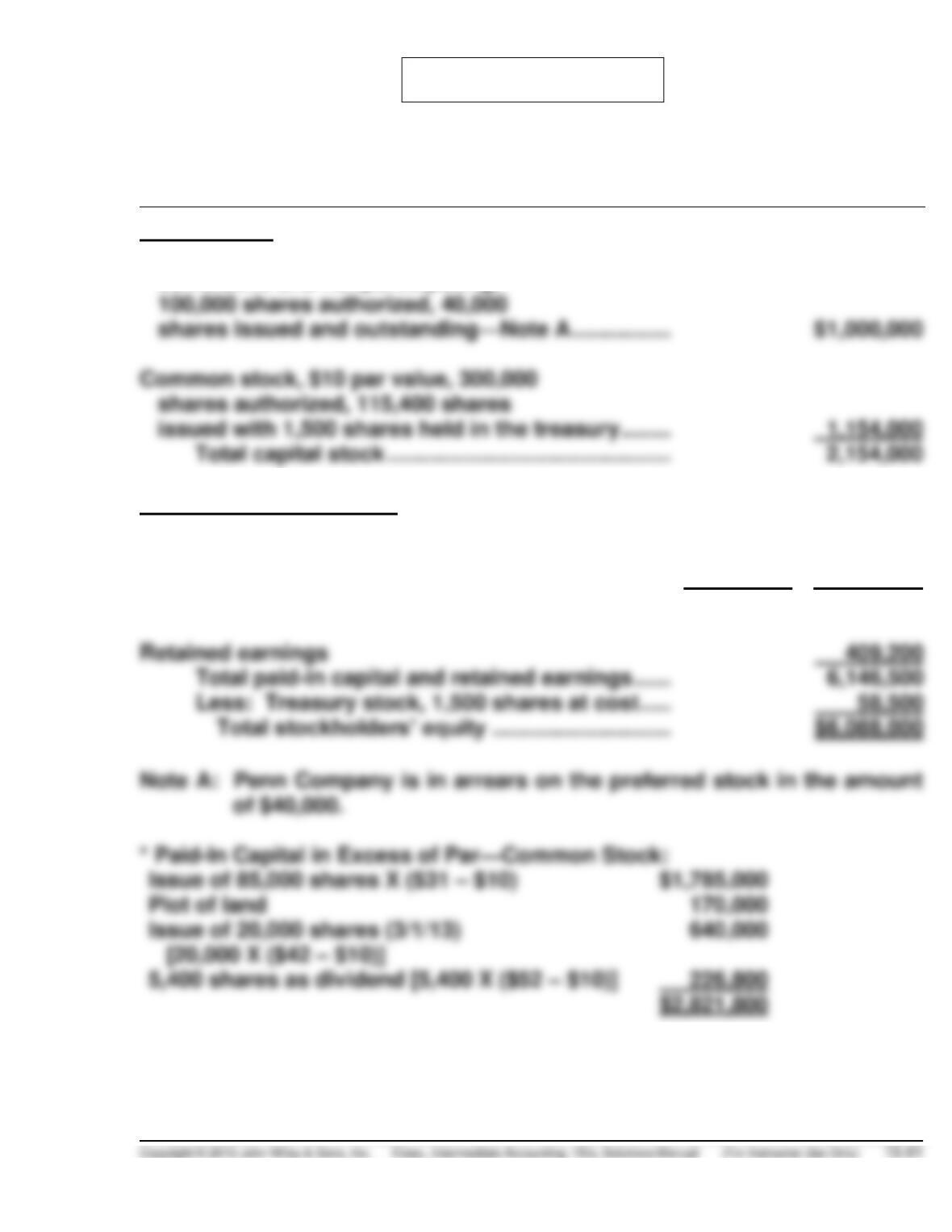

PROBLEM 15–12

PENN COMPANY

Stockholders’ Equity

June 30, 2015

Capital stock

8% preferred stock, $25 par value,

cumulative and nonparticipating,

100,000 shares authorized, 40,000

$1,000,000

shares authorized, 115,400 shares

issued with 1,500 shares held in the treasury ……..

