EXERCISE 7-3 (10–15 minutes)

Current assets

Accounts receivable

Customers

bank loan)

due after December 31, 2014*

Other** ($2,640 + $1,500)

Accounts (of which accounts in

the amount of $40,000 have

Investments

Advance to subsidiary company

81,000

EXERCISE 7-4 (10–15 minutes)

Computation of cost of goods sold:

Merchandise purchased

Less: Ending inventory

EXERCISE 7-4 (Continued)

Selling price = 1.4 (Cost of good sold)

= 1.4 ($230,000)

= $322,000

Sales on account

$322,000

Less: Collections

Uncollected balance

Balance per ledger

82,000

EXERCISE 7-5 (15–20 minutes)

(a)

(1)

June 3

Accounts Receivable—Chester …………………………..

3,000

Sales Revenue ………………………………………………..

3,000

June 12

Cash ……………………………………………………….

2,940

Sales Discounts ($3,000 X 2%) …………………………..

Accounts Receivable—Chester ……………………….

3,000

(2)

June 3

Accounts Receivable—Chester …………………………..

2,940

Sales Revenue ($3,000 X 98%) …………………………

2,940

June 12

Cash ……………………………………………………….

2,940

Accounts Receivable—Chester ……………………….

2,940

EXERCISE 7-5 (Continued)

(b)

July 29

Cash ……………………………………………………….

3,000

Accounts Receivable—Chester ……………………….

2,940

Sales Discounts Forfeited …………………………..

EXERCISE 7-6 (5–10 minutes)

July 1

Accounts Receivable ………………………………………………

20,000

Sales Revenue ……………………………………………….

20,000

July 10

Cash ……………………………………………………….

Sales Discounts ………………………………………………………

Accounts Receivable …………………………..

20,000

July 17

Accounts Receivable ………………………………………………

Sales Revenue ……………………………………………….

July 30

Cash ……………………………………………………….

Accounts Receivable …………………………..

EXERCISE 7-7 (10–15 minutes)

(a)

Bad Debt Expense …………………………………………………..

8,500

Allowance for Doubtful Accounts …………………….

8,500*

*.01 X ($900,000 – $50,000) = $8,500

(b)

Bad Debt Expense …………………………………………………..

3,000

Allowance for Doubtful Accounts …………………….

3,000*

EXERCISE 7-8 (15–20 minutes)

(a)

Allowance for Doubtful Accounts …………………………..

6,000

Accounts Receivable …………………………..

6,000

(b)

Accounts Receivable

Less: Allowance for Doubtful Accounts

Net realizable value

(c)

Accounts Receivable

Less: Allowance for Doubtful Accounts

Net realizable value

EXERCISE 7-9 (8–10 minutes)

(a)

Bad Debt Expense …………………………………………………..

5,350

Allowance for Doubtful Accounts …………………….

($90,000 X 4%) + $1,750 = $5,350

(b)

Bad Debt Expense …………………………………………………..

6,800

Allowance for Doubtful Accounts …………………….

$680,000 X 1% = $6,800

EXERCISE 7-10 (10–12 minutes)

(a) The direct write-off approach is not theoretically justifiable even

though required for income tax purposes. The direct write-off method

EXERCISE 7-11 (8–10 minutes)

Balance 1/1 ($700 – $155)

Over one year

4/12 (#2412) ($1,710 – $1,000 – $300*)

Eight months and 19 days

11/18 (#5681) ($2,000 – $1,250)

One month and 13 days

Inasmuch as later invoices have been paid in full, all three of these

amounts should be investigated in order to determine why Hopkins Co. has

not paid them. The amounts in the beginning balance and #2412 should be

of particular concern.

EXERCISE 7-12 (15–20 minutes)

7/1

Accounts Receivable—Harding Co. ………………………….

7,840

Sales Revenue ($8,000 X 98%) …………………………

7,840

7/5

Cash [$9,000 X (1 – .09)]…………………………..

8,190

Loss on Sale of Receivables …………………………..

Accounts Receivable ($9,000 X 98%) ………………..

8,820

Sales Discounts Forfeited …………………………..

EXERCISE 7-12 (Continued)

7/9

Accounts Receivable ……………………………………………….

180

Sales Discounts Forfeited

($9,000 X 2%) ……………………………………………….

180

Cash ……………………………………………………….

5,640

Interest Expense ($6,000 X 6%) …………………………..

360

Notes Payable …………………………………………………

7/11

Account Receivable—Harding Co. …………………………..

