PROBLEM 21-3 (Continued)

(e) WINSTON INDUSTRIES

Lease Amortization Schedule

Date

Annual

Lease

Receipt/

Payment

Interest on

Receivable/

Liability at 8%

Reduction in

Receivable/

Liability

Lease

Receivable/

Liability

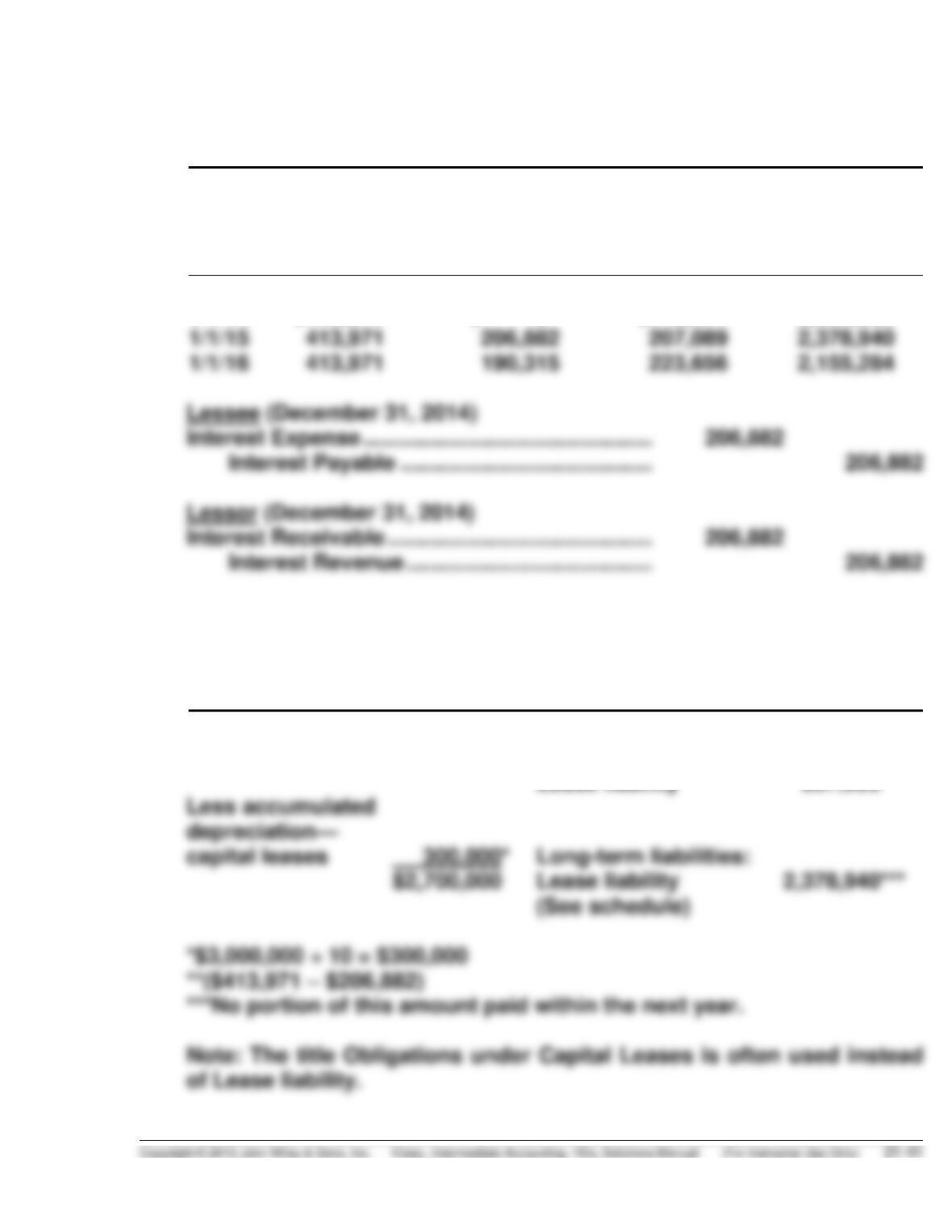

1/1/14

$3,000,000

1/1/14

$413,971

$ –0–

$413,971

2,586,029

1/1/15

2,378,940

(f) WINSTON INDUSTRIES

Balance Sheet (Partial)

December 31, 2014

Property, plant, and equipment:

Current liabilities:

Leased property

$3,000,000

Interest payable

$ 206,882

Lease liability

207,089**

PROBLEM 21-3 (Continued)

EWING INC.

