CHAPTER 22

SOLUTIONS TO B PROBLEMS

PROBLEM 22-1B

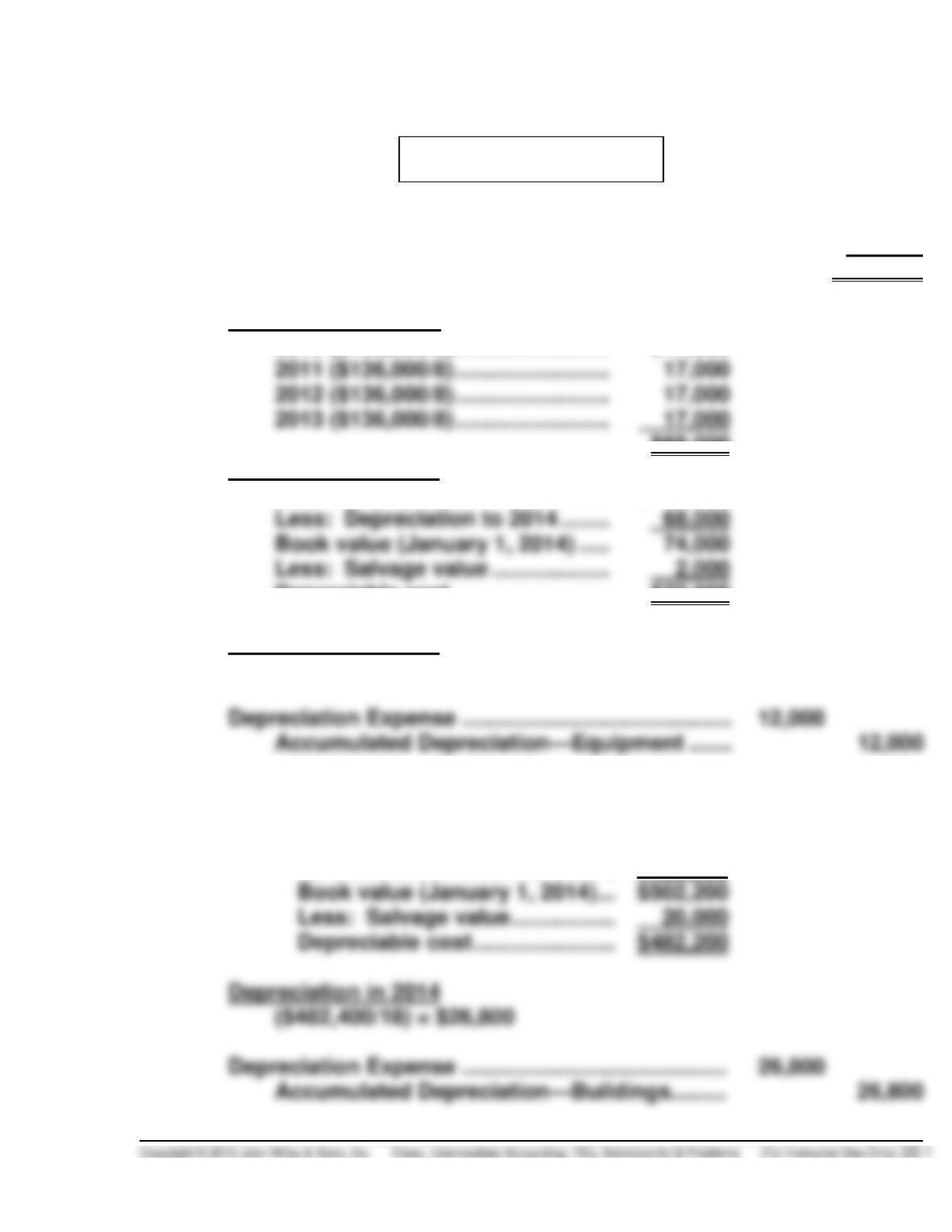

(a) 1. Cost of equipment …………………………………………………. $142,000

Less: Salvage value ……………………………………………….. 6,000

Depreciable cost ……………………………………………………. $136,000

Depreciation to 2014

2010 ($136,000/8) ……………………. $17,000

$68,000

Depreciation in 2014

Cost of equipment ………………….. $142,000

Depreciable cost ……………………. $72,000

Depreciation in 2014

$72,000/6 = $12,000

2. Cost of Building …………………………….. $620,000

Less: Depreciation to 2014

2012 ……………………………………. 62,000

2013 ……………………………………. 55,800

PROBLEM 22-1B (Continued)

3. Depreciation Expense ($72,000 – $9,000) ÷ 6 ……… 10,500

Accumulated Depreciation—Machinery ……… 10,500

Depreciation

taken

Depreciation that

should be taken

Differences

2012

$6,000

$5,250

$ 750

2013

(b) BISHOP WAY COMPANY

Comparative Income Statements

For the Years 2014 and 2013

2014

2013

Income before depreciation expense ………………..

