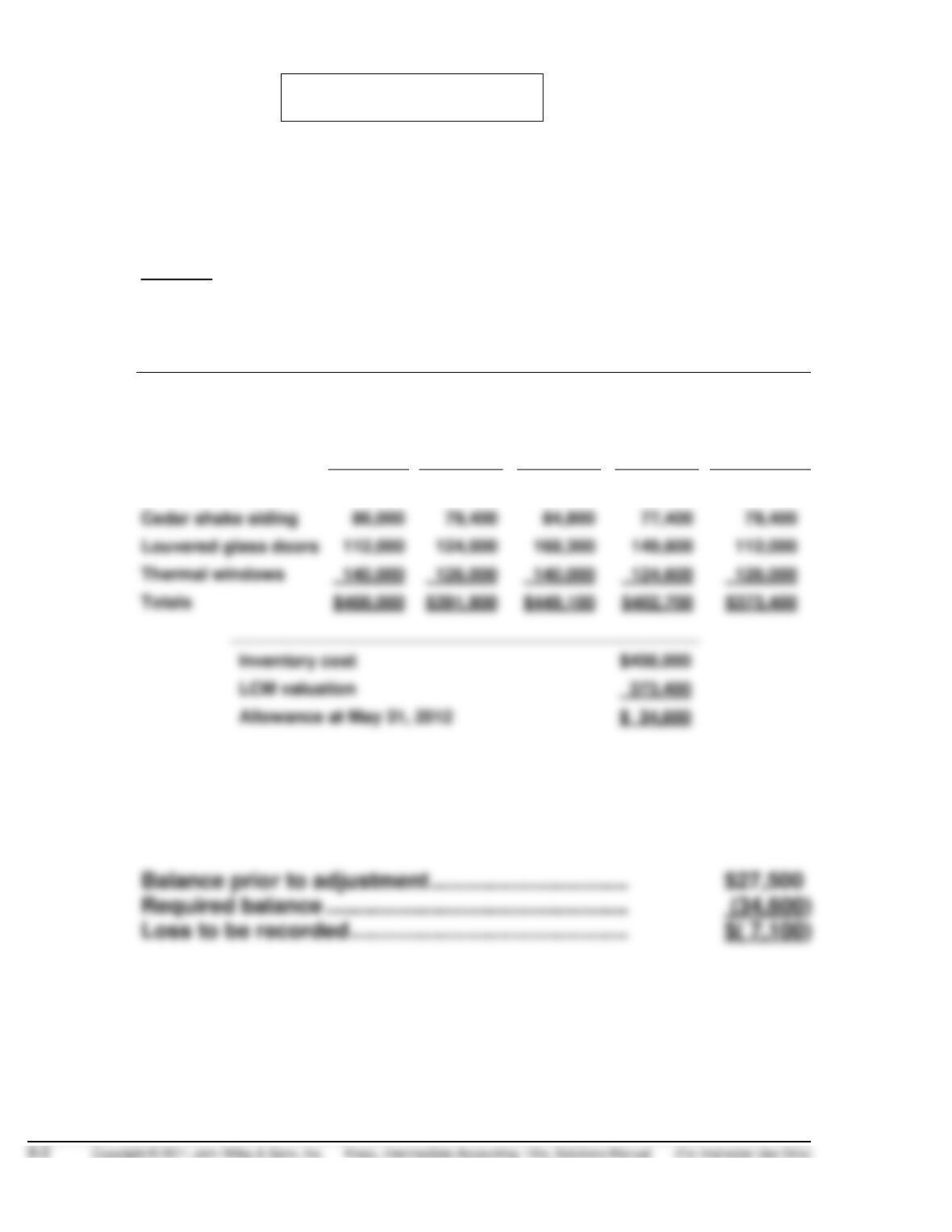

(a) 1. The balance in the Allowance to Reduce Inventory to Market at

May 31, 2012, should be $34,600, as calculated in Exhibit 1 below.