Balance Sheet (Partial)

December 31, 2014

Assets

Current assets:

Interest receivable……………………………………………… $ 206,882

PROBLEM 21-4

(a) 1. $ 23,768 Interest expense (See amortization schedule)

$ 5,500 Lease executory expense

$ 50,064 Depreciation expense ($300,383 ÷ 6 = $50,064)

2. Current liabilities:

$ 38,932 Lease liability

3. $ 19,875 Interest expense (See amortization schedule)

4. Current liabilities:

$ 42,825 Lease liability

$ 19,875 Interest payable

Long-term liabilities:

$155,926 Lease liability

PROBLEM 21-4 (Continued)

2. Current liabilities:

$ 38,932 Lease liability

$ 5,942 Interest payable

3. $ 22,795 Interest expense

[($23,768 – $5,942) + ($19,875 X 3/12) =

4. Current liabilities:

$ 42,825 Lease liability

$ 4,969 Interest payable ($19,875 X 3/12 = $4,969)

PROBLEM 21-5

(a) 1. $ 23,768 Interest revenue

2. Current assets:

Lease receivable $38,932

Interest receivable $23,768

(b) 1. $ 5,942 Interest revenue ($23,768 X 3/12 = $5,942)

2. Current assets:

Lease receivable $38,932

PROBLEM 21-6

Note: This lease is a capital lease to the lessee because the lease term

(six years) exceeds 75% of the remaining economic life of the asset (six years).

Also, the present value of the minimum lease payments exceeds 90% of the

fair value of the asset.

