EXERCISE 10-23 (20–25 minutes)

(a) C

(b) E (immaterial)

EXERCISE 10-24 (20–25 minutes)

(a)

Depreciation Expense (8/12 X $60,000) ……………………..

40,000

Accumulated Depreciation—Machinery …………….

40,000

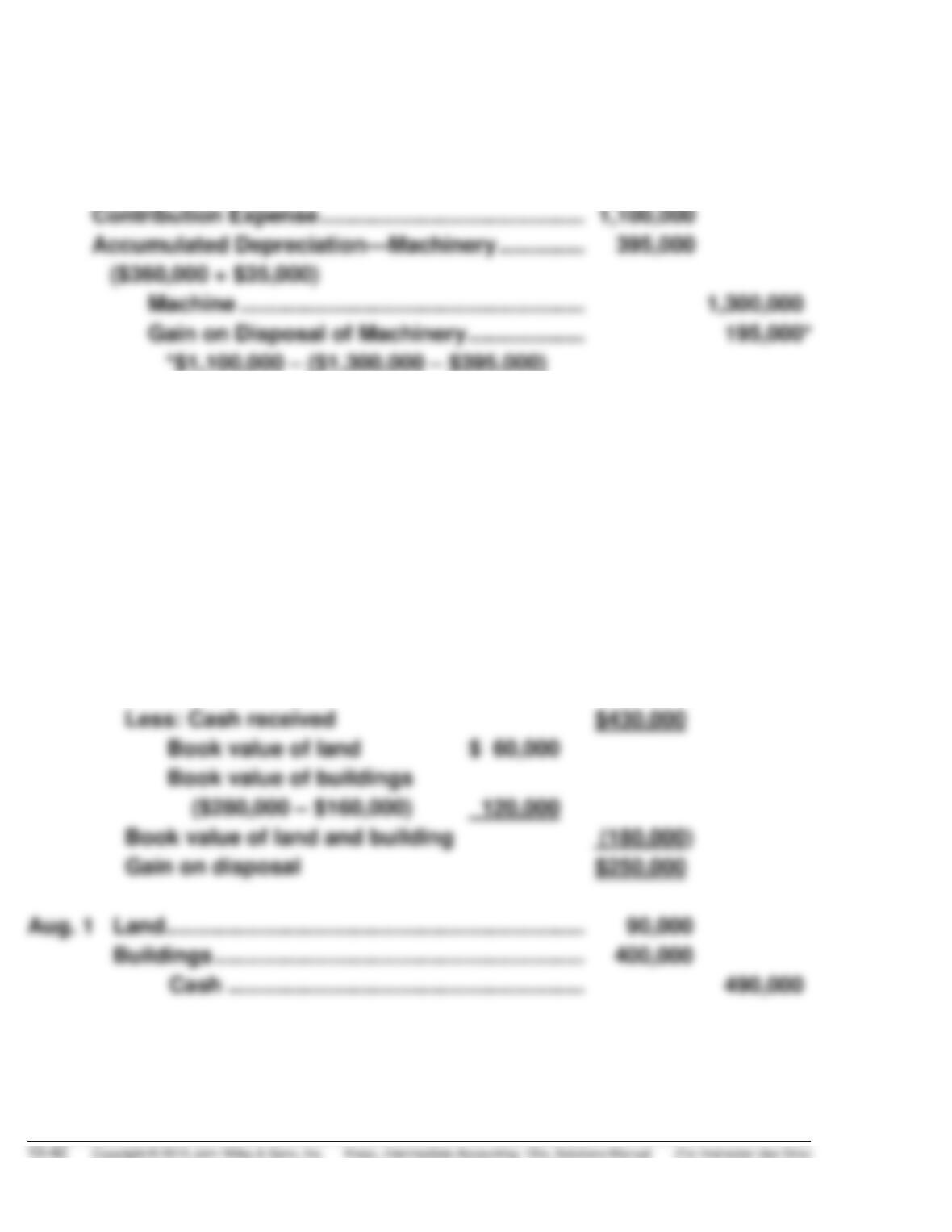

Loss on Disposal of Machinery …………………………..

($1,300,000 – $400,000) – $430,000

Cash ………………………………………………………………………

Accumulated Depreciation—Machinery …………………….

($360,000 + $40,000)

Machine ……………………………………………………….

(b)

Depreciation Expense (3/12 X $60,000) ……………………..

15,000

Accumulated Depreciation—Machinery …………….

15,000

Cash ………………………………………………………………………

1,040,000

Accumulated Depreciation—Machinery …………………….

($360,000 + $15,000)

Machine ……………………………………………………….

Gain on Disposal of Machinery …………………………

EXERCISE 10-24 (Continued)

(c)

Depreciation Expense (7/12 X $60,000) …………………….

35,000

Accumulated Depreciation—Machinery ……………

35,000

Contribution Expense ……………………………………………..

Accumulated Depreciation—Machinery ……………………

($360,000 + $35,000)

Machine ……………………………………………………….

Gain on Disposal of Machinery ………………………..

*$1,100,000 – ($1,300,000 – $395,000)

EXERCISE 10-25 (15–20 minutes)

April 1

Cash ………………………………………………………………………

430,000

Accumulated Depreciation—Buildings ……………………..

160,000

Land ……………………………………………………….

60,000

Building ……………………………………………………….

280,000

Gain on Disposal of Plant Assets ……………………..

250,000*

*Computation of gain:

Aug. 1

Land …………………………..…………………………………………..

90,000

Buildings ……………………………………………………….

400,000

Cash ……………………………………………………….

