EXERCISE 18-7 (Continued)

2. 6/3 Accounts Receivable (Ann Mount) ………… 7,840

Sales Revenue

[$8,000 – (2% X $8,000)] ………………. 7,840

6/5 Sales Returns and Allowances ……………… 588

EXERCISE 18-8 (10–15 minutes)

(a) Cash ……………………………………………………………………… 240,000

Rent Revenue

EXERCISE 18-8 (continued)

(b) The marina operator should recognize that advance rentals generated

$190,400 ($152,000 + $38,400) of cash in exchange for the marina’s

EXERCISE 18-9 (15–20 minutes)

(a) Inventoriable costs:

80 units shipped at cost of $500 each ………… $40,000

Freight ……………………………………………………… 840

Total inventoriable cost ………………………. $40,840

EXERCISE 18-10 (10–15 minutes)

(a) The conditions for a multiple-deliverable arrangement exist for Appliance

Center since the delivered item has value to the customer on a stand–

EXERCISE 18-11 (5–10 minutes)

(a) Cash …………………………………………………………………. 50,000

EXERCISE 18-12 (20–25 minutes)

(a) Gross profit recognized in:

2014

2015

2016

Contract price

$1,600,000

$1,600,000

$1,600,000

Costs:

$400,000

$825,000

Total estimated profit

to date

recognized

years

EXERCISE 18-12 (Continued)

(b) Construction in Process ($825,000 – $400,000) …. 425,000

Materials, Cash, Payables …………………………. 425,000

Accounts Receivable ($900,000 – $300,000) ……… 600,000

EXERCISE 18-13 (10–15 minutes)

(a) Contract billings to date ………………………………….. $61,500

Less: Accounts receivable 12/31/14 ………………… 18,000

EXERCISE 18-14 (10–12 minutes)

DOUGHERTY INC.

Computation of Gross Profit to be

Recognized on Uncompleted Contract

EXERCISE 18-15 (25–30 minutes)

(a) 1. Gross profit recognized in 2014:

Contract price ………………………………………… $1,200,000

Costs:

Costs to date …………………………………… $280,000

2. Construction in Process ($600,000 – $280,000) … 320,000

Materials, Cash, Payables ……………………….. 320,000

Accounts Receivable ($500,000 – $150,000) ……. 350,000

Billings on Construction in Process ………… 350,000

Cash ($320,000 – $120,000) ……………………………. 200,000

EXERCISE 18-16 (15–20 minutes)

in 2014) = $1,320,000 (revenue recognized in 2015).

EXERCISE 18-16 (Continued)

(b) All $2,200,000 of the contract price is recognized as revenue in 2015.

(c) Using the percentage-of-completion method, the following entries

would be made:

EXERCISE 18-17 (15–25 minutes)

(a) Computation of Gross Profit to Be Recognized under Completed–

Contract Method.

EXERCISE 18-17 (Continued)

(b) Computation of Gross Profit to Be Recognized under Percentage–of–

Completion Method.

