CHAPTER 4

Income Statement and Related Information

ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC)

Topics

Questions

Brief

Exercises

Exercises

Problems

Concepts

for Analysis

1.

Income measurement

concepts.

1, 2, 3, 4, 5,

6, 7, 8, 9, 10,

18, 22, 23, 30,

33, 34, 35

2, 3, 4, 6

2.

income from balance

sheets and selected

accounts.

Computation of net

1

1, 2, 3, 8

3.

statements; earnings

per share.

25, 26

10, 11, 13,

17

Single-step income

11, 19,

1, 2, 8

4, 5, 7, 8,

2, 3, 4, 5

1, 5

4.

Multiple-step income

statements.

12, 17,

19, 20

3, 4

5, 6, 7, 9

1, 4

5.

Extraordinary items;

accounting changes;

13, 14, 15,

16, 22, 29,

4, 5, 6, 7

6, 8, 10, 11,

13, 14

3, 5, 6, 7

1, 2, 4, 5, 6

6.

Retained earnings

statement.

32

9, 10, 11

9, 12,

16, 17

1, 2, 4, 5, 6

7.

Intraperiod tax

allocation.

21, 24, 27,

28, 29

9, 11, 13,

14, 17

3, 5, 7

8.

Comprehensive

income.

36

11

15, 16, 17

7

9.

Disposal of a

component (discon-

tinued operations).

1, 3, 6, 7

ASSIGNMENT CLASSIFICATION TABLE (BY LEARNING OBJECTIVE)

Learning Objectives

Questions

Brief

Exercises

Exercises

Problems

Concepts

for

Analysis

1. Understand the uses and

limitations

of an income statement.

1, 2, 6, 7,

9

CA4-1,

CA4-2,

CA4-3

format of the income

statement.

6, 7

CA4-6

2. Describe the content and

5, 8, 10

4, 5

1, 2, 3, 4, 5,

CA4-5,

statement.

19, 20, 17

9, 11, 15,

17

7

3. Prepare an income

8, 11, 12,

1, 2, 3, 4, 5

4, 5, 6, 7, 8,

1, 2, 3, 4, 5,

CA4-6

4. Explain how to report

various income items.

3, 4, 13,

21, 22, 23,

24, 27, 28,

29, 30, 31,

33, 17

4, 5

2, 3, 6, 8, 9,

11, 17

1, 3, 4,

5, 6, 7

CA4-4

earnings per share

information.

10, 11, 13,

14, 17

5, 7

5. Identify where to report

25, 26

8

6, 7, 8, 9,

1, 2, 3, 4,

CA4-4

accounting changes, and

errors.

18

6. Understand the reporting of

14, 15, 16,

6, 7, 10

14

4, 5, 6, 7

CA4-2

7. Prepare a retained earnings

statement.

32

9, 10

9, 12, 16,

17

1, 2, 4, 5, 6

CA4-6

8. Explain how to report other

comprehensive income.

34, 35, 36,

37

11

15, 16, 17

CA4-7

ASSIGNMENT CHARACTERISTICS TABLE

Item

Description

Level of

Difficulty

Time

(minutes)

E4-1

Computation of net income.

Simple

18–20

E4-2

Compute income measures.

Simple

10–15

E4-3

Income statement items.

Simple

25–35

E4-4

Single-step income statement.

Moderate

20–25

E4-5

Multiple-step and single-step.

Simple

30–35

E4-6

Multiple-step and extraordinary items.

Moderate

30–35

E4-7

Multiple-step and single-step.

Moderate

30–40

E4-8

Income statement, EPS.

Simple

15–20

E4-9

Multiple-step statement with retained earnings.

Simple

30–35

E4–10

Earnings per share.

Simple

20–25

E4–11

Condensed income statement—periodic inventory

method.

Moderate

20–25

E4–12

Retained earnings statement.

Simple

20–25

E4–13

Earnings per share.

