PROBLEM 21-9B

Entries on September 1, 2014:

(1) Leased Equipment ……………………………………… 1,044,315

Lease Liability ……………………………………… 1,044,315

Explanation and computation: This is a capital lease because the lease

term exceeds 75% of the asset’s useful life.

(2) Maintenance and Repairs Expense …………….. 2,000

Lease Liability …………………………………………… 23,000

Cash …………………………………………………… 25,000

Explanation: This entry is to record the September 1, 2014, first

Entries on September 30, 2014:

(1) Interest Expense …………………………..…………… 10,213

Interest Payable ………………………………….. 10,213

Explanation and computation: Interest accrued on the unpaid balance

(2) Depreciation Expense ……………………………….. 17,405

Accumulated Depreciation—Capital

Leases ……………………………………………. 17,405

Explanation and computation: Depreciation is recorded for one month of

PROBLEM 21-10B

(a) The lease is a sales-type lease because: (1) the lease term exceeds

75% of the asset’s estimated economic life, (2) collectibility of payments

is reasonably assured and there are no further costs to be incurred,

and (3) George Company realized an element of profit aside from the

financing charge.

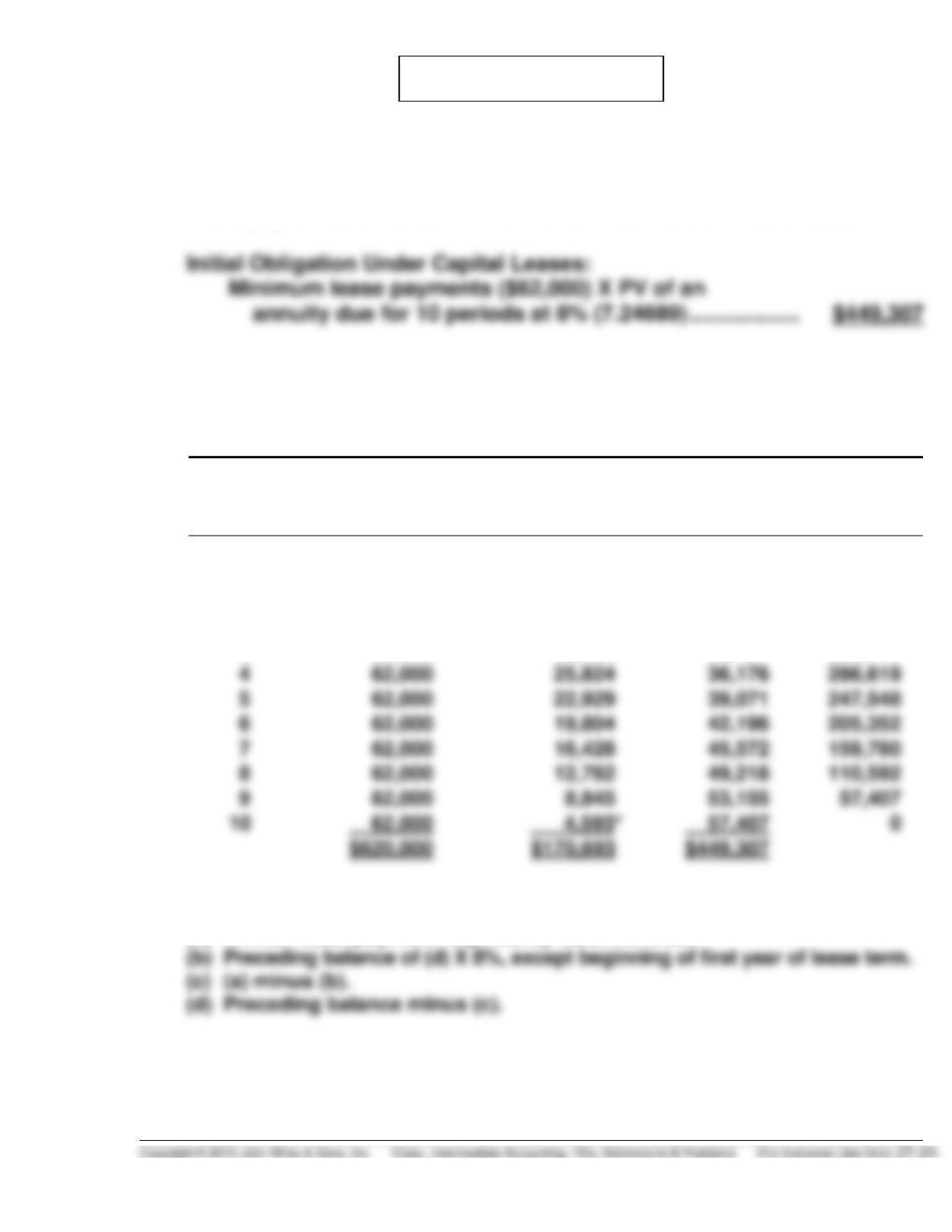

1. Present value of an annuity due of $1 for

10 periods discounted at 8% ……………………………….. 7.24689

2. Sales price is $449,307 (the present value of the 10 annual lease

3. Cost of sales is $361,472 (the $380,000 cost of the asset less the

present value of the unguaranteed residual value).

PROBLEM 21-10B (Continued)

(b) SKITOWN COMPANY (Lessor)

Lease Amortization Schedule

Annuity Due Basis, Unguaranteed Residual Value

Beginning

of Year

Annual Lease

Payment Plus

Residual Value

Interest (8%)

on Lease

Receivable

Lease

Receivable

Recovery

Lease

Receivable

(a)

(b)

(c)

(d)

Initial PV

—

—

—

$467,835

1

$ 62,000

—

