COMPARATIVE ANALYSIS CASE

(a) Coca-Cola sponsors and/or contributes to pension plans covering

substantially all U.S. employees and certain employees in international

locations. Coca-Cola also sponsors nonqualified, unfunded defined

(b) Coca-Cola reported “net periodic benefit cost” of $249 million in 2011.

PepsiCo reported “pension expense” of $415 million in 2011 for U.S. plans.

(c) 2011 Funded Status ($millions) Pensions OPEB

COMPARATIVE ANALYSIS CASE (Continued)

Coca-Cola

Cash Flows

Pension Benefits

Other Benefits

Expected benefit payments:

2012

$ 486

$ 53

2013

501

56

2014

521

59

2015

537

62

2016

553

65

PepsiCo

Future Benefit Payments

Our estimated future benefit payments to beneficiaries are as follows:

2012

2013

2014

2015

2016

2017–2021

Pension

$560

$560

$560

$600

$645

$4,050

Retiree medical

$135

$135

$140

$145

$145

$ 730

FINANCIAL STATEMENT ANALYSIS CASE

(a) The components of postretirement expense are service cost, interest

(b) The accounting for defined-benefit plans and OPEBs is very similar.

For example, the measures of the obligation are similar and the com–

ponents of expense and their calculation are the same (with similar

smoothing mechanisms employed for both types of plans with respect to

gains and losses.) There are, however, a number of differences between

Postretirement Healthcare Benefits and Pensions:

Item

Pensions

Healthcare Benefits

Funding

Generally funded.

Generally NOT funded.

Benefit Payable

Monthly.

As needed and used.

Additionally, although healthcare benefits are generally covered by

the fiduciary and reporting standards for employee benefit funds under

ERISA, the stringent minimum vesting, participation, and funding

standards that apply to pensions do not apply to healthcare benefits.

ACCOUNTING, ANALYSIS, AND PRINCIPLES

Accounting

Balance in PBO at 12/31/2015

Balance at 1/1/2015 $820.5

Amount of plan assets at 12/31/2015

$516.9

Corridor test and amortization of net gain/loss

Corridor limit: 10% times greater of $820.5 and $476.5 = $ 82.1

Excess of net G/L over corridor limit = $92.0 – $82.1 = 9.9

Amortization = $9.9 ÷ 15 = 0.7

Pension expense:

Interest cost = ($820.5 X 0.10) = $ 82.1

$ 82.6

Balance in pension liability

Projected benefit obligation $904.6

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Balance in Unamortized Net Gain or Loss at 12/31/2015

($138.1)

Journal entry:

Pension Expense ……………………………………………… 82.6

PENCOMP, INC.

Income Statement

for the year ended Dec. 31, 2015

Revenues:

Sales ……………………………………………………………….. $3,000.0

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

PENCOMP, INC.

Statement of Financial Position

at Dec. 31, 2013

Assets:

Cash ……………………………………………………………………. $ 368.0

Liabilities:

Note payable ………………………………………………………… $1,000.0

Pension liability ……………………………………………………. 387.7

Total Liabilities ………………………………………… 1,387.7

Equity:

Common stock …………………………………………………….. $2,000.0

Note payable = no change from previous statement of financial position.

Pension liability = $387.7 per above analysis

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued)

Analysis

ROE = $37.4 ÷ $2,460.3 = 0.0152 or 1.52%.

In this example, the unexpected return on plan assets ‘skipped’ the income

statement and went to other comprehensive income. Had this item been

included in income, ROE would have been = ($37.4 –$46.8) ÷ $2,460.3 = –

Principles

The effects of plan amendments and actuarial gains and losses in a given

PROFESSIONAL RESEARCH

(a) According to FASB ASC 715–30–35:

35–22 Asset gains and losses are differences between the actual

return on plan assets during a period and the expected return

on plan assets for that period. Asset gains and losses include

35–24 As a minimum, amortization of a net gain or loss included in

accumulated other comprehensive income (excluding asset

gains and losses not yet reflected in market-related value) shall

be included as a component of net pension cost for a year if,

PROFESSIONAL RESEARCH (Continued)

(b) According to FASB ASC 715-30–35:

Gains and Losses

35–18 As established in the definition of the term, a gain or loss

results from a change in the value of either the projected

benefit obligation or the plan assets resulting from experience

35–19 Because gains and losses may reflect refinements in estimates

as well as real changes in economic values and because some

(c) According to FASB ASC 715-30–25:

25-1 If the projected benefit obligation exceeds the fair value of plan

assets, the employer shall recognize in its statement of

PROFESSIONAL SIMULATION

Note: This assignment is available on the Kieso website.