Moderate

15–20

E4–14

Change in accounting principle.

Moderate

15–20

E4–15

Comprehensive income.

Simple

15–20

E4–16

Comprehensive income.

Moderate

15–20

E4–17

Various reporting formats.

Moderate

30–35

P4-1

Multiple-step income, retained earnings.

Moderate

30–35

P4-2

Single-step income, retained earnings, periodic inventory.

Simple

25–30

P4-3

Irregular items.

Moderate

30–40

P4-4

Multiple- and single-step income, retained earnings.

Moderate

45–55

P4-5

Irregular items.

Moderate

20–25

P4-6

Retained earnings statement, prior period adjustment.

Moderate

25–35

P4-7

Income statement, irregular items.

Moderate

25–35

CA4-1

Identification of income statement deficiencies.

Simple

20–25

CA4-2

Earnings management.

Moderate

20–25

CA4-3

Earnings management.

Simple

15–20

CA4-4

Income reporting items.

Moderate

30–35

Classification of income statement items.

Moderate

20–25

CA4-7

Comprehensive income.

Simple

10–15

SOLUTIONS TO CODIFICATION EXERCISES

CE4-1

According to the Glossary:

(a) A change in accounting estimate is a change that has the effect of adjusting the carrying amount

of an existing asset or liability or altering the subsequent accounting for existing or future assets or

with assets and liabilities.

(b) A change in accounting principle reflects a change from one generally accepted accounting

principle to another generally accepted accounting principle when there are two or more generally

(c) Comprehensive Income is defined as the change in equity (net assets) of a business during a

period from transactions and other events and circumstances from nonowner sources. It includes

all changes in equity during a period except those resulting from investments by owners and

distributions to owners.

CE4-2

The master glossary provides the term “Unusual Nature”, a link from which yields the following:

Glossary Term Usage

The glossary term is used in the following locations.

Unusual Nature

• 225 Income Statement > 20 Extraordinary and Unusual Items > 45 Other Presentation

45-2 Extraordinary items are events and transactions that are distinguished by their unusual nature

and by the infrequency of their occurrence. Thus, both of the following criteria shall be met to

classify an event or transaction as an extraordinary item:

a. Unusual nature. The underlying event or transaction should possess a high degree of

CE4-2 (Continued)

b. Infrequency of occurrence. The underlying event or transaction should be of a type that

would not reasonably be expected to recur in the foreseeable future, taking into account the

CE4-3

Entering “extraordinary item” and “interim” into the search window, yields the following guidance (FASB

ASC 225-20–50-4):

Interim Reporting

50-4 As indicated in paragraph FASB ASC 270–10–50-5, extraordinary items shall be disclosed

separately and included in the determination of net income for the interim period in which they

occur. In determining materiality, extraordinary items shall be related to the estimated income for

CE4-4

Entering “effect of preferred stock” in the search window yields the following link (FASB ASC 260–10–

S55): 260 Earnings per Share > 10 Overall > S55 Implementation Guidance and Illustrations.

General

Effect of Preferred Stock Dividends and Accretion of Carrying Amount of Preferred Stock on Earnings

S99-5 The following is the text of SAB Topic 6.B, Accounting Series Release 280—General Revision Of

Regulation S-X: Income Or Loss Applicable To Common Stock.

Facts: A registrant has various classes of preferred stock. Dividends on those preferred stocks

and accretions of their carrying amounts cause income applicable to common stock to be less

than reported net income.