$ 62,000

405,835

2

62,000

*$ 32,467

29,533

376,302

3

62,000

30,104

31,896

344,406

4

309,958

5

62,000

24,797

37,203

272,755

6

21,820

40,180

232,575

7

189,181

8

62,000

15,134

46,866

142,315

9

62,000

11,385

50,615

*$192,165

*Rounding error is $1.

(a) Annual lease payment required by lease contract.

(b) Preceding balance of (d) X 8%, except beginning of first year of lease term.

(c) Beginning of the Year

Lease Receivable ……………………………………………. 467,835

Cost of Goods Sold ………………………………………… 361,472

Sales Revenue …………………………………………. 449,307

PROBLEM 21-10B (Continued)

Cash …………………………..……………………………………. 62,000

Lease Receivable ……………………………………….. 62,000

PROBLEM 21-11B

(a) The lease is a capital lease because: (1) the lease term exceeds 75% of

the asset’s economic life and (2) the present value of the minimum

lease payments exceeds 90% of the fair value of the leased asset.

(b) ALPINE SKI RESORTS (Lessee)

Lease Amortization Schedule

(Annuity due basis and URV)

Beginning

of Year

Annual Lease

Payment

Interest (8%)

on Lease

Liability

Reduction

of Lease

Liability

Lease

Liability

(a)

(b)

(c)

(d)

Initial PV

—

—

—

$449,307

1

$ 62,000

—

$ 62,000

387,307

2

62,000

$ 30,985

31,015

356,292

3

62,000

28,503

33,497

322,795

4

62,000

36,176

286,619

5

62,000

39,071

247,548

6

62,000

19,804

42,196

205,352

7

62,000

45,572

159,780

8

62,000

49,218

110,592

9

62,000

53,155

*Rounding error is $1.

(a) Annual lease payment required by lease contract.

PROBLEM 21-11B (Continued)

(c) Lessee’s journal entries:

Beginning of the Year

Leased Equipment …………………………………………. 449,307

End of the Year

Interest Expense …………………………..……………….. 30,985

Interest Payable ………………………………………. 30,985

(To record accrual of annual interest on

lease obligation)