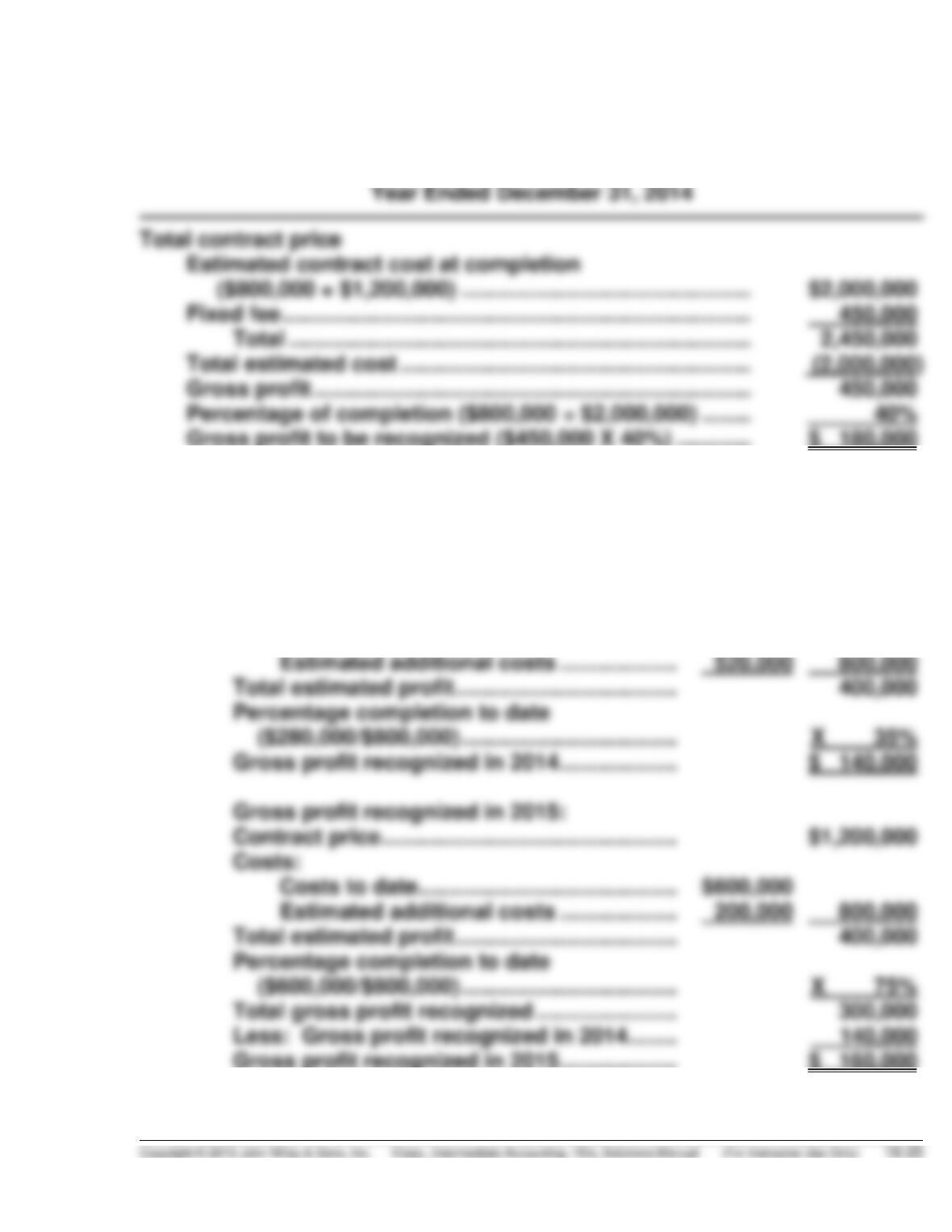

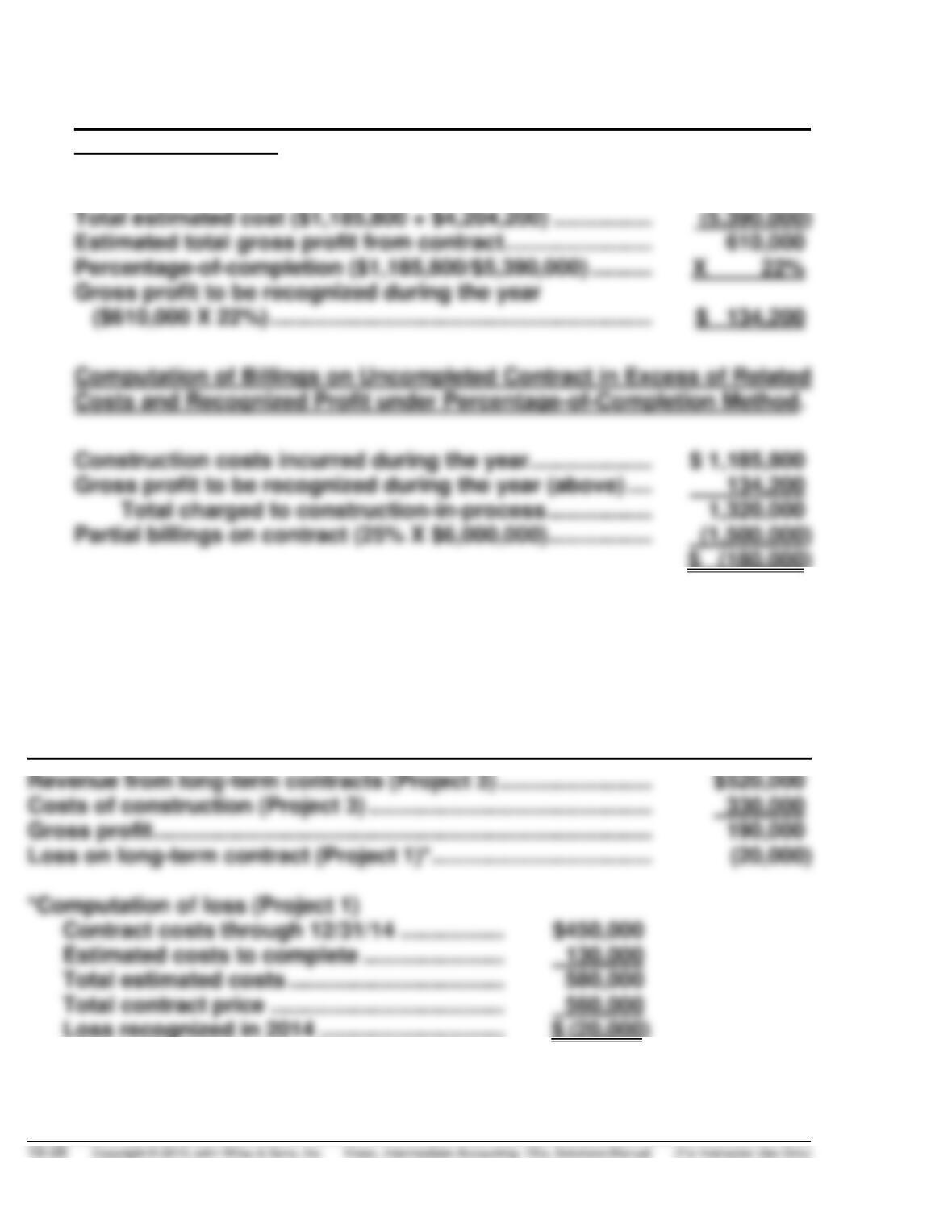

Total contract price ……………………………………………………. $6,000,000

EXERCISE 18-18 (15–25 minutes)

BERSTLER CONSTRUCTION COMPANY

Partial Income Statement

Year Ended December 31, 2014

EXERCISE 18-18 (Continued)

BERSTLER CONSTRUCTION COMPANY

Partial Balance Sheet

December 31, 2014

EXERCISE 18-19 (15–20 minutes)

(a) Computation of gross profit recognized:

2014

2015

$370,000 X 34%*

$125,800

$450,000 X 32%**

$125,800

EXERCISE 18-19 (Continued)

Cash ………………………………………………………………. 800,000

Installment Accounts Receivable, 2014 ………… 350,000

EXERCISE 18-20 (15–20 minutes)

(a) Deferred Gross Profit, 2014 ……………………………… 2,800*

Deferred Gross Profit, 2015 ……………………………… 12,800**

Deferred Gross Profit, 2016 ……………………………… 69,400***

Realized Gross Profit ……………………………….. 85,000

EXERCISE 18-20 (Continued)

(b) Cash collected in 2016 on accounts receivable of 2014:

EXERCISE 18-21 (15–20 minutes)