Question: In ASR 280, the Commission stated that although it had determined not to mandate

CE4-4 (Continued)

Interpretive Response: Income or loss applicable to common stock should be reported on the

face of the income statement (FN1) when it is materially different in quantitative terms from

(FN1) If a registrant elects to follow the encouraged disclosure discussed in paragraph 23 of

Statement 130, and displays the components of other comprehensive income and the total for

comprehensive income using a one-statement approach, the registrant must continue to follow

ANSWERS TO QUESTIONS

1. The income statement is important because it provides investors and creditors with information

that helps them predict the amount, timing, and uncertainty of future cash flows. It helps investors

and creditors predict future cash flows in a number of different ways. First, investors and creditors can

2. Information on past transactions can be used to identify important trends that, if continued, provide

information about future performance. If a reasonable correlation exists between past and future

3. Some situations in which changes in value are not recorded in income are:

(a) Unrealized gains or losses on available-for-sale investments,

(b) Changes in the fair values of long-term liabilities, such as bonds payable,

4. Some situations in which application of different accounting methods or estimates lead to comparison

problems include:

5. The transaction approach focuses on the activities that have occurred during a given period and

instead of presenting only a net change, a description of the components that comprise the change

Questions Chapter 4 (Continued)

6. Earnings management is often defined as the planned timing of revenues, expenses, gains and

losses to smooth out bumps in earnings. In most cases, earnings management is used to increase

7. Earnings management has a negative effect on the quality of earnings if it distorts the information

in a way that is less useful for predicting future cash flows. Within the Conceptual Framework,

8. Caution should be exercised because many assumptions and estimates are made in accounting

and the net income figure is a reflection of these assumptions. If for any reason the assumptions are

9. The term “quality of earnings” refers to the credibility of the earnings number reported. Companies

that use aggressive accounting policies report higher income numbers in the short-run. In such

10. The major distinction between revenues and gains (or expenses and losses) depends on the

typical activities of the company. Revenues can occur from a variety of different sources, but these

11. The advantages of the single-step income statement are: (1) simplicity and conciseness, (2) probably

better understood by the layperson, (3) emphasis on total costs and expenses, and net income,

and (4) does not imply priority of one revenue or expense over another. The disadvantages are that

12. Operating items are the expenses and revenues which relate directly to the principal activity of the

concern; they are revenues realized from, or expenses which contribute to, the sale of goods or

13. The current operating performance income statement contains only the revenues and usual

expenses of the current year, with all unusual gains or losses or material corrections of prior periods’

Questions Chapter 4 (Continued)

GAAP recommends a modified all-inclusive income statement, excluding from the income statement

14. Items considered corrections of errors should be charged or credited to the opening balance of

retained earnings.

15. (a) This might be shown in the income statement as an extraordinary item if it is a material,

unusual, and infrequent gain realized during the year. However, in general and in accordance

with FASB ASC 225-20 this transaction would normally not be considered extraordinary, but

would be shown in the nonoperating section of a multiple-step income statement. If unusual or

infrequent but not both, it should be separately disclosed in the income statement.

16. (a) The remaining book value of the equipment should be depreciated over the remainder of the

five-year period. The additional depreciation ($425,000) is not a correction of an error and is not

shown as an adjustment to retained earnings. The change is considered a change in estimate.

(b) The loss should be shown as an extraordinary item, assuming that it is unusual and infrequent.

17. (a) Other expenses and losses section or in a separate section, appropriately labeled as an

unusual item, if unusual or infrequent but not both.

(b) Operating expense section or other expenses and losses section or in a separate section,

Questions Chapter 4 (Continued)

(e) Other revenues and gains section or in a separate section, appropriately labeled as an

unusual item, if unusual or infrequent but not both.

18. Perlman and Sheehan should not report the sales in a similar manner. This type of transaction

appears to be typical of Perlman’s central operations. Therefore, Perlman should report revenues of

19. You should tell Greg that a company’s reported net income is the same whether the single-step or

multiple-step format is used. Either way, the company has the same revenues, gains, expenses,

and losses; they are simply organized in a different format.

20. Both formats are acceptable. The amount of detail reported in the income statement is left to the

judgment of the company, whose goal in making this decision should be to present financial

21. Intraperiod tax allocation should not affect the reporting of an unusual gain. The FASB specifically

prohibits a “net–of–tax” treatment for such items to insure that users of financial statements can

22. (a) A loss on discontinued operations is reported net of tax in the income statement between

income from continuing operations and net income.