160

Sales Discounts Forfeited …………………………..

($8,000 X 2%)

This entry may be made at the next time financial statements are

prepared. Also, it may occur on 12/29 when Harding Company’s

receivable is adjusted.

12/29

Allowance for Doubtful Accounts …………………………..

7,200

Accounts Receivable—Harding Co. …………………….

[$7,840 + $160 = $8,000;

EXERCISE 7-13 (10–15 minutes)

(a)

Cash ………………………………………………………………………

192,000

Interest Expense …………………………………………………….

Notes Payable ………………………………………………..

*2% X $400,000 = $8,000

Accounts Receivable …………………………..

EXERCISE 7-13 (Continued)

(c)

Notes Payable …………………………..…………………………..

200,000

Interest Expense …………………………………………………….

Cash ……………………………………………………….

*10% X $200,000 X 3/12 = $5,000

EXERCISE 7-14 (15–18 minutes)

1.

Cash ……………………………………………………….

22,500

Loss on Sale of Receivables …………………………..

2,500

($25,000 X 10%)

Accounts Receivable …………………………..

25,000

2.

Cash ……………………………………………………….

50,600

Interest Expense ($55,000 X 8%) …………………………..

4,400

Notes Payable …………………………………………………

55,000

3.

Bad Debt Expense …………………………………………………..

6,220

Allowance for Doubtful Accounts …………………….

[($82,000 X 5%) + $2,120]

4.

Bad Debt Expense …………………………………………………..

6,450

Allowance for Doubtful Accounts …………………….

($430,000 X 1.5%)

EXERCISE 7-15 (10–15 minutes)

Computation of net proceeds:

Cash received

Less: Recourse liability

EXERCISE 7-15 (Continued)

Computation of gain or loss:

Carrying value

$200,000

Net proceeds

The following journal entry would be made:

Cash ………………………………………………………………

$160,000

Loss on Sale of Receivables …………………………..

Recourse Liability ……………………………………

Accounts Receivable …………………………..

EXERCISE 7-16 (15–20 minutes)

(a)

To be recorded as a sale, all of the following conditions would be met:

(1)

The transferred asset has been isolated from the transferor (put

beyond reach of the transferor and its creditors).

(2)

The transferees have obtained the right to pledge or to exchange

(b)

Computation of net proceeds:

Cash received ($175,000 X 94%)

$164,500

Due from factor ($175,000 X 4%)

7,000

$171,500

Less: Recourse liability

2,000

EXERCISE 7-16 (Continued)

Computation of gain or loss:

Carrying value

Net proceeds

Loss on sale of receivables

The following journal entry would be made:

Cash ……………………………………………………….

164,500

Due from Factor ………………………………………………

Loss on Sale of Receivables …………………………..

Recourse Liability …………………………..

Accounts Receivable …………………………..

EXERCISE 7-17 (10–15 minutes)

(a)

July 1

Cash ……………………………………………………….

283,500

Due from Factor ………………………………………………………

12,000*

Loss on Sale of Receivables …………………………..

**(1 1/2% X $300,000) = $4,500

(b)

July 1

Accounts Receivable …………………………..

300,000

Due to JFK Corp. …………………………..

Interest Revenue …………………………..

Cash ……………………………………………………….

EXERCISE 7-18 (10–15 minutes)

1.

7/1/14

Notes Receivable …………………………………………………….

1,101,460.00

Discount on Notes Receivable …………………………

401,460.00

Land ……………………………………………………….

590,000.00

Gain on Disposal of Land …………………………..

110,000.00

Computation of the discount

Face value of note

Present value of 1 for 4 periods at 12%

Present value of note

Face value of note

2.

7/1/14

Notes Receivable …………………………………………………….

400,000.00

Discount on Notes Receivable …………………………

178,836.32

Service Revenue …………………………..

221,163.68

Computation of the present value of the note:

Maturity value

$400,000.00

Present value of $400,000 due

in 8 years at 12%—$400,000 X .40388

Present value of $12,000

payable annually for 8 years

at 12% annually—$12,000 X 4.96764

Present value of the note

EXERCISE 7-19 (20–25 minutes)

(a)

Notes Receivable ……………………………………………………

200,000

Discount on Notes Receivable …………………………

34,710

Service Revenue ……………………………………………

$200,000 X .82645 = $165,290

(b)

Discount on Notes Receivable …………………………..

16,529

Interest Revenue ……………………………………………

16,529*

*$165,290 X 10% = $16,529

(c)

Discount on Notes Receivable …………………………..