490,000

TIME AND PURPOSE OF PROBLEMS

Problem 10-1 (Time 35–40 minutes)

Purpose—to provide a problem involving the proper classification of costs related to property, plant,

Problem 10-2 (Time 40–55 minutes)

Purpose—to provide a problem involving the proper classification of costs related to property, plant,

Problem 10-3 (Time 35–45 minutes)

Purpose—to provide a problem involving the proper classification of costs related to land and buildings.

Typical transactions involve allocation of the cost of removal of a building, legal fees paid, general

expenses, cost of organization, special tax assessments, etc. A good problem for providing a broad

perspective as to the types of costs expensed and capitalized.

Problem 10-4 (Time 35–40 minutes)

Purpose—to provide a problem involving the method of handling the disposition of certain properties.

Problem 10-5 (Time 20–30 minutes)

Purpose—to provide the student with a problem in which schedules must be prepared on the costs of

acquiring land and the costs of constructing a building. Interest costs are included.

Problem 10-6 (Time 25–35 minutes)

Problem 10-7 (Time 20–30 minutes)

Problem 10-8 (Time 35–45 minutes)

Purpose—to provide the student with a problem involving the exchange of machinery. Four different

Problem 10-9 (Time 30–40 minutes)

Purpose—to provide a problem on the accounting treatment for exchanges of assets that have and do

not have commercial substance involving gain situations.

Problem 10-10 (Time 30–40 minutes)

Problem 10-11 (Time 35–45 minutes)

Purpose—to provide a property, plant, and equipment problem consisting of three transactions that

have to be recorded—(1) an asset purchased on a deferred payment contract, (2) a lump-sum purchase,

and (3) a nonmonetary exchange.

SOLUTIONS TO PROBLEMS

PROBLEM 10-1

(a) REAGAN COMPANY

Analysis of Land Account

for 2014

Balance at January 1, 2014 ……………….

$ 230,000

Land site number 621

Acquisition cost ………………………………

Commission to real estate agent ………

Less: Amounts recovered ……………….

Total land site number 621 ……..

Land site number 622

Land value ………………………………………

300,000

Building value ………………………………….

Demolition cost ……………………………….

Total land site number 622 ……..

461,000

REAGAN COMPANY

Analysis of Buildings Account

for 2014

Balance at January 1, 2014 ………………………

$ 890,000

Cost of new building constructed

on land site number 622

Construction costs ………………………….

Architectural design fees …………………

Building permit fee ………………………….

PROBLEM 10-1 (Continued)

REAGAN COMPANY

Analysis of Leasehold Improvements Account

for 2014

Balance at January 1, 2014 ………………………………………..

$660,000

Balance at December 31, 2014 …………………………..

$749,000

REAGAN COMPANY

Analysis of Equipment Account

for 2014

Balance at January 1, 2014 ………………………………………..

$875,000

Cost of the new equipment acquired

Installation costs …………………………………………….

92,700

Balance at December 31, 2014 …………………………..

$967,700

(b) Items in the fact situation which were not used to determine the

answer to (a) above are as follows:

1. Interest imputed on common stock financing is not permitted by

GAAP and thus does not appear in any financial statement.

PROBLEM 10-2

(a) LOBO CORPORATION

Analysis of Land Account

2014

Balance at January 1, 2014 ……………………………………..

$ 300,000

Plant facility acquired from Mendota

LOBO CORPORATION

Analysis of Land Improvements Account

2014

Balance at January 1, 2014 ……………………………………..

$ 140,000

LOBO CORPORATION

Analysis of Buildings Account

2014

Balance at January 1, 2014 ……………………………………..

$1,100,000

LOBO CORPORATION

Analysis of Equipment Account

2014

Balance at January 1, 2014 ……………………………………..

$ 960,000

Cost of new equipment acquired

Sales taxes …………………………………………………….

PROBLEM 10-2 (Continued)