1,154,000

Total capital stock ……………………………………….

2,154,000

Additional paid-in capital

In excess of par-preferred …………………………………….

$ 760,000

In excess of par-common …………………………………….

2,821,800*

From treasury stock …………………………………………….

1,500

3,583,300

Total paid-in capital ……………………………………..

5,737,300

409,200

6,146,500

58,500

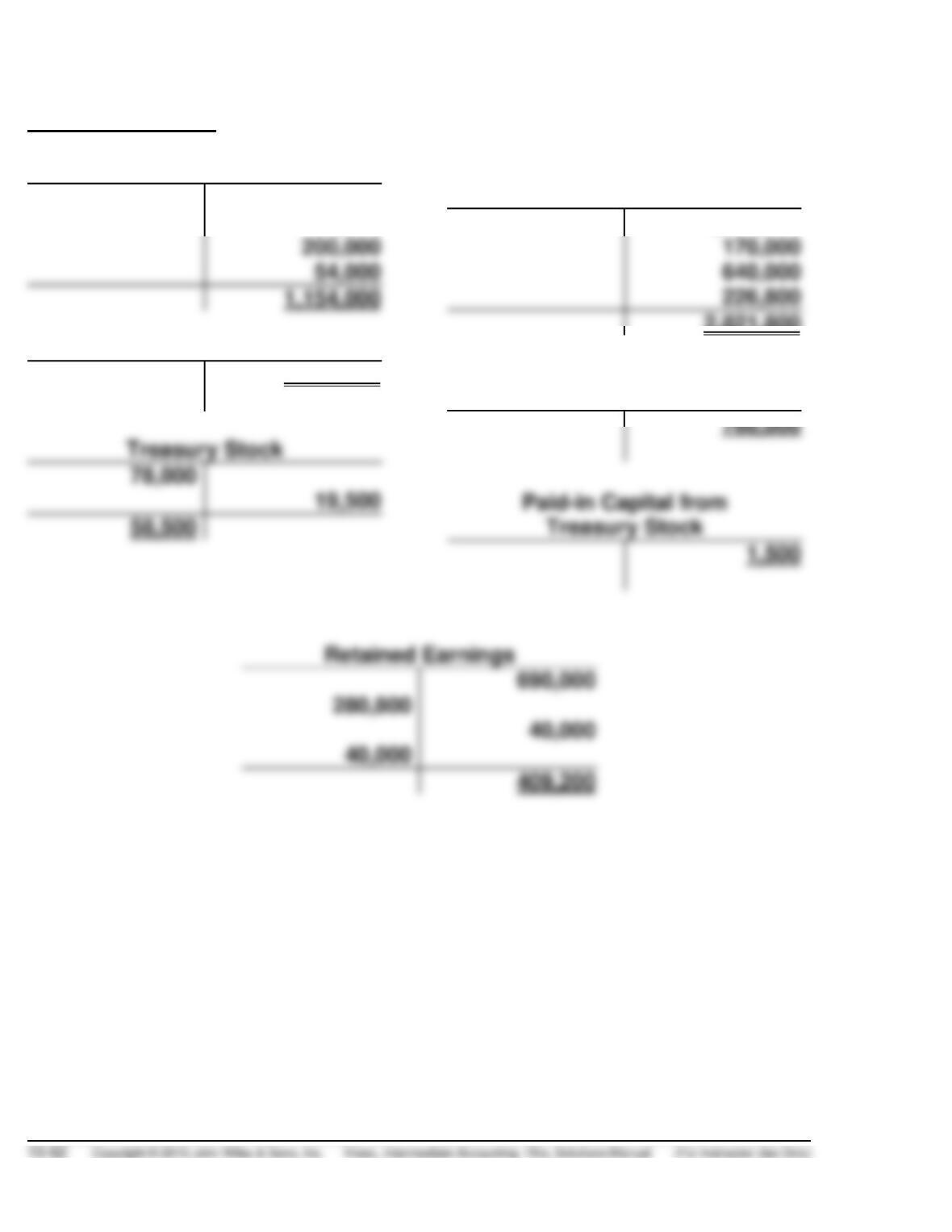

PROBLEM 15-12 (Continued)

