PROBLEM 16-1 (Continued)

Calculations:

Common Stock

Paid-in Capital

in Excess of Par

At beginning of year …………………..

300,000 shares

$ 600,000

From stock rights (entry #3) ……….

From stock warrants (entry #4) …..

Total …………………………………..

320,100 shares

$1,123,800

PROBLEM 16-2

(a) Entries at August 1, 2015

Bonds Payable ………………………………………………… 250,000

Discount on Bonds Payable (Schedule 1) …… 4,815*

*($54,000 X 1/10) X (107/120)

**($250,000 – $4,815) – $200,000

Interest Payable ………………………………………………. 2,500

(b) Entries at August 31, 2015

Interest Expense ……………………………………………… 405*

Discount on Bonds Payable (Schedule 1) …………. 405

*($54,000 X 90%) X (1/120)

Interest Expense ……………………………………………… 22,500

(c) Entries at December 31, 2015

(Same as August 31, 2015, and the following closing entry)

Income Summary…………………………………………….. 292,675

PROBLEM 16-2 (Continued)

Schedule 1

Monthly Amortization Schedule

Unamortized discount on bonds payable:

Amount to be amortized over 120 months ………………………………. $54,000

Schedule 2

Interest Expense Schedule

Amortization of bond discount charged to bond interest expense in 2015

would be as follows:

Interest on Bonds:

12% on $2,500,000 …………………………………………………………………. $300,000

Amount per month ($300,000 ÷ 12) …………………………………………. $ 25,000

Total interest

Amortization of discount ……………… $ 5,175

PROBLEM 16-3

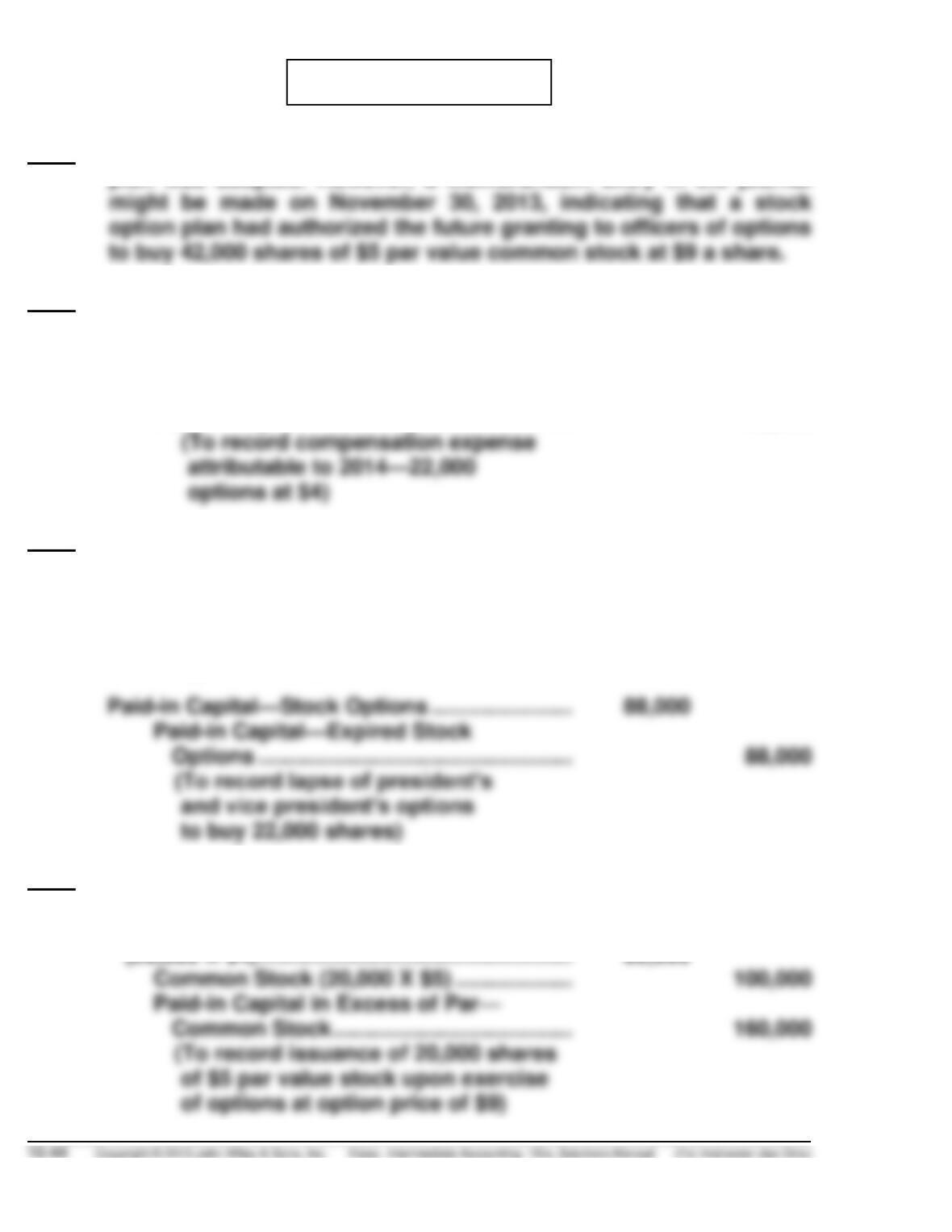

2013 No journal entry would be recorded at the time the stock option

plan was adopted. However, a memorandum entry in the journal

2014 January 2

No entry

December 31

Compensation Expense …………………………….. 88,000

Paid-in Capital—Stock Options …………… 88,000

2015 December 31

Compensation Expense …………………………….. 80,000

Paid-in Capital—Stock Options …………… 80,000

(To record compensation expense

attributable to 2015—20,000

options at $4)

2016 December 31

Cash (20,000 X $9) …………………………………….. 180,000

Paid-in Capital—Stock Options

(20,000 X $4) …………………………………………… 80,000

PROBLEM 16-4

(a) 1/1/14 No entry

12/31/14 Compensation Expense ($6 X 5,000 ÷ 5) …… 6,000

Paid-in Capital—Stock Options ………… 6,000

(b) 1/1/14 Unearned Compensation ($40 X 700) ……….. 28,000

(c) No change for part (a), unless the fair value of the options change.

For part (b):

1/10/14 Unearned Compensation ($45 X 700) ……….. 31,500

(d) Numbers (1) substantially all employees may participate; (2) The

discount from market is small (less than 5%); and (3) The plan offers

PROBLEM 16-5

The computation of Fitzgerald Pharmaceutical Industries’ basic earnings

per share and the diluted earnings per share for the fiscal year ended June

30, 2014, are shown below.

1Preferred dividend = .06 X $1,250,000

= $75,000

2Use “if converted” method for 8% bonds

Adjustment for interest expense (net of tax)

($5,000,000 X .08 X .6) ……………………………………… $240,000

PROBLEM 16-5 (Continued)