$420,000

$386,000

Net income ……………………………………………………..

$170,700

$202,700

*Depreciation Expense

$ 12,000

PROBLEM 22-2B

(a) 1. Bad debt expense for 2014 should not have been reduced by

$26,000. A change in the experience rate is considered a change

in estimate, which should be handled prospectively.

(b) ROYAL PALM INC.

Comparative Income Statements

For the Years 2012 through 2014

2012

2013

2014

(45,000)

Income before

2012

2013

2014

Net income (unadjusted)

$230,000

$205,000

$240,000

1. Bad debt expense

adjustment

(26,000)

PROBLEM 22-3B

1. Retained Earnings ……………………………………………. 6,100

Sales Commissions Payable ………………………. 4,500

Sales Commissions Expense ……………………… 1,600

3. Accumulated Depreciation—Equipment …………….. 18,000

Depreciation Expense ………………………………… 18,000*

4. Construction in Process……………………………………. 46,000

PROBLEM 22-4B

(a) POWER CORPORATION

Projected Income Statement

For the Year Ended December 31, 2014

Sales …………………………………………….. $45,000,000

Cost of goods sold ………………………… $26,000,000

Depreciation expense …………………….. 2,200,000a

Conditions met:

1. Net income before taxes and bonus > $5,000,000.

2. Payable for income taxes does not exceed $1,800,000.

aDepreciation for the current year includes $1,600,000 for the old

equipment and $1,200,000 for the robotic equipment. If the robotic

PROBLEM 22-4B (Continued)

(b) Students’ answers will vary.

There is nothing unethical about changing the first-year election of

depreciation back to the straight-line method provided that it meets with

the approval of appropriate corporate decision makers. Considering the

the attention of the board of directors.

Some stakeholders and their interests are:

Stakeholder

Interests

President

Personal gain of $1,000,000 bonus.

CFO

Placed in ethical dilemma between the interests

of the president and the corporation.