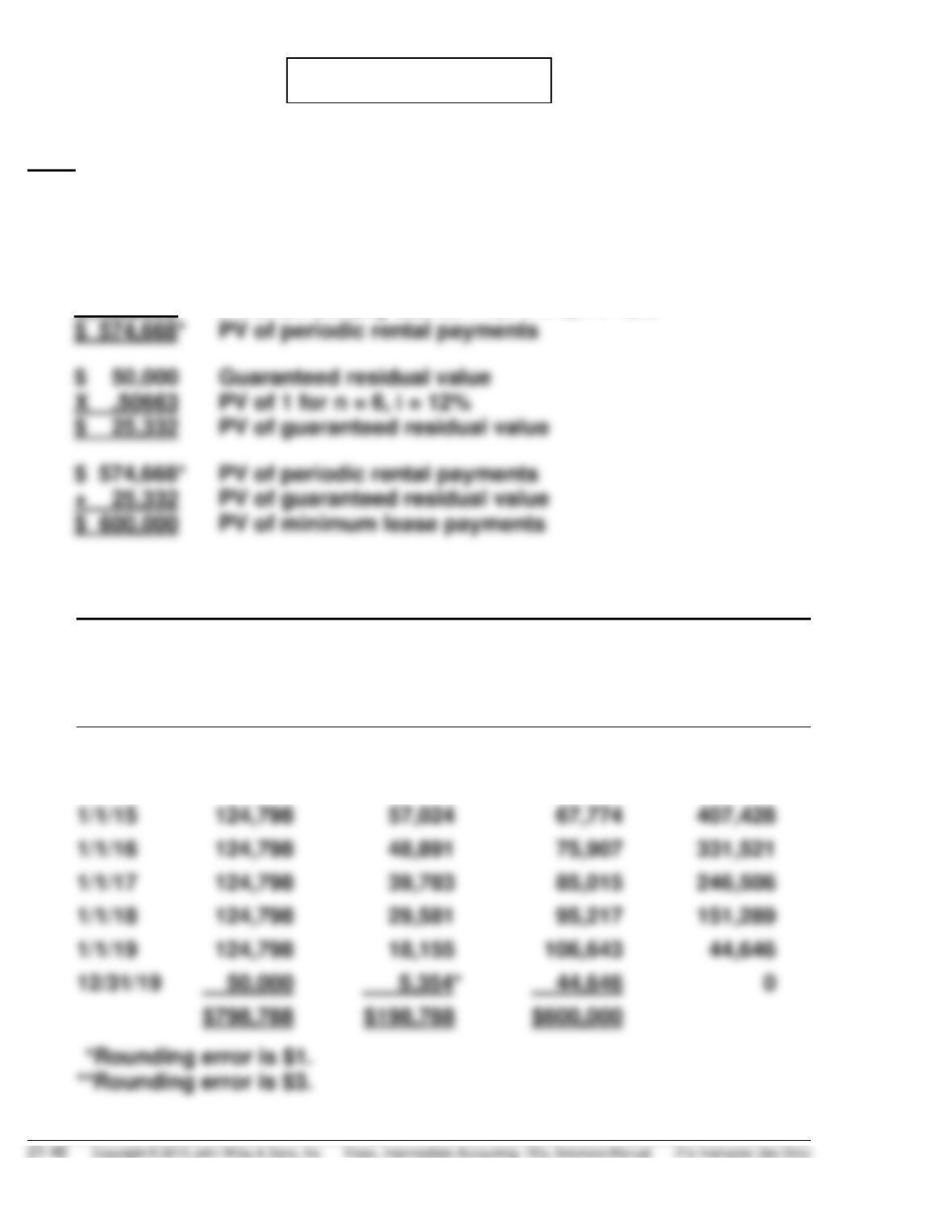

$ 124,798 Annual rental payment

X 4.60478 PV of an annuity-due of 1 for n = 6, i = 12%

(a) VANCE COMPANY (Lessee)

Lease Amortization Schedule

Date

Annual

Lease

Payment

Plus GRV

Interest (12%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/14

$600,000

1/1/14

$124,798

$ –0–

$124,798

475,202

1/1/16

124,798

331,521

1/1/17

124,798

246,506

1/1/18

124,798

151,289

1/1/19

124,798

12/31/19

50,000

44,646

PROBLEM 21-6 (Continued)

(b) January 1, 2014

Leased Equipment ………………………………………….. 600,000

Lease Liability ………………………………………….. 600,000

Depreciation Expense …………………………………….. 91,667

Accumulated Depreciation—Capital

Leases ([$600,000 – $50,000] ÷ 6) …………… 91,667

January 1, 2015

Interest Payable ……………………………………………… 57,024

Interest Expense ………………………………………. 57,024

Depreciation Expense …………………………………….. 91,667

Accumulated Depreciation—Capital

Leases …………………………………………………. 91,667

PROBLEM 21-6 (Continued)

(Note to instructor: The guaranteed residual value was subtracted for

purposes of determining the depreciable base. The reason is that at

PROBLEM 21-7

(a) December 31, 2014

Leased Equipment ………………………………………….. 166,794

Lease Liability ………………………………………….. 166,794

(b) December 31, 2015

Depreciation Expense …………………………………….. 23,828

Accumulated Depreciation—Capital

December 31, 2015

Interest Expense …………………………………………….. 12,679

Lease Liability ………………………………………………… 27,321

PROBLEM 21-7 (Continued)

LUDWICK STEEL COMPANY (Lessee)

Lease Amortization Schedule

(Annuity Due Basis)

Date

Annual

Lease

Payment

Interest (10%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

12/31/14

—

—

—

$166,794

12/31/14

$40,000

$ 0

$40,000

126,794

12/31/16

12/31/17

12/31/18

(c) December 31, 2016

Depreciation Expense ………………………………………. 23,828

Accumulated Depreciation—Capital

PROBLEM 21-7 (Continued)

(d) LUDWICK STEEL COMPANY

Balance Sheet (Partial)

December 31, 2016

Property, plant, and equipment:

Current liabilities:

PROBLEM 21-8

(a) The $550,000 is the present value of the five annual lease payments of

$137,899 less the $6,000 attributable to the payment for taxes, insurance,

and maintenance. In other words, it is the present value of five $131,899

(b) Leased Equipment …………………………………………. 550,000

Lease Liability …………………………………………. 550,000

(c) Depreciation Expense ……………………………………. 220,000

(d) Interest Expense ……………………………………………. 41,810

Interest Payable ………………………………………. 41,810

(See amortization schedule)

(e) Executory Costs ……………………………………………. 6,000

PROBLEM 21-8 (Continued)

