CHAPTER 23

Statement of Cash Flows

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Format, objectives

purpose, and source

of statement.

1, 2, 7,

8, 12

1, 2, 5, 6

2.

Classifying investing,

financing, and operating

activities.

3, 4, 5, 6,

16, 17, 19

1, 2, 3,

6, 7,

8, 12

1, 2, 10, 16

1, 3, 4, 5

3.

Direct vs. indirect

methods of preparing

operating activities.

9, 20

4, 5, 9,

10, 11

3, 4

5

Statement of cash flows—

direct method.

11, 13, 14

8

4, 5, 7, 9,

12, 13

3, 4, 6,

7, 8

5.

Statement of cash flows—

indirect method.

10, 13,

15, 16

8

3, 6, 8, 11,

14, 15, 16,

17, 18

1, 2, 5, 6,

7, 8, 9

2

6.

Preparing schedule

of noncash investing

and financing activities.

5, 7, 8, 9

5

Worksheet adjustments.

19, 20, 21

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

Concepts for

Analysis

1. Describe the purpose of

the statement

of cash flows.

1, 2

CA23-5

2. Identify the major

classifications

of cash flows.

3, 4

3

1, 2, 10, 16

CA23-5

3. Prepare a statement of

cash flows.

5, 6, 7

8

9, 11, 12, 13,

14, 15, 17,

1, 2, 3, 4,

5,

CA23-1, CA23-

2

4. Differentiate between net

income and net cash flow

from operating activities.

8, 9, 10, 11,

12

4, 5, 9, 10,

11

2, 4, 5, 6, 7,

8, 11, 16

1

CA23-3

5. Determine net cash flows

from investing and

financing activities.

13, 14

1, 2

16

CA23-4

for a statement of cash

flows.

7, 8, 9

flow from operating

activities.

8. Discuss special problems

in preparing

a statement of cash flows.

17, 18, 19

12

10, 18

1, 2, 4, 5,

6, 7, 8, 9

CA23-6

9. Explain the use of a

worksheet in preparing a

statement of cash flows.

21

13

19, 20, 21

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E23-1

Classification of transactions.

Simple

10–15

E23-2

Statement presentation of transactions—indirect method.

Moderate

20–30

E23-3

Preparation of operating activities section—indirect method,

periodic inventory.

Simple

15–25

E23-4

Preparation of operating activities section—direct method.

Simple

20–30

E23-5

Preparation of operating activities section—direct method.

Simple

20–30

E23-6

Preparation of operating activities section—indirect method.

Simple

15–20

E23-7

Computation of operating activities—direct method.

Simple

15–20

E23-8

Schedule of net cash flow from operating activities—

indirect method.

20–30

E23-9

SCF—direct method.

Moderate

20–30

E23-10

Classification of transactions.

Moderate

25–35

E23-11

SCF—indirect method.

Moderate

30–35

E23-12

SCF—direct method.

Moderate

20–30

E23-13

SCF—direct method.

Moderate

30–40

E23-14

SCF—indirect method.

Moderate

30–40

E23-15

SCF—indirect method.

Moderate

25–35

E23-16

Cash provided by operating, investing, and financing

activities.

30–40

E23-17

SCF—indirect method and balance sheet.

Moderate

30–40

E23-18

Partial SCF—indirect method.

Moderate

25–30

E23-19

Worksheet analysis of selected accounts.

Moderate

20–25

E23-20

Worksheet analysis of selected transactions.

Moderate

20–25

P23-1

SCF—indirect method.

Moderate

40–45

P23-2

SCF—indirect method.

Moderate

50–60

P23-3

SCF—direct method.

Complex

50–60

P23-4

SCF—direct method.

Moderate

45–60

P23-5

SCF—indirect method.

Complex

50–65

P23-6

activities, direct method.

40–50

P23-7

financial statements.

30–40

P23-8

SCF—direct and indirect methods.

Moderate

30–40

P23-9

Indirect SCF.

Moderate

30–40

CA23-1

Analysis of improper SCF.

Moderate

30–35

CA23-2

SCF theory and analysis of improper SCF.

Moderate

30–35

CA23-3

SCF theory and analysis of transactions.

Moderate

30–35

CA23-4

Moderate

20–30

CA23-5

Purpose and elements of SCF.