Exhibit 1

CALCULATIONS OF PROPER BALANCE

in the Allowance to Reduce Inventory to Market

At May 31, 2012

Cost

Replace-

ment

Cost

NRV

(Ceiling)

NRV less

normal

profit

(Floor)

LCM

Aluminum siding

$ 70,000

$ 62,500

$ 56,000

$ 50,900

$ 56,000

Cedar shake siding

86,000

79,400

84,800

77,400

79,400

Louvered glass doors

Thermal windows

Totals

$408,000

2. For the fiscal year ended May 31, 2012, the loss that would be

recorded due to the change in the Allowance to Reduce Inventory

to Market would be $7,100, as calculated below.

PROBLEM 9-2 (Continued)

(b) The use of the lower-of-cost–or–market (LCM) rule is based on both the

expense recognition principle and the concept of conservatism. The

PROBLEM 9-3

(a)

12/31/12 (Cost-of–goods-sold Method)

Cost of Goods Sold …………………………………………………

68,000

Inventory …………………………..…………………………..

Cost of Goods Sold …………………………………………………

75,000

Inventory …………………………..…………………………..

(b)

12/31/12 (Loss Method)

To write down inventory to market:

Loss Due to Market Decline of Inventory ………………….

68,000

Allowance to Reduce Inventory to Market …………

To write down inventory to market:

Loss Due to Market Decline of Inventory ………………….

Allowance to Reduce Inventory to Market

[($905,000 – $830,000) – $68,000] …………………..

PROBLEM 9-4

Beginning inventory ……………………………………………..

$ 80,000

Purchases ……………………………………………………………

290,000

370,000

Purchase returns ………………………………………………….

(28,000)

Total goods available ……………………………………………

342,000

Sales ……………………………………………………………………

Sales returns ……………………………………………………….

Less: Gross profit (35% of $394,000) …………………….

Ending inventory (unadjusted for damage) …………….

Less: Goods on hand—undamaged

($30,000 X [1 – 35%]) …………………………………..