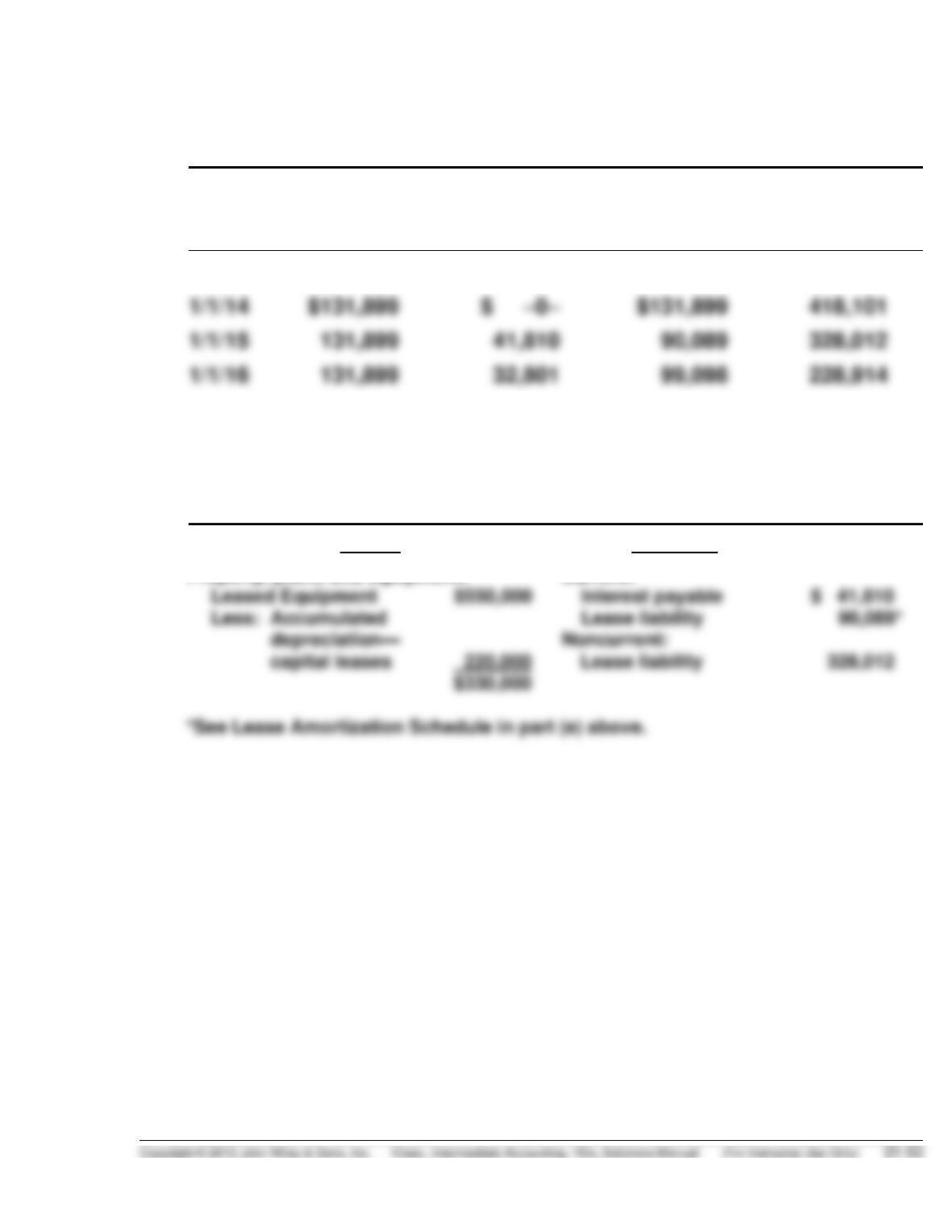

CAGE COMPANY (Lessee)

Lease Amortization Schedule

Date

Annual

Lease

Payment

Interest (10%)

on Liability

Reduction

of Lease

Liability

Lease

Liability

1/1/14

$550,000

1/1/14

$131,899

418,101

1/1/16

228,914

(f) CAGE COMPANY

Balance Sheet (Partial)

December 31, 2014

Assets

Liabilities

Property, plant, and equipment:

Current:

Noncurrent:

PROBLEM 21-9

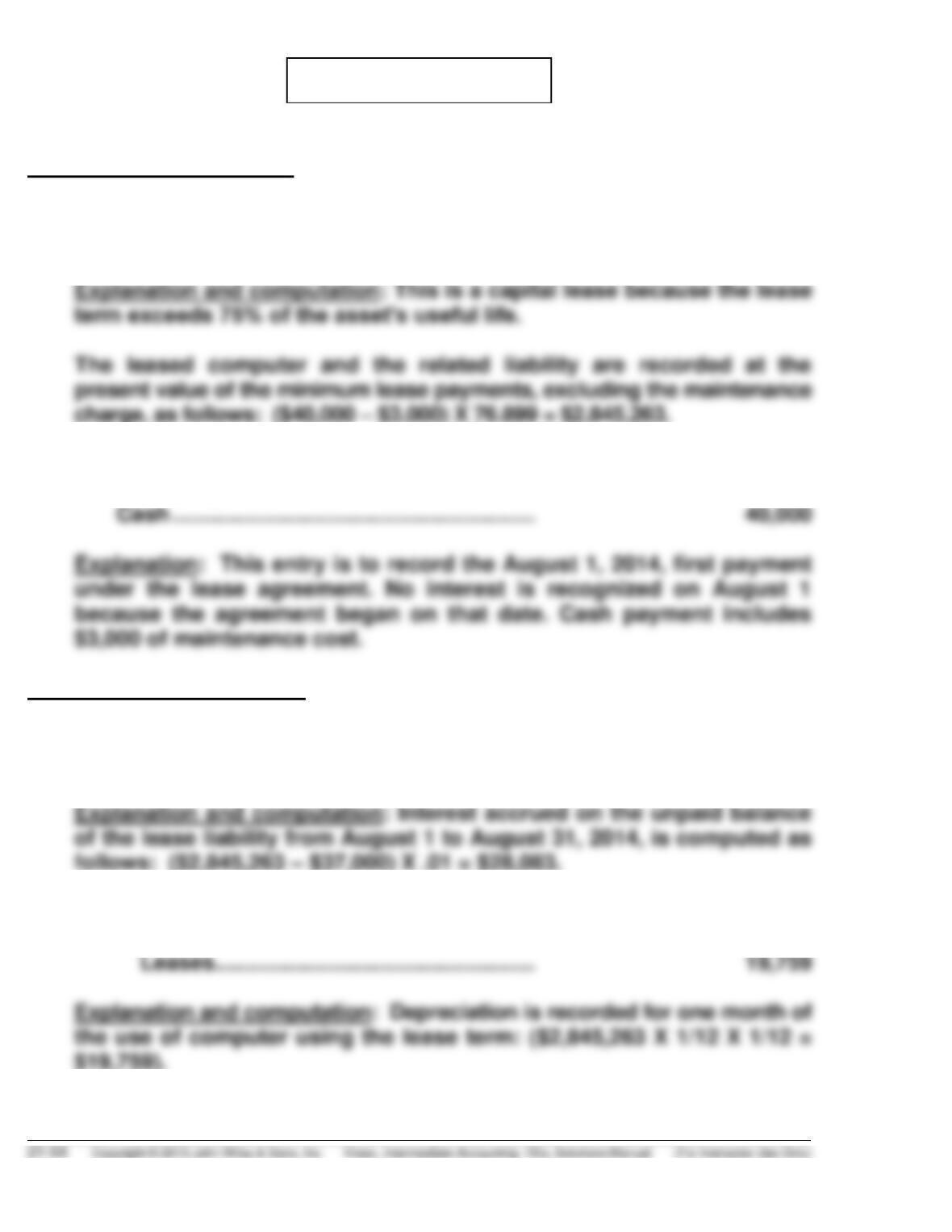

Entries on August 1, 2014:

(1) Leased Equipment ……………………………………… 2,845,263

Lease Liability ……………………………………… 2,845,263

(2) Maintenance and Repairs Expense ……………. 3,000

Lease Liability ………………………………………….. 37,000

Entries on August 31, 2014:

(1) Interest Expense ………………………………………. 28,083

Interest Payable …………………………………. 28,083

(2) Depreciation Expense ………………………………. 19,759

Accumulated Depreciation—Capital

PROBLEM 21-10

(a) The lease is a sales-type lease because: (1) the lease term exceeds

75% of the asset’s estimated economic life, (2) collectibility of payments

is reasonably assured and there are no further costs to be incurred,

and (3) George Company realized an element of profit aside from the

financing charge.

1. Present value of an annuity due of $1 for

10 periods discounted at 10% ……………………………… 6.75902

2. Sales price is $270,361 (the present value of the 10 annual lease

payments); or, the initial PV of $278,072 minus the PV of the un–

PROBLEM 21-10 (Continued)