Complex

30–40

CA23-6

Cash flow reporting.

Moderate

20–30

CE23-1

Master Glossary

(a) Cash equivalents are short-term, highly liquid investments that have both of the following

characteristics:

1. Readily convertible to known amounts of cash

2. So near their maturity that they present insignificant risk of changes in value because of

changes in interest rates.

Generally, only investments with original maturities of three months or less qualify under that

(b) Financing activities include obtaining resources from owners and providing them with a return

on, and a return of, their investment; receiving restricted resources that by donor stipulation must

(c) Investing activities include making and collecting loans and acquiring and disposing of debt or

equity instruments and property, plant, and equipment and other productive assets, that is,

(d) Operating activities include all transactions and other events that are not defined as investing or

financing activities (see paragraphs 230–10–45-12 through 45-15). Operating activities generally

CE23-2

According to FASB ASC 230-10–45-14 (Statement of Cash Flow—Other Presentation Matters—Cash

Flows from Financing Activities):

All of the following are cash inflows from financing activities:

(a) Proceeds from issuing equity instruments.

(b) Proceeds from issuing bonds, mortgages, notes, and from other short- or long-term borrowing.

CE23-2 (Continued)

(c) Receipts from contributions and investment income that by donor stipulation are restricted for the

purposes of acquiring, constructing, or improving property, plant, equipment, or other long-lived

CE23-3

According to FASB ASC 230-10–45-11 (Statement of Cash Flows—Other Presentation Matters—Cash

CE23-4

According to FASB ASC 230-10–50-3 (Statement of Cash Flows—Disclosure—Noncash Investing and

Financing Activities):

Information about all investing and financing activities of an entity during a period that affect recognized

ANSWERS TO QUESTIONS

1. The main purpose of the statement of cash flows is to provide information about a company’s cash

2. Some uses of this statement are:

Assessing future cash flows: Income data when augmented with current cash flow data provide a

better basis for assessing future cash flows.

Assessing reasons for differences between income and net cash flow from operation:

3. Investing activities generally involve long-term assets and include (1) lending money and collecting

on those loans and (2) acquiring and disposing of investments and productive long-lived assets.

4. Examples of sources of cash in a statement of cash flows include cash from operating activities,

issuance of debt, issuance of capital stock, sale of investments, and the sale of property, plant,

5. Preparing the statement of cash flows involves three major steps:

(1) Determine the change in cash. This is simply the difference between the beginning and ending

cash balances.

6. Purchase of land—investing;

Payment of dividends—financing;

Cash sales—operating;

Purchase of treasury stock—financing.

7. Comparative balance sheets, a current income statement, and certain transaction data all provide

information necessary for preparation of the statement of cash flows. Comparative balance sheets

Questions Chapter 23 (Continued)

8. It is necessary to convert accrual-based net income to a cash basis because net income includes

items that do not provide or use cash. An example would be an increase in accounts receivable.

9. Net cash flow from operating activities under the direct method is the difference between cash

revenues and cash expenses. The direct method adjusts the revenues and expenses directly to

10. Net cash flow from operating activities is $3,820,000. Using the indirect method, the solution is:

Net income …………………………………………………………………….. $3,500,000

11. Accrual basis sales ……………………………………………………. $100,000

Less: Increase in accounts receivable …………………………. 30,000

70,000

Less: Write-off of accounts receivable …………………………. 2,000

Cash sales ……………………………………………………………….. $ 68,000

12. A number of factors could have caused an increase in cash despite the net loss. These are: (1) high

13. Declared dividends ……………………………………………………. $260,000

Add: Dividends payable (beginning of year) ………………….. 85,000

345,000

Deduct: Dividends payable (end of year) ……………………… 90,000

Cash paid in dividends during the year …………………………. $255,000

14. To determine cash payments to suppliers, it is first necessary to find purchases for the year. To

find purchases, cost of goods sold is adjusted for the change in inventory (increased when

15. Cash flows from operating activities

Net income ……………………………………………………………… $320,000

Adjustments to reconcile net income to net cash

Questions Chapter 23 (Continued)

16. (a) Cash flows from operating activities

Net income …………………………………………………………………… XXXX

Adjustments to reconcile net income to net

cash provided by operating activities:

Loss on sale of plant assets

17. (a) Operating activity. (g) Operating activity.