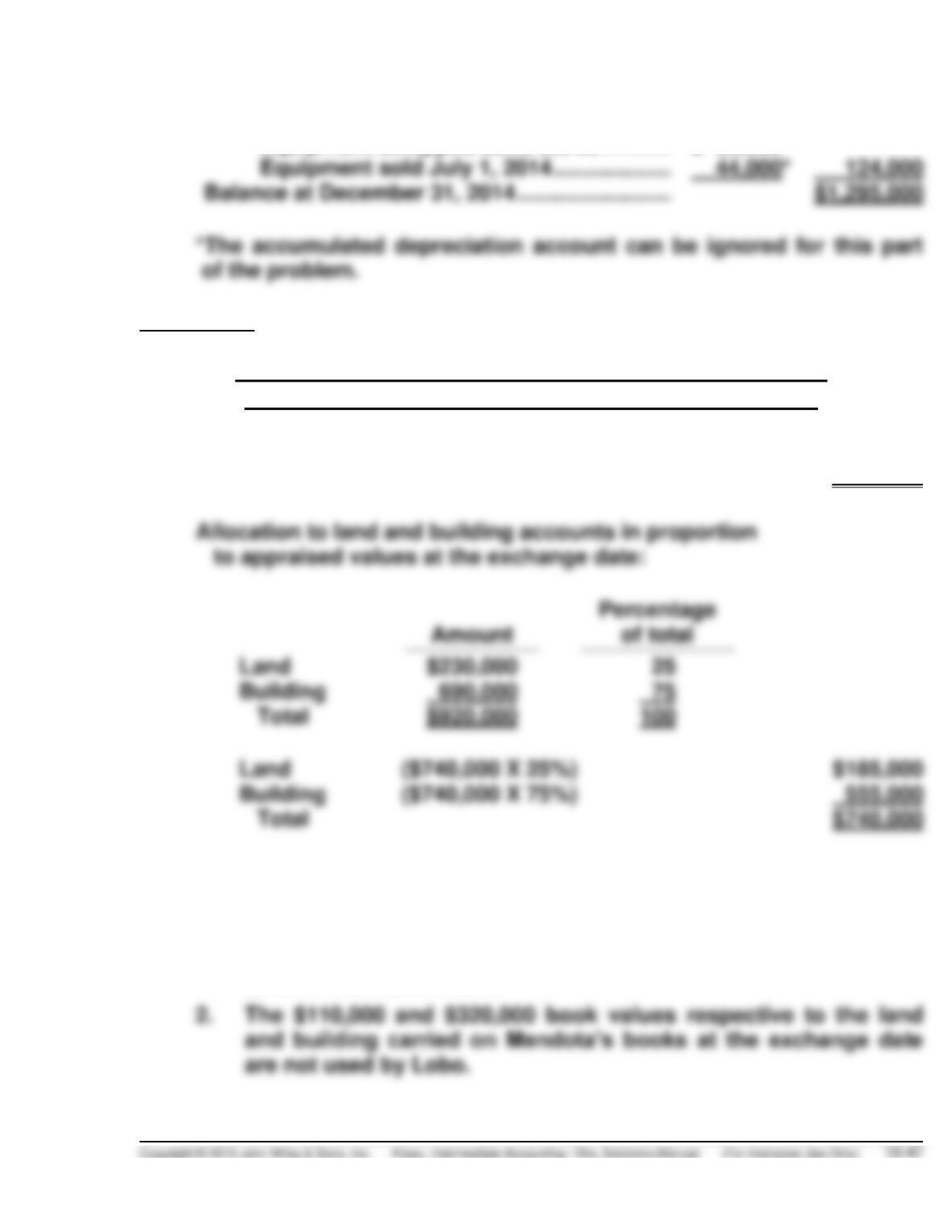

Deduct cost of equipment disposed of

Equipment scrapped June 30, 2014 ………………….

$ 80,000*

Schedule 1

Computation of Fair Value of Plant Facility Acquired from

Mendota Company and Allocation to Land and Building

20,000 shares of Lobo common stock at $37 quoted

market price on date of exchange (20,000 X $37)

$740,000

Building

Building

($740,000 X 75%)

(b) Items in the fact situation that were not used to determine the answer

to (a) above, are as follows:

1. The tract of land, which was acquired for $150,000 as a potential

future building site, should be included in Lobo’s balance sheet

as an investment in land.

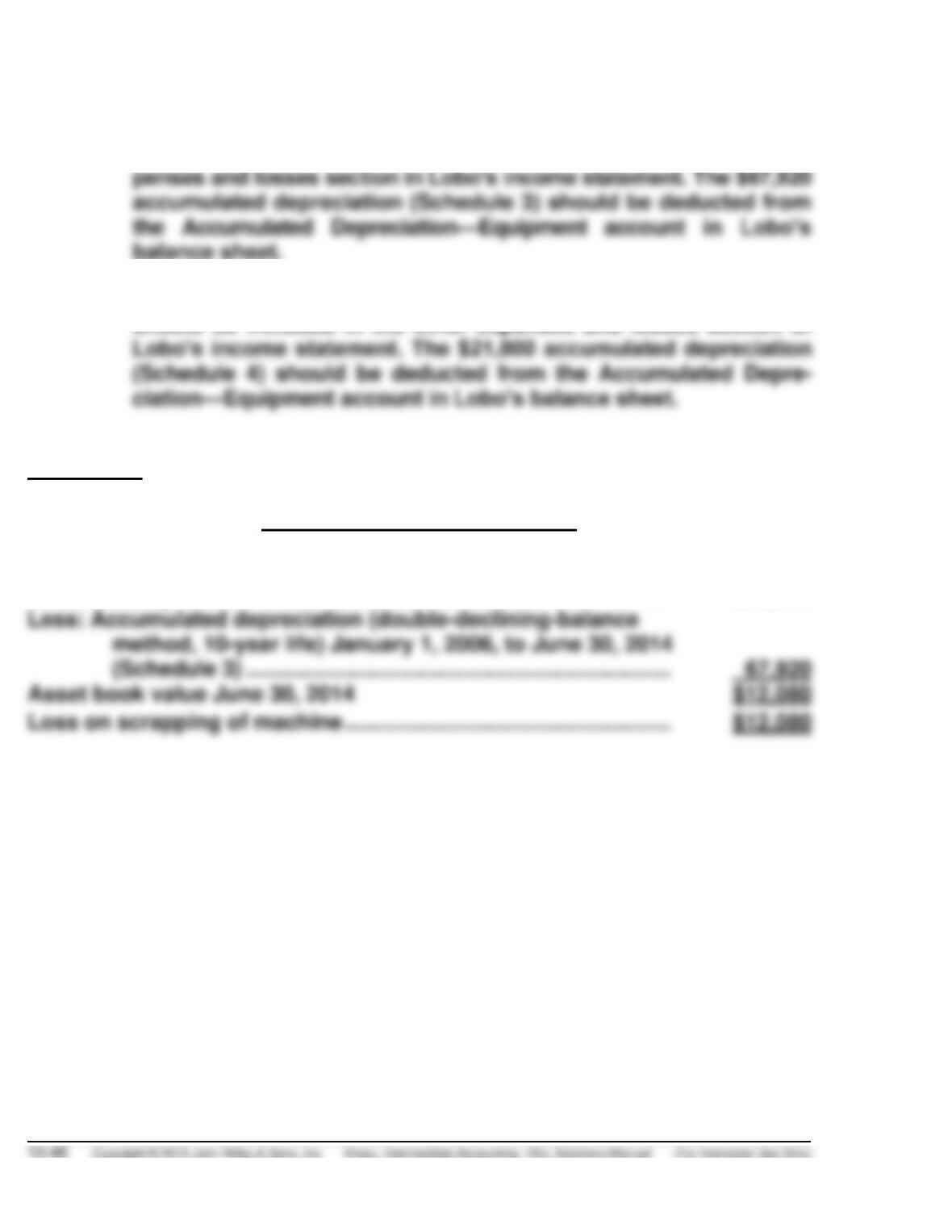

PROBLEM 10-2 (Continued)