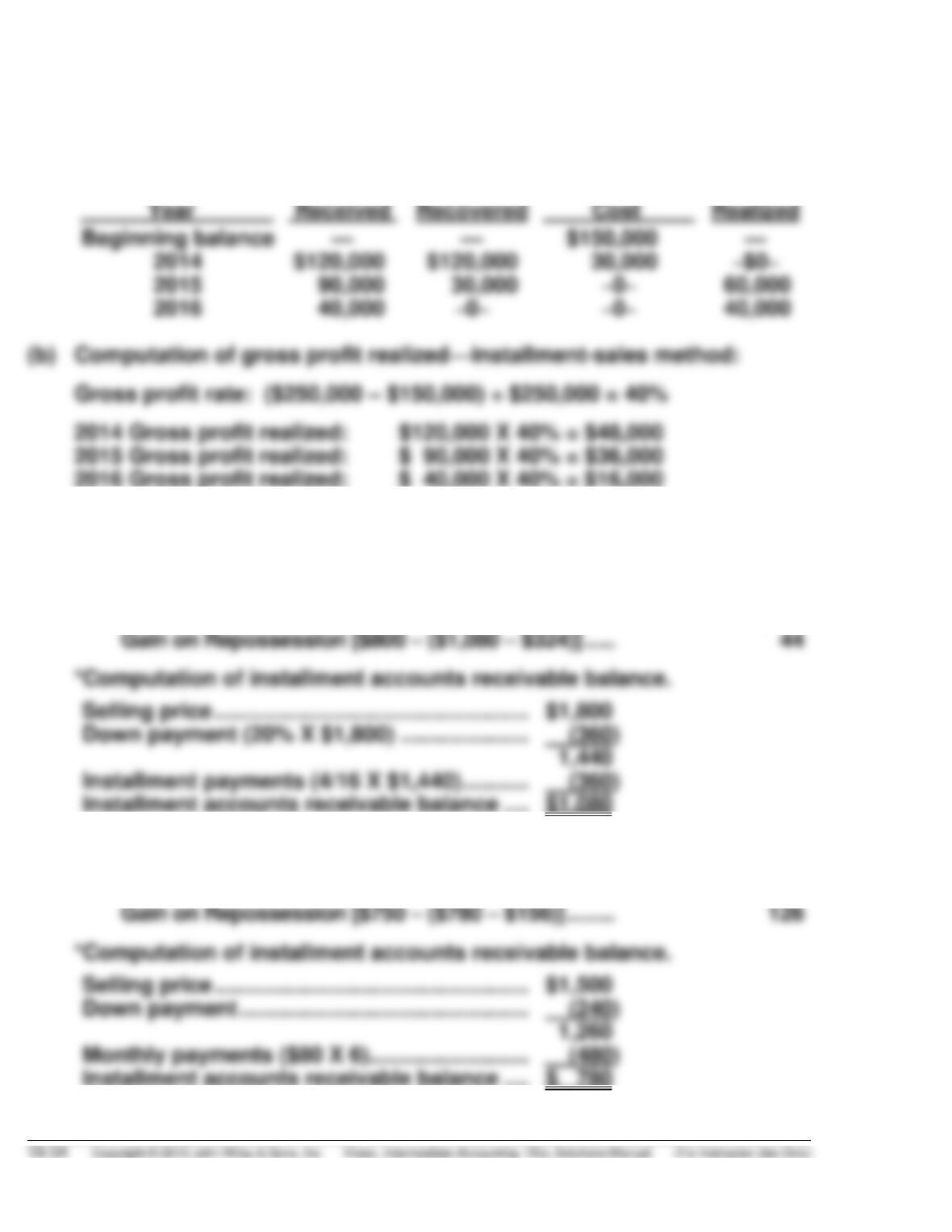

Gross Profit Rate—2014: ($750,000 – $510,000) ÷ $750,000 = 32%

Gross Profit Rate—2015: ($840,000 – $588,000) ÷ $840,000 = 30%

(a) Balance, December 31, 2014:

Deferred Gross Profit Account—2014 Installment Sales

EXERCISE 18-21 (Continued)

(b) Repossessed Merchandise ……………………………….. 8,000

EXERCISE 18-22 (10–15 minutes)

BECKER CORPORATION

Income before Income Taxes on Installment-Sale Contract

For the Year Ended December 31, 2014

EXERCISE 18-23 (10–15 minutes)

(a) Realized gross profit recognized in 2015 under the installment-sales

and 21.875% respectively.