3Shares assumed to be issued if converted

$5,000,000 ÷ $1,000/bond X 50 shares …………………… 250,000

PROBLEM 16-6

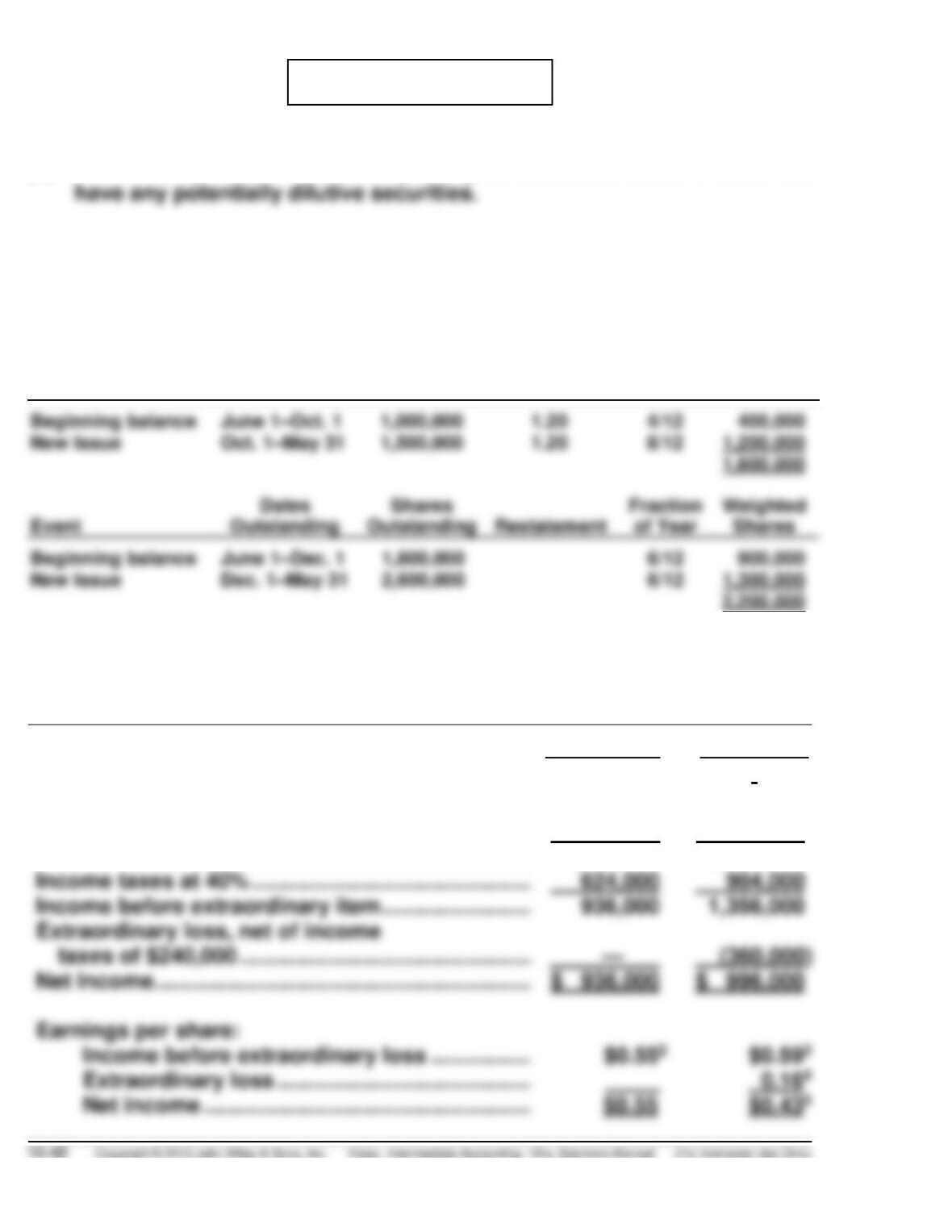

(a) Melton Corporation has a simple capital structure since it does not

(b) The weighted-average number of shares outstanding that Melton

Corporation would use in calculating earnings per share for the fiscal

years ended May 31, 2014, and May 31, 2015, is 1,600,000 and 2,200,000

respectively, calculated as follows:

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

(c) MELTON CORPORATION

Comparative Income Statement

For Fiscal Years Ended May 31, 2014 and 2015

2014

2015

Income from operations ……………………………………

$1,800,000

$2,500,000

Interest expense1 ……………………………………………..

240,000

240,000

Income before taxes …………………………………………

1,560,000

2,260,000

Income before extraordinary item ………………………

1,356,000

Extraordinary loss, net of income

Net income ……………………………………………………….

$ 936,000

$ 996,000

Income before extraordinary loss ……………….

PROBLEM 16-6 (Continued)

1Interest expense = $2,400,000 X .10

= $240,000

($936,000 – $60,000*)

=

*Preferred dividends = (No. of Shares X Par Value X Dividend %)

= (20,000 X $50 X .06)

= $60,000 per year

3Earnings per share

=

=

$0.59 per share

Weighted-Average Number of Shares Outstanding

=

$0.16 per share

5Earnings per share

=

Net Income – Preferred Dividends

Weighted-Average Number of Shares Outstanding

=

$996,000 – $60,000

2,200,000

=

$0.43

PROBLEM 16-7

(a) The number of shares used to compute basic earnings per share is

4,951,000, as calculated below.