Board of Directors

May be subject to the manipulations of the CEO

PROBLEM 22-5B

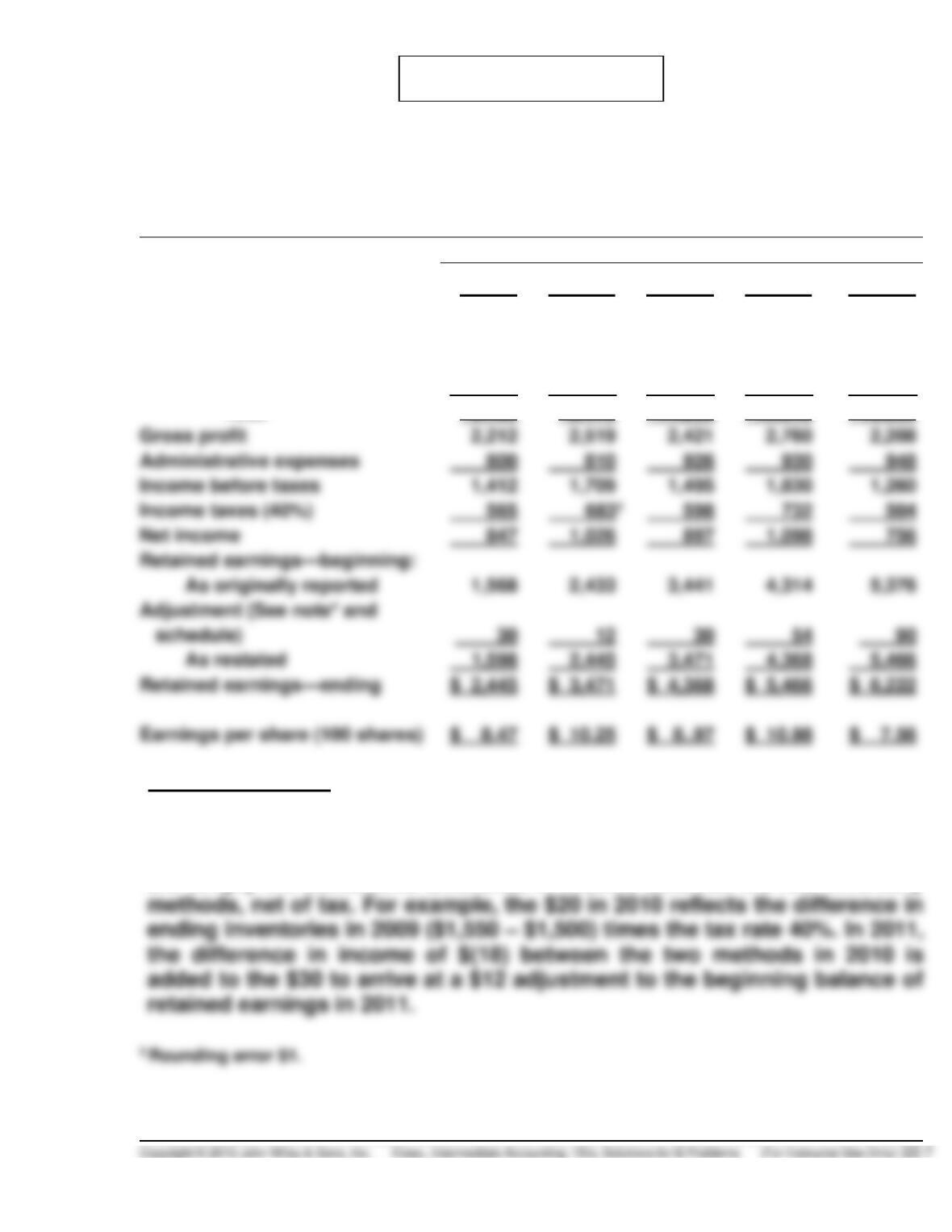

CAO FIXTURES COMPANY

Statement of Income and Retained Earnings

For the Years Ended May 31

2010

2011

2012

2013

2014

Sales—net

$8,642

$10,689

$14,381

$15,400

$16,098

Cost of goods sold

Beginning inventory

1,550

1,120

1,050

1,690

2,150

Purchases

6,000

8,100

12,600

13,100

13,900

Ending inventory

(1,120)

(1,050)

(1,690)

(2,150)

(2,160)

Total

6,430

8,170

11,960

12,640

13,890

Gross profit

2,212

2,519

2,421

Administrative expenses

Income before taxes

1,412

1,495

1,830

1,260

Income taxes (40%)

Net income

1,026

1,098

As originally reported

2,433

3,441

4,314

As restated

Earnings per share (100 shares)

*Note to instructor:

The retained earnings balances are usually reported in the above manner.

If desired, only the restated balances might be reported. The adjustments

are simply the cumulative difference in income between the two inventory

PROBLEM 22-5B (Continued)