Measurement

(a)

A

B

C

D

E

F

G

H

I

J

K

L

M

N

5

6

General Journal Entries

Memo Record

7

Items

Annual

Pension

Expense

Cash

OCI—Prior

Service Cost

OCI—

Gain/Loss

Pension

Asset/Liability

Projected

Benefit

Obligation

Plan assets

8

9

Balance, Jan. 1, 2014

(145,000)

(625,000)

480,000

20–90 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

Service cost

Interest cost

Actual /Expected return

(52,000)

(5,000)

57,000

Amortization of PSC

(19,000)

Benefits

(85,000)

Liability increase

76,000

Journal entry for 2014

113,250

(99,000)

(19,000)

71,000

Accumulated OCI, Dec. 31, 2013

Balance, Dec. 31, 2014

71,000

(211,250)

(762,250)

551,000

PROFESSIONAL SIMULATION (Continued)

(b) Simply change the formula in cell B11 to multiply by .07; change the

formula in cell B12 to multiply .10 times (N9* – 1).

Journal Entry

Other Comprehensive Income (PSC) ………………… 19,000

Disclosure

Financial Statements

Income Statement

Pension expense …………………………………………….. $113,250

IFRS CONCEPTS AND APPLICATION

IFRS20-1

Net interest is defined as the amount that accrues by multiplying the net

benefit obligation by the discount rate (using defined benefit obligation and

Because payment of the pension obligation is deferred, companies record

the pension liability on a discounted basis. As a result, the liability accrues

interest over the life of the employee (passage of time), which is essentially

interest expense. Similarly, companies earn a return on its plan assets.

IFRS20-2

The service cost component of pension expense is determined as the

IFRS20-3

Past service cost is the cost of retroactive benefits (either positive or

negative) granted in a plan amendment or initiation of a pension plan. Also

IFRS20-4

IFRS20-5

Joshua Co. would report a pension asset of $10,000 ($345,000 – $335,000)

and in equity, accumulated other comprehensive gain of $8,300.

IFRS20-6

Current Service cost ……………………………………………….. $26,000

Statement of Comprehensive Income

Revenues $125,000

Expenses 85,000

20–94 Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only)

IFRS20-8

DOREEN CORP.

Pension Worksheet—2014

General Journal Entries Memo Record

Items

Annual

Pension

Expense

Cash

Pension

Asset/

Liability

Projected

Benefit

Obligation

Plan

Assets

Balance, Dec. 31, 2013

13,800 Cr.

560,000 Cr.

546,200 Dr.

Prior service cost

120,000 Dr.

120,000 Cr.

Balance, Jan. 1, 2014

680,000 Cr.

546,200 Dr.

Service cost

58,000 Dr.

61,200 Dr.

Interest revenue**

49,158 Cr.

Contributions

Benefits

Journal entry for 2014

190,042 Dr.

Balance, Dec. 31, 2014

759,200 Cr.

620,358 Dr.

Copyright © 2013 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 15/e, Solutions Manual (For Instructor Use Only) 20–95