Event

Dates

Outstanding

Shares

Outstanding

Restatement

Fraction

of Year

Weighted

Shares

Beginning Balance,

including 5% stock

dividend

Jan. 1–Apr. 1

2,100,000

2.0

3/12

1,050,000

Conversion of

1,260,000

Issued shares for

building

1,335,000

(b) The number of shares used to compute diluted earnings per share is

5,791,000, as shown below.

Number of shares to compute

basic earnings per share …………………………... 4,951,000

(c) The adjusted net income to be used as the numerator in the basic

earnings per share calculation for the year ended December 31, 2015, is

$10,350,000, as computed below.

After-tax net income ……………………………………. $11,550,000

PROBLEM 16-8

(a)

Basic EPS

=

$1,200,000 – ($4,000,000 X .06)

600,000*

=

$1.60 per share

*$6,000,000 ÷ $10

(b)

Diluted EPS

=

(Net income – Preferred dividends) + Interest

savings (net of tax)

Weighted-average number of shares outstanding +

Potentially dilutive common shares

=

=

=

aPreferred stock is not included since conversion would be antidilutive.

That is, conversion of the preferred stock increases the numerator

$240,000 ($4,000,000 X .06) and the denominator 120,000 shares

[(4,000,000 ÷ 100) X 3] as shown in the following:

=

$1.61 per share > $1.54; therefore

PROBLEM 16-8 (Continued)

cMarket price – Option price

X Number of options = incremental shares

Market price

Note to instructor: This problem can be used to apply the procedures in

Appendix 17B for analysis of multiple dilutive securities.

First, compute the dilutive effect for each security and rank from smallest

to largest:

PROBLEM 16-9

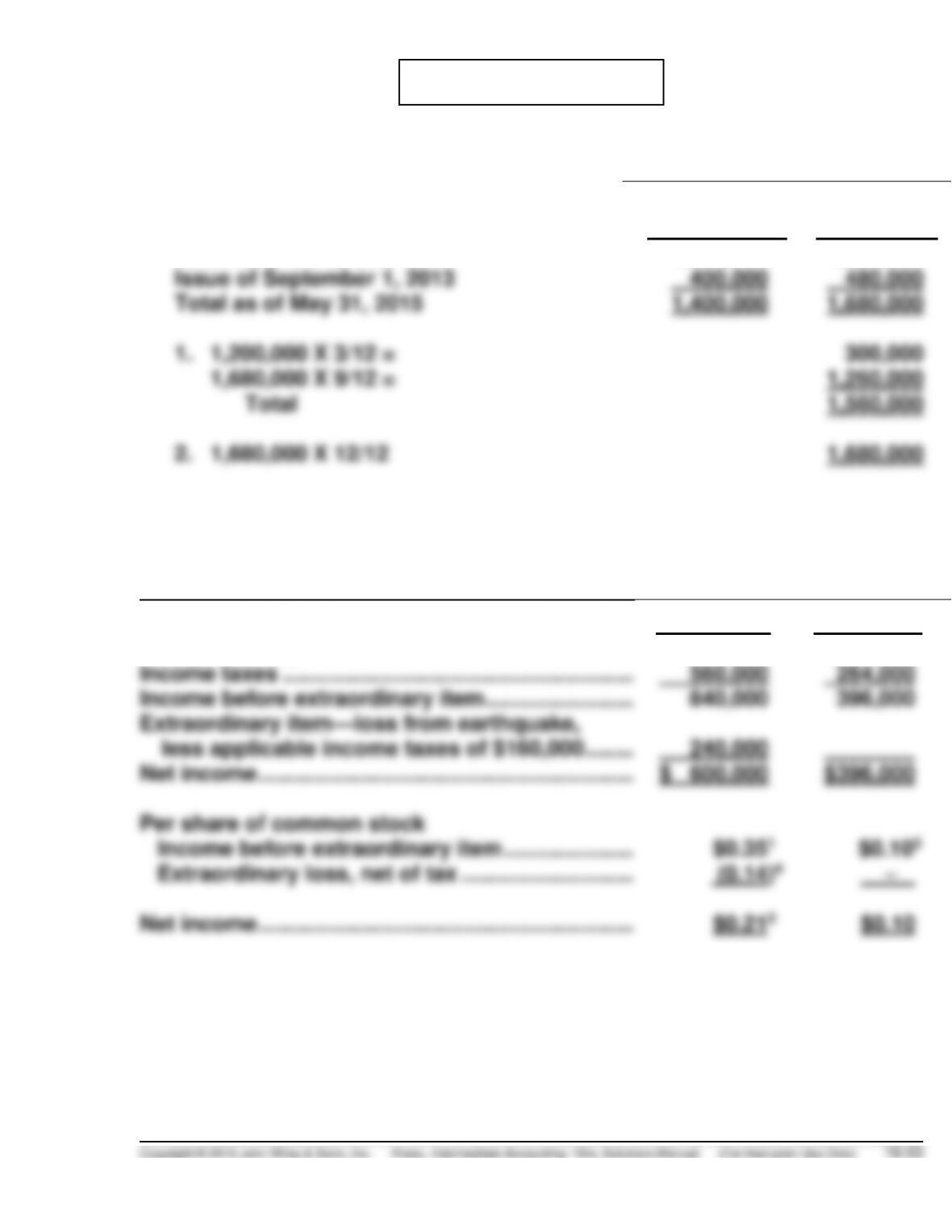

(a)

Weighted-Average Shares

Before Stock

Dividend

After Stock

Dividend

Total as of June 1, 2013

1,000,000

1,200,000

Issue of September 1, 2013

400,000

Total as of May 31, 2015

1,400,000

Total

(b) AGASSI CORPORATION

Comparative Income Statement

For the Years Ended May 31, 2015 and 2014

2015

2014

Income from operations before income taxes ….

$1,400,000

$660,000

Income taxes …………………………………………………

560,000

Net income …………………………………………………….

$ 600,000

Per share of common stock

Income before extraordinary item …………………

Extraordinary loss, net of tax ……………………….

Net income …………………………………………………….

PROBLEM 16-9 (Continued)

EPS calculations =

Net income – Preferred dividends

Weighted-average common shares

Preferred dividends = 40,000 X $100 X .06 = $240,000

(c) 1. A corporation’s capital structure is regarded as simple if it

consists only of common stock or includes no potentially dilutive

2. A corporation having a complex capital structure would be

required to make a dual presentation of earnings per share; i.e.,

TIME AND PURPOSE OF CONCEPTS FOR ANALYSIS

CA 16-1 (Time 20–25 minutes)

Purpose—to provide the student with an understanding of the underlying rationale behind the

CA 16-2 (Time 15–20 minutes)

CA 16-3 (Time 15–20 minutes)

Purpose—to provide the student with an understanding of the proper accounting and conceptual merits

CA 16-4 (Time 25–35 minutes)

CA 16-5 (Time 25–35 minutes)

Purpose—to provide the student with an understanding of how earnings per share is affected by

preferred dividends and convertible debt. The student is required to explain how preferred dividends

and convertible debt are handled for EPS computations. The student is also required to explain when

the “treasury stock method” is applicable in EPS computations.

CA 16-6 (Time 25–35 minutes)

SOLUTIONS TO CONCEPTS FOR ANALYSIS

CA 16-1

(a) (1) When the debt instrument and the option to acquire common stock are inseparable, as in

the case of convertible bonds, the entire proceeds of the bond issue should be allocated to

the debt and the related premium or discount accounts.

When the debt and the warrants are separable, the proceeds of their sale should be

(2) In the case of convertible debt there are two principal reasons why all the proceeds should

be ascribed to the debt. First, the option is inseparable from the debt. The investor in such

(3) Arguments have been advanced that accounting for convertible debt should be the same as

for debt issued with detachable stock purchase warrants. Convertible debt has features of

debt and stockholders’ equity, and separate recognition should be given to those

characteristics at the time of issuance. Difficulties encountered in separating the relative

values of the features are not insurmountable and, in any case, should not result in a

(b) Incremental Cash……………………………………………………………….. 20,040,000

Discount on Bonds Payable ($18,000,000 X 22%)…………………… 3,960,000

Bonds Payable ……………………………………………………………. 18,000,000

Paid-in Capital—Stock Warrants ……………………………………. 6,000,000

CA 16-2

(a) Devers recognizes that altering the estimate will benefit Adkins and other executive officers of the

CA 16-3

(a) 1. The objective of issuing warrants to existing stockholders on a pro-rata basis is to raise new

equity capital. This method of raising equity capital may be used because of preemptive

rights on the part of a company’s stockholders and also because it is likely to be less

expensive than a public offering.