3. The $12,080 loss (Schedule 2) incurred on the scrapping of a

machine on June 30, 2014, should be included in the other ex–

4. The $3,000 loss on sale of equipment on July 1, 2014 (Schedule 4)

should be included in the other expenses and losses section of

Schedule 2

Loss on Scrapping of Machine

June 30, 2014

Cost, January 1, 2006 …………………………………………………………..

$80,000

PROBLEM 10-2 (Continued)

Schedule 3

Accumulated Depreciation Using

Double-Declining-Balance Method

June 30, 2014

(Double-declining-balance rate is 20%)

Year

Book Value

at Beginning

of Year

Depreciation

Expense

Accumulated

Depreciation

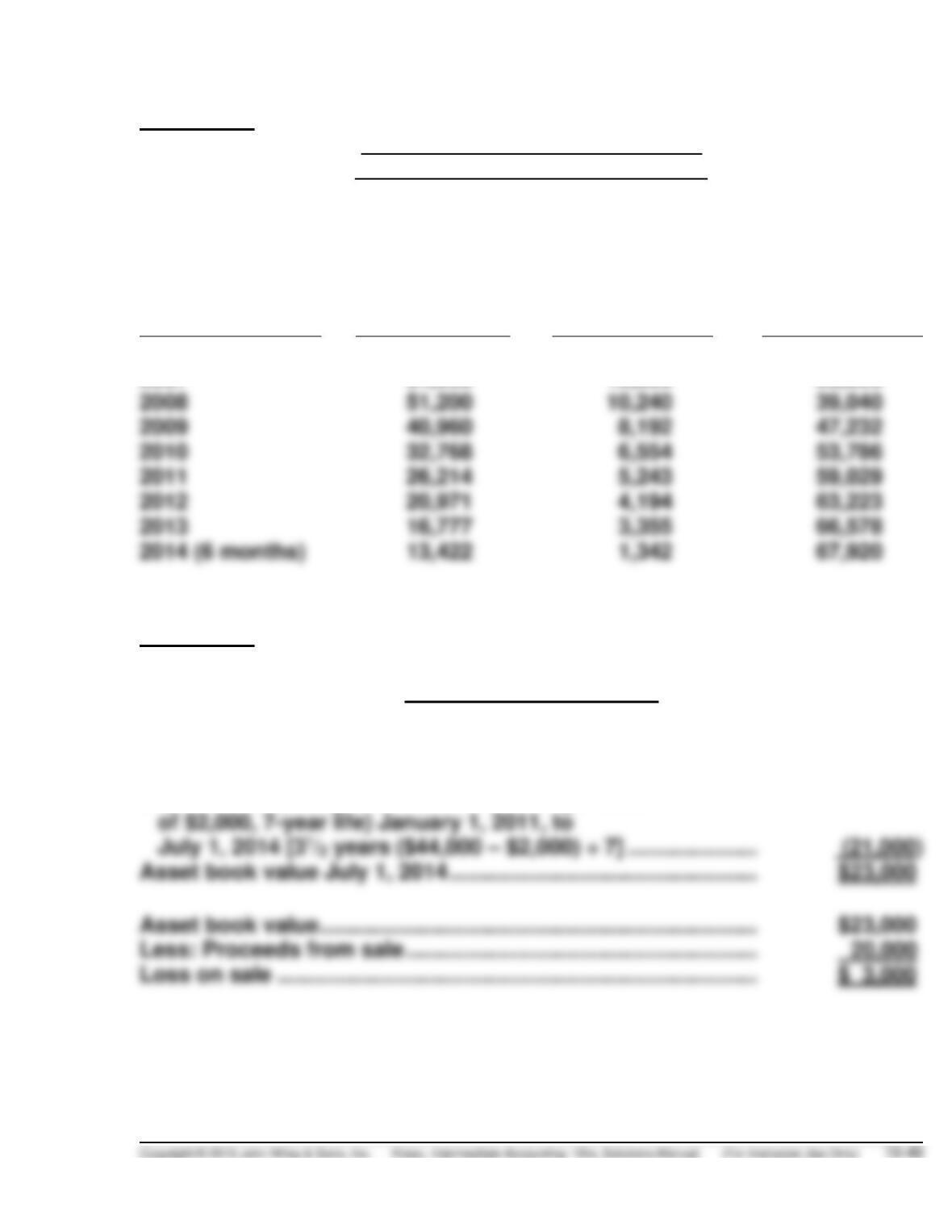

2006

$80,000

$16,000

$16,000

2007

64,000

12,800

28,800

2010

32,768

6,554

53,786

2013

16,777

3,355

66,578

Schedule 4

Loss on Sale of Machine

July 1, 2014

Cost, January 1, 2011 ……………………………………………………….

$44,000

Asset book value ……………………………………………………………..

$23,000

Less: Proceeds from sale …………………………..…………………….

20,000

Depreciation (straight-line method, salvage value

PROBLEM 10-3

(a)

1.

Land (Schedule A) ……………………………………….

188,700

Buildings (Schedule B) ………………………………..

136,250

Insurance Expense (6 months X $95) …………….