Inventory damaged ………………………………………………

Less: Salvage value of damaged inventory……………

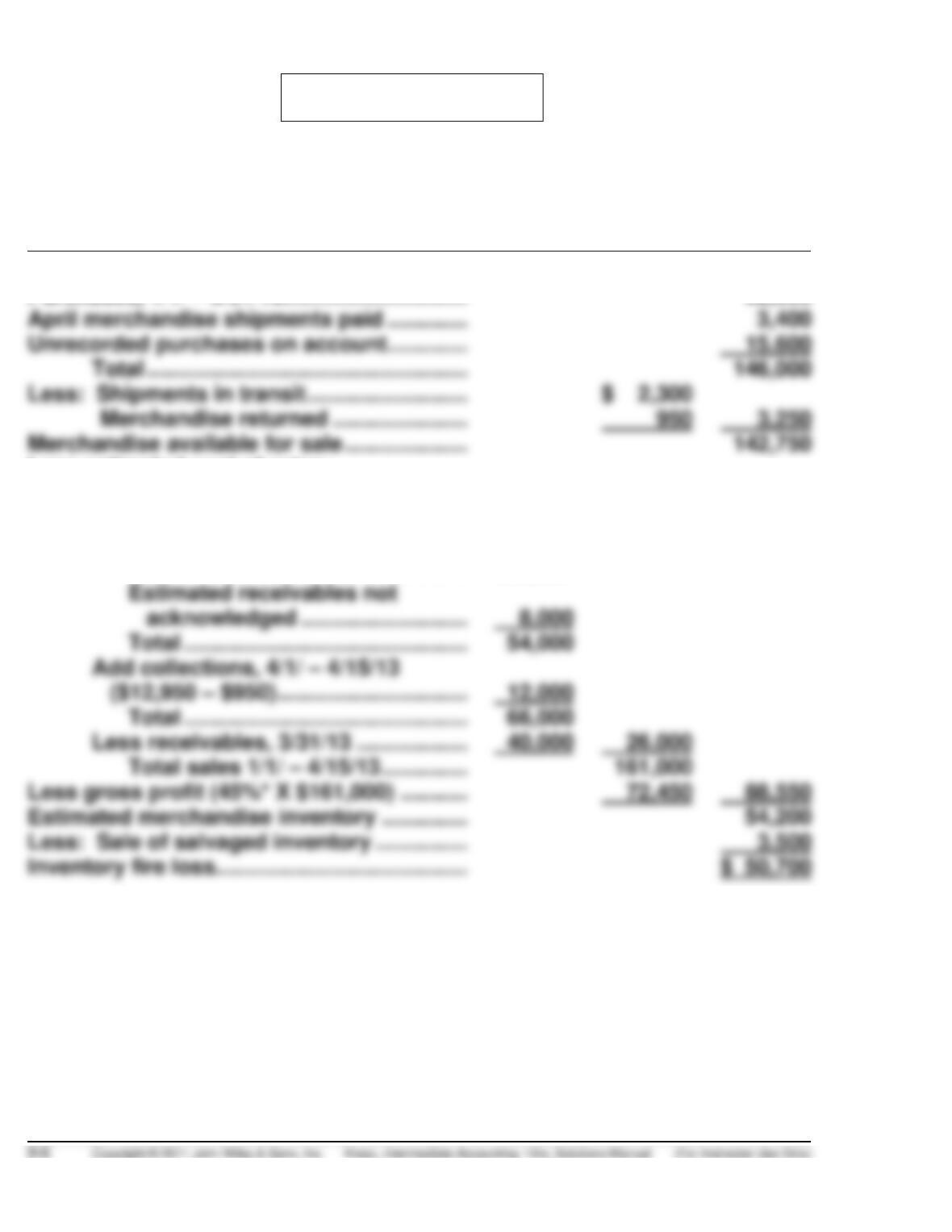

PROBLEM 9-5

STANISLAW CORPORATION

Computation of Inventory Fire Loss

April 15, 2013

Inventory, 1/1/13 …………………………………….

$ 75,000

Purchases, 1/1/ – 3/31/13…………………………

52,000

April merchandise shipments paid ………….

Unrecorded purchases on account ………….

Total …………………………………………….

146,000

Less: Shipments in transit ……………………..

$ 2,300

Merchandise returned ………………….

Merchandise available for sale ………………..

142,750

Less estimated cost of sales:

Sales, 1/1/ – 3/31/13 ……………………….

135,000

Sales, 4/1/ – 4/15/13

Receivables acknowledged

at 4/15/13 ………………………………

$46,000

Estimated receivables not

acknowledged ………………………

Add collections, 4/1/ – 4/15/13

($12,950 – $950) ………………………….

Total ……………………………………….

Less receivables, 3/31/13 ………………

Total sales 1/1/ – 4/15/13 …………..

Less gross profit (45%* X $161,000) ………..

Estimated merchandise inventory …………..

54,200

Less: Sale of salvaged inventory ……………

3,500

PROBLEM 9-5 (Continued)

*Computation of Gross Profit Rate

Net sales, 2011 …………………………………………

$390,000

Net sales, 2012 …………………………………………

530,000

Total net sales …………………………………

920,000

Net purchases, 2011 ………………………………….

235,000

Net purchases, 2012 ………………………………….

280,000

Less: Ending inventory …………………………....