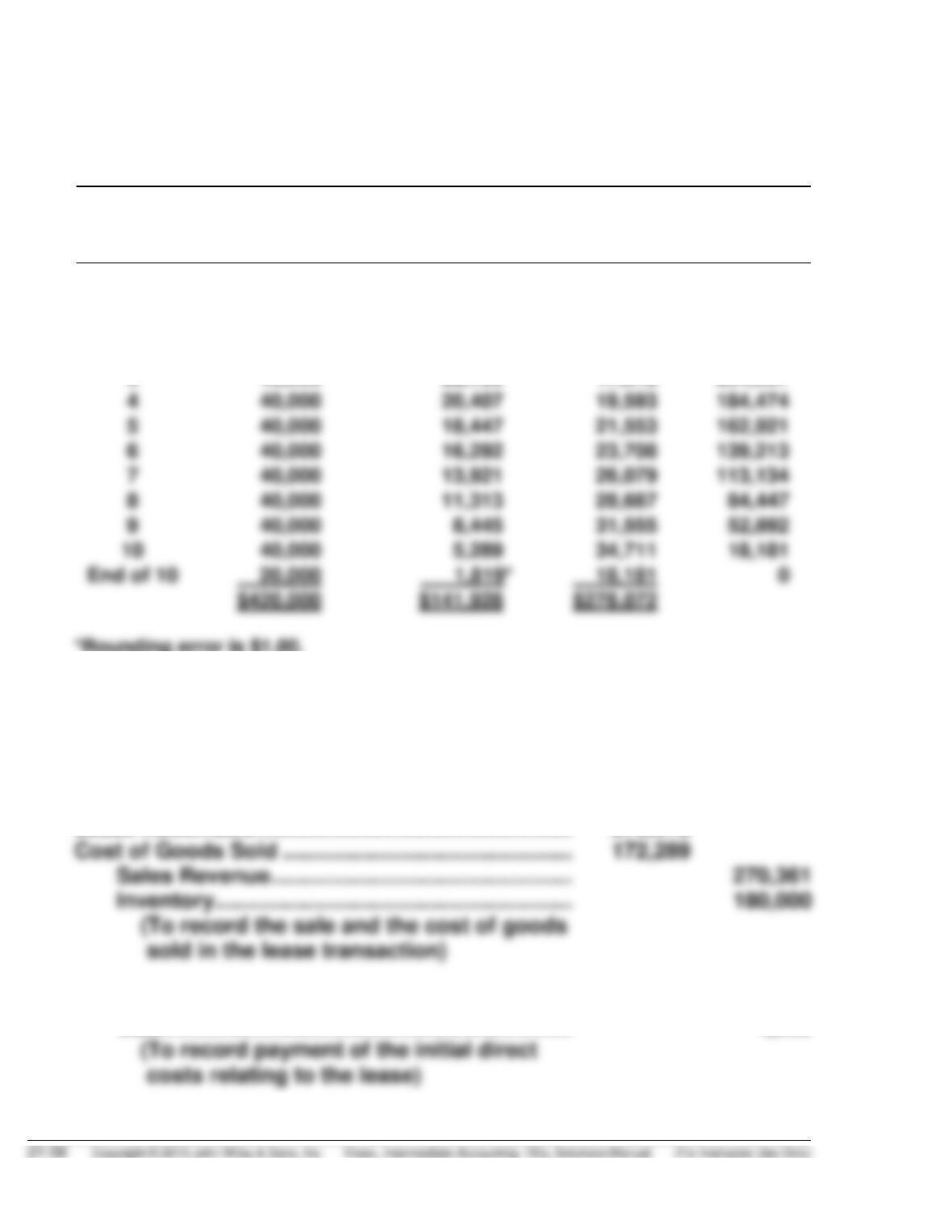

(b) GEORGE COMPANY (Lessor)

Lease Amortization Schedule

Annuity Due Basis, Unguaranteed Residual Value

Beginning

of Year

Annual Lease

Payment Plus

Residual Value

Interest (10%)

on Lease

Receivable

Lease

Receivable

Recovery

Lease

Receivable

(a)

(b)

(c)

(d)

Initial PV

$ 0

$ 0

$ 0

$278,072

1

40,000

0

40,000

238,072

2

40,000

23,807

16,193

221,879

3

40,000

22,188

17,812

204,067

4

184,474

5

40,000

18,447

21,553

162,921

6

40,000

16,292

23,708

139,213

7

113,134

8

40,000

11,313

28,687

9

40,000

31,555

*Rounding error is $1.00.

(a) Annual lease payment required by lease contract.

(b) Preceding balance of (d) X 10%, except beginning of first year of lease term.

(c) (a) minus (b).

(d) Preceding balance minus (c).

(c) Beginning of the Year

Lease Receivable …………………………………………… 278,072

Selling Expenses …………………………………………… 4,000

Cash ……………………………………………………….. 4,000

PROBLEM 21-10 (Continued)

Cash …………………………………………………………………. 40,000

Lease Receivable ………………………………………… 40,000

PROBLEM 21-11

(a) The lease is a capital lease because: (1) the lease term exceeds 75% of

the asset’s economic life and (2) the present value of the minimum

lease payments exceeds 90% of the fair value of the leased asset.