(b) Financing activity. (h) Financing activity.

18. Examples of noncash transactions are: (1) issuance of stock for noncash assets, (2) issuance of stock

to liquidate debt, (3) issuance of bonds or notes for noncash assets, and (4) noncash exchanges of

property, plant, and equipment.

19. Cash flows from operating activities

Net income………………………………………………………………………….. XXXX

20. Arguments for the indirect or reconciliation method are:

(a) By providing a reconciliation between net income and net cash provided by operating

Questions Chapter 23 (Continued)

(c) There is some question as to whether the direct method is cost/benefit-justified as this

method would probably lead to additional preparation cost because the financial records are

not maintained on a cash basis.

21. A worksheet is desirable because it allows the orderly accumulation and classification of data that

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 23-1

Cash flows from investing activities

Sale of land ……………………………………………………………

Purchase of equipment …………………………………………..

Purchase of available-for-sale securities …………………

BRIEF EXERCISE 23-2

Cash flows from financing activities

Issuance of common stock …………………………………….

Issuance of bonds payable ……………………………………..

Payment of dividends …………………………………………….

Purchase of treasury stock …………………………………….

BRIEF EXERCISE 23-3

(a)

P-I

(g)

P-F

(m)

N

(b)

A

(h)

D

(n)

D

(c)

R-F

(i)

P-I

(o)

R-F

(d)

A

(j)

A

(p)

P-F

(e)

R-I

(k)

D

(q)

R-I, A

R-I, D

(l)

R-F

(r)

P-F

BRIEF EXERCISE 23-4

Cash flows from operating activities

Cash received from customers

($200,000 – $12,000) …………………………………..

Cash payments:

To suppliers

($120,000 + $11,000 – $13,000) …………….

For operating expenses

BRIEF EXERCISE 23-5

Cash flows from operating activities

Net income …………………………………………………..

$30,000

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense …………………………...

Increase in accounts receivable ……………..

Increase in inventory …………………………….

BRIEF EXERCISE 23-6

Sales revenue ………………………………………………………

$420,000

Cash receipts from customers ………………………………

$438,000

BRIEF EXERCISE 23-7

Cost of goods sold ……………………………………………….

$500,000

Add: Increase in inventory ($113,000 – $95,000) …….

18,000

Purchases ……………………………………………………………

518,000

Cash payments to suppliers ………………………………….

$510,000

BRIEF EXERCISE 23-8

Net cash provided by operating activities ……………………

$531,000

Net cash used by investing activities ………………………….

(963,000)

Net cash provided by financing activities ……………………

Net increase in cash …………………………………………………..

Cash, 1/1/14 ………………………………………………………………

BRIEF EXERCISE 23-9

(a)

Cash flows from operating activities

Cash received from customers …………………………..

$90,000

Cash payments for expenses

($60,000 – $1,840) …………………………………………..

58,160

Net cash provided by operating

(b)

Cash flows from operating activities

Net income ……………………………………………………….

Net cash provided by operating

activities ………………………………………………..

BRIEF EXERCISE 23-10

Cash flows from operating activities

Net income ……………………………………………………….

$50,000

Adjustments to reconcile net income to net cash

provided by operating activities:

Depreciation expense ………………………………..

Increase in accounts payable ……………………..

Increase in accounts receivable ………………….

Increase in inventory ………………………………….

BRIEF EXERCISE 23-11

Cash flows from operating activities:

Net loss ……………………………………………………………

Adjustments to reconcile net income (loss)

to net cash provided by operating activities:

Depreciation expense ………………………………..

BRIEF EXERCISE 23-12

(a)

Land ……………………………………………………….……………..

40,000

Common Stock ……………………………………………….

10,000

Paid-in Capital in Excess of Par—

Common Stock …………………………………………..

30,000

(b)

No effect

(c)

Noncash investing and financing activities:

Purchase of land through issuance of

common stock …………………………..…………………

BRIEF EXERCISE 23-13

(a)

Operating—Net Income …………………………………………..

317,000

Retained Earnings …………………………………………..

317,000

(b)

Retained Earnings …………………………………………………..

120,000

Financing—Cash Dividends …………………………..

120,000

(c)

Equipment ……………………………………………………….