23. Lebron presents the income information as follows:

Net income

$ 124,700

Less: Net income attributed to

the noncontrolling interest

30,000

Net income attributable to Lebron

Company

$ 94,700

24. Intraperiod tax allocation has no effect on reported net income, although it does affect the amounts

Questions Chapter 4 (Continued)

25. If Neumann has preferred stock outstanding, the numerator in its computation may be incorrect.

A better description of “earnings per share” is “earnings per common share.” The numerator should

26. The earnings per share trend is not favorable. Extraordinary items are one-time occurrences which

are not expected to be reported in the future. Therefore, earnings per share on income before

extraordinary items is more useful because it represents the results of ordinary business activity.

Considering this EPS amount, EPS has decreased from $7.21 to $6.40.

27. Tax allocation within a period is the practice of allocating the income tax for a period to such items

as income before extraordinary items, extraordinary items, and prior period adjustments.

28. Tax allocation within a period (intraperiod) becomes necessary when a firm encounters such items

as discontinued operations, extraordinary items, or corrections of errors. Such allocation is neces–

sary to bring about an appropriate relationship between income tax expense and income from

29.

LISELOTTE COMPANY

Partial Income Statement

For the Year Ended December 31, 2014

Income before tax and extraordinary item ………………………………

$1,500,000

Income tax ………………………………………………………………………..

510,000

Income before extraordinary item …………………………………………

Extraordinary item—gain on sale of plant (condemnation) ………..

Less: Applicable income tax …………………………………………

315,000

30. The damages would probably be reported in Frazier Corporation’s financial statements in the other

expenses and losses section. If the damages are unusual in nature, the damage settlement might be

reported as an unusual item. The damages would not be reported as a correction of an error (prior

period adjustment).

Questions Chapter 4 (Continued)

31. The assets, cash flows, results of operations, and activities of the plants closed would not appear to

32. The major items reported in the retained earnings statement are: (1) adjustments of the beginning

balance for corrections of errors or changes in accounting principle, (2) the net income or loss for

33. Generally accepted accounting principles are ordinarily concerned only with a “fair presentation” of

business income. In contrast, taxable income is a statutory concept which defines the base for

raising tax revenues by the government, and any method of accounting which meets the statutory

definition will “clearly reflect” taxable income as defined by the Internal Revenue Code. It should

be noted that the Code prohibits use of the cash receipts and disbursements method as a method

which will clearly reflect income in accounting for purchases and sales if inventories are involved.

The cash receipts and disbursements method will not usually fairly present income because:

(1) The completed transaction, not receipt or disbursement of cash, increases or diminishes

34. Problems arise both from the revenue side and from the expense side. There sometimes may be

doubt as to the amount of revenue under our common rules of revenue recognition. However, the

more difficult problem is the determination of costs expired in the production of revenue. During

a single fiscal period it often is difficult to determine the expiration of certain costs which may

benefit several periods. Business is continuous and estimates have to be made of the future if we

are to systematically apportion costs to fiscal periods. Examples of items which present serious

obstacles include such items as institutional advertising costs.

Questions Chapter 4 (Continued)

35. Elements are the basic ingredients which comprise the income statement; that is, revenues, gains,

expenses, and losses. Items are descriptions of the elements such as rent revenue, rent expense, etc.

36. Other comprehensive income must be displayed (reported) in one of two ways: (1) a single

continuous income statement or (2) two separate but consecutive statements of net income and

other comprehensive income (two statement approach).