506,000

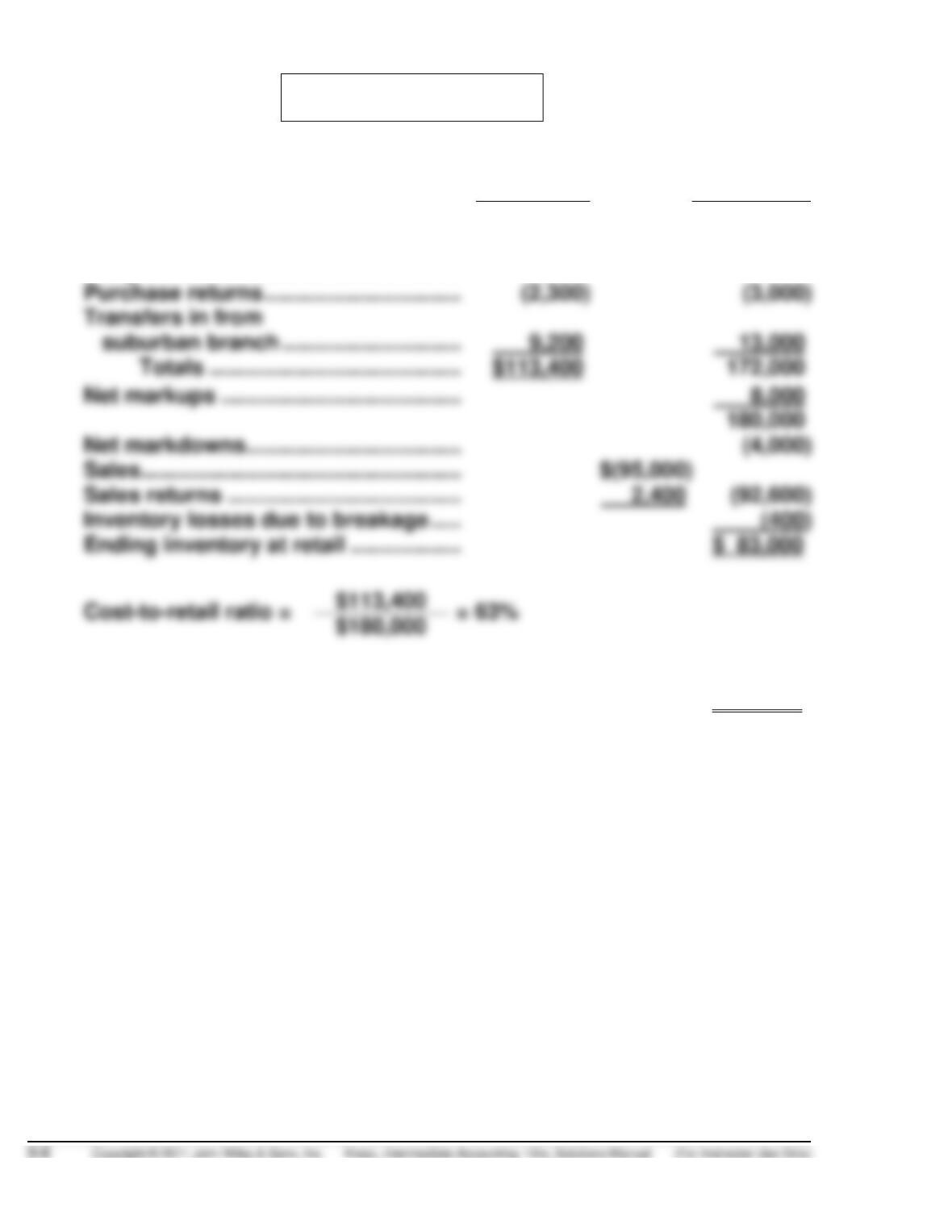

PROBLEM 9-6

(a)

Cost

Retail

Beginning Inventory ………………………

$ 17,000

$ 25,000

Purchases …………………………………….

82,500

137,000

Freight-in ………………………………………

7,000

Purchase returns …………………………..

Totals …………………………………..

Net markups …………………………………

180,000

Net markdowns ……………………………..

Sales …………………………………………….

$(95,000)

Sales returns ………………………………..

Inventory losses due to breakage …..

Ending inventory at retail ………………

$ 83,000

(b)

Ending inventory at lower-of-average-cost-or-market

(63% of $83,000) …………………………

$ 52,290

Copyright © 2011 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 14/e, Solutions Manual (For Instructor Use Only) 9-9