114,000

Investing—Purchase of Equipment ………………….

(d)

Investing—Sale of Equipment …………………………..

Equipment ……………………………………………………..

40,000

Operating—Gain on Sale of Equipment ……………

SOLUTIONS TO EXERCISES

EXERCISE 23-1 (10–15 minutes)

(a) Investing activity.

(b) Financing activity.

(c) Investing activity.

EXERCISE 23-2 (20–30 minutes)

(a)

Plant assets (cost)

$20,000)

Accumulated depreciation ([$20,000 10] X 6)

12,000)

Book value at date of sale

8,000)

Sale proceeds

(5,300)

Loss on sale

$ 2,700)

(b)

Shown in the financing activities section of a statement of cash

flows as follows:

Sale of common stock

$430,000

EXERCISE 23-2 (Continued)

(c) The writeoff of the uncollectible accounts receivable of $27,000 is not

reported on the statement of cash flows. The writeoff reduces the

(d) The net loss of $50,000 should be reported in the operating activities

section of the statement of cash flows. Depreciation of $22,000 is

reported in the operating activities section of the statement of cash

flows. The gain on sale of land also appears in the operating activities

section of the statement of cash flows. The proceeds from the sale of

land of $39,000 are reported in the investing activities section of the

statement of cash flows. These four items might be reported as follows:

Cash flows from operating activities

Net loss

$(50,000)

Adjustments to reconcile net income

to net cash used in operating activities*:

Gain on sale of land

Cash flows from investing activities

Sale of land

(e) The purchase of the U.S. Treasury bill is not reported in the statement

of cash flows. This instrument is considered a cash equivalent and

therefore cash and cash equivalents have not changed as a result of

this transaction.

EXERCISE 23-2 (Continued)

(g) The exchange of common stock for an investment in Tabasco is

reported as a “noncash investing and financing activity.” It is shown

EXERCISE 23-3 (15–25 minutes)

VINCE GILL COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income

$1,050,000

Adjustments to reconcile net income

to net cash provided by operating activities:

Depreciation expense

Decrease in accounts receivable

Decrease in inventory

Increase in prepaid expenses

Decrease in accounts payable

Decrease in accrued expenses payable

EXERCISE 23-4 (20–30 minutes)

VINCE GILL COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers

$7,260,000

(a)