Account Balances

Common Stock

850,000

50,000

54,000

640,000

226,800

Preferred Stock

1,000,000

1,500

280,800

40,000

409,200

Paid-in Capital in

Excess of Par—Common Stock

1,785,000

2,821,800

Paid-in Capital in

Excess of Par—Preferred Stock

Note that the Penn Company is authorized to issue 300,000 shares of

$10 par value common and 100,000 shares of $25 per value, cumulative and

nonparticipating preferred.

PROBLEM 15-12 (Continued)

Entries supporting the balances.

Common Stock

Entries

1. Cash ……………………………………………………….. 2,635,000

2. Land ……………………………………………………….. 220,000

3. Cash ……………………………………………………….. 840,000

Common Stock …………………………………. 200,000

Paid-in Capital in Excess of Par—

Common Stock ………………………………. 640,000

At the beginning of the year, Penn had 110,000 common shares out–

standing, of which 85,000 shares were issued at $31 per share, resulting

Preferred Stock

Cash ……………………………………………………….. 1,760,000

Preferred Stock ………………………………… 1,000,000

Paid-in Capital in Excess of Par—

Preferred Stock ………………………………. 760,000

PROBLEM 15-12 (Continued)

The issuance of 40,000 shares of preferred at $44 resulted in $1,000,000

(40,000 shares at $25) of preferred stock outstanding and $760,000

(40,000 shares at $19) of paid-in capital on preferred.

Treasury Stock

Nov. 30 Treasury Stock ……………………………………. 78,000

Cash ………………………………………………. 78,000

Stock Dividend

Dec. 15 Retained Earnings …………………………….. 280,800**

Common Stock …………………………….. 54,000*

Paid-in Capital in Excess of Par—

Common Stock. …………………………. 226,800

PROBLEM 15-12 (Continued)

Retained Earnings

The cash dividends only affect the retained earnings. Note that the

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 15-1 (Time 10–20 minutes)

Purpose—to provide the student with some familiarity with the applications of the capital stock share

CA 15-2 (Time 15–20 minutes)

CA 15-3 (Time 25–30 minutes)

Purpose—to provide a five-part theory case on equity based on Statement of Financial Accounting

Concepts No. 6. It requires defining terms and analyzing the effects of equity transactions on financial

statement elements.

CA 15-4 (Time 25–30 minutes)

Purpose—to provide the student with an understanding of the conceptual framework which underlies

CA 15-5 (Time 15–20 minutes)

Purpose—to provide the student with an understanding of the theoretical concepts and implications that

CA 15-6 (Time 20–25 minutes)

Purpose—to provide the student with a situation containing a cash dividend declaration, a stock dividend,

and a reacquisition and reissuance of shares requiring the student to explain the accounting treatment.

CA 15-7 (Time 10–15 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 15-1

(a) To share proportionately in any new issues of stock of the same class (the preemptive right).

(b) Derek Wallace bought an additional $100,000 par value stock. His original ownership was

(c) No information is given with respect to the fair value of the stock. In this situation, an estimate for

fair value could be developed based on market transactions involving comparable assets. Otherwise,

CA 15-2

(a) The general rule to be applied when stock is issued for services or property other than cash is

that the property or services be recorded at either their fair value or the fair value of the stock

issued, whichever is more clearly determinable.

CA 15-3

(a) Equity, or net assets, is the owners’ residual interest in the assets of an entity that remains after

deducting liabilities; in other words, equity equals assets less liabilities. Assets are probable future

CA 15-3 (Continued)

(b) Transactions or events that change owners’ equity include revenues and expenses, gains and

losses, investments by owners, distributions to owners, and changes within owners’ equity.