37. The results of continuing operations should be reported separately from discontinued operations,

and any gain or loss from disposal of a component of a business should be reported with the

related results of discontinued operations and not as an extraordinary item. The following format

SOLUTIONS TO BRIEF EXERCISES

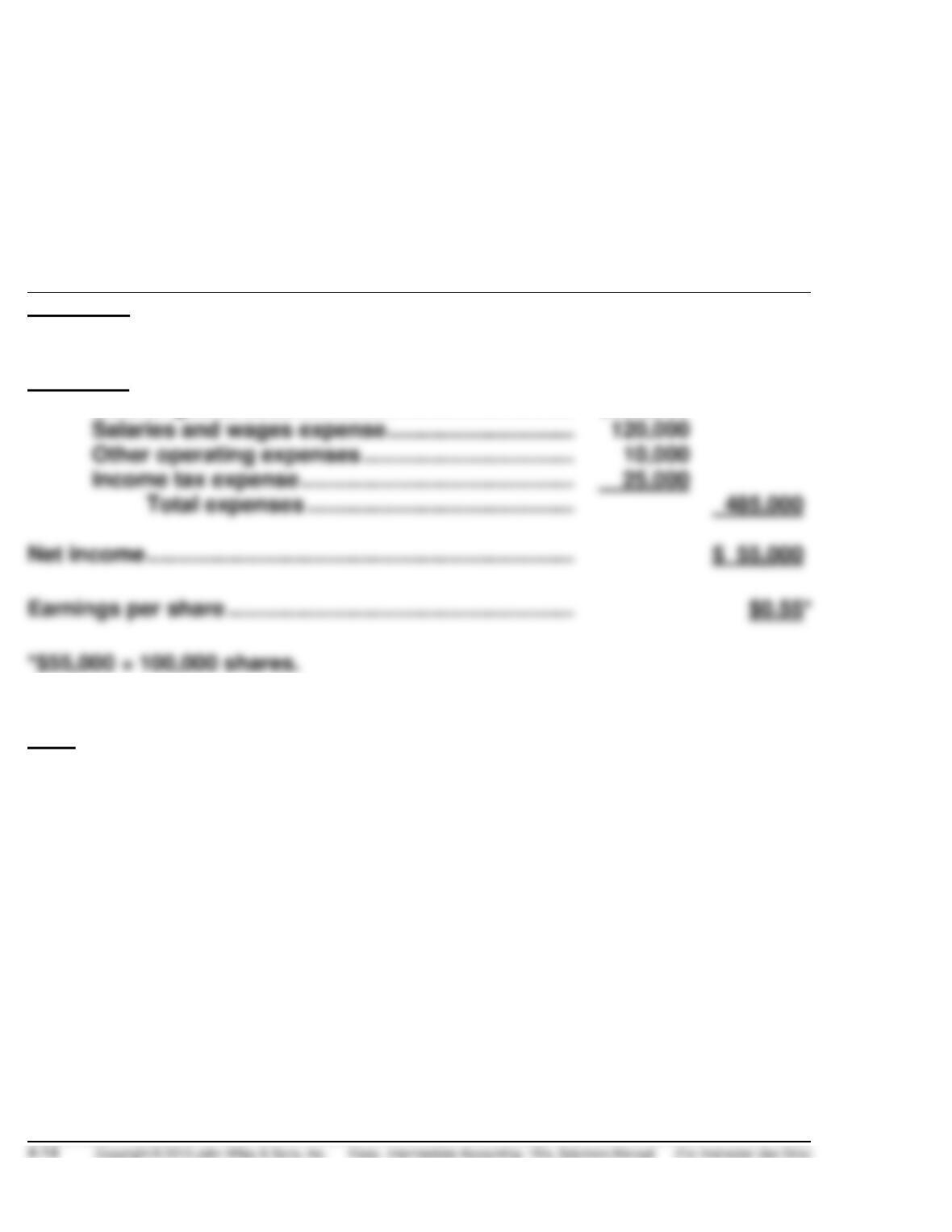

BRIEF EXERCISE 4-1

STARR CO.

Income Statement

For the Year 2014

Revenues

Sales revenue ………………………………………………….