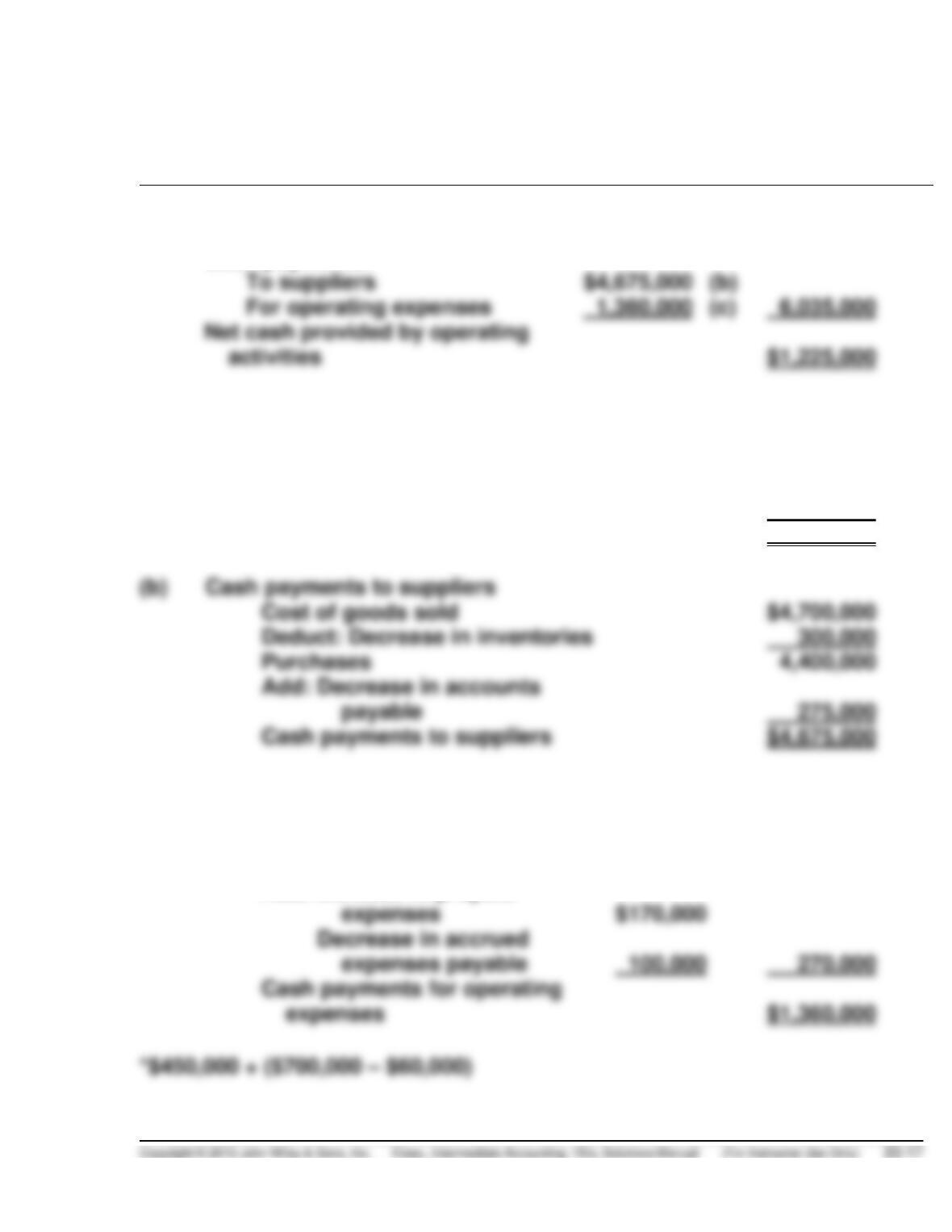

Cash payments:

To suppliers

$4,675,000

(b)

For operating expenses

(c)

Net cash provided by operating

activities

$1,225,000

Computations:

(a)

Cash receipts from customers

Sales revenue

$6,900,000

Add: Decrease in accounts

Add: receivable

360,000

Cash receipts from customers

$7,260,000

(b)

Cash payments to suppliers

Cost of goods sold

$4,700,000

Deduct: Decrease in inventories

300,000

Purchases

Add: Decrease in accounts

Add: payable

275,000

Cash payments to suppliers

$4,675,000

(c)

Cash payments for operating

expenses

Operating expenses, exclusive

of depreciation

$1,090,000*

Add: Increase in prepaid

Add: Decrease in accrued

Add: expenses payable

270,000

Cash payments for operating

expenses

$1,360,000

EXERCISE 23-5 (20–30 minutes)

KRAUSS COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Cash receipts from customers

$857,000

(a)

Cash payments:

For operating expenses

$614,000

(b)

For income taxes

44,500

(c)