PROBLEM 21-12B

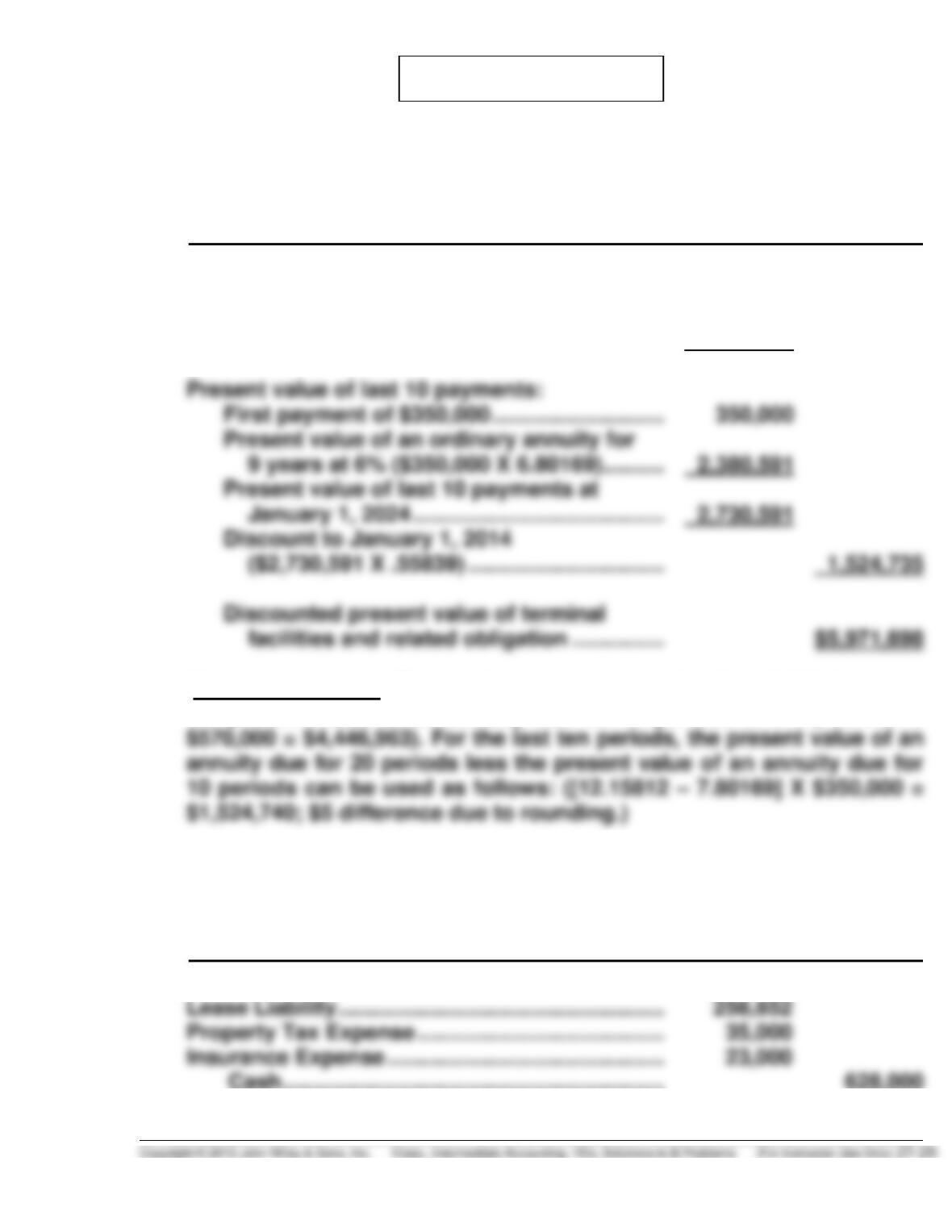

(a) DUDE TRANSPORTATION COMPANY

Schedule to Compute the Discounted Present Value

of Terminal Facilities and the Related Obligation

January 1, 2014

Present value of first 10 payments:

Immediate payment ……………………………….. $ 570,000

Present value of an ordinary annuity for

9 years at 6% ($570,000 X 6.80169) ………. 3,876,963 $4,446,963

(Note to instructor: The student can compute the $4,446,963 by using

the present value of an annuity due for 10 periods at 6% (7.80169 X

(b) DUDE TRANSPORTATION COMPANY

Journal Entries

2016

(1) (1/1/16)

Interest Payable …………………………..……………… 311,148

PROBLEM 21-12B (Continued)