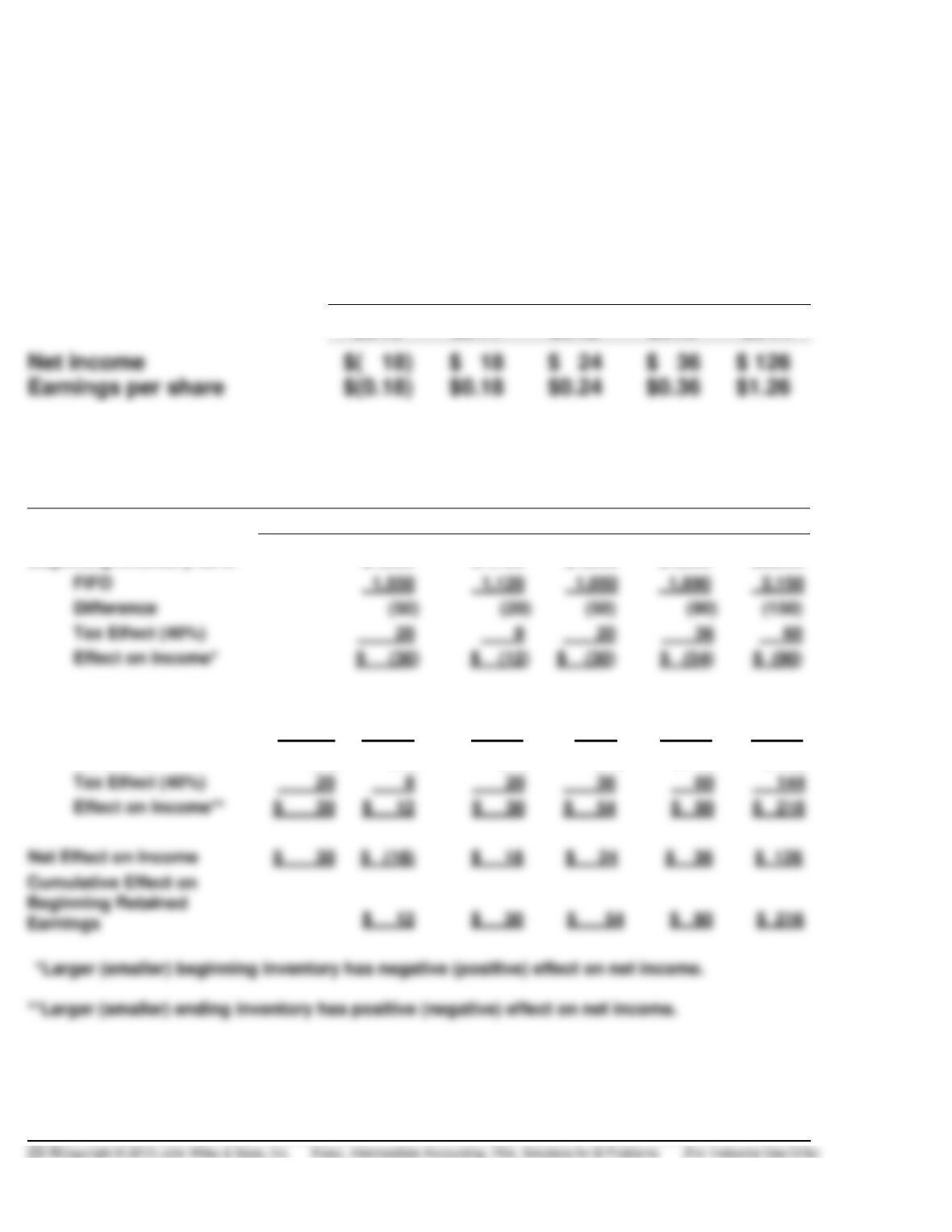

In 2014, the Company changed its method of pricing inventory from the

last-in, first out (LIFO) to the first-in first-out (FIFO) method in order to more

fairly present the financial operations of the company. The financial

statements for prior years have been restated to retrospectively reflect this

change, resulting in the following effects on net income and related per

share amounts:

Increase in

2010

2011

2012

2013

2014

Schedule of Income Reconciliation

and Retained Earnings Adjustments

2010–2014

2007

2010

2011

2012

2013

2014

Beginning Inventory LIFO

$1,500

$1,100

$1,000

$1,600

$2,000

FIFO

1,550

1,120

1,690

2,150

Difference

Tax Effect (40%)

36

Effect on Income*

$ (90)

Ending Inventory LIFO

$1,500

$1,100

$1,000

$1,600

$2,000

$1,800

FIFO

1,550

1,120

1,050

1,690

2,150

2,160

Difference

(50)

(20)

(50)

(90)

(150)

(360)

Tax Effect (40%)