658,500

Net cash provided by operating

activities

$198,500

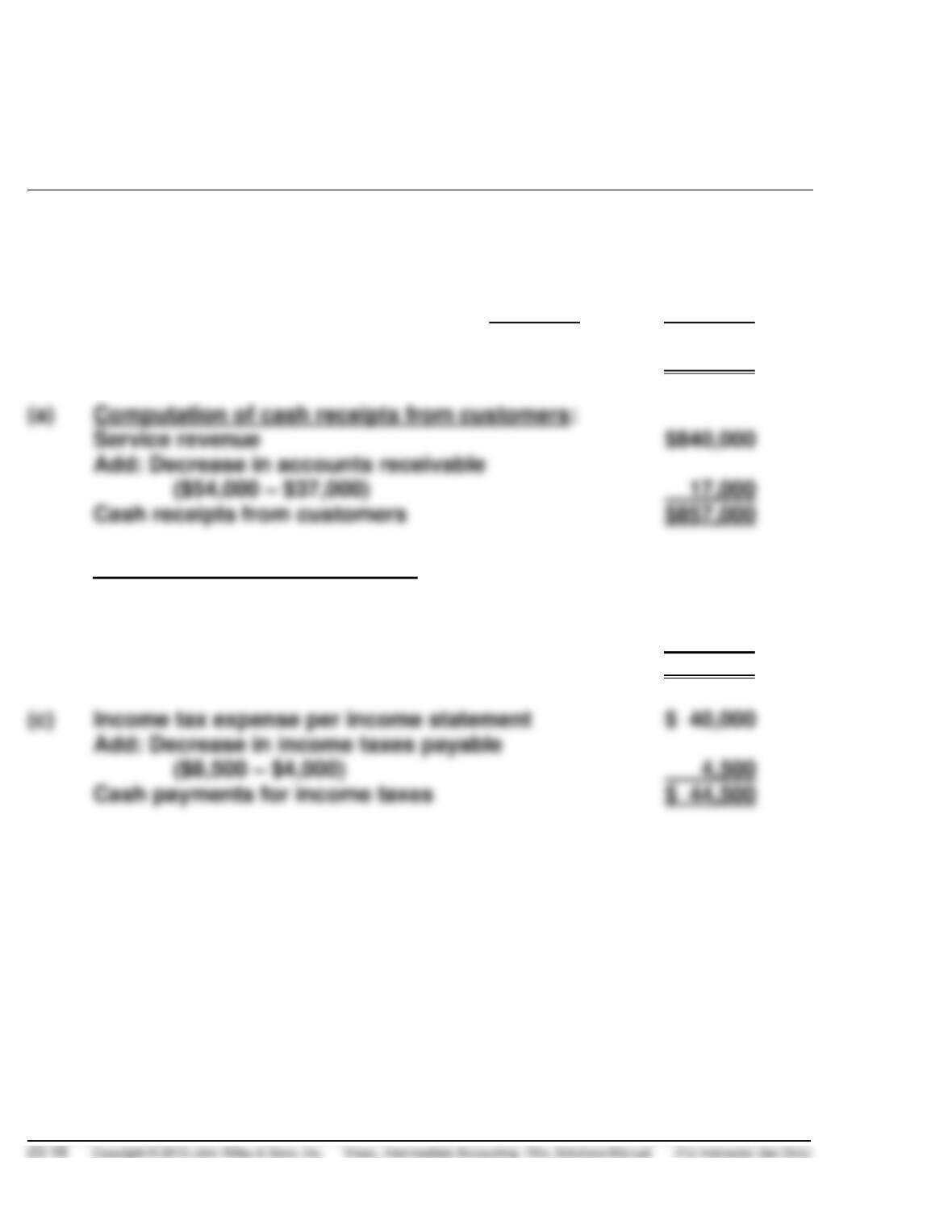

(a)

Computation of cash receipts from customers:

Service revenue

$840,000

Add: Decrease in accounts receivable

17,000

Cash receipts from customers

$857,000

(b)

Computation of cash payments:

Operating expenses per income statement

$624,000

Deduct: Increase in accounts payable

Deduct: ($41,000 – $31,000)

10,000

Cash payments for operating expenses

$614,000

(c)

Income tax expense per income statement

$ 40,000

Add: Decrease in income taxes payable

4,500

Cash payments for income taxes

$ 44,500

EXERCISE 23-6 (15–20 minutes)

KRAUSS COMPANY

Partial Statement of Cash Flows

For the Year Ended December 31, 2014

Cash flows from operating activities

Net income

$90,000

Adjustments to reconcile net income

to net cash provided by operating activities:

Depreciation expense

Loss on sale of equipment

Decrease in accounts receivable

Increase in accounts payable

Decrease in income taxes payable

EXERCISE 23-7 (15–20 minutes)

Situation A:

Cash flows from operating activities

Cash receipts from customers

($200,000 – $71,000)

$129,000

($110,000 – $29,000)

Situation B:

(a)

Computation of cash payments to suppliers

Cost of goods sold

Plus: Increase in inventory

Decrease in accounts payable

Operating expenses

Deduct: Decrease in prepaid expenses

Increase in accrued expenses

payable

EXERCISE 23-8 (20–30 minutes)

Cash flows from operating activities

$145,000

Net income

Adjustments to reconcile net income

to net cash provided by operating

activities:

Depreciation expense

Decrease in accounts receivable

Other comments:

No. 1 is shown as a cash inflow from the issuance of treasury stock and

cash outflow for the purchase of treasury stock, both financing activities.

No. 2 is shown as a cash inflow from investing activities of $20,000 and

the gain of $5,500 is deducted from net income in the operating activities

section.