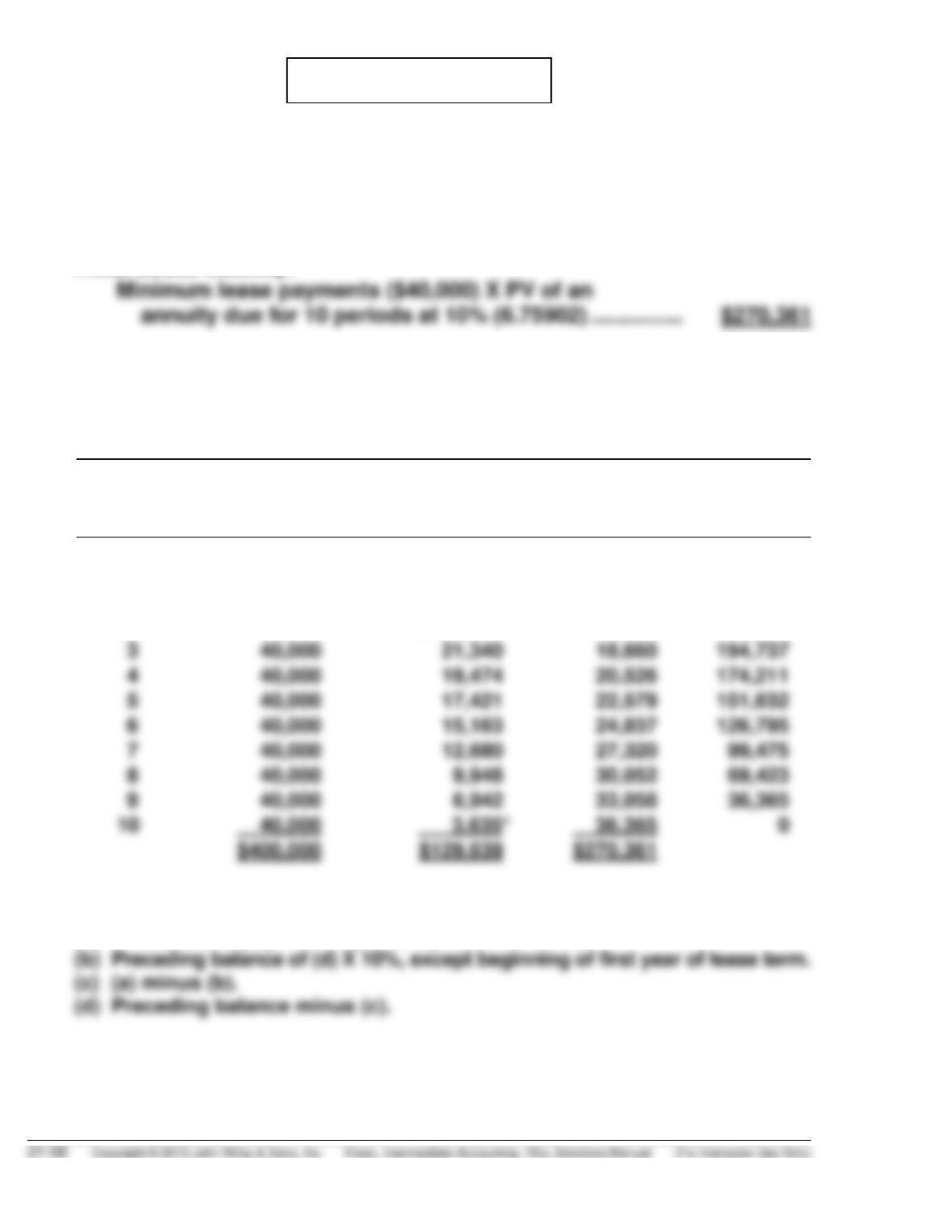

Initial Lease Liability:

(b) NATIONAL AIRLINES (Lessee)

Lease Amortization Schedule

(Annuity-due basis and URV)

Beginning

of Year

Annual Lease

Payment

Interest (10%)

on Lease

Liability

Reduction

of Lease

Liability

Lease

Liability

(a)

(b)

(c)

(d)

Initial PV

—

—

—

$270,361

1

$ 40,000

—

$ 40,000

230,361

2

40,000

$ 23,036

16,964

213,397

3

40,000

18,660

194,737

4

174,211

5

40,000

22,579

151,632

6

40,000

24,837

126,795

7

8

40,000

30,052

9

40,000

33,058

$129,639

*Rounding error is $1.

(a) Annual lease payment required by lease contract.