18,181*

Interest Revenue …………………………………………….

18,181

*$34,710 – $16,529 (or [$165,290 + $16,529] X 10%)

Cash ………………………………………………………………………

200,000

Notes Receivable …………………………………………..

EXERCISE 7-20 (10–15 minutes)

(a)

Accounts Receivable ………………………………………………

100,000

Sales Revenue ………………………………………………..

Cash ………………………………………………………………………

Accounts Receivable …………………………..

EXERCISE 7-20 (Continued)

(b) Accounts Receivable Turnover =

Net Sales

Average Trade Receivables (net)

Average Trade Receivables (net)

($15,000 + $45,000*)/2

(c) Jones Company’s turnover ratio has declined significantly. That is, it

is turning receivables 3.33 times a year and collections on receivables

EXERCISE 7-21

(a)

Cash [$25,000 X (1 – .09)] …………………………………………

22,750

Due from Factor ………………………………………………………

1,250

Loss on Sale of Accounts Receivable ………………………

2,200

Accounts Receivable …………………………..

Recourse Liability …………………………………………..

Computation of cash received

Accounts receivable ……………………………………….

Less: Due from factor (5% X $25,000) ……………….

Finance charge (4% X $25,000) ………………

1,000

Cash received …………………………………………..

Cash received …………………………………………………

Due from factor ………………………………………………

$24,000

Less: Recourse liability …………………………..

EXERCISE 7-21 (Continued)

Computation of loss

Less: Net proceeds …………………………………………

Loss on sale of receivables ……………………….

(b) Accounts Receivable Turnover =

Net Sales

Average Trade Receivables (net)

Net Sales

With the factoring transaction, Jones Company’s turnover ratio still declines

but by less than in the earlier exercise. While Jones’ collections have

*EXERCISE 7-22 (5–10 minutes)

1.

April 1

Petty Cash ……………………………………………………….

200

Cash ……………………………………………………….

200

2.

April 10

Freight-In (or Invertory) …………………………..

60

Supplies Expense …………………………..

25

Postage Expense …………………………………………………….

33

Accounts Receivable—Employees …………………………..

17

Miscellaneous Expense …………………………..

36

Cash Over and Short …………………………..

Cash ($200 – $27) …………………………..

173

3.

April 20

Petty Cash ……………………………………………………….

100

Cash ……………………………………………………….

100

*EXERCISE 7-23 (10–15 minutes)

Accounts Receivable—Employees …………………………..

74.00

($40.00 + $34.00)

Maintenance and Repairs Expense …………………………..

14.35

Postage Expense ($20.00 – $2.90) …………………………..

17.10

Supplies Expense ……………………………………………………

Cash Over and Short ……………………………………………….

Cash ($300.00 – $15.20) ……………………………………

*EXERCISE 7-24 (15–20 minutes)

(a) Angela Lansbury Company

Bank Reconciliation

July 31

Balance per bank statement, July 31

$8,650

Add: Deposits in transit

2,350a

Deduct: Outstanding checks

(1,100)b

Correct cash balance, July 31

$9,900

Add: Collection of note

Less: Bank service charge

NSF check

aComputation of deposits in transit

Deposits per books

$5,810

Deposits per bank in July

$5,000

Less deposits in transit (June)

July

(3,460)

Deposits in transit, July 31

bComputation of outstanding checks

Checks written per books

$3,100

Checks cleared by bank in July

$4,000

(June)*

July

(2,000)

Outstanding checks, July 31

*EXERCISE 7-24 (Continued)

(b)