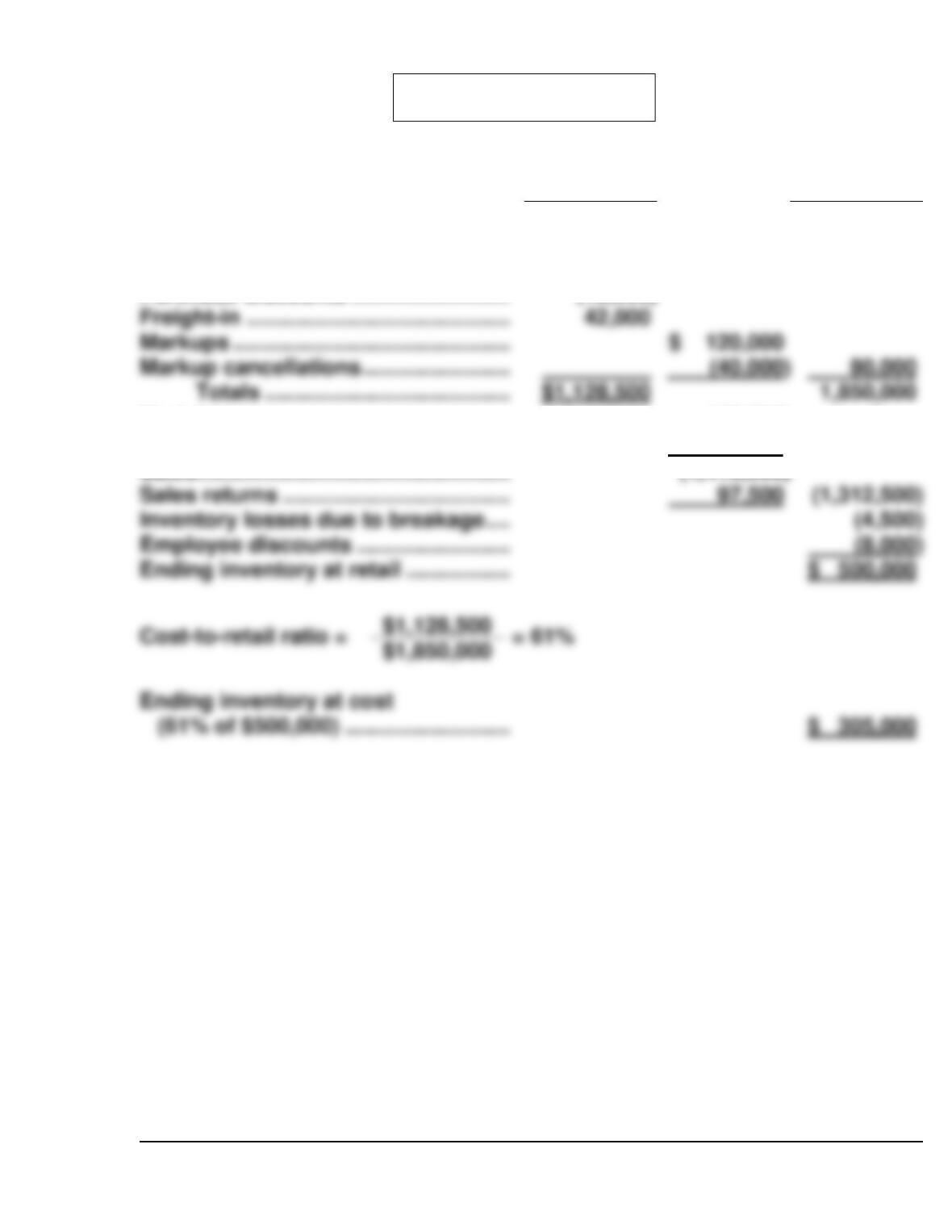

PROBLEM 9-7

Cost

Retail

Beginning Inventory ……………………..

$ 250,000

$ 390,000

Purchases ……………………………………

914,500

1,460,000

Purchase returns ………………………….

(60,000)

(80,000)

Purchase discounts ……………………..

(18,000)

Markdowns ………………………………….

(45,000)

Markdown cancellations ……………….

20,000

(25,000)

Sales ……………………………………………

(1,410,000)

Sales returns ……………………………….

(1,312,500)

Inventory losses due to breakage ….

Employee discounts …………………….