570

Prepaid Insurance (16 months X $95) ……………

Organization Expense ………………………………….

610

Retained Earnings ……………………………………….

Salaries and Wages Expense ……………………….

Land and Buildings ……………………………..

Schedule A

Amount Consists of:

Acquisition Cost

($80,000 + [800 X $117]) ……………………..

$173,600

Removal of Old Building ………………………

9,800

Legal Fees (Examination of title) …………..

1,300

Special Tax Assessment ………………………

4,000

Schedule B

Amount Consists of:

Legal Fees (Construction contract) ……….

$ 1,860

Construction Costs (First payment) ………

60,000

Construction Costs (Second payment) ….

Insurance (2 months)

([2,280 ÷ 24] = $95 X 2 = $190) …………….

4,200

Construction Costs (Final payment) ……..

30,000

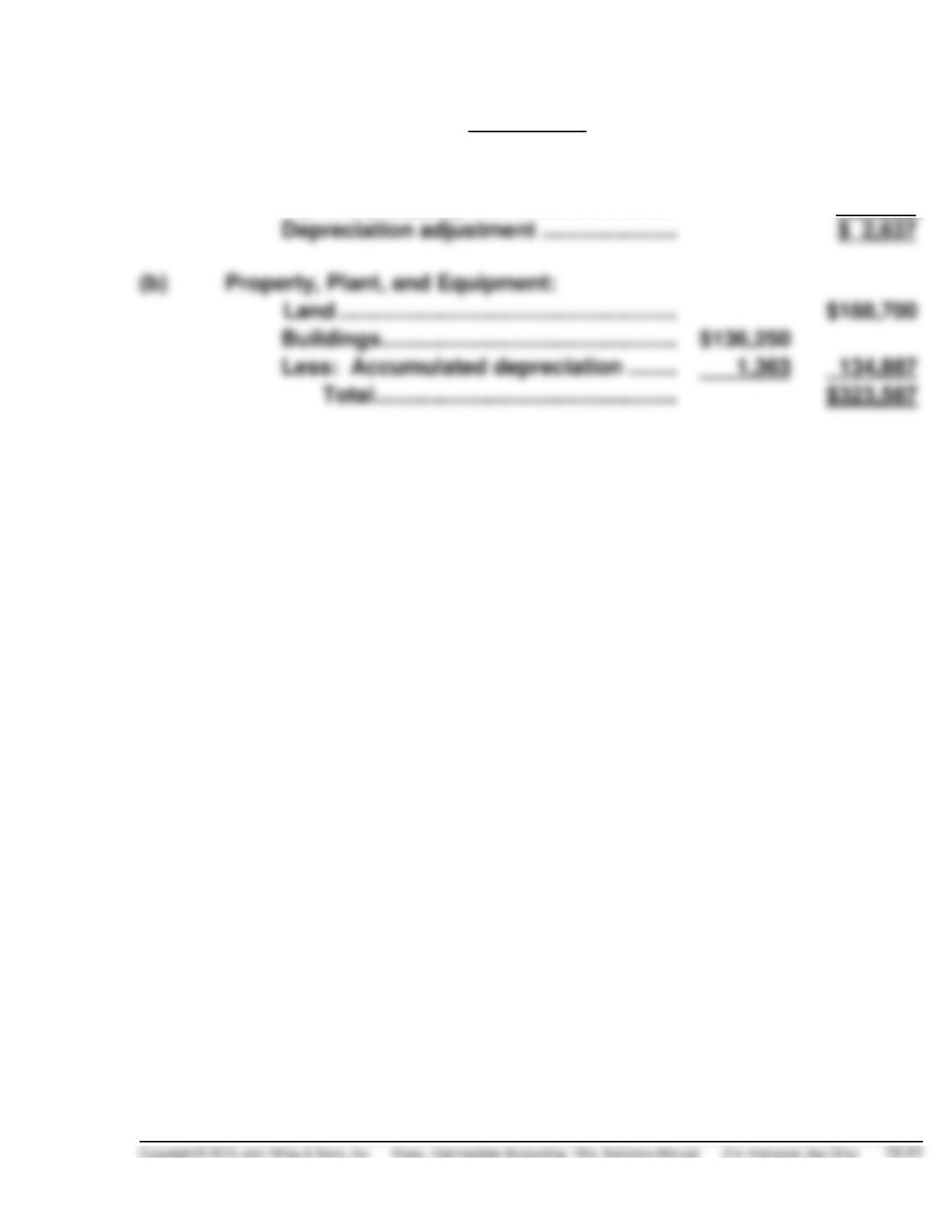

2.

Land and Buildings ……………………………………..

4,000

Depreciation Expense ………………………….

2,637

Accumulated Depreciation—Buildings ….

1,363

PROBLEM 10-3 (Continued)

Schedule C

Depreciation taken …………………………..

$ 4,000

Depreciation that should be taken

(1% X $136,250) …………………………….

(1,363)

PROBLEM 10-4

The following accounting treatment appears appropriate for these items:

Land—The loss on the condemnation of the land of $9,000 ($40,000 – $31,000)

should be reported as an extraordinary item on the income statement. If

Warehouse—The gain on the destruction of the warehouse should be reported

as an extraordinary item, assuming that it is unusual and infrequent. The

gain is computed as follows:

Insurance proceeds ………………………………..

$74,000

Deduct: Cost ………………………………………….

Some contend that a portion of this gain should be deferred because the

proceeds are reinvested in similar assets. We do not believe such an

approach should be permitted. Deferral of the gain in this situation is not

permitted under GAAP.

Machine—The recognized gain on the transaction would be computed as

follows:

Deduct: Book value of old machine

Cost …………………………………………………..

