Continuing Case Solution

Chapter 11

(a)

Memorandum

To: Eric Conner and Phil Martin, CM2

From: L. Harbach

Re: Depreciation and Impairment

Date: January 18, 2013

According to FASB ASC 360-10-35-4:

The cost of a productive facility is one of the costs of the services it renders

during its useful economic life. Generally accepted accounting principles require

The general concept of depreciation is a method of cost allocation, rather than

asset valuation. The definition of depreciation is the process of allocating costs of

tangible assets to an expense in those periods expected to benefit from the use

Continuing Case Solution

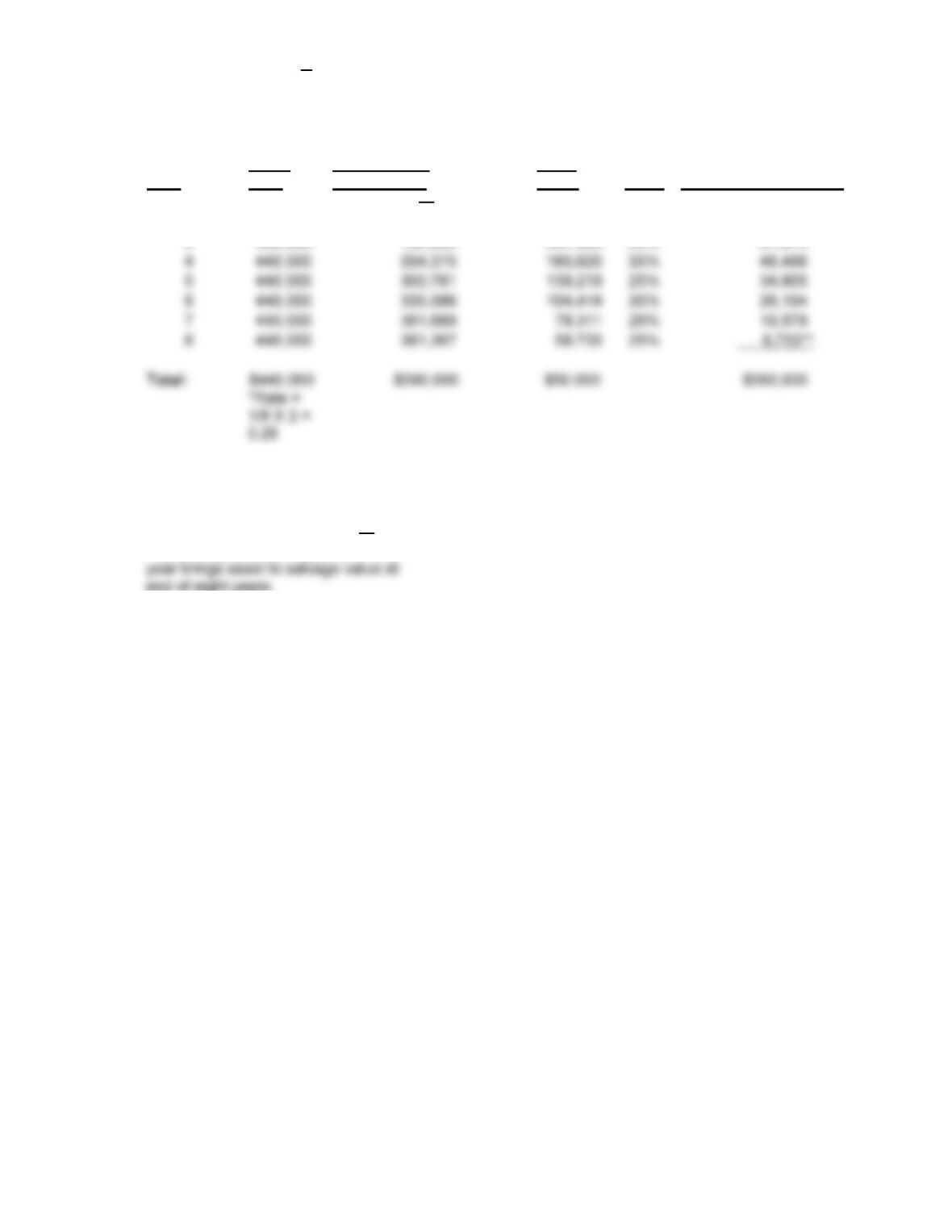

(b) See the table below, excerpted from the spreadsheet.

Year

Asset

Cost

Accumulated

Depreciation

Book

Value Rate*

Depreciation Expense

1 $440,000 $440,000 25% $110,000

2 440,000 $110,000 330,000 25% 82,500

3 440,000 192,500 247,500 25% 61,875

Year 3 Journal Entry:

Depreciation Expense 61,875

Accumulated Depreciation Equipment

61,875

**8,733 depreciation expense in final

Continuing Case Solution

(c) According to FASB ASC 360-10-35-7:

The declining-balance method is an example of one of the methods that meet the

requirements of being systematic and rational. If the expected productivity or

In industries where obsolescence due to the development of new technology is

straight-line depreciation is preferred because the decline in usefulness is simply

One argument for using an accelerated method is that an asset is most

productive and thus generates greater revenue in the early years, and thus the

early years should bear the greatest cost. Another argument for using an

Continuing Case Solution

(d) FASB ASC 360-10- the condition that

exists when the carrying amount of a long-lived asset (asset group) exceeds its

fair value. FASB ASC 360-10-35-21 identifies the following circumstances that

indicate an asset or asset group should be reviewed for impairment:

A significant decrease in the market price of a long-lived asset (asset group)

A significant adverse change in the extent or manner in which a long-lived asset

(asset group) is being used or in its physical condition

To determine if a long-lived asset is impaired, the first step is to estimate the

and eventual disposal. If this amount is less than the carrying value of the asset,

an impairment loss is recognized to write down the asset to its fair value. The

–

impairment net book value. This loss on impairment is reported as a component

Continuing Case Solution

Additional Activities: Extend your accounting knowledge

Memorandum

To: Eric Conner and Phil Martin, CM2

From: L. Harbach

Re: Impairments and Earnings Management

Date: January 18, 2013

There is room for manipulation of income through the recognition of impairments.

A company can incur a large write-off in one year and show an increase in future

Examples of companies with large asset impairments:

In connection with store closings, Blockbuster recorded significant asset impairment

charges of $35.9 million and $20.4 million on its property and equipment in fiscal

In the Altria Group, Inc. 2004 Annual Report it was reported that during 2004, Kraft

recorded $603 million of asset impairment and exit costs on the consolidated

statement of earnings. These pre-tax charges were composed of $583 million of costs

under the restructuring program, $12 million of impairment charges relating to

In its third quarter, 2003, Eastman Chemical Company recorded a total of $496

million in charges against its bottom line. Of that, $482 million consisted of non-cash

asset impairments, representing a decline in value of the company’s capital and

intangible assets. “The non-cash asset impairments of $482 million for third quarter

reflect adjustments to the company’s balance sheet and do not represent cash leaving

Continuing Case Solution

the company,” said Eastman spokeswoman Nancy Ledford. (Source: www.sullivan-