Partial Amortization Schedule

(Annuity Due Basis)

Date

Lease

Payment

Executory

Costs

Interest

(6%) on

Lease

Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/14

—

—

—

—

$6,000,000

1/1/14

$628,000

$58,000

$ 0

$570,000

5,430,000

1/1/15

1/1/17

4,652,565

(2) (12/31/16)

Depreciation Expense ……………………………………. 200,000

Accumulated Depreciation—Capital

Leases …………………………………………………. 200,000

(3) (12/31/16)

Interest Expense …………………………..……………….. 295,617

Interest Payable ………………………………………. 295,617

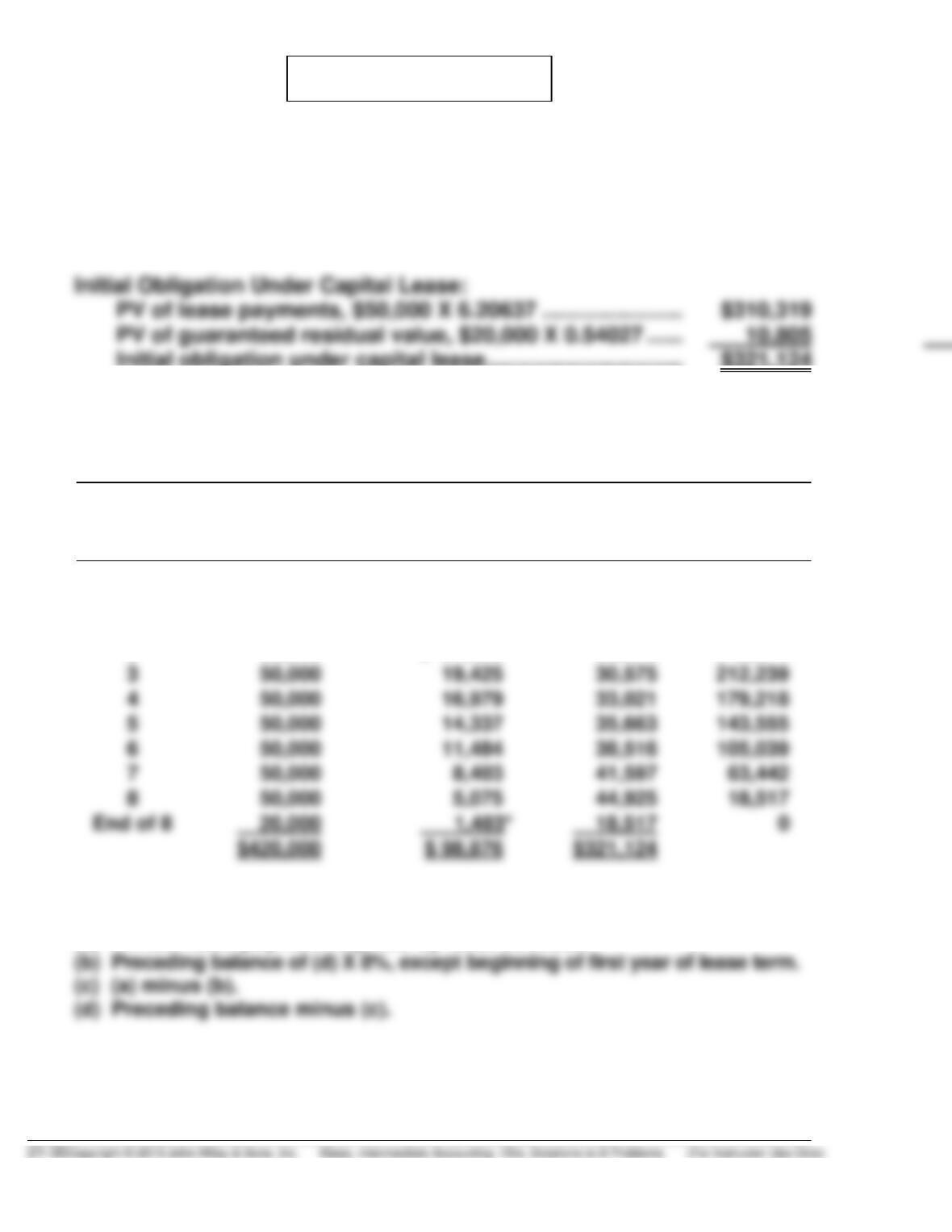

PROBLEM 21-13B

(a) The noncancelable lease is a sales-type lease because: (1) the lease

term is for 80% (8 ÷ 10) of the economic life of the leased asset,

1. Lease Receivable:

Present value of annual payments of $50,000

2. Sales price is the same as the present value of

minimum lease payments ……………………………………… $321,124

PROBLEM 21-13B (Continued)

(b) DANFORTH INC. (Lessor)

Lease Amortization Schedule

(Annuity due basis, guaranteed residual value)

Beginning

of Year

Annual Lease

Payment Plus

Residual Value

Interest (8%)

on Lease

Receivable

Recovery

of Lease

Receivable

Lease

Receivable

(a)

(b)

(c)

(d)

Initial PV

—

—

—

$321,124

1

$ 50,000

—

$ 50,000

271,124

2

50,000

$ 21,690

28,310

242,814

4

5

50,000

35,663

143,555

6

7

8

50,000

44,925

*Rounding error is $2.

(a) Annual lease payment required by lease contract.

(c) Lessor’s journal entries:

Beginning of the Year

Lease Receivable …………………………………………… 321,124

PROBLEM 21-13B (Continued)

Cash …………………………………………………………………. 50,000

Lease Receivable ………………………………………… 50,000

(To record receipt of the first lease

payment)

PROBLEM 21-14B