PROBLEM 10-4 (Continued)

This gain would probably be reported in other revenues and gains. It might

be reported as an unusual item if the company believes that such a situa–

tion occurs infrequently and if material. The cost of the new machine would

be capitalized at $4,550.

Fair value of new machine ……………………………………….

$6,300

PROBLEM 10-5

(a) BLAIR CORPORATION

Cost of Land (Site #101)

As of September 30, 2015

Cost of land and old building ………………………………..

$500,000

Legal fees …………………………………………………………….

Title insurance ……………………………………………………..

Removal of old building ………………………………………..

54,000

(b) BLAIR CORPORATION

Cost of Building

As of September 30, 2015

Fixed construction contract price ………………………….

$3,000,000

Plans, specifications, and blueprints ……………………..

Interest capitalized during 2014 (Schedule 1) …………

Interest capitalized during 2015 (Schedule 2) …………

Cost of building ………………………………………………..

Schedule 1

Interest Capitalized During 2014 and 2015

Weighted-average

accumulated construction

expenditures

X

Interest rate

=

Interest to be

capitalized

2014:

$1,300,000

X

10%

=

$130,000*

2015:

$1,900,000

X

10%

=

PROBLEM 10-6

INTEREST CAPITALIZATION

Balance in the Land Account

Purchase Price ……………………………………………………………..

$139,000

Surveying Costs ……………………………………………………………

2,000

Title Insurance Policy ……………………………………………………

4,000

Salvage ………………………………………………………………………..

Expenditures (2014)

Weighted—Average

Accumulated Expenditures

Date

Amount

Fraction

1-Dec

$147,000

1/12

$12,250

1-Dec

30,000

1/12

2,500

Interest Capitalized for 2014

Weighted—Average

Accumulated Expenditures

Interest

Rate

Amount

Capitalizable

PROBLEM 10-6 (Continued)

Expenditures (2015)

Fraction

Weighted

Expenditure

Date

Amount

1-Jan

$180,000

6/12

$ 90,000

1-Mar

4/12

80,000

Interest Capitalized for 2015

Weighted-

Average

Expenditure

Interest

Rate

Amount

Capitalizable

$225,600

(a) Balance in Land Account—2014 and 2015 …….. 147,000

(b) Balance in Building—2014 ……………………………. 34,200*

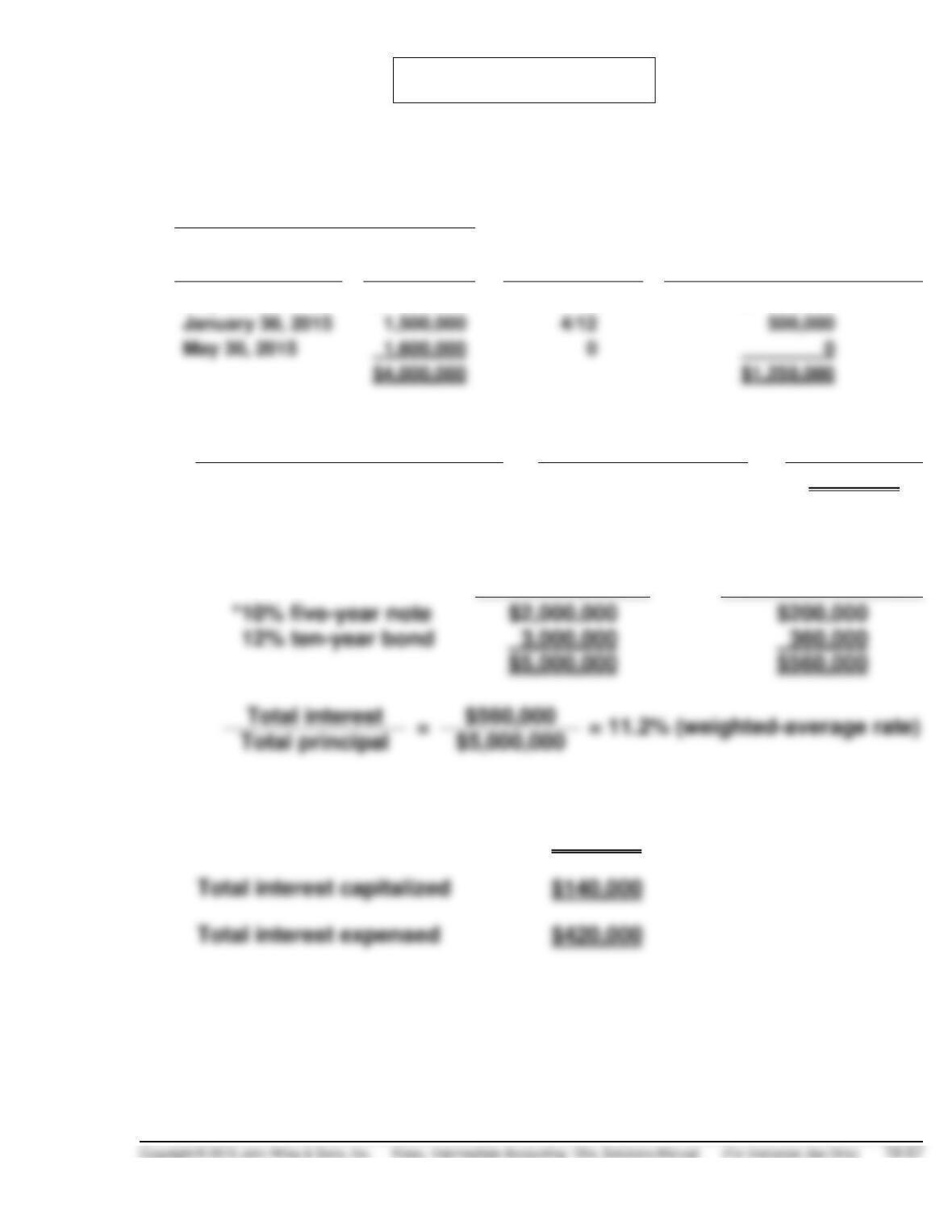

PROBLEM 10-7

(a) Computation of Weighted-Average Accumulated Expenditures

Expenditures

Date

Amount

X

Capitalization

Period

=

Weighted-Average

Accumulated Expenditures

July 30, 2014

$ 900,000

10/12

$ 750,000

January 30, 2015

May 30, 2015

0

0

(b)