2. The purpose of issuing stock warrants to certain key employees, usually in the form of a

non-qualified stock option plan, is to increase their interest in the long-term growth and

3. Warrants to purchase shares of its common stock may be issued to purchasers of a

company’s bonds in order to stimulate the sale of the bonds by increasing their speculative

appeal and aiding in overcoming the objection that rising price levels cause money invested

2. Warrants may be offered to key employees below, at, or above the market price of the stock

on the day the rights are granted except for incentive stock-option plans. If a stock-option

plan is to provide a strong incentive, warrants that can be exercised shortly after they are

3. Income tax laws impose no restrictions on the exercise price of warrants issued to purchasers

of a company’s bonds. The exercise price may be above, equal to, or below the current

CA 16-3 (Continued)

(c) 1. Financial statement information concerning outstanding stock warrants issued to a

2. Financial statement information concerning stock warrants issued to key employees should

include the following: status of these plans at the end of each period presented, including

3. Financial statement disclosure of outstanding stock warrants that have been issued to

CA 16-4

(a) In 2004, FASB issued an accounting standard related to stock compensation plans.

Generally, the rule indicates that employee stock options be treated like all other types of

compensation and that their value be included in financial statements as part of the costs of

employee services. The rule requires that all types of stock options be recognized as

(b) According to Ciesielski’s commentary, the bill in Congress would only record expense for the

options granted to the top five executives. They also are recommending that the SEC conduct

(c) Here is an excerpt from a presentation given by Dennis Beresford on the concept of neutrality,

which says it well.

The FASB often hears that it should take a broader view, that it must consider the economic

consequences of a new accounting standard. The FASB should not act, critics maintain, if a new

accounting standard would have undesirable economic consequences. We have been told that

providing retiree health care or creating employee incentives.

CA 16-4 (Continued)

There is a common element in those assertions. The goals are desirable but the means require

that the Board abandon neutrality and establish reporting standards that conceal the financial

impact of certain transactions from those who use financial statements. Costs of transactions

exist whether or not the FASB mandates their recognition in financial statements. For example,

Many observers believe that the effect was to delay action and hide the true dimensions of the

problem. The public interest is best served by neutral accounting standards that inform policy

rather than promote it. Stated simply, truth in accounting is always good policy.

Neutrality does not mean that accounting should not influence human behavior. We expect that

changes in financial reporting will have economic consequences, just as economic

Indeed, most people are repelled by the notion that some “big brother,” whether

government or private, would tamper with scales or speedometers surreptitiously to

CA 16-5

(a) Dividends on outstanding preferred stock must be subtracted from net income or added to net loss

for the period before computing EPS on the common shares. This generalization will be modified

by the various features and different requirements preferred stock may have with respect to

CA 16-5 (Continued)

(b) When options and warrants to buy common stock are outstanding and their exercise price (i.e.,

proceeds the corporation would derive from issuance of common stock pursuant to the warrants

and options) is less than the average price at which the company could acquire its outstanding

shares as treasury stock, the treasury stock method is generally applicable. In these

circumstances, existence of the options and warrants would be dilutive. However, if the exercise

(c) In arriving at the calculation of diluted EPS where convertible debentures are assumed to be

converted, their interest (net of tax) is added back to net income as the numerator element of the

EPS calculation while the weighted-average number of shares of common stock into which they

would be convertible is added to the shares outstanding to arrive at the denominator element of

the calculation.

CA 16-6

Dear Mr. Dolan:

I hope that the following brief explanation helps you understand why your warrants were not included in

Rhode’s earnings per share calculations.

Earnings per share (EPS) provides income statement users a quick assessment of the earnings that

In order not to mislead users of financial information, the accounting profession insists that EPS

calculations be transparent. Thus, a security which might dilute EPS must be figured into EPS

calculations as though it had been converted into common stock. Basic EPS assumes a weighted-

average of common stock outstanding while diluted EPS assumes that any potentially dilutive security

has been converted.