(a) The noncancelable lease is a capital lease because: (1) the lease term is

for 80% (8 ÷ 10) of the economic life of the leased asset and (2) the

present value of the minimum lease payments exceeds 90% of the fair

market value of the leased asset.

Initial obligation under capital lease ………………………….. $321,124

(b) CHAMBERLAIN AIRPORTS (Lessee)

Lease Amortization Schedule

(Annuity Due Basis, GRV)

Beginning

of Year

Annual Lease

Payment Plus

GRV

Interest (8%)

on Unpaid

Liability

Reduction

of Lease

Liability

Lease

Liability

(a)

(b)

(c)

(d)

Initial PV

—

—

—

$321,124

1

$ 50,000

—

$ 50,000

271,124

2

50,000

$ 21,690

28,310

242,814

3

212,239

4

179,218

5

50,000

35,663

143,555

6

105,039

7

8

50,000

44,925

$420,000

$321,124

*Rounding error is $2.

(a) Annual lease payment required by lease contract.

PROBLEM 21-14B (Continued)

(c) Lessee’s journal entries:

Beginning of the Year

Leased Equipment ………………………………………….. 321,124

Lease Liability ………………………………………….. 321,124

End of the Year

Interest Expense …………………………..………………… 21,690

Interest Payable ……………………………………….. 21,690

(To record accrual of annual interest on

lease obligation)

PROBLEM 21-15B

Memorandum Prepared by: (Your Initials)

Date:

ATLATNIV, INC.

December 31, 2014

Reclassification of Leased Truck

As a Capital Lease

While performing a routine inspection of the client’s garage, I found a used

life (6 years).

I advised the client to capitalize this lease at the present value of its minimum

lease payments: $21,532 (the present value of the monthly payments), plus

$1,552 (the present value of the guaranteed residual). The following journal

entry was suggested:

PROBLEM 21-15B (Continued)