Weighted-Average

Accumulated Expenditures

X

Weighted-Average

Interest Rate

=

Avoidable

interest

$1,250,000

11.2%*

$140,000

Loans Outstanding During Construction Period

Principal

Actual Interest

(c) (1) and (2)

Total actual interest cost

$560,000

Total interest capitalized

$140,000

Total interest expensed

$420,000

PROBLEM 10-8

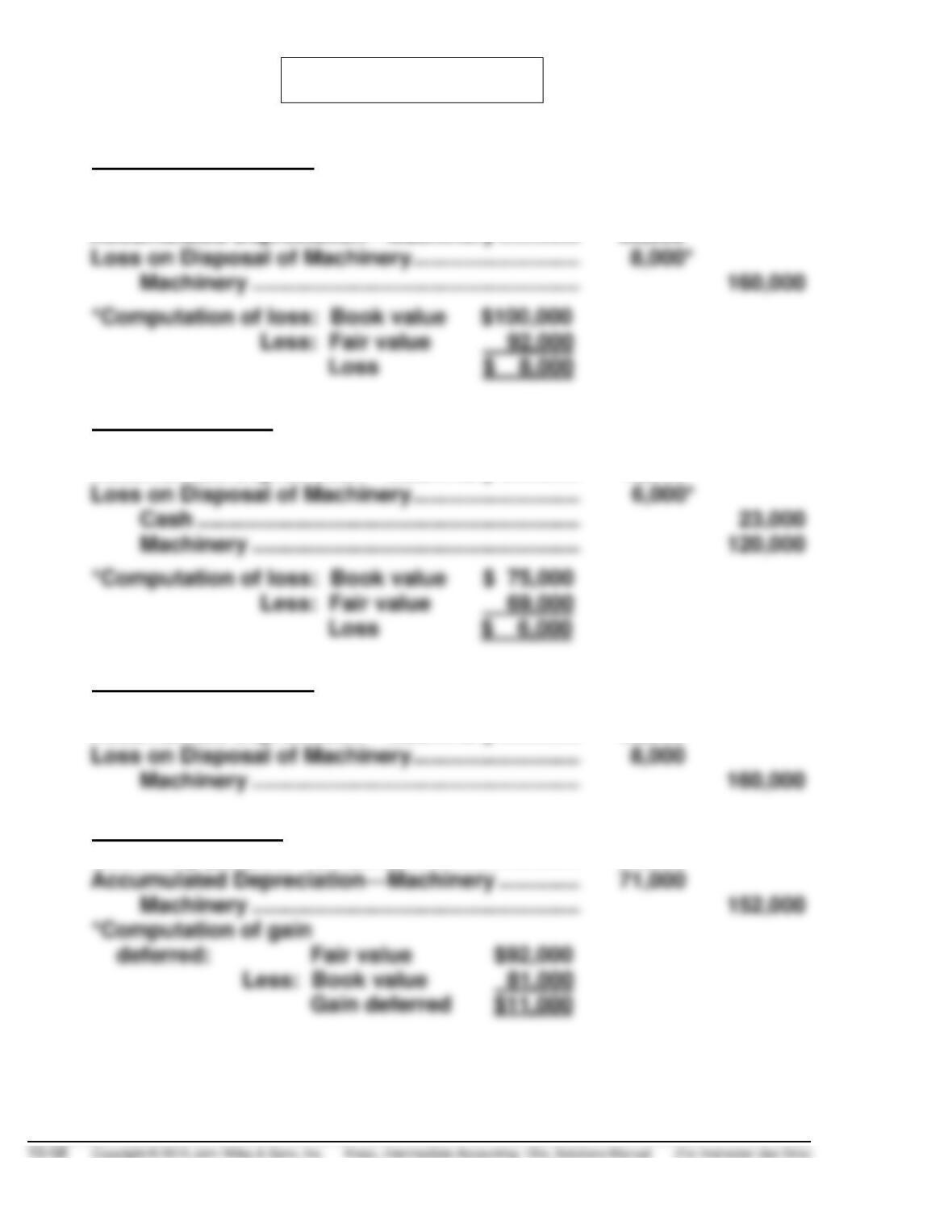

1.

Holyfield Corporation

Cash ………………………………………………………………

23,000

Machinery ………………………………………………………

69,000

Accumulated Depreciation—Machinery ……………

60,000

Loss on Disposal of Machinery ………………………..

Machinery ……………………………………………….

*Computation of loss: Book value

Less: Fair value

Dorsett Company

Machinery ………………………………………………………

92,000

Accumulated Depreciation—Machinery ……………

45,000

Loss on Disposal of Machinery ………………………..

Cash ……………………………………………………….

Machinery ……………………………………………….

*Computation of loss: Book value

Less: Fair value

2.

Holyfield Corporation

Machinery ………………………………………………………

92,000

Accumulated Depreciation—Machinery ……………

60,000

Loss on Disposal of Machinery ………………………..

Machinery ……………………………………………….