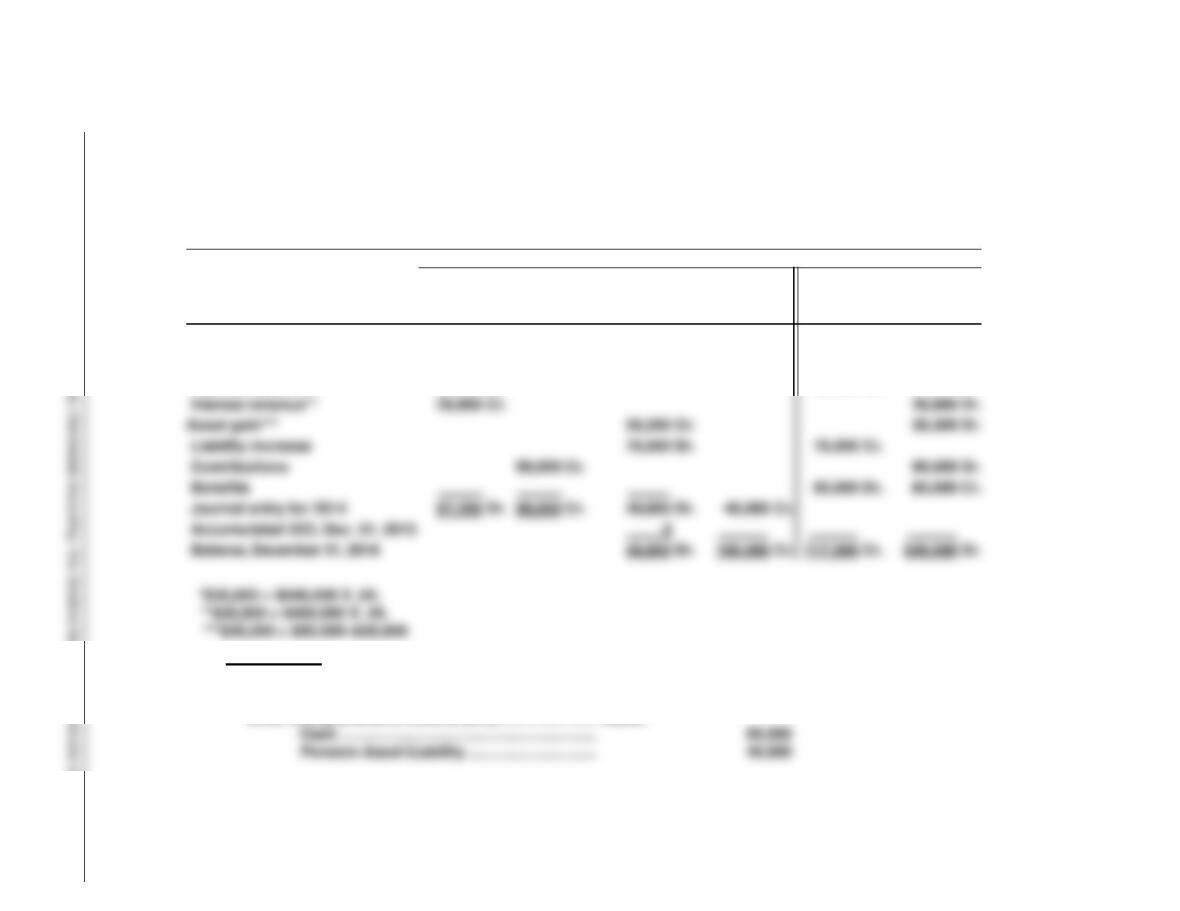

IFRS20-9

(a) BUHL CORP

Pension Worksheet

General Journal Entries

Memo Record

Items

Annual

Pension

Expense

Cash

OCI—

Gain/Loss

Pension

Asset/

Liability

Defined

Benefit

Obligation

Plan Assets

Balance, Jan. 1, 2014

120,000 Cr.

600,000 Cr.

480,000 Dr.

Service cost

90,000 Dr.

90,000 Cr.

Interest expense*

36,000 Dr.

36,000 Cr.

(b) Journal Entry

Pension Expense………………………………………………. 97,200

Other Comprehensive Income (G/L)…………………… 49,800

Interest revenue**

28,800 Cr.

Liability increase

76,000 Cr.

Contributions

Benefits

85,000 Dr.

Journal entry for 2014

97,200 Dr.

Accumulated OCI, Dec. 31, 2013

Balance, December 31, 2014

168,000 Cr.

717,000 Cr.

549,000 Dr.

IFRS20-10

(a) Actual Return = (Ending – Beginning) – (Contributions – Benefits)

Fair value of plan assets,

(b) Computation of pension liability gains and losses and pension asset gains and losses.

Difference between 12/31/14 actuarially computed DBO and 12/31/14 recorded

projected benefit obligation (DBO):

Difference between actual fair value of plan assets and

12/31/14 actual fair value

of plan assets …………………………………. 2,620

The amount recorded in other comprehensive income is The asset gain and

liability loss:

Asset gain ………………………………………………………………………… $ 250

Liability loss ……………………………………………………………………… 350

IFRS20-11 Accounting Research

(a) According to IAS 19, (pars 127–130) 127 Remeasurements of the net

defined benefit liability (asset) comprise: (a) actuarial gains and losses (see

128 Actuarial gains and losses result from increases or decreases in the

present value of the defined benefit obligation because of changes in

actuarial assumptions and experience adjustments. Causes of actuarial

gains and losses include, for example: (a) unexpectedly high or low rates

of employee turnover, early retirement or mortality or of increases in

salaries, benefits (if the formal or constructive terms of a plan provide for

inflationary benefit increases) or medical costs;

130 In determining the return on plan assets, an entity deducts the costs of

managing the plan assets and any tax payable by the plan itself, other than

tax included in the actuarial assumptions used to measure the defined

benefit obligation (paragraph 76). Other administration costs are not

deducted from the return on plan assets.

IFRS20-11 (Continued)

BC90 The Board confirmed the proposal made in the 2010 ED that an entity

should recognize remeasurements in other comprehensive income. The

BC95 However, most respondents to the 2010 ED expressed the view that it

would be inappropriate to recognise in profit or loss short-term

fluctuations in an item that is long-term in nature. The Board concluded

that in the light of the improved presentation of items of other

comprehensive income in its amendment to IAS 1 issued in June 2011, the

most informative way to disaggregate the components of defined benefit

cost with different predictive values is to recognise the remeasurement

component in other comprehensive income.

With respect to recycling these amounts into net income in subsequent

periods:

(a) there is no consistent policy on reclassification to profit or loss in

IFRSs, and it would have been premature to address this matter in the

context of the amendments made to IAS 19 in 2011.

IFRS20-11 (Continued)

64 When an entity has a surplus in a defined benefit plan, it shall measure

65 A net defined benefit asset may arise where a defined benefit plan has

been overfunded or where actuarial gains have arisen. An entity recognises

a net defined benefit asset in such cases because:

(a) the entity controls a resource, which is the ability to use the surplus to

generate future benefits;

IFRS20–12

(a) M&S provides pension arrangements for the benefit of its UK

employees through the Marks & Spencer UK Pension Scheme. This

has a defined benefit section, which was closed to new entrants with

effect from 1 April 2002, and a defined contribution section which has

IFRS20-12 (Continued)

(d) M&S’s Analysis of assets and expected rates of return portion of its

pension footnote details the major categories of assets, which are