$540,000

Expenses

Cost of goods sold…………………………………………..

$330,000

Salaries and wages expense …………………………..

Other operating expenses ………………………………..

Income tax expense …………………………………………

25,000

Total expenses ………………………………………..

Note: The increase in value of the company reputation and the unrealized

gain on the value of patents are not reported.

BRIEF EXERCISE 4-2

BRISKY CORPORATION

Income Statement

For the Year Ended December 31, 2014

Revenues

Net sales ……………………………………………………….

$2,400,000

Total revenues…………………………………………

Expenses

Cost of goods sold …………………………………………

$1,450,000

Interest expense …………………………………………….

Income tax expense* ………………………………………

133,200

BRIEF EXERCISE 4-3

BRISKY CORPORATION

Income Statement

For the Year Ended December 31, 2014

Net sales ……………………………………………………….

$2,400,000

Cost of goods sold ………………………………………….

1,450,000

Gross profit …………………………………………..

950,000

Selling expenses …………………………………………….

$280,000

Administrative expenses …………………………………

Income from operations …………………………………..

458,000

Other revenue and gains

Other expenses and losses

Interest expense …………………………………….

45,000

Income before income tax …………………………..…..

Income tax expense ………………………………………..

133,200

BRIEF EXERCISE 4-4

Income from continuing operations ……………………..

$10,600,000

Discontinued operations

Earnings per share ……………………………………………..

Discontinued operations, net of tax ……………..

Loss from operation of discontinued

BRIEF EXERCISE 4-5

Income before income tax and extraordinary

item …………………………………………………………………

$6,300,000

Income tax expense …………………………………………….

1,890,000

Less: Applicable income tax ………………………..

Income before extraordinary item …………………

BRIEF EXERCISE 4-6

2014

2013

2012

BRIEF EXERCISE 4-7

Vandross would not report any cumulative effect because a change in estimate

BRIEF EXERCISE 4-8

BRIEF EXERCISE 4-9

PORTMAN CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1 …………………………………….

$ 675,000

BRIEF EXERCISE 4-10

PORTMAN CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2014

Retained earnings, January 1, as reported …………………….

$ 675,000

Retained earnings, January 1, as adjusted ……………………

Less: Cash dividends ………………………………………………….

75,000

Correction for overstatement of expenses in

BRIEF EXERCISE 4-11

(a) Net income (Dividend revenue) ………………………..

$3,000

(b) Net income ……………………………………………………..

$3,000

Unrealized holding gain (net of tax) ………………….

Comprehensive income …………………………………..

$7,000

Unrealized holding gain (net of tax) ………………….

SOLUTIONS TO EXERCISES

EXERCISE 4-1 (18–20 minutes)

Computation of net income

Change in assets:

$79,000 + $45,000 + $127,000 – $47,000 = $204,000 Increase

Change in stockholders’ equity accounted

for as follows:

Net increase

$ 173,000

Increase in common stock

of par

dividend declaration

Net increase accounted for

EXERCISE 4-2 (10–15 minutes)

Sales revenue ……………………………………………………………….

$310,000

Cost of goods sold ………………………………………………………..

Gross profit …………………………………………………………………..

Selling administrative expenses …………………………………….

50,000

120,000

Other revenues and gains

Gain on sale of plant assets …………………………………..

30,000

Income from operations …………………………………………………

150,000(a)

Interest expense ……………………………………………………………

Income from continuing operations ………………………………..

Loss on discontinued operations …………………………………..

Net Income ……………………………………………………………………

Allocation to noncontrolling interest ………………………………

Net income attributable to controlling shareholders ………..

Net income ……………………………………………………………………

$132,000

Unrealized gain on available-for-sale investments …………..

10,000

Comprehensive income …………………………………………………

$142,000(d)

Net income ……………………………………………………………………

$132,000

Dividends …………………………..…………………………………………

12/31/14 Retained earnings ……………………………………………