EXERCISE 18-23 (Continued)

Sale Year

Gross Profit Percentage

2015

Collections

2015

Realized Profit

1. As a current liability on the theory that it is related to Installment

Accounts Receivables that are normally treated as current assets;

3. As an adjustment or offset to the related Installment Accounts

Receivable. This is because the deferred gross profit is a part of reve–

nue from installment sales not yet realized. The related receivable

will be overstated unless the deferred gross profit is deducted.

EXERCISE 18-24 (15–20 minutes)

(a) Computation of gross profit realized—cost-recovery method:

Cash

Original

Cost

Balance of

Unrecovered

Gross

Profit

EXERCISE 18-25 (10–15 minutes)

1. Repossessed Merchandise …………………………………… 800

Deferred Gross Profit (30% X $1,080*)……………………. 324

Installment Accounts Receivable ……………………. 1,080*

2. Repossessed Merchandise …………………………………… 750

Deferred Gross Profit (20% X $780*) ……………………… 156

Installment Accounts Receivable ……………………. 780*

EXERCISE 18-26 (15–20 minutes)

Cash ………………………………………………………………………… 500

Installment Accounts Receivable ………………………… 500

Deferred Gross Profit (30% X $500) ……………………………. 150

Realized Gross Profit …………………………………………. 150

Discount on Notes Receivable

[$42,000 – (2.48685* X $14,000)] ……………….. 7,184

Revenue from Franchise Fees …………………….. 62,816

(b) Cash …………………………………………………………………. 28,000

Unearned Franchise Fees ……………………………. 28,000

Present value of an ordinary annuity

($8,000 X 3.69590) ……………………………….. 29,567.20

Total revenue recorded by Campbell and

total acquisition cost recorded by

Lesley Benjamin ………………………………….. $39,567.20

2. $10,000 cash received from down payment.

TIME AND PURPOSE OF PROBLEMS

Problem 18-1 (Time 30–45 minutes)

Purpose—the student defines and describes the point of sale, completion of production, percentage-of–

Problem 18-2 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of both the percentage-of-completion and

Problem 18-3 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of the percentage-of-completion method of

Problem 18-4 (Time 20–30 minutes)

Purpose—to provide the student with an understanding of both the accounting procedures involved

Problem 18-5 (Time 25–30 minutes)

Problem 18-6 (Time 20–25 minutes)

Purpose—to provide the student with a long-term construction contract problem that requires the

Problem 18-7 (Time 20–25 minutes)

Purpose—to provide the student with a long-term construction contract problem that requires the

Problem 18-8 (Time 25–30 minutes)

Purpose—to provide the student with an understanding of the proper accounting under the installment-

Problem 18-9 (Time 30–35 minutes)

Purpose—to provide the student with an understanding of the installment-sales method of accounting

Problem 18-10 (Time 30–40 minutes)

Purpose—to provide the student with an understanding of the applications of the installment-sales

Problem 18-11 (Time 20–25 minutes)

Problem 18-12 (Time 40–50 minutes)

Purpose—to provide the student with an understanding of the applications of the installment-sales

Problem 18-13 (Time 20–25 minutes)

Problem 18-14 (Time 50–60 minutes)

Purpose—to provide the student with an understanding of the installment-sales method of accounting

Problem 18-15 (Time 20–30 minutes)

Purpose—to provide the student with a problem requiring the computation of “cost of uncompleted

Problem 18-16 (Time 40–50 minutes)

Problem 18-17 (Time 50–60 minutes)

PROBLEM 18-1

(a) 1. The point of sale method recognizes revenue when the earnings

2. The completion-of-production method recognizes revenue only when

the project is complete and the contract is completed. This is used

primarily with short-term contracts, or with long–term contracts when

3. The percentage-of-completion method of revenue recognition is

used on long-term projects, usually construction. To apply it, the

following conditions must exist:

(i) A firm contract price with a high probability of collection.