20

20

60

Effect on Income**

$ 12

$ 30

$ 90

Net Effect on Income

$ 18

PROBLEM 22-6B

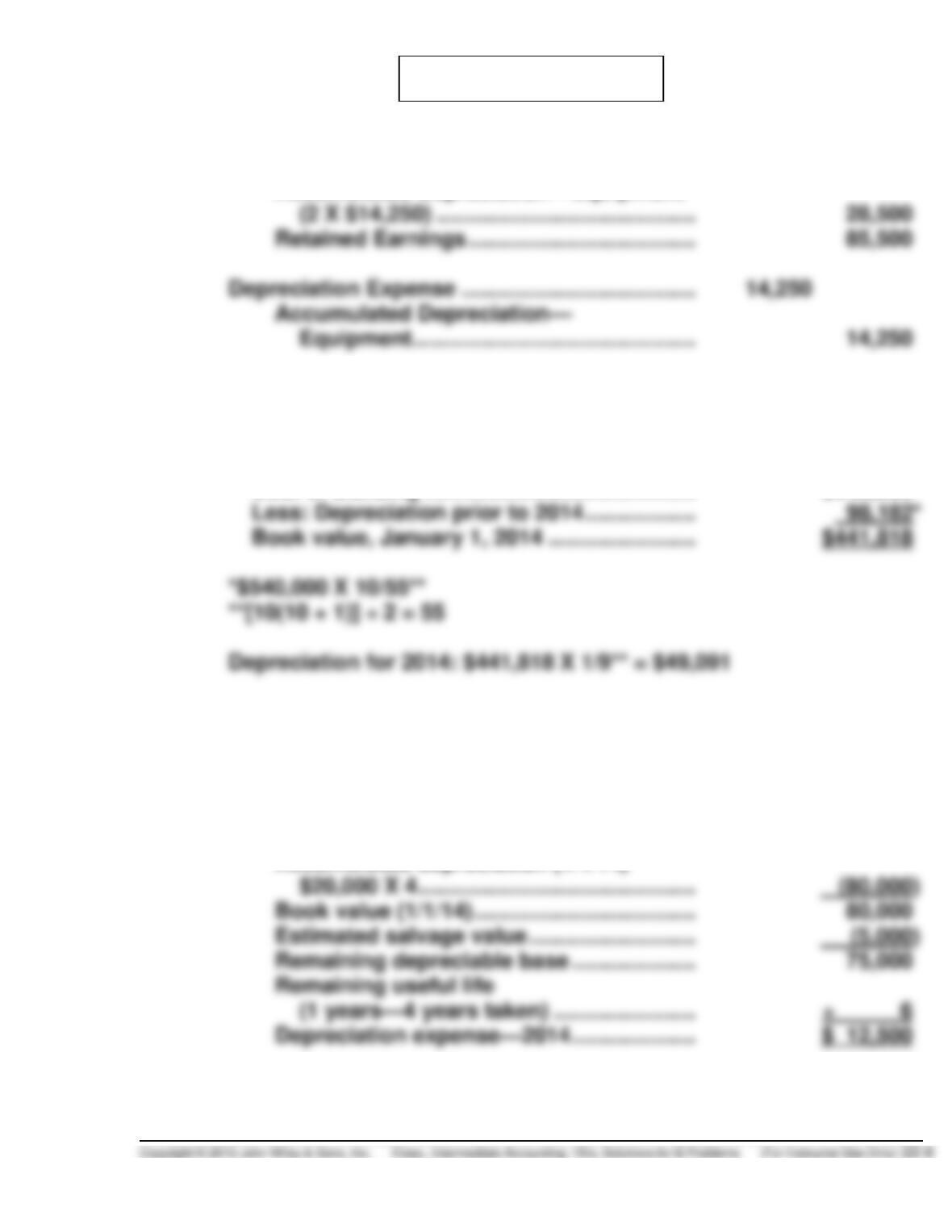

(a) 1. Equipment (Asset X) ………………………………….. 114,000

Accumulated Depreciation—Equipment

2. Depreciation Expense ……………………………….. 49,091

Accumulated Depreciation—Buildings …. 49,091

Computations:

Cost of Building …………………………………….. $540,000

3. Depreciation Expense ……………………………….. 12,500

Accumulated Depreciation—

Equipment ………………………………………. 12,500

Computations:

Original cost ………………………………………. $160,000

Accumulated depreciation (1/1/14)

PROBLEM 22-6B (Continued)

(b) TANNERY INC.

Comparative Retained Earnings Statements

For the Years Ended

2014

2013

Retained earnings, January 1, as previously

reported

$325,000

Add: Error in recording equipment (Asset X)

99,750*

Retained earnings, December 31

*Amount expensed incorrectly in 2012 ……………….. $114,000

Depreciation to be taken to January 1, 2013

($14,250 X 1) …………………………………………………. (14,250)

Prior period adjustment for income …………………… $99,750

**Income before depreciation expense (2014) $316,000

Depreciation for 2014

PROBLEM 22-7B

(1)

Depreciation Expense …………………………..……………….. 2,500

Accumulated Depreciation—Equipment …………… 2,500

(2)

(4)

Accumulated Depreciation—Equipment …………………. 12,000

Equipment ……………………………………………………… 9,000

Gain on Sale of Plant Assets …………………………... 3,000

(5)

(7)

Salaries and Wages Payable ($4,600 – $1,200) ………… 3,400

Salaries and Wages Expense ………………………….. 3,400

(8)

Depreciation Expense …………………………..……………….. 15,000