Finally, this vehicle must be depreciated over its lease term. Using straight–

line, I computed annual depreciation of $4,117 (the capitalized amount,

PROBLEM 21-16B

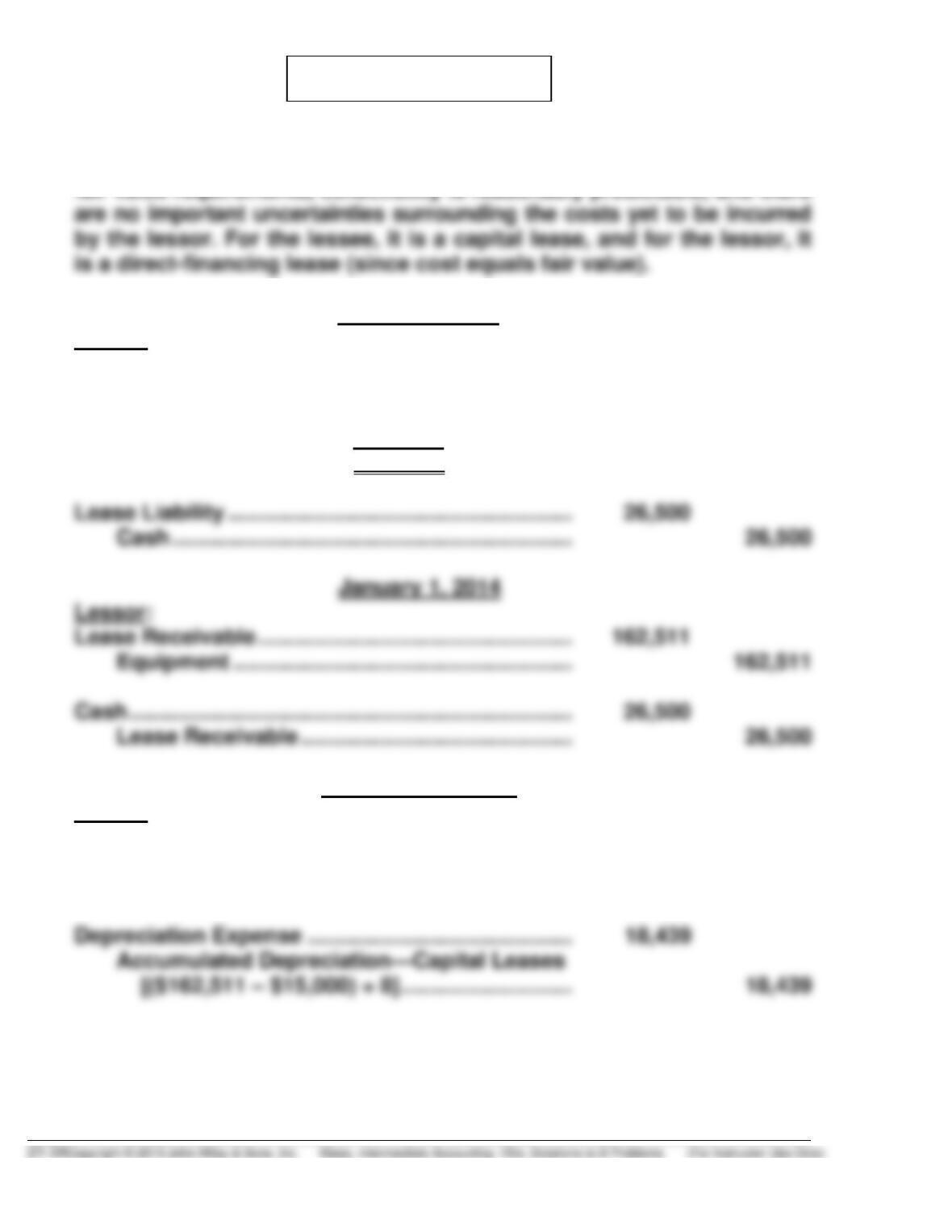

(a) The lease agreement satisfies both the 75% of useful life and 90% of

(b) January 1, 2014

Lessee:

Leased Equipment …………………………………………. 162,511

Lease Liability …………………………………………. 162,511

($26,500 X 5.86842 = $155,513)

($15,000 X 0.46651 = 6,998)

= $162,511)

December 31, 2014

Lessee:

Interest Expense …………………………..……………….. 13,601

Interest Payable

[($162,511 – $26,500) X 0.10] …………………. 13,601

PROBLEM 21-16B (Continued)

December 31, 2014

Lessor:

Interest Receivable ……………………………………………. 13,601

Interest Revenue …………………………………………. 13,601

(c) (1) and (2) are both $155,513, as the lessee has no obligation to pay the

residual value.