PROBLEM 18-1 (Continued)

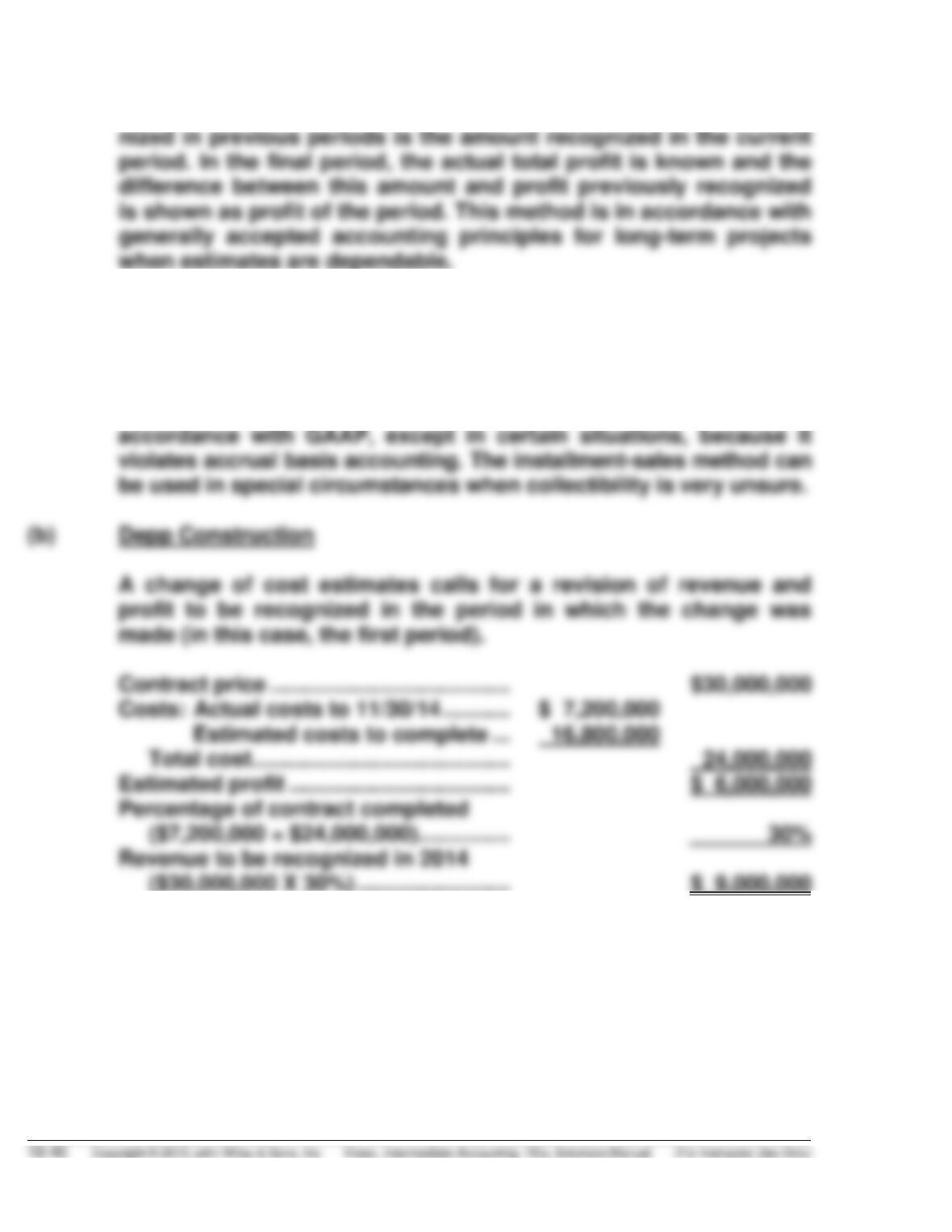

recognized to that date. That total less the income that was recog–

4. The installment-sales method may be applicable when the sales

price is received over an extended period of time. The installment–

sales method recognizes revenue as the cash is collected and is used

when the collection of the sales price is not reasonably assured.

This method is commonly used for tax purposes, but it is not in