Markups ………………………………………

$ 120,000

Markup cancellations ……………………

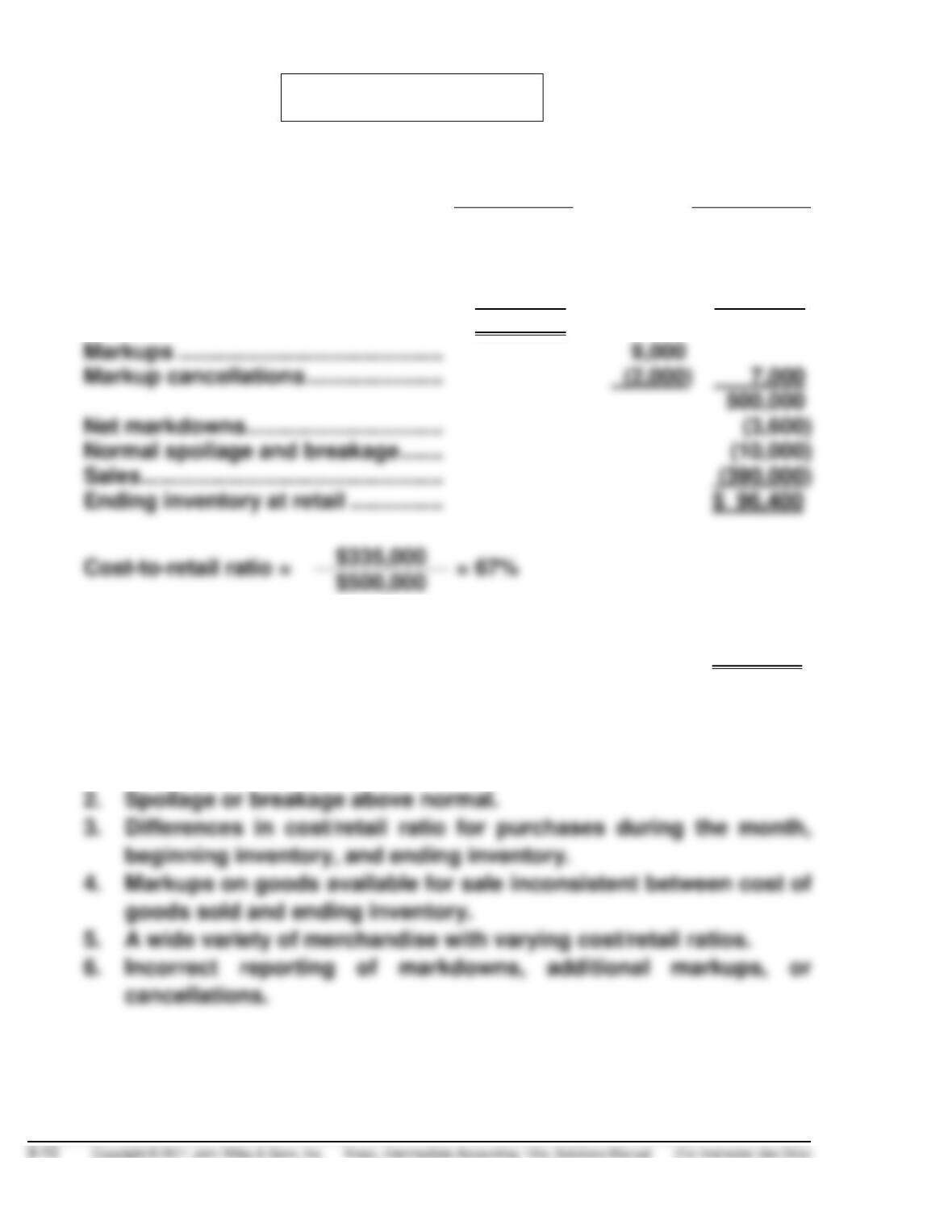

PROBLEM 9-8

(a)

Cost

Retail

Inventory (beginning) ………………….

$ 52,000

$ 78,000

Purchases ………………………………….

272,000

423,000

Purchase returns ………………………..

(5,600)

(8,000)

Freight-in ……………………………………

16,600

Totals ………………………………..

$335,000

493,000

Markups …………………………………….

Markup cancellations ………………….

Net markdowns …………………………..

(3,600)

Normal spoilage and breakage …….

Sales ………………………………………….

Ending inventory at retail ……………

$ 96,400

Ending inventory at lower-of-cost-or-market

(67% of $96,400) ………………………

$ 64,588

(b) The difference between the inventory estimate per retail method and

the amount per physical count may be due to:

1. Theft losses (shoplifting or pilferage).

PROBLEM 9-9

(a) The inventory section of Maddox’s balance sheet as of November 30,

2012, including required footnotes, is presented below. Also presented

below are the inventory section supporting calculations.

Current assets

Finished goods (Note 2.) ……………………

Work-in-process ………………………………..

Factory supplies………………………………..

Note 1. Lower-of-cost (first-in, first-out) or-market is applied on a

major category basis for finished goods, and on a total inven-

tory basis for work-in-process, raw materials, and factory

supplies.