Winston Company

Machinery ($92,000 – $11,000) …………………………

81,000*

Accumulated Depreciation—Machinery ……………

71,000

Machinery ……………………………………………….

PROBLEM 10-8 (Continued)

3.

Holyfield Corporation

Machinery ………………………………………………………

95,000

60,000

Machinery ……………………………………………….

160,000

Cash ……………………………………………………….

Liston Company

Machinery ………………………………………………………

92,000

Accumulated Depreciation—Machinery ……………

75,000

Cash ………………………………………………………………

3,000

Machinery ……………………………………………….

160,000

*Fair value

$ 95,000

Less: Book value

85,000

4.

Holyfield Corporation

Machinery ………………………………………………………

185,000

Accumulated Depreciation—Machinery ……………

60,000

Loss on Disposal of Machinery ……………………….

8,000

Machinery ……………………………………………….

Greeley Company

93,000

Inventory ……………………………………………………….

Cost of Goods Sold …………………………………………

Inventory …………………………..…………………….

PROBLEM 10-9

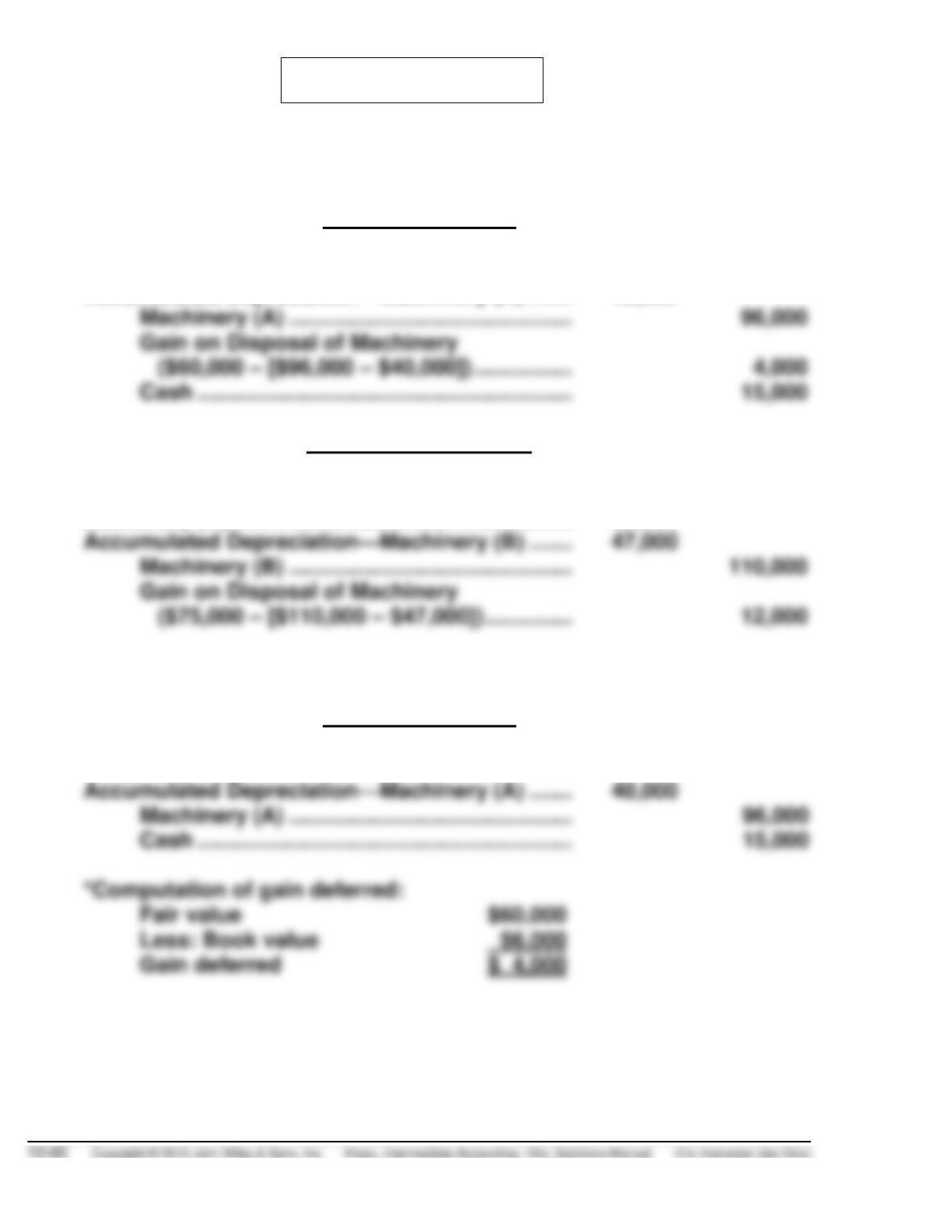

(a) Exchange has commercial substance:

Hyde, Inc.’s Books

Machinery (B)…………………………………………………..

75,000

Accumulated Depreciation—Machinery (A) ……….

40,000

Gain on Disposal of Machinery

($60,000 – [$96,000 – $40,000]) ……………….

Wiggins, Inc.’s Books

Cash ……………………………………………………………….

15,000

Machinery (A)…………………………………………………..

60,000

Accumulated Depreciation—Machinery (B) ……….

Machinery (B) ………………………………………….

Gain on Disposal of Machinery

($75,000 – [$110,000 – $47,000]) ……………..

(b) Exchange lacks commercial substance:

Hyde, Inc.’s Books

Machinery (B) ($75,000 – $4,000) ……………………….

71,000*

Accumulated Depreciation—Machinery (A) ……….

40,000

Machinery (A) ………………………………………….

*Computation of gain deferred:

Less: Book value