Cash ………………………………………………………………………

650

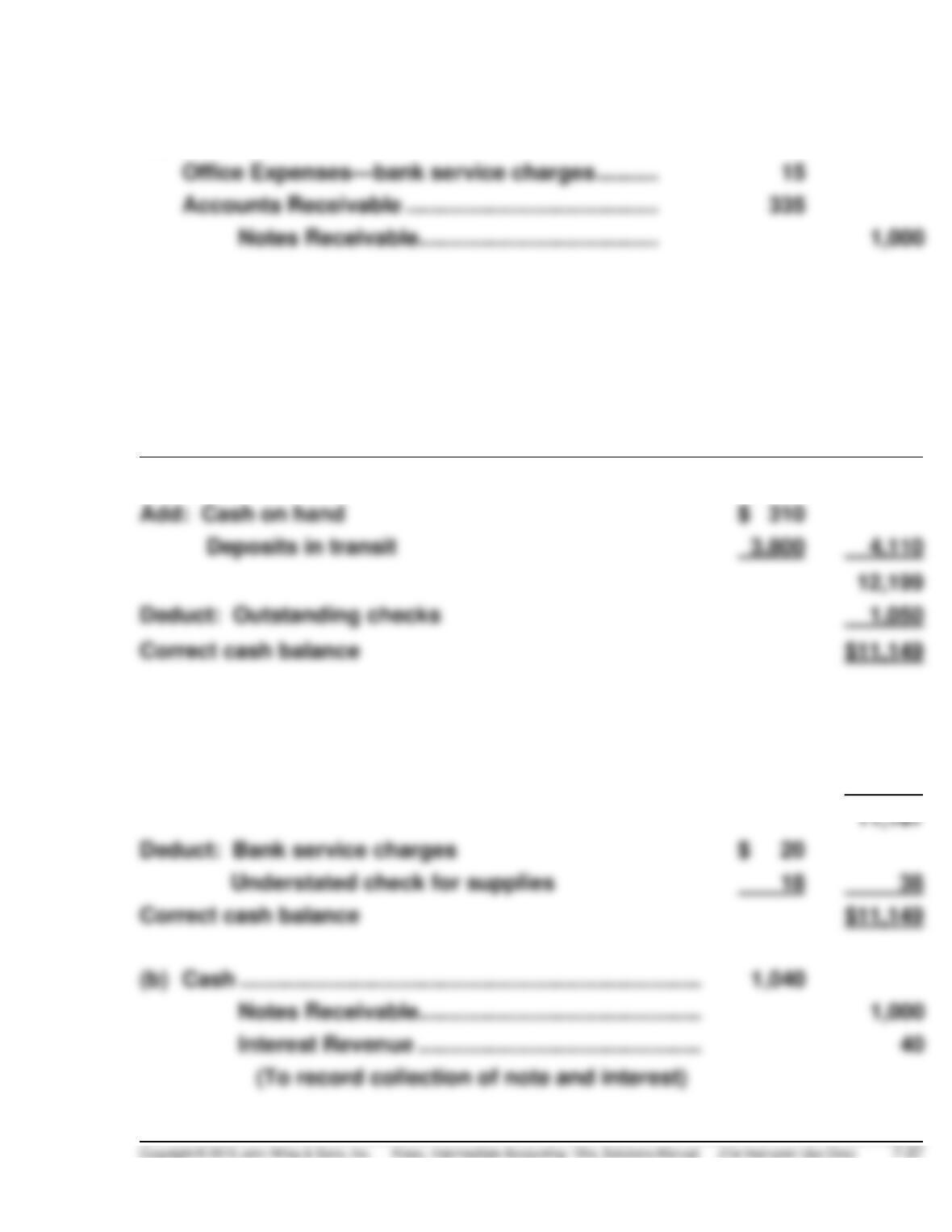

Office Expenses—bank service charges …………………..

Accounts Receivable ………………………………………………

335

Notes Receivable…………………………………………….

*EXERCISE 7-25 (15–20 minutes)

(a) Logan Bruno Company

Bank Reconciliation, August 31, 2014

County National Bank

Balance per bank statement, August 31, 2014

$ 8,089

Add: Cash on hand

Balance per books, August 31, 2014

($10,050 + $35,000 – $34,903)

$10,147

Add: Note ($1,000) and interest ($40) collected

1,040

Deduct: Bank service charges

Understated check for supplies

38

(b)

Cash ………………………………………………………………………

Notes Receivable…………………………………………….

Interest Revenue …………………………………………….

(To record collection of note and interest)

*EXERCISE 7-25 (Continued)

Office Expense—bank service charges …………………….

20

Cash ………………………………………………………………

(To record August bank charges)

Supplies Expense …………………………..……………………….

18

Cash ………………………………………………………………

supplies)

*EXERCISE 7-26 (15-25 minutes)

(a) Journal entry to record issuance of loan by Paris Bank:

December 31, 2014

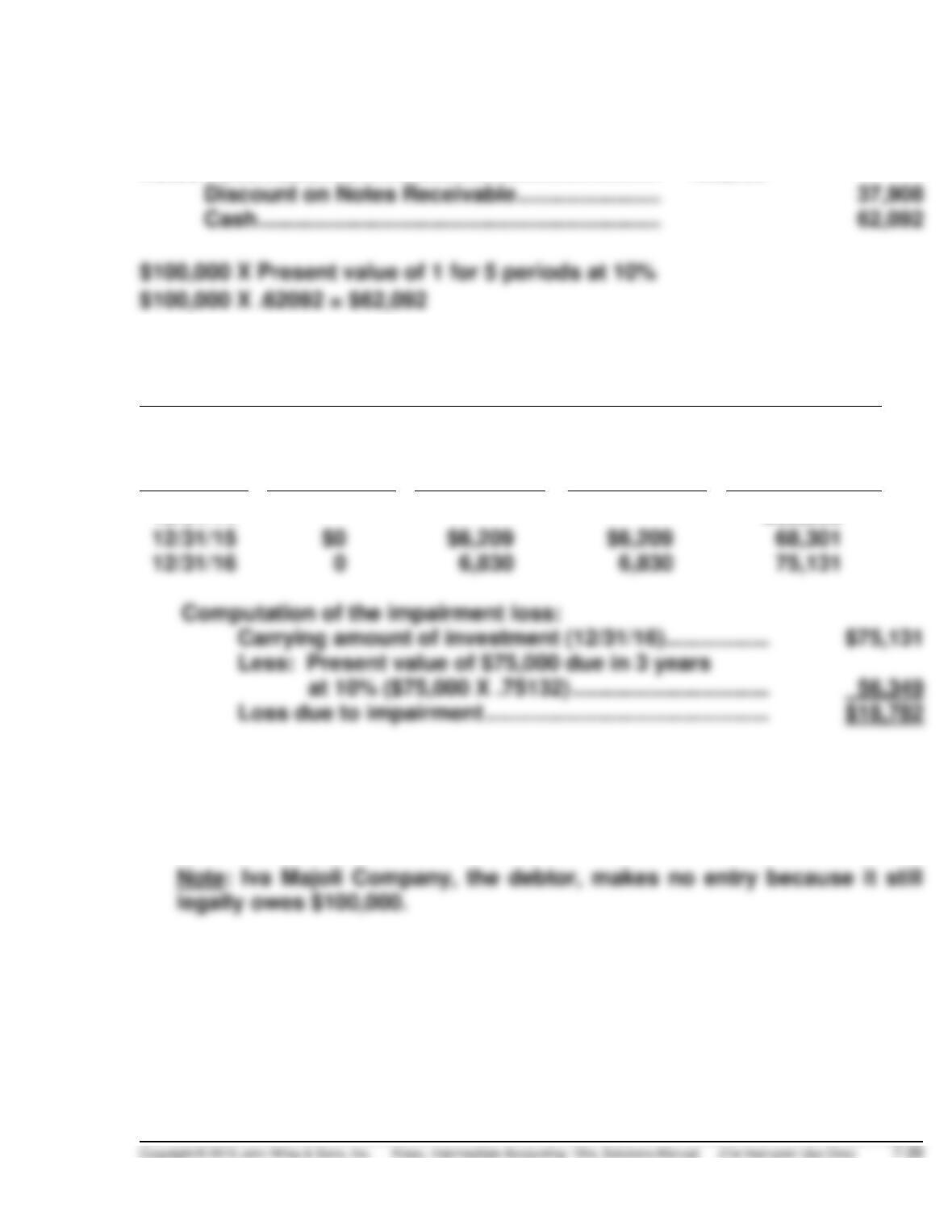

Notes Receivable………………………………………………………

100,000

Discount on Notes Receivable ………………………….

(b) Note Amortization Schedule

(Before Impairment)

Date

Cash

Received

(0%)

Interest

Revenue

(10%)

Increase in

Carrying

Amount

Carrying

Amount of

Note

12/31/14

$62,092

12/31/15

Computation of the impairment loss:

Carrying amount of investment (12/31/16)……………..

Loss due to impairment ……………………………………….

The entry to record the loss by Paris Bank is as follows:

Bad Debt Expense …………………………………………………..

18,782

Allowance for Doubtful Accounts …………………….

18,782

*EXERCISE 7-27 (15-25 minutes)

(a) Cash received by Conchita Martinez Company on December 31, 2014:

Present value of interest ($100,000 X 3.60478) ……….

Cash received ……………………………………………………..

$927,908

(b) Note Amortization Schedule

(Before Impairment)

Date

Cash

Received

(10%)

Interest

Revenue

(12%)

Increase in

Carrying

Amount

Carrying

Amount of

Note

12/31/14

$927,908

12/31/15

(c) Loss due to impairment:

Carrying amount of loan (12/31/16) …………………..

$951,968

Loss due to impairment …………………………………..

$284,717