PROBLEM 21-11 (Continued)

(c) Lessee’s journal entries:

Beginning of the Year

Leased Equipment ………………………………………….. 270,361

End of the Year

Interest Expense …………………………………………….. 23,036

Interest Payable ……………………………………….. 23,036

PROBLEM 21-12

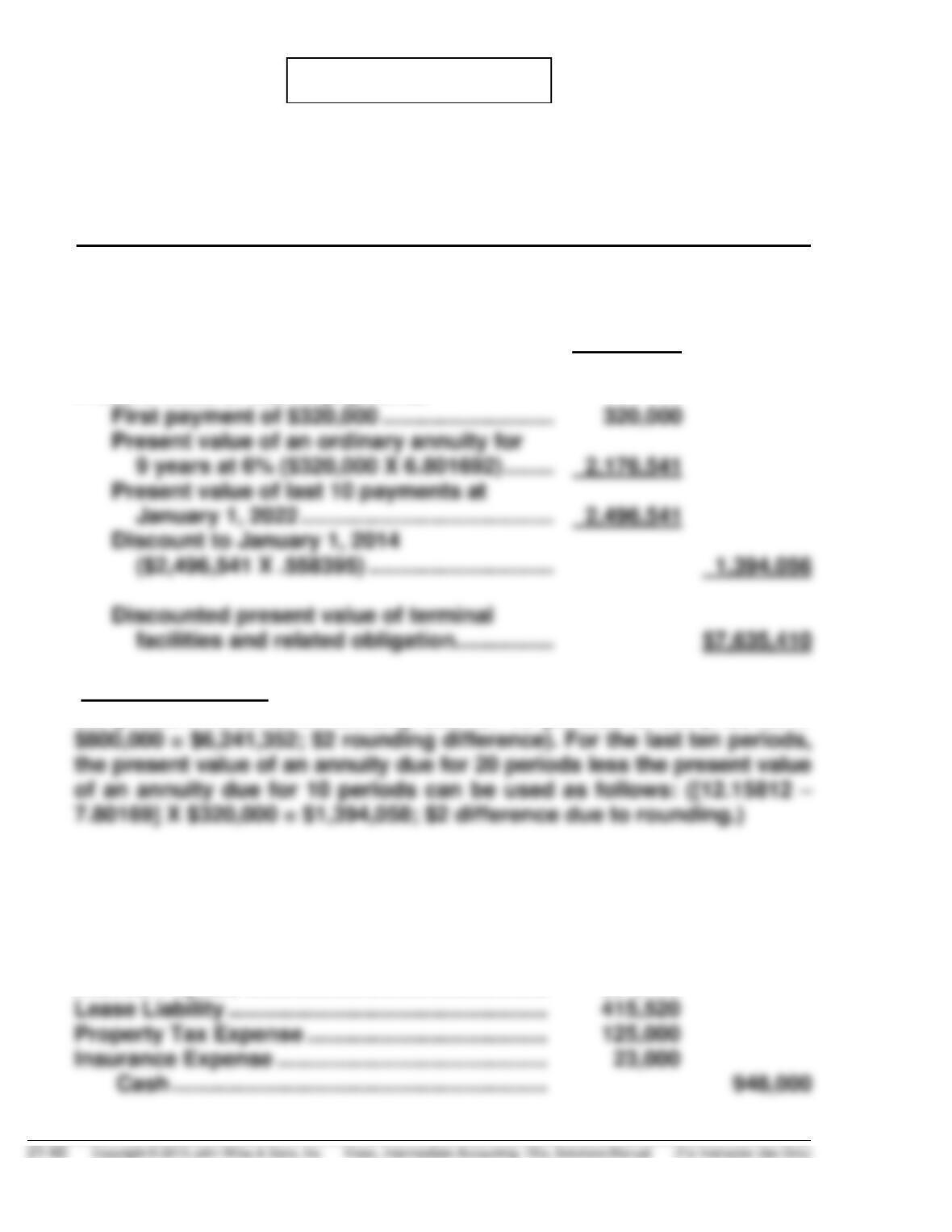

(a) GRISHELL TRUCKING COMPANY

Schedule to Compute the Discounted Present Value

of Terminal Facilities and the Related Obligation

January 1, 2014

Present value of first 10 payments:

Immediate payment ……………………………….. $ 800,000

Present value of an ordinary annuity for

9 years at 6% ($800,000 X 6.801692) …….. 5,441,354 $6,241,354

Present value of last 10 payments:

(Note to instructor: The student can compute the $6,241,354 by using

the present value of an annuity due for 10 periods at 6% (7.80169 X

(b) GRISHELL TRUCKING COMPANY

Journal Entries

2016

(1/1/16)

Interest Payable …………………………………………. 384,480