(c) Investments by owners are increases in net assets resulting from transfers by other entities of

something of value to obtain ownership. Examples of investments by owners are issuance of

CA 15-4

(a) A stock dividend is the issuance by a corporation of its own stock to its stockholders on a prorata

(1) From the legal standpoint a stock split is distinguished from a stock dividend in that a split

results in an increase in the number of shares outstanding and a corresponding decrease in

(2) The major distinction is that a stock dividend requires a journal entry to decrease retained

earnings and increase paid-in capital, while there is no entry for a stock split. Also, from the

accounting standpoint the distinction between a stock dividend and a stock split is

(b) The usual reason for issuing a stock dividend is to give the stockholders something on a dividend

date and yet conserve working capital.

A stock dividend that is charged to retained earnings reduces the total accumulated earnings,

CA 15-4 (Continued)

A stock dividend also may be issued for the purpose of obtaining a wider distribution of the stock.

Although this is the main consideration in a stock split, it may be a secondary consideration in the

(c) The amount of retained earnings to be capitalized in connection with a stock dividend (in the

accounting sense) might be (1) the legal minimum (usually par or stated value), (2) the average

paid-in capital per outstanding share, or (3) the fair value of the shares.

CA 15-5

(a) The case against treating an ordinary stock dividend as income is supported by a majority of

accounting authorities. It is based upon “entity” and “proprietary” interpretations.

If the corporation is considered an entity separate from stockholders, the income of the

corporation is corporate income and not income to stockholders, although the equity of the

equity since there is no increase in total proprietorship.

(b) The case against issuing stock dividends on treasury stock rests principally upon the argument

that stock reacquired by the corporation is a “reduction of capital” through the payment of cash to

reduce the number of outstanding shares. According to this view, the corporation cannot obtain a

CA 15-6

(a) Mask Company should account for the purchase of the treasury stock on August 15, 2014, by

debiting Treasury Stock and crediting Cash for the cost of the purchase (1,000 shares X $18 per

share). Mask should account for the sale of the treasury stock on September 14, 2014, by

(b) Mask should account for the stock dividend by debiting Retained Earnings for $21 per share (the

market price of the stock in October 2014, the date of the stock dividend) multiplied by the

1,950 shares distributed. Mask should then credit Common Stock for the par value of the common

(c) Mask should account for the cash dividend on December 20, 2014, the declaration date, by

debiting Retained Earnings and crediting Dividends Payable for $1 per share multiplied by the

CA 15-7

(a) The stakeholders are the dissident stockholders, the other stockholders, potential investors,

creditors, and Kenseth.

(b) The ethical issues are honesty, job security, and personal responsibility to others. That is, by

FINANCIAL REPORTING PROBLEM

(a) P&G’s preferred stock has a stated value of $1 per share.

(d) At June 30, 2011 and June 30, 2010, P&G had 2,766 (4,008 – 1,242)

million and 2,844 (4,008 – 1,164) million shares of common stock

outstanding, respectively.

(f) Rate of return on common stock equity:

2011: ($11,797 – $233)/[$66,406 + $59,838)/2] = 18.3%

2010: ($12,736 – $219)/[$59,838 + $61,775)/2] = 20.6%

(g) Payout ratio:

(h) Price range for the quarter ended June 30, 2011:

COMPARATIVE ANALYSIS CASE

(a) Par value:

Coca-Cola, $0.25 per share.

PepsiCo, $0.012/3 per share.

(d) Common or capital stock shares outstanding, year-end 2011:

Coca-Cola, 3,520,000,000 – 1,257,000,000 = 2,263,000,000.

PepsiCo, 1,865,000,000 – 301,000,000 = 1,564,000,000.

(f) Rate of return on common stock equity.

2011:

COMPARATIVE ANALYSIS CASE (Continued)

2010:

PepsiCo,

= 33.1%

(g) Payout ratios for 2011.

Coca-Cola,

$4,300

= 50.2%

$8,572

(h) Market price range of stock during